Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Ciena Corporation (NYSE:CIEN) presented its fiscal second-quarter 2025 earnings results on June 5, revealing strong revenue growth amid its strategic shift toward cloud providers and non-telecommunications customers. Despite reporting significant improvements across multiple financial metrics, Ciena’s stock fell 7.59% in premarket trading to $77.52, suggesting investor concerns about gross margin pressure and broader market conditions.

The networking equipment provider reported Q2 revenue of $1.13 billion, representing a 23.6% year-over-year increase, as the company continues to benefit from growing bandwidth demands and the emerging AI-driven infrastructure build-out.

Quarterly Performance Highlights

Ciena delivered substantial financial improvements in its second quarter ended May 3, 2025. Revenue reached $1.13 billion, compared to $910.8 million in the same period last year. The company’s adjusted earnings per share rose to $0.42, up 55.6% from $0.27 in Q2 2024, while adjusted EBITDA increased 36% to $116.7 million.

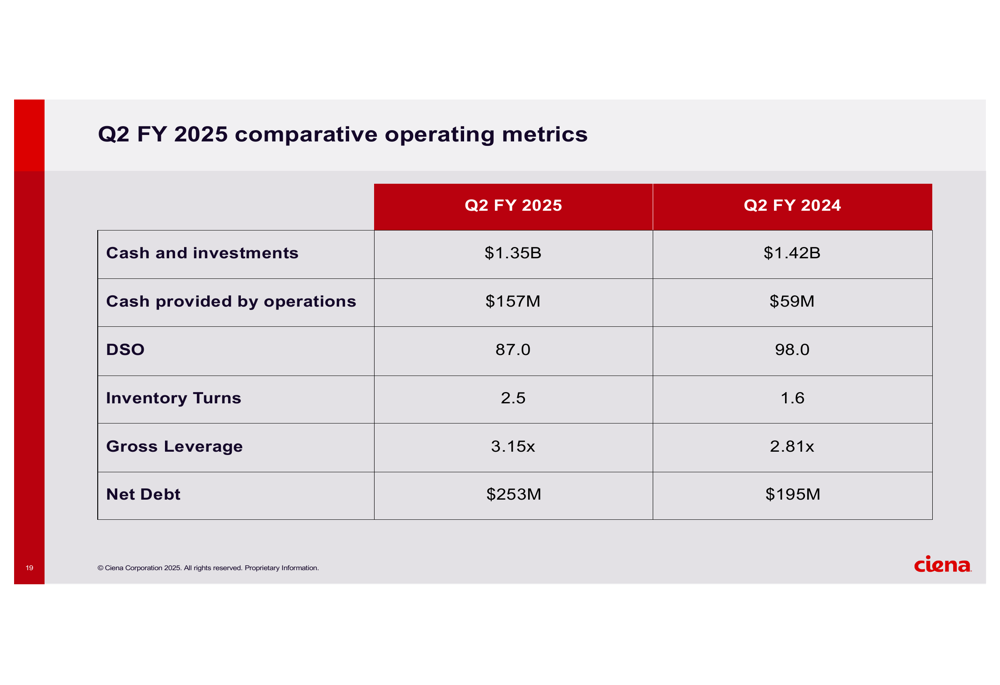

As shown in the following comparative financial highlights:

While revenue and profitability metrics improved significantly, adjusted gross margin declined to 41.0% from 43.5% in the prior-year period. This margin compression likely contributed to investor concerns, despite the company’s improved adjusted operating margin of 8.2%, up from 6.8% a year earlier.

Operational metrics also showed notable improvements, with days sales outstanding (DSO) decreasing to 87 days from 98 days, and inventory turns increasing to 2.5 from 1.6 in the prior-year quarter, indicating better working capital management.

