Trump says Nvidia not allowed to sell advanced AI chips to China- 60 Minutes

Introduction & Market Context

Chevron Corporation (NYSE:CVX) released its third-quarter 2025 earnings presentation on October 31, revealing a 42% sequential increase in earnings despite year-over-year declines. The oil giant reported adjusted earnings of $1.85 per share, exceeding analyst expectations of $1.75. Following the announcement, Chevron’s stock rose 2.39% to $157.19, building on a 1.14% gain in pre-market trading.

The company’s performance comes amid a challenging commodity price environment, with Brent crude prices averaging $69 per barrel in Q3 2025, down from $80 in the same period last year but slightly up from $68 in Q2 2025.

Quarterly Performance Highlights

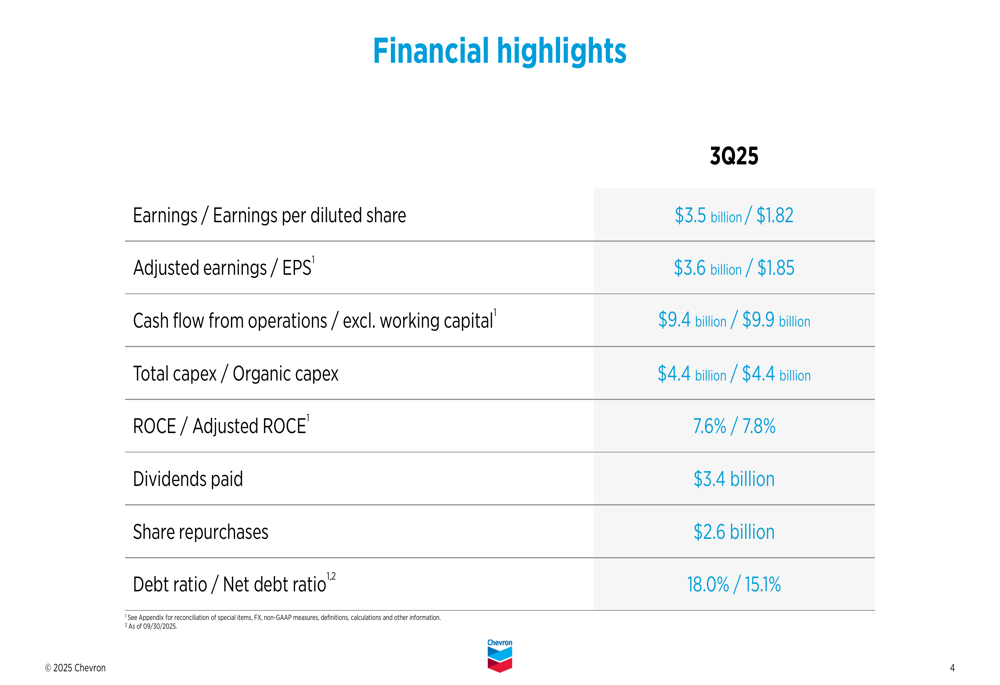

Chevron reported earnings of $3.5 billion ($1.82 per diluted share) for the third quarter of 2025, compared to $2.49 billion in Q2 2025 and $4.49 billion in Q3 2024. On an adjusted basis, earnings were $3.6 billion ($1.85 per diluted share), beating market expectations.

