HK-listed gold stocks jump as US economic fears boost bullion prices

Introduction & Market Context

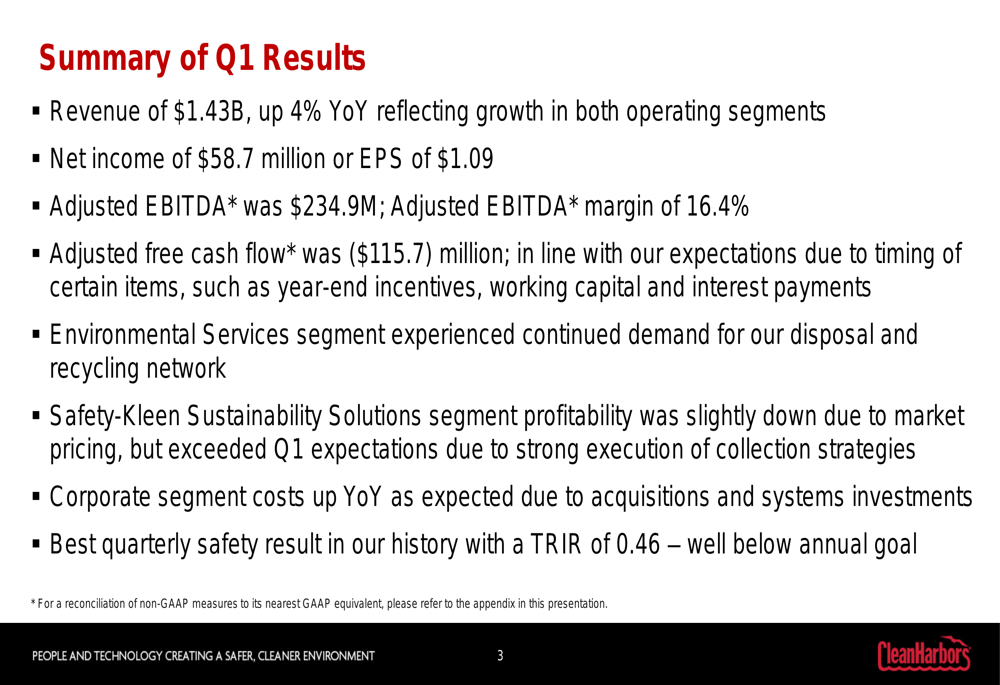

Clean Harbors (NYSE:CLH), a leading provider of environmental and industrial services, released its first quarter 2025 investor presentation on April 30, showing mixed results with revenue growth offset by margin pressure. The company reported a 4% year-over-year revenue increase to $1.43 billion, while earnings per share declined to $1.09 from $1.29 in the same period last year.

The stock was down 2.24% in pre-market trading following the release, reflecting investor concerns about the profitability decline despite top-line growth. This reaction follows a similar pattern to the company’s Q4 2024 results, which saw the stock drop 4.14% despite an earnings beat.

Quarterly Performance Highlights

Clean Harbors delivered $1.43 billion in Q1 2025 revenue, representing a 4% increase from the prior year. However, net income decreased to $58.7 million from $69.8 million in Q1 2024, resulting in earnings per share of $1.09 compared to $1.29 a year earlier.

Adjusted EBITDA showed modest improvement, reaching $234.9 million versus $230.1 million in Q1 2024, though the adjusted EBITDA margin contracted slightly to 16.4% from 16.7%.

As shown in the following summary of quarterly results:

The company also highlighted achieving its best quarterly safety result in company history with a Total (EPA:TTEF) Recordable Incident Rate (TRIR) of 0.46, underscoring its commitment to operational excellence and workplace safety.

