Soleno Therapeutics tumbles despite Q3 earnings, revenue beat

Introduction & Market Context

Cloudflare, Inc. (NYSE:NET) delivered strong financial results in its Q2 2025 investor presentation, showcasing 28% year-over-year revenue growth and strategic advancements in AI and cloud services. The company’s stock closed at $227.38, up 1.08%, approaching its 52-week high of $231.13, reflecting positive investor sentiment toward the company’s performance and outlook.

The cybersecurity and cloud services provider highlighted its expanding global network, growing customer base, and increasing penetration among large enterprises as key drivers of its continued success. Cloudflare’s focus on AI innovation has positioned it as a preferred platform for AI companies, with CEO Matthew Prince noting that "Cloudflare is increasingly the platform the most innovative companies are choosing to power the future of AI."

Quarterly Performance Highlights

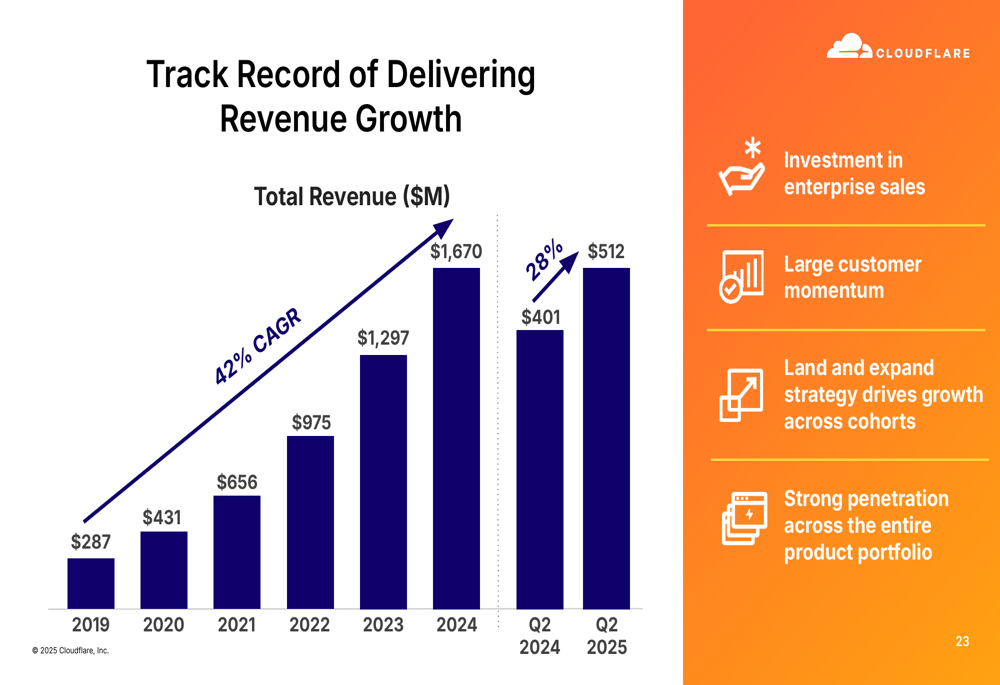