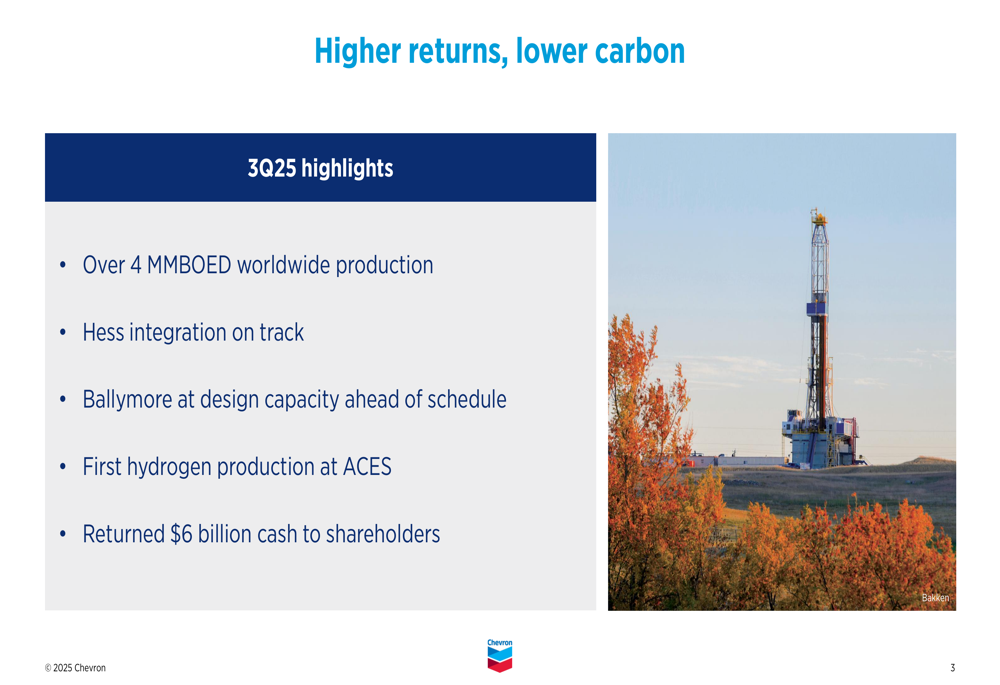

The company highlighted several operational achievements during the quarter, including worldwide production exceeding 4 million barrels of oil equivalent per day (MMBOED), progress on the Hess integration, and the Ballymore project reaching design capacity ahead of schedule.

Cash flow from operations reached $9.4 billion, or $9.9 billion excluding working capital effects. The company maintained its commitment to shareholder returns, distributing $6 billion through dividends and share repurchases.

Production Growth Analysis

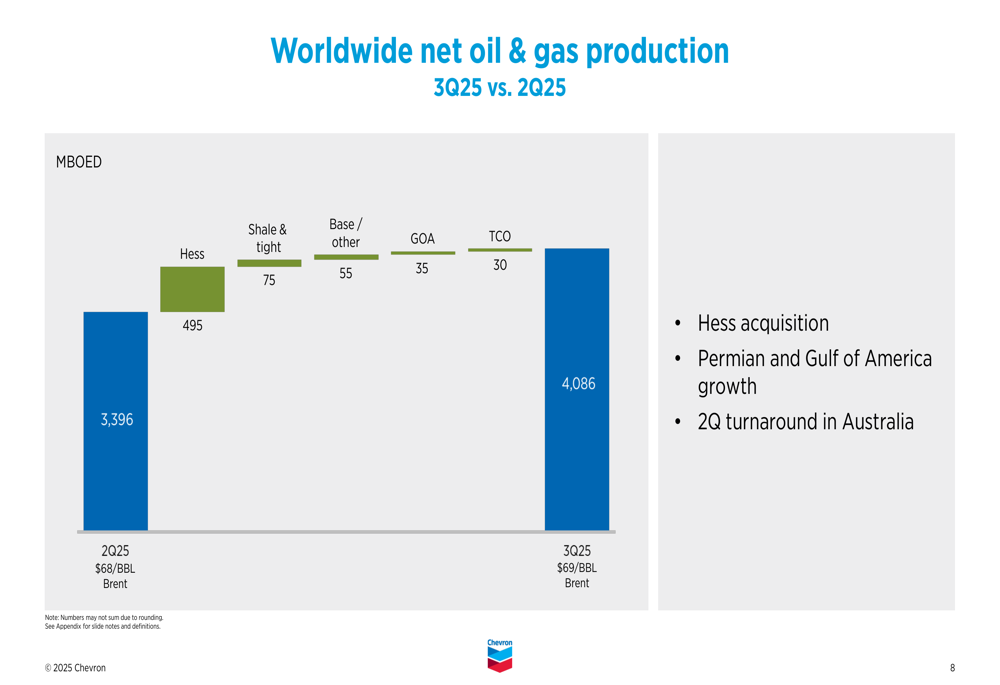

Chevron’s worldwide net oil and gas production increased significantly to 4,086 MBOED in Q3 2025, up 20.3% from 3,396 MBOED in Q2 2025. This substantial growth was primarily driven by the Hess acquisition, which contributed 495 MBOED. Other growth factors included increases in shale and tight oil production (+75 MBOED), base production and other sources (+55 MBOED), Gulf of America operations (+35 MBOED), and TCO (+30 MBOED).

