Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Citizens Community Bancorp Inc (NASDAQ:CZWI) released its first quarter 2025 earnings presentation on April 27, highlighting the company’s continued strategic transformation and financial performance. Operating primarily in northwestern Wisconsin, the Twin Cities metro area, and the Mankato, Minnesota MSA, the bank has leveraged diverse regional economies to support steady growth.

The bank currently trades at $14.77, within its 52-week range of $11.74 to $17.04, as it continues to execute on its strategy of optimizing its balance sheet while maintaining strong capital ratios.

Executive Summary

Citizens Community Bancorp’s Q1 2025 presentation emphasized its ongoing transformation from a consumer-focused lender to a more diversified community bank with expanded commercial lending capabilities. The company highlighted its strong capital position with a tangible common equity (TCE) ratio of 8.5%, which provides a buffer against economic uncertainty while supporting continued dividend growth and share repurchases.

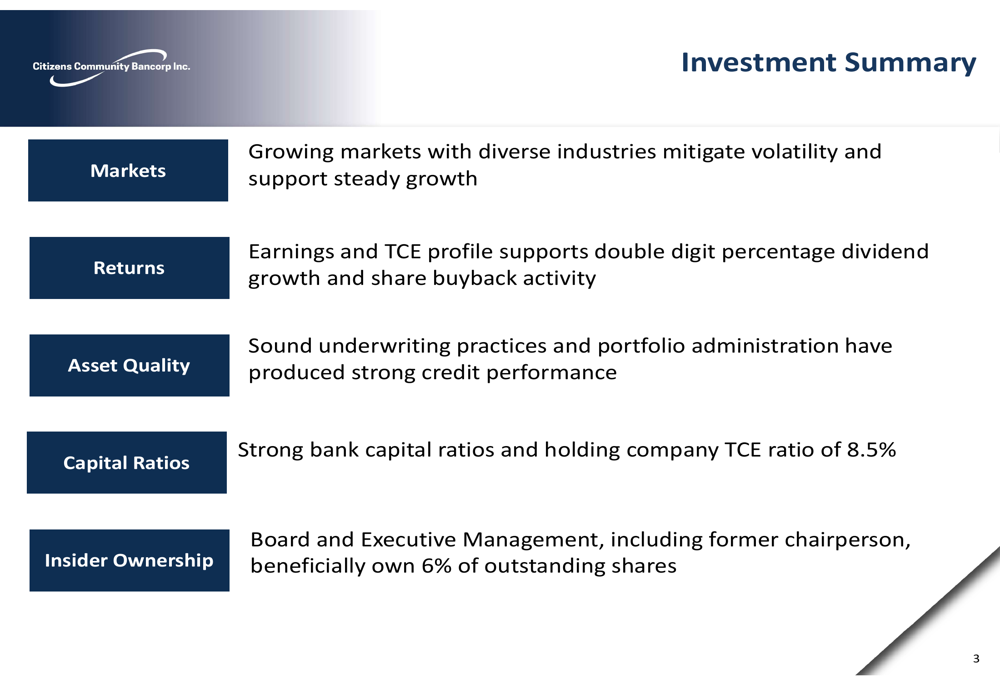

Management pointed to the bank’s growing markets with diverse industry exposure as key factors in mitigating volatility and supporting steady growth. The presentation also emphasized the bank’s sound underwriting practices, which have resulted in strong credit performance with net charge-offs averaging just 0.05% since 2017.

As shown in the following investment highlights chart, the bank has positioned itself for sustainable growth through strategic initiatives:

Quarterly Performance Highlights

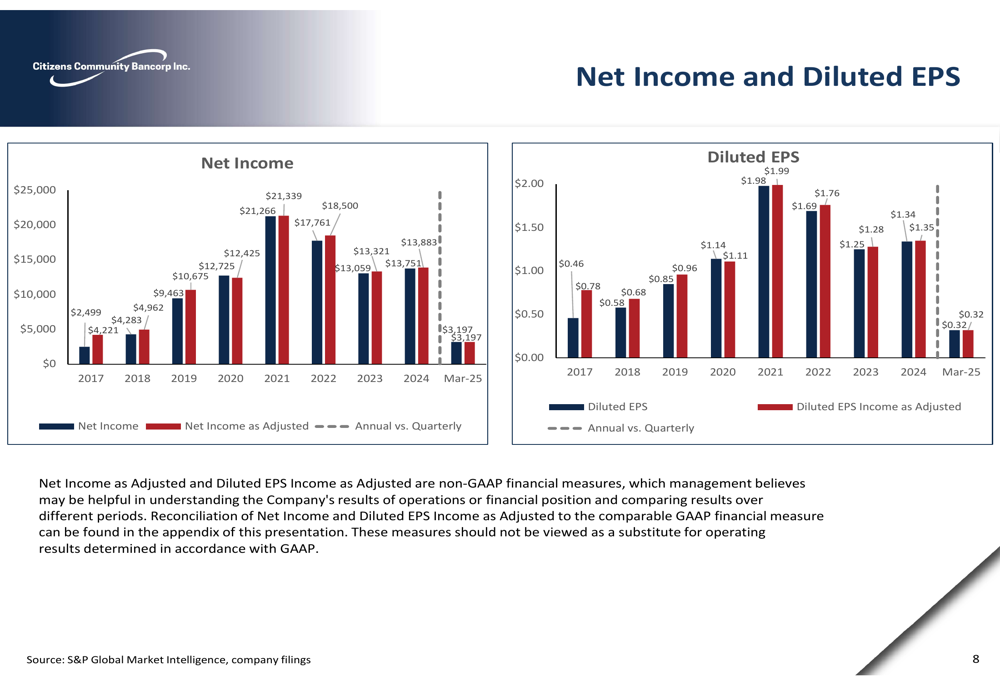

The Q1 2025 results demonstrated Citizens Community’s ability to maintain profitability while navigating the current interest rate environment. The bank’s net income and earnings per share figures show consistent performance, with management using both GAAP and adjusted (non-GAAP) metrics to provide a clearer picture of underlying operational performance.

The following chart illustrates the bank’s net income and diluted EPS trends:

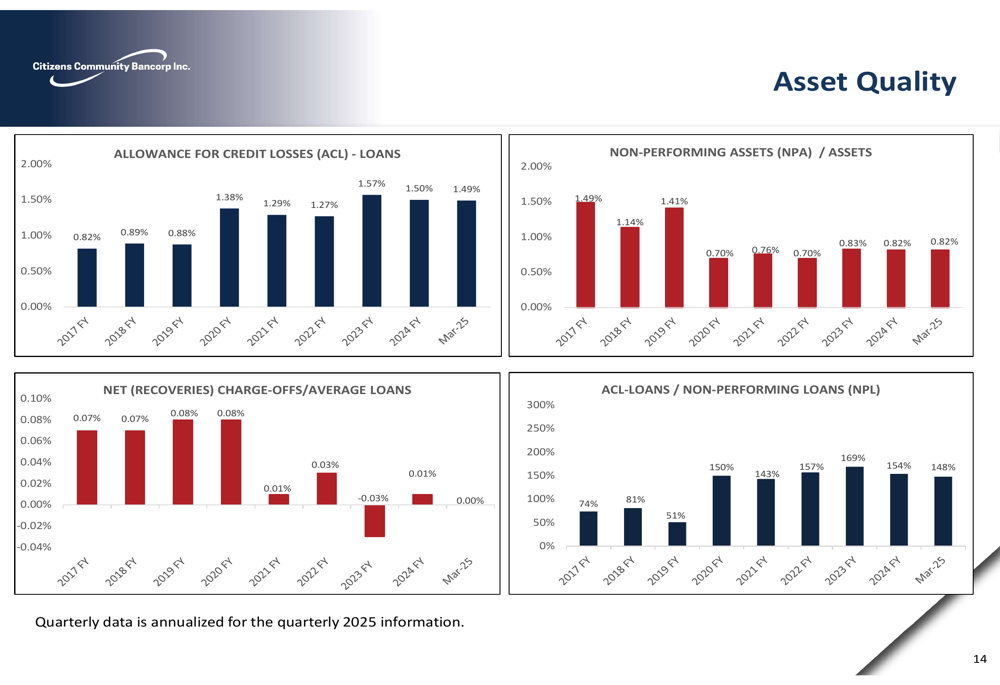

Asset quality remains a strength for Citizens Community, with key metrics demonstrating the effectiveness of the bank’s credit culture. The presentation highlighted the bank’s allowance for credit losses (ACL) to loans ratio, non-performing assets (NPA) to assets ratio, net charge-offs to average loans ratio, and ACL to non-performing loans ratio.