Segment Analysis

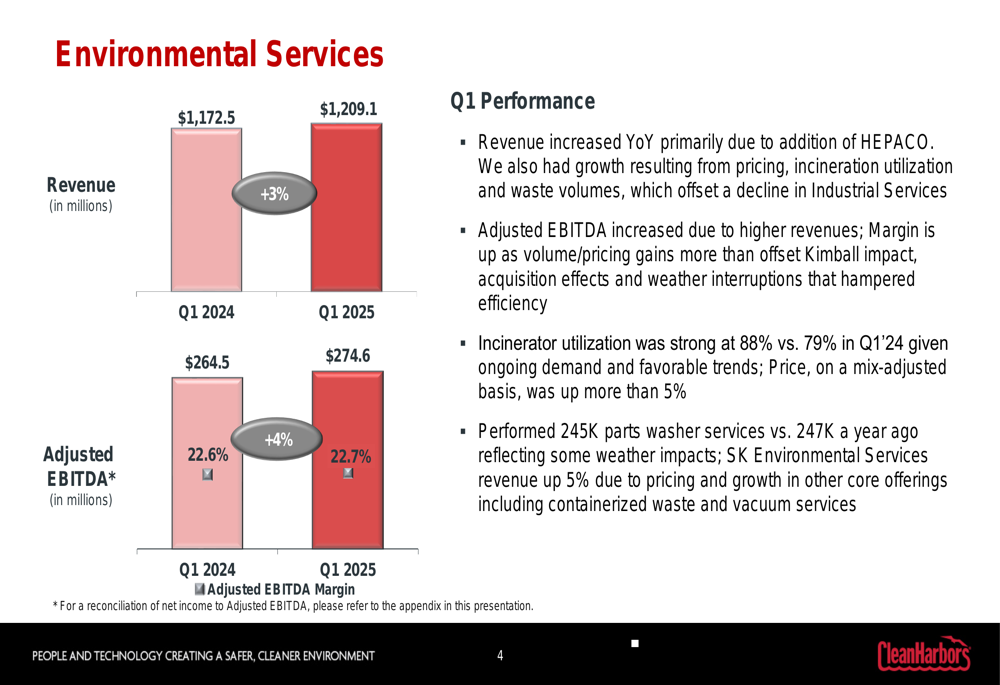

Clean Harbors’ Environmental Services segment, which accounts for approximately 84% of total revenue, demonstrated solid performance with 3% revenue growth to $1.21 billion and a 4% increase in Adjusted EBITDA to $274.6 million. The segment’s margin improved slightly to 22.7% from 22.6% in the prior year.

Key drivers for this segment included the addition of HEPACO (acquired in 2024), pricing improvements, and strong incinerator utilization, which reached 88% compared to 79% in Q1 2024.

The segment’s performance is illustrated in the following chart:

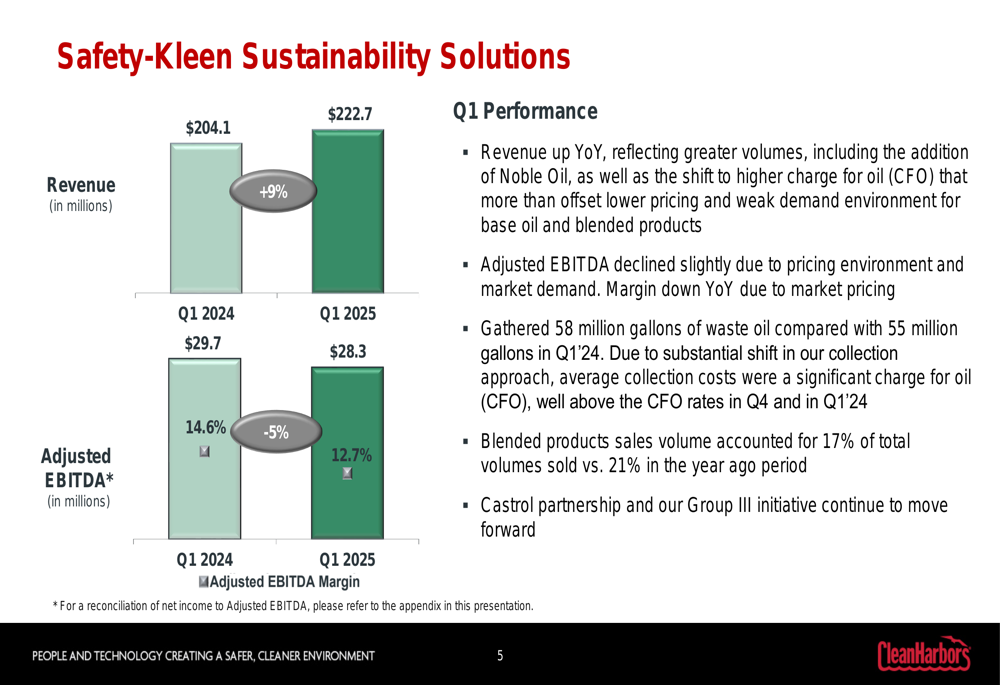

Meanwhile, the Safety-Kleen Sustainability Solutions segment showed more challenging results. Despite 9% revenue growth to $222.7 million, driven by greater volumes and the addition of Noble Oil, Adjusted EBITDA decreased to $28.3 million from $29.7 million in Q1 2024. This resulted in margin compression from 14.6% to 12.7%.

The company attributed this decline to pricing pressures and weak market demand, though performance exceeded internal expectations. Waste oil collection increased to 58 million gallons from 55 million gallons in Q1 2024, but blended products sales declined to 17% of total volumes from 21% a year earlier.

The following chart details the Safety-Kleen segment’s performance:

Balance Sheet and Cash Flow

Clean Harbors maintained a strong financial position with $595.3 million in cash and short-term marketable securities as of March 31, 2025, up from $442.6 million a year earlier but down from $789.8 million at year-end 2024. The company’s debt level remained stable at approximately $2.78 billion.

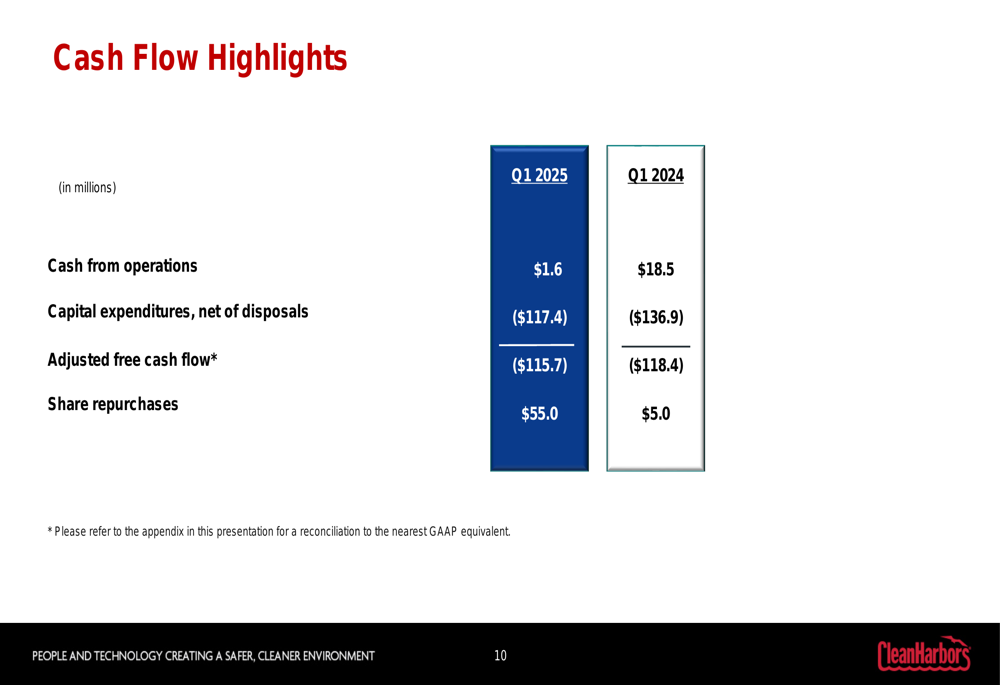

As typical for the first quarter, Clean Harbors reported negative free cash flow of $115.7 million, slightly improved from the $118.4 million deficit in Q1 2024. Cash from operations decreased to $1.6 million from $18.5 million in the prior year, while capital expenditures decreased to $117.4 million from $136.9 million.