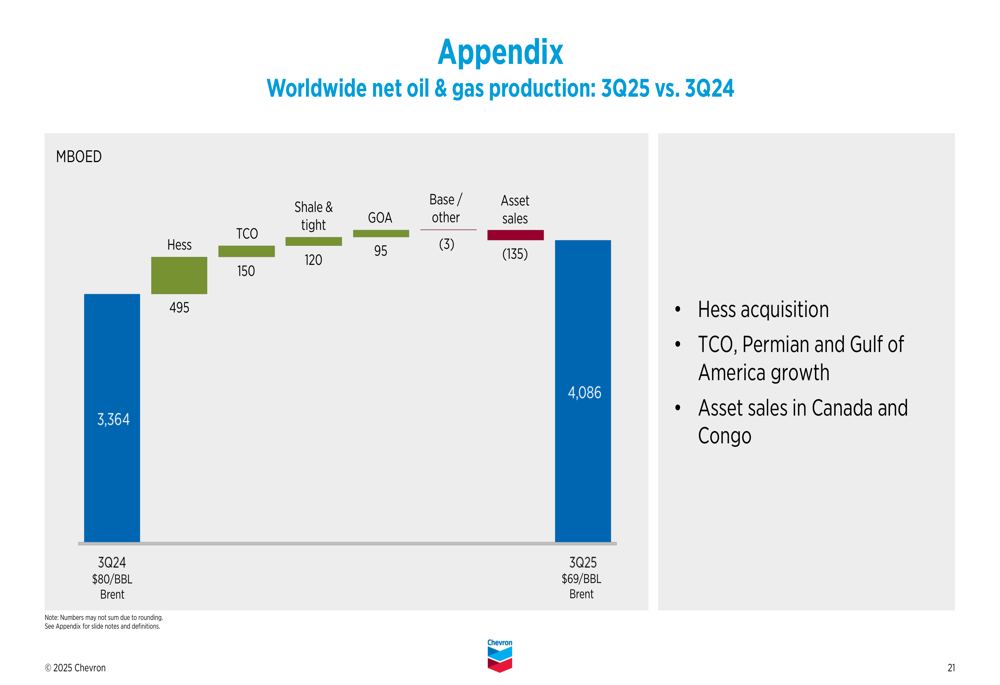

Year-over-year production growth was even more pronounced, with Q3 2025 production up 21.5% from 3,364 MBOED in Q3 2024. Besides the Hess acquisition (+495 MBOED), significant contributions came from TCO (+150 MBOED), shale and tight oil (+120 MBOED), and Gulf of America operations (+95 MBOED). These gains were partially offset by asset sales in Canada and Congo (-135 MBOED).

Financial Results Deep Dive

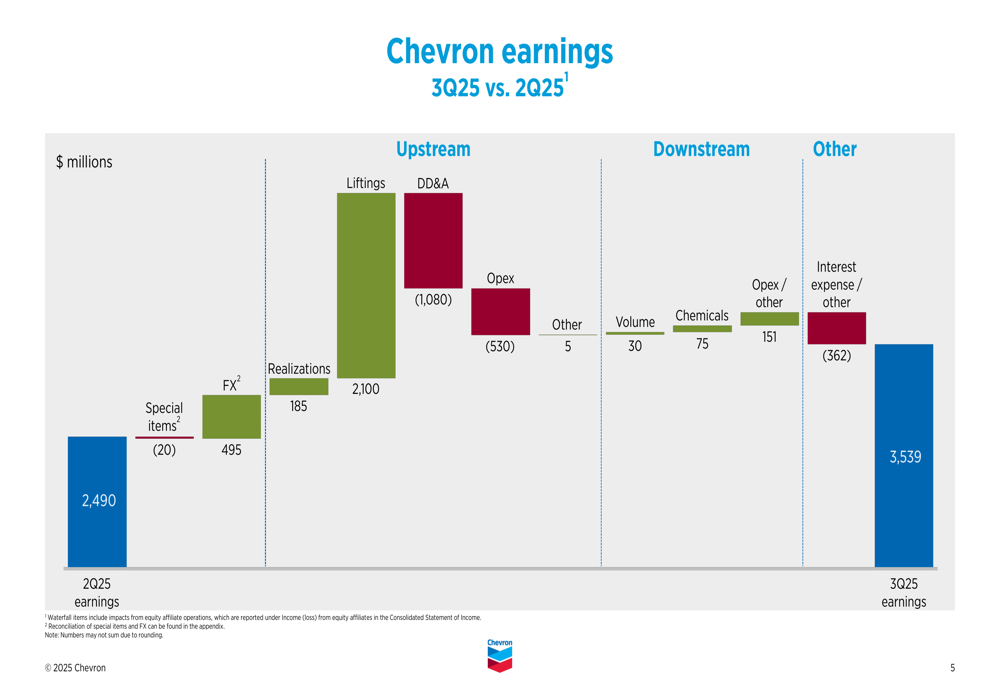

The sequential improvement in Chevron’s earnings from Q2 2025 to Q3 2025 was driven by several factors. As illustrated in the company’s waterfall chart, the $1.05 billion increase in earnings was primarily due to higher liftings (+$2.1 billion) and favorable foreign exchange impacts (+$495 million). These gains were partially offset by increased depreciation, depletion, and amortization expenses (-$1.08 billion) and higher operating expenses (-$530 million).