The following chart demonstrates the bank’s consistent asset quality metrics:

Strategic Initiatives

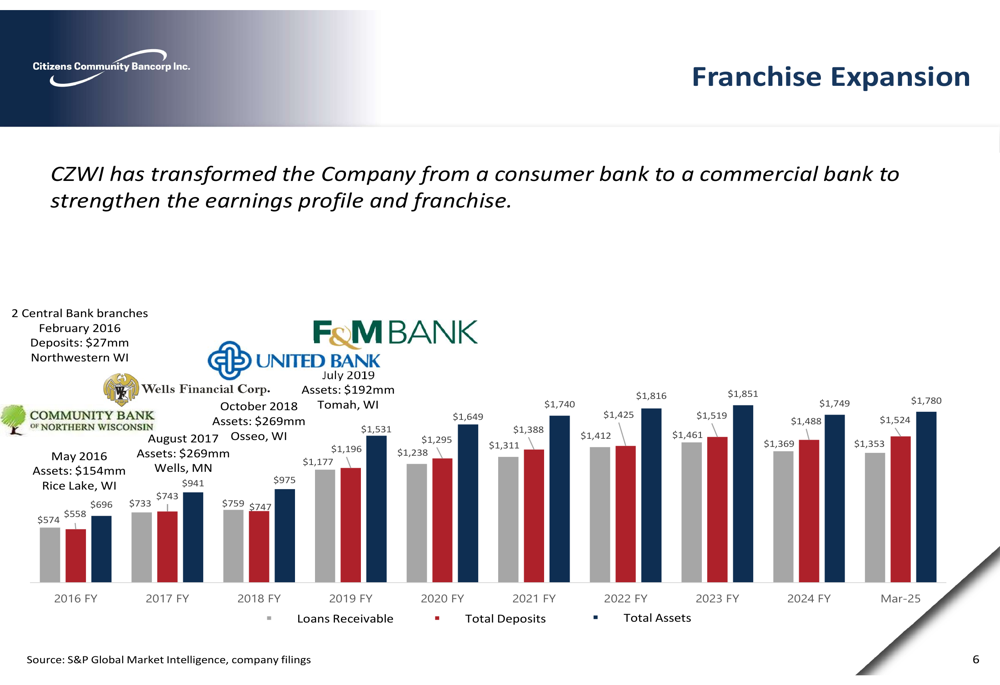

Citizens Community has pursued a deliberate expansion strategy through acquisitions, which has contributed significantly to its growth trajectory. Since 2016, the bank has completed several strategic acquisitions, including two Central Bank branches (2016), Community Bank of Northern Wisconsin (2017), and F&M United Bank (2019).

The bank’s franchise expansion is illustrated in the following chart, showing growth in loans, deposits, and total assets:

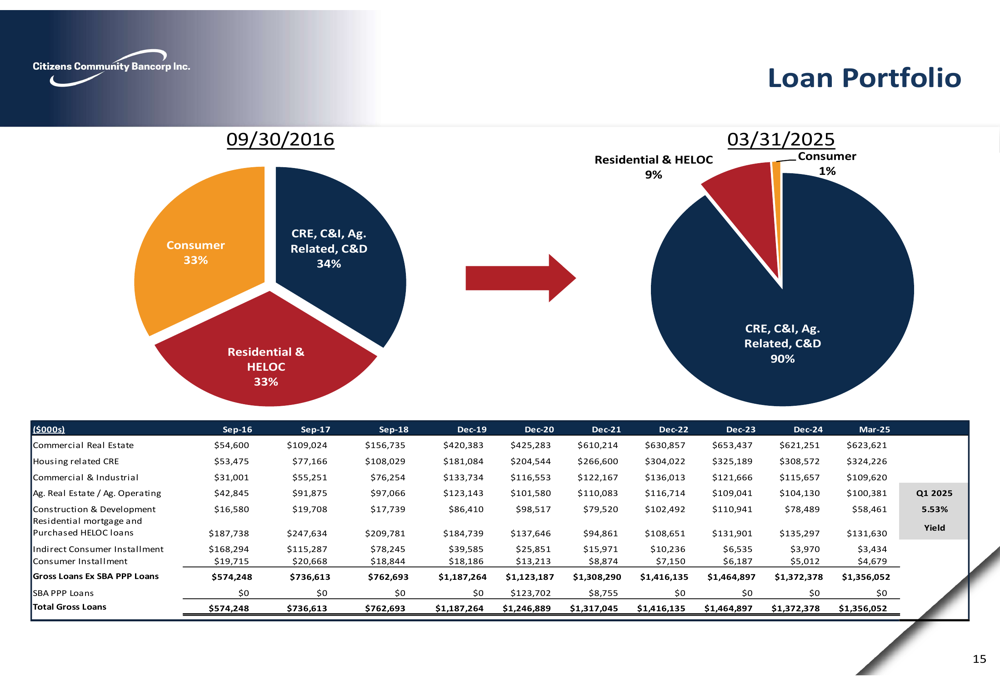

A key aspect of Citizens Community’s strategy has been the transformation of its loan portfolio. The bank has significantly diversified its lending activities, shifting from a consumer-focused portfolio in 2016 to a more balanced mix that includes commercial real estate (CRE), commercial and industrial (C&I), and agricultural lending by 2025.

The following chart illustrates this strategic shift in the loan portfolio composition:

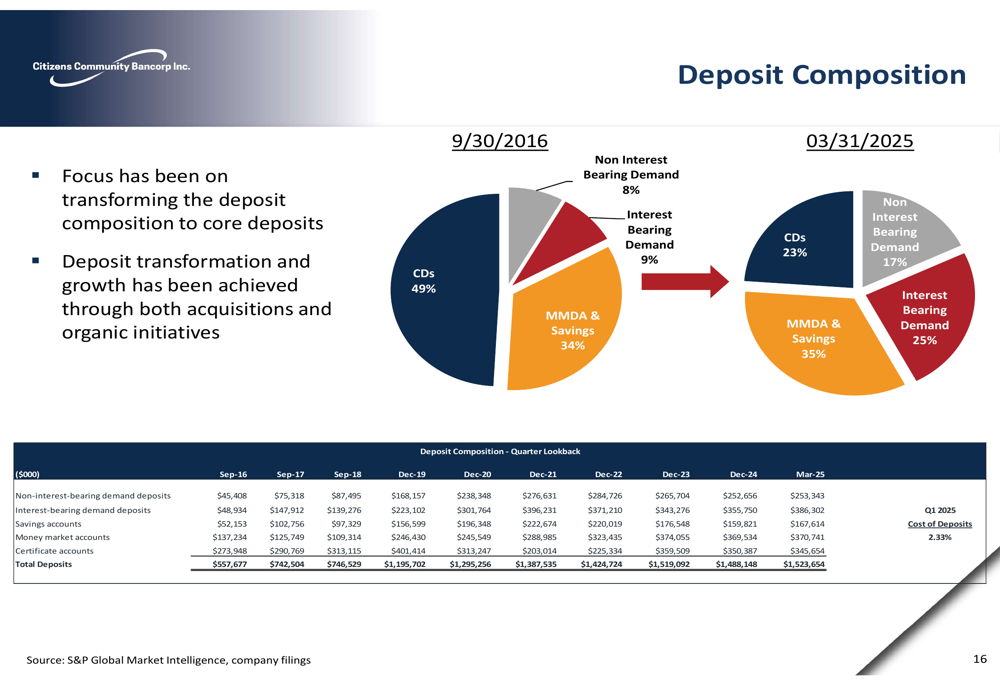

Similarly, the bank has transformed its deposit base, focusing on growing core deposits and reducing reliance on certificates of deposit. This shift provides more stable funding and improves the bank’s interest rate risk profile.