The company also accelerated its share repurchase program, buying back $55 million worth of shares compared to just $5 million in Q1 2024, demonstrating confidence in its long-term outlook despite the quarterly challenges.

The following slide shows the detailed cash flow comparison:

Forward Guidance

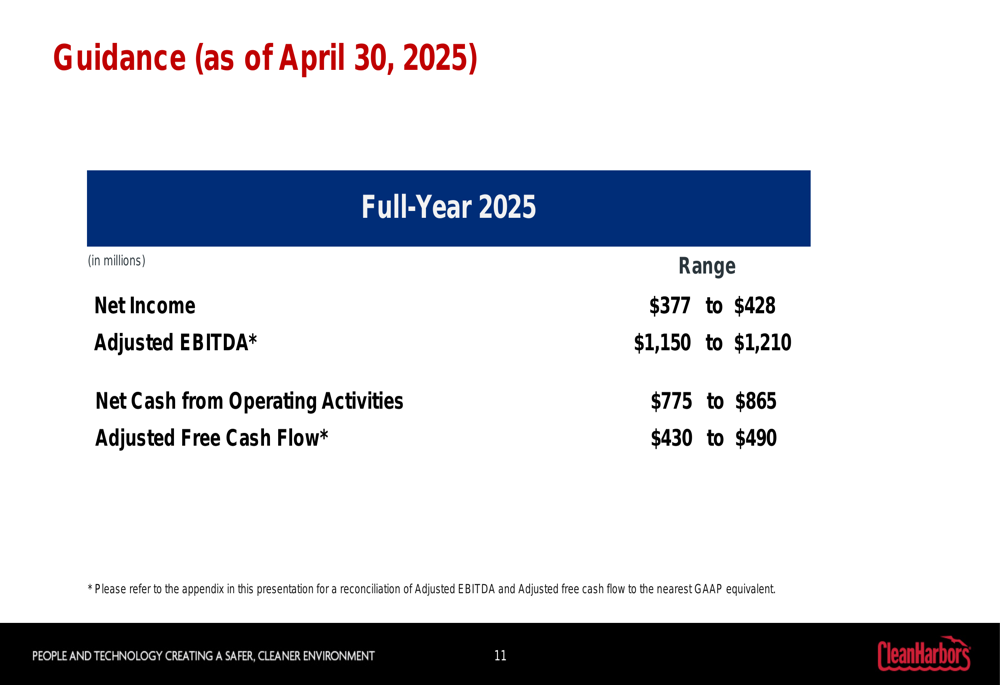

Despite the mixed Q1 results, Clean Harbors maintained its full-year 2025 guidance, projecting net income between $377 million and $428 million and Adjusted EBITDA between $1.15 billion and $1.21 billion. The company expects to generate between $430 million and $490 million in adjusted free cash flow for the year.

This guidance suggests management anticipates improved performance in the coming quarters, particularly in the Safety-Kleen segment where market conditions are expected to stabilize.

The detailed guidance is presented in the following slide:

Clean Harbors continues to execute its disciplined capital allocation strategy, focusing on organic growth investments, strategic acquisitions, share repurchases, and debt management. The company highlighted its ongoing investment in the Phoenix Hub expansion, with $15 million allocated for 2025.

Market Reaction and Conclusion

The market’s initial reaction to Clean Harbors’ Q1 2025 results was cautious, with the stock trading down 2.24% in pre-market activity. This follows a pattern similar to the Q4 2024 results, which saw a 4.14% decline despite beating earnings expectations.

Investors appear concerned about the company’s profitability trajectory, particularly the declining net income and EPS despite revenue growth. However, the maintained full-year guidance suggests management confidence in the company’s ability to improve performance throughout the remainder of 2025.

Clean Harbors’ Environmental Services segment continues to demonstrate resilience and growth, while the Safety-Kleen segment faces ongoing market challenges that may require additional strategic adjustments. The company’s strong balance sheet and commitment to shareholder returns through share repurchases provide some stability amid these mixed results.

As Clean Harbors progresses through 2025, investors will likely focus on whether the company can deliver the improved performance implied by its maintained guidance, particularly regarding margin recovery and accelerated cash flow generation in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.