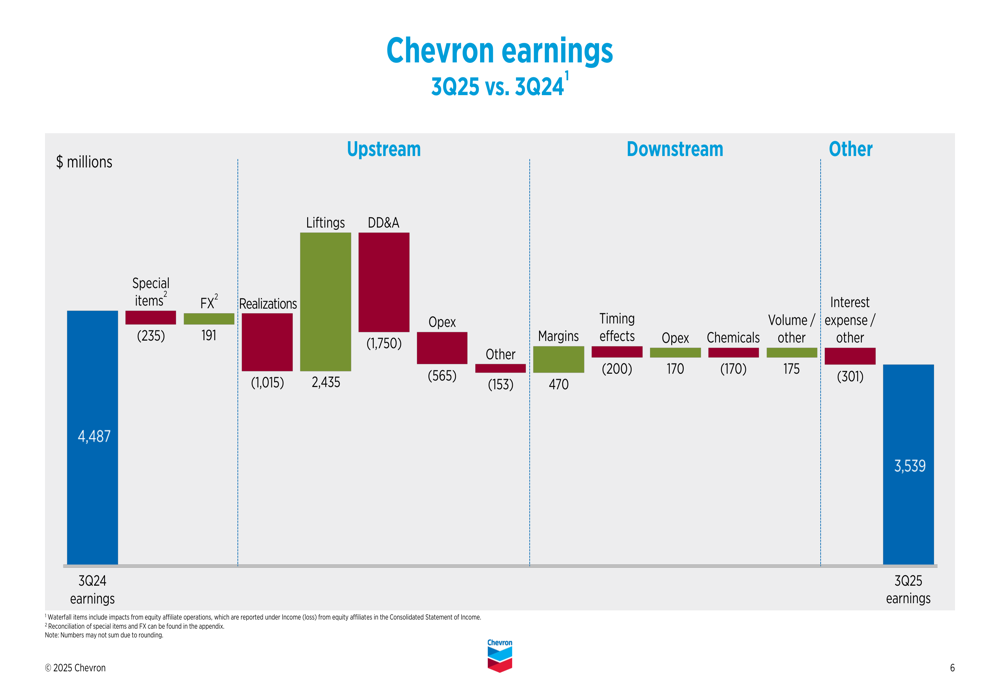

Year-over-year comparisons show a different picture, with Q3 2025 earnings down $948 million from Q3 2024. This decline was primarily due to lower realizations (-$1.02 billion), higher DD&A (-$1.75 billion), and increased operating expenses (-$565 million), partially offset by higher liftings (+$2.44 billion).

Cash Flow and Shareholder Returns

Chevron demonstrated strong cash generation in Q3 2025, with adjusted free cash flow of $7 billion. The company’s cash balance increased from $4.1 billion at the end of Q2 2025 to $7.7 billion at the end of Q3 2025. This improvement was driven by adjusted free cash flow, asset sales and equity affiliate loans (+$1.5 billion), debt issuance (+$2.1 billion), and Hess cash acquired (+$1.1 billion), partially offset by capital expenditures (-$4.4 billion), dividends (-$3.4 billion), share repurchases (-$2.6 billion), and working capital and other items (-$0.4 billion).

The company maintained its commitment to shareholder returns, distributing $6 billion in Q3 2025 through dividends ($3.4 billion) and share repurchases ($2.6 billion). Chevron’s financial position remains solid, with a debt ratio of 18.0% and a net debt ratio of 15.1%.

Forward Guidance and Outlook

Looking ahead to Q4 2025, Chevron expects upstream turnarounds and downtime to impact production by approximately 125 MBOED. In the downstream segment, turnarounds and downtime are expected to affect earnings by $400-500 million. The company anticipates affiliate dividends of $0.8-0.9 billion, share repurchases of $2.5-3.0 billion, and "All Other" segment earnings of $(0.9)-(1.1) billion.

Chevron will hold its Investor Day on November 12, 2025, where it plans to provide a more comprehensive outlook through 2030. The event will be an opportunity for the company to outline its strategy for balancing traditional energy operations with lower-carbon initiatives, as highlighted by its first hydrogen production at ACES during Q3.

CEO Mike Wirth emphasized the importance of affordable and reliable energy in his comments, stating, "Affordable and reliable energy is the lifeblood of a modern economy." He also highlighted Chevron’s ongoing efficiency and productivity improvements, particularly in its fleet operations.

With production now exceeding 4 MMBOED and a strengthened cash position, Chevron appears well-positioned to navigate the evolving energy landscape while continuing to deliver returns to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.