Detailed Financial Analysis

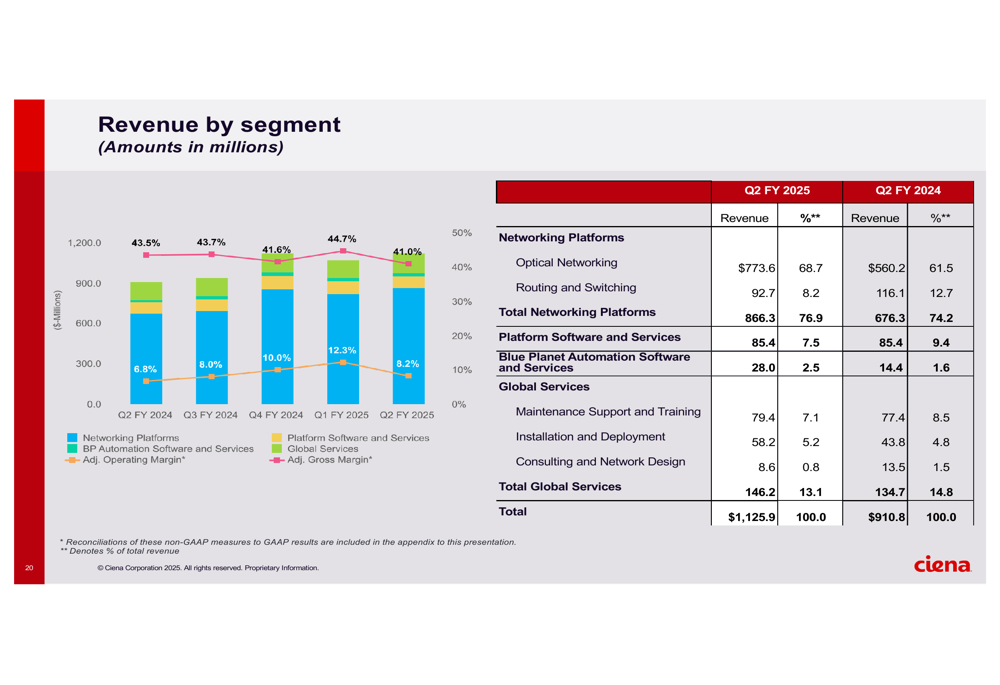

Ciena’s revenue growth was primarily driven by its Optical Networking segment, which surged to $773.6 million from $560.2 million in the year-ago period. This 38.1% increase reflects strong demand for the company’s WaveLogic optical technology, particularly from cloud providers building out AI infrastructure. Conversely, the Routing and Switching segment saw a decline to $92.7 million from $116.1 million.

The company’s Blue Planet Automation Software (ETR:SOWGn) and Services segment nearly doubled its revenue to $28.0 million from $14.4 million, while Global Services revenue increased modestly to $146.2 million from $134.7 million.

As illustrated in the following segment breakdown:

Strategic Initiatives

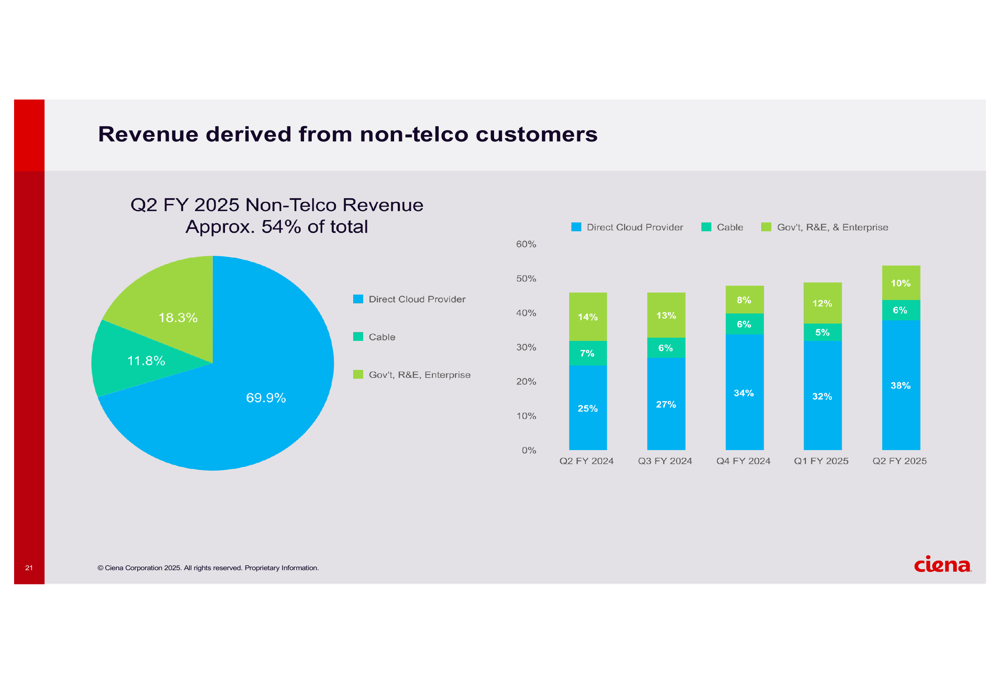

A key element of Ciena’s strategy is diversifying its customer base beyond traditional telecommunications providers. In Q2, non-telco customers accounted for 54% of total revenue, with direct cloud provider revenue growing 85% year-over-year to represent 38% of total revenue.

The following chart illustrates this strategic shift:

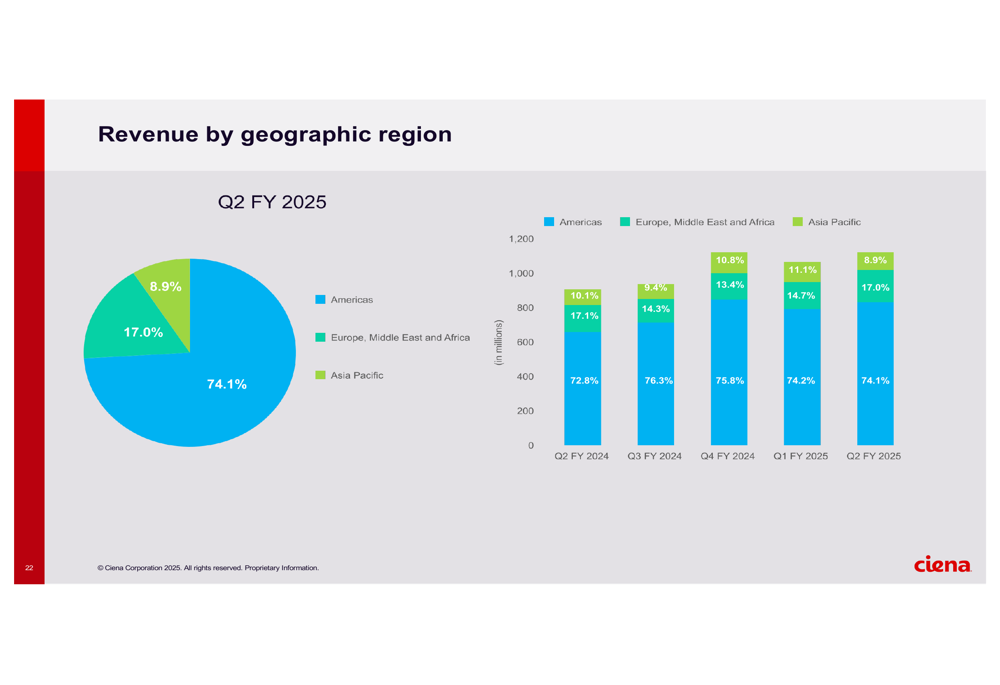

Geographically, the Americas remained Ciena’s largest market at 74.1% of revenue, while Europe, Middle East and Africa (EMEA) contributed 17.0% after growing 23% year-over-year. Asia Pacific accounted for 8.9% of revenue.

Ciena highlighted several key achievements during the quarter, including adding 24 new customers for its WaveLogic 6 Extreme technology, bringing the total to 49 within just two quarters of availability. The company also expanded its customer base for broadband solutions, adding 8 additional customers for a total of 87.