The deposit transformation is shown in the following chart:

Detailed Financial Analysis

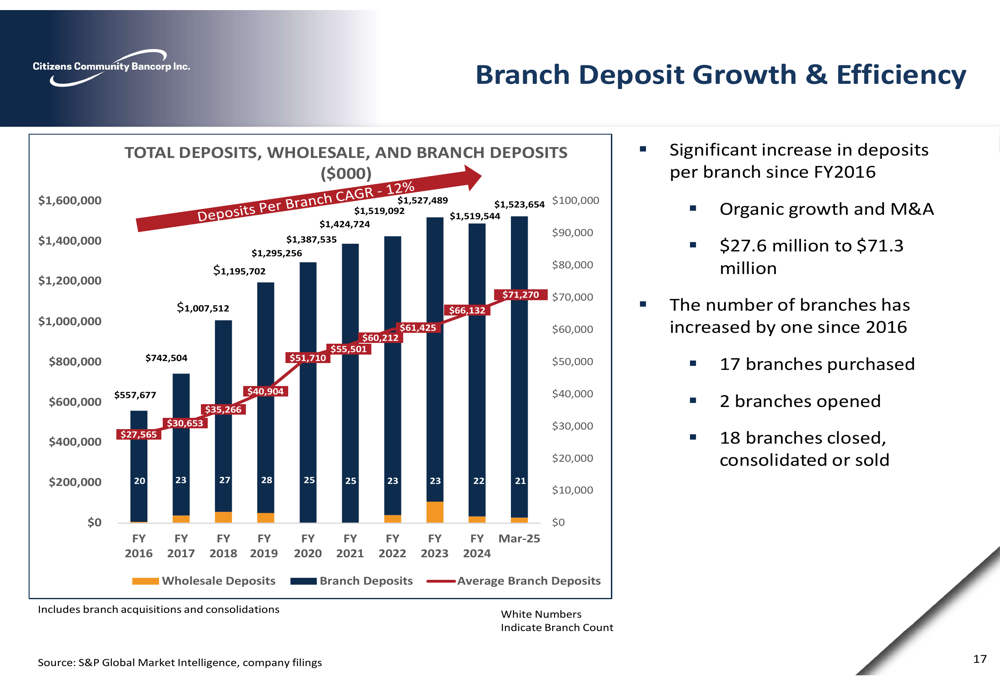

Citizens Community has demonstrated impressive operational efficiency improvements, particularly in its branch network. The bank has increased deposits per branch from $27.6 million to $71.3 million, reflecting both organic growth and strategic acquisitions.

The following chart illustrates the bank’s deposit growth and branch efficiency:

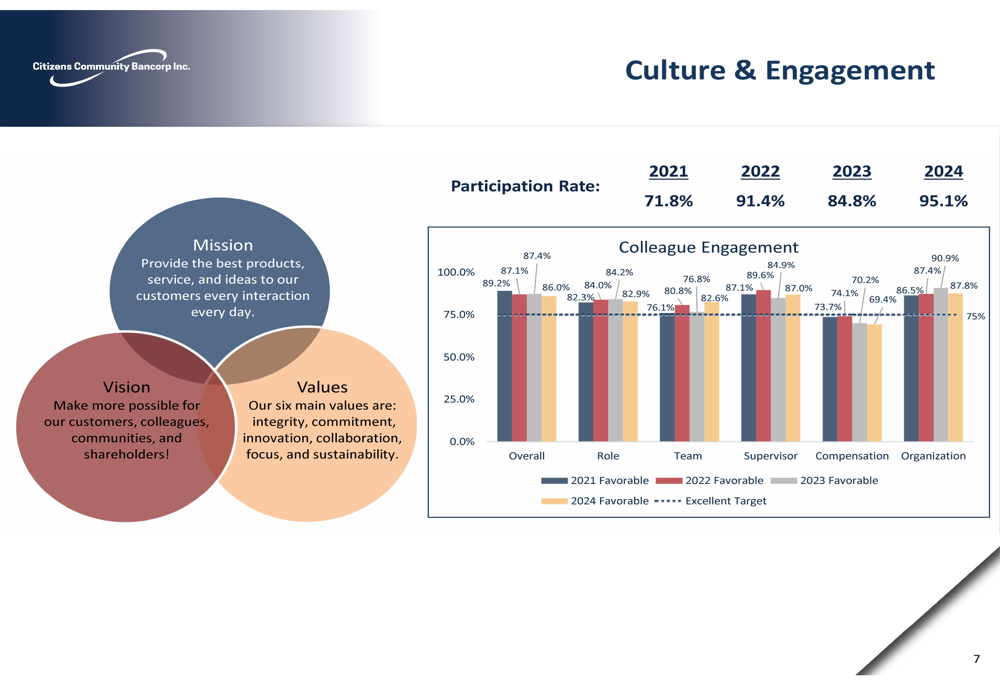

The bank’s culture and employee engagement have also shown significant improvement, with participation rates increasing from 71.8% in 2021 to 95.1% in 2024. Management views this as a critical component of operational success and customer satisfaction.

The following chart shows the improvement in colleague engagement metrics:

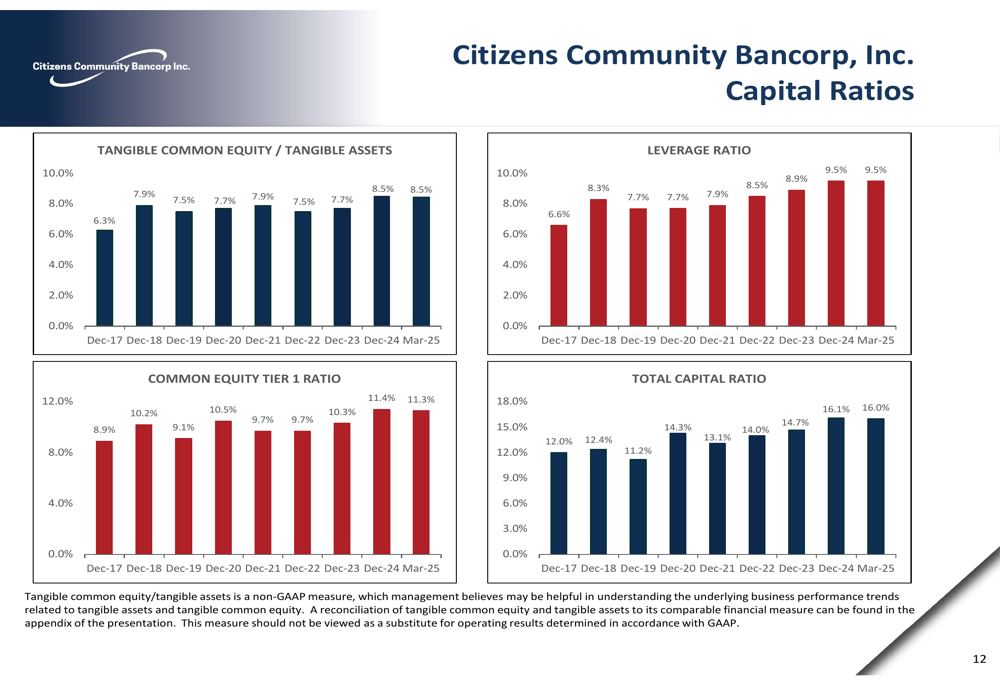

Capital management remains a priority for Citizens Community, with the bank maintaining strong capital ratios while supporting share repurchases. The presentation highlighted the bank’s tangible common equity to tangible assets ratio, leverage ratio, common equity tier 1 ratio, and total capital ratio.

The following chart shows the bank’s capital ratio trends:

Forward-Looking Statements

Looking ahead, Citizens Community aims to continue optimizing its balance sheet and earnings to support share buybacks while maintaining a TCE ratio above 8% to weather potential economic shocks. Management emphasized its track record of controlling expense growth below the rate of inflation by leveraging technology to reduce operating costs and improve productivity.

The bank’s performance objectives include maintaining its strong credit culture, achieving operating leverage through technological improvements, and fostering a culture of accountability for executing business strategy. Management believes these initiatives will continue to generate strong results and increase franchise value.

The bank’s diverse market exposure across northwestern Wisconsin and parts of Minnesota is expected to provide stability in earnings, capital, and asset quality through various economic cycles, positioning Citizens Community for continued growth in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.