Market Expansion

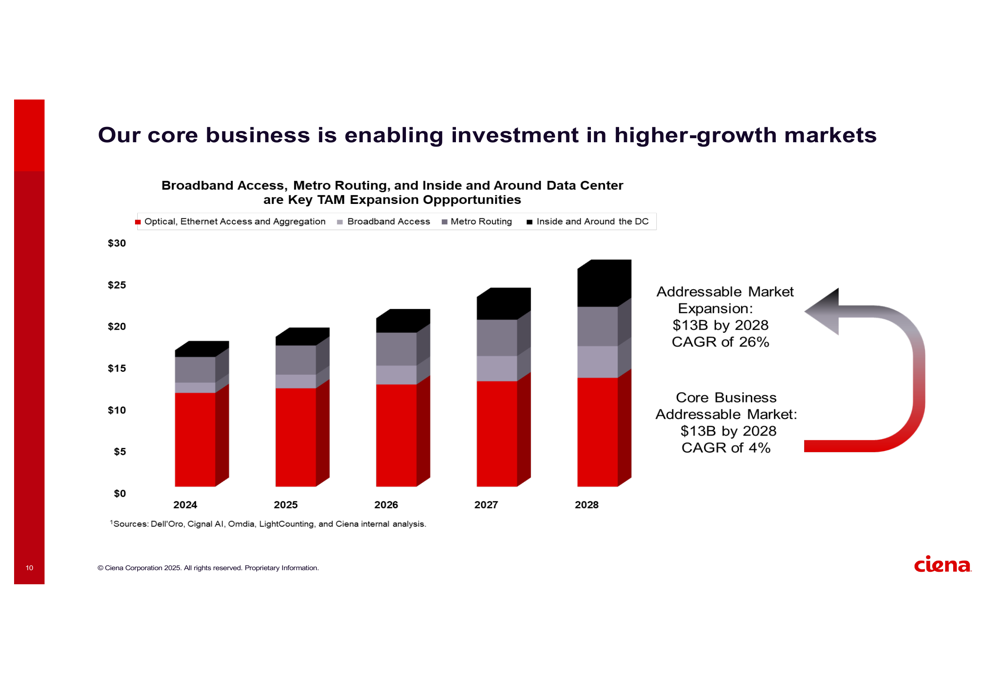

Ciena’s presentation emphasized its strategy to expand beyond its core optical networking business into higher-growth adjacent markets. The company identified broadband access, metro routing, and data center connectivity as key growth opportunities, projecting its addressable market expansion to reach $13 billion by 2028, representing a 26% compound annual growth rate (CAGR).

This expansion strategy is illustrated in the following chart:

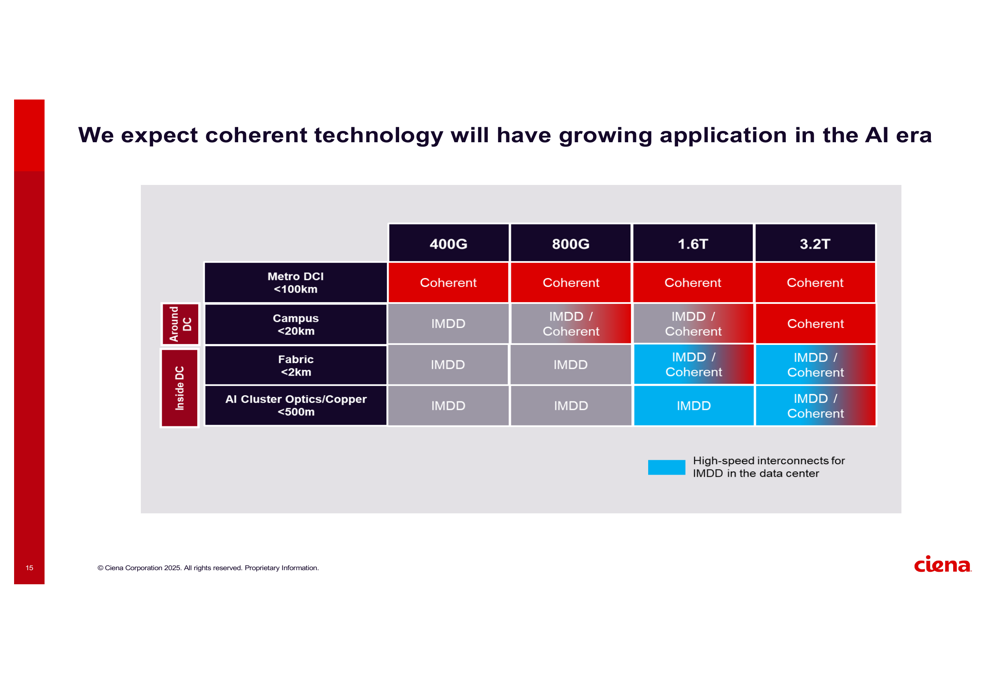

The company is particularly focused on capitalizing on AI-driven infrastructure investments, highlighting how coherent optical technology is becoming increasingly important for AI data center connectivity. Ciena positioned its WaveLogic technology as well-suited for these emerging applications.

As shown in this analysis of coherent technology applications in the AI era:

Forward-Looking Statements

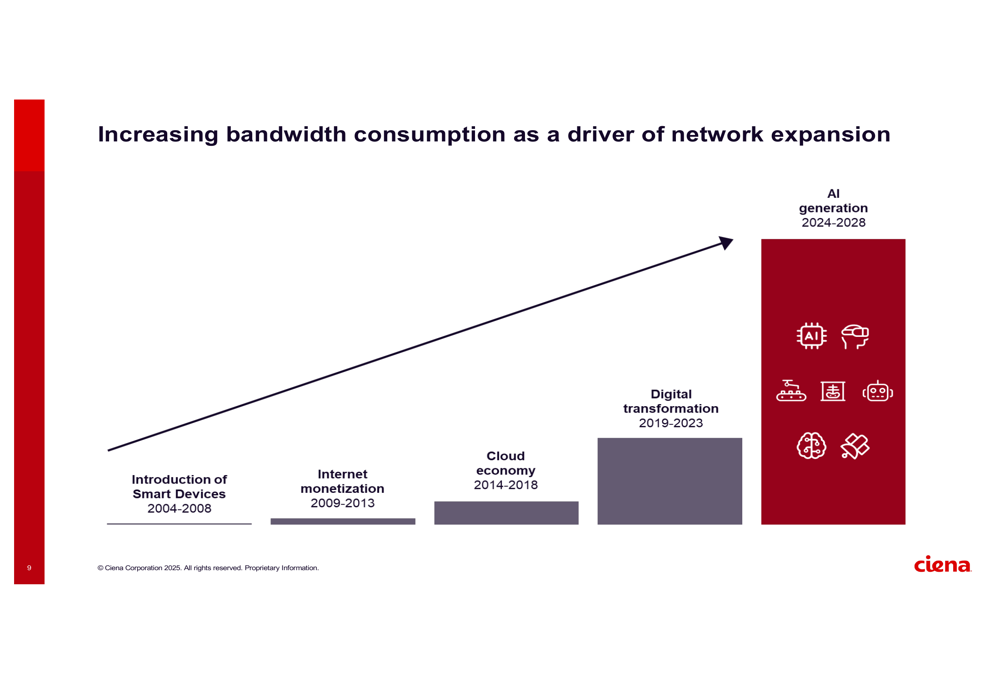

Ciena’s presentation emphasized long-term growth opportunities across different customer segments, particularly in cloud providers and service providers. The company highlighted that its expansion into new addressable markets provides an opportunity to outpace its traditional revenue growth rate over time.

While the presentation didn’t provide specific numerical guidance for upcoming quarters, it positioned the company to benefit from increasing bandwidth consumption driven by AI applications. This strategic direction is illustrated in the following chart showing bandwidth consumption trends:

Despite the positive narrative in the presentation, investors appear concerned about margin pressure and potential challenges ahead, as reflected in the premarket stock decline. This reaction mirrors what happened after Q1 results, when the stock fell despite beating expectations, suggesting ongoing investor caution about supply chain issues, tariff uncertainties, or potential growth deceleration.

Ciena’s cash position remains strong at $1.35 billion, though slightly down from $1.42 billion a year earlier. The company continued its share repurchase program, buying back approximately 1.2 million shares for $84.3 million during the quarter as part of its three-year repurchase initiative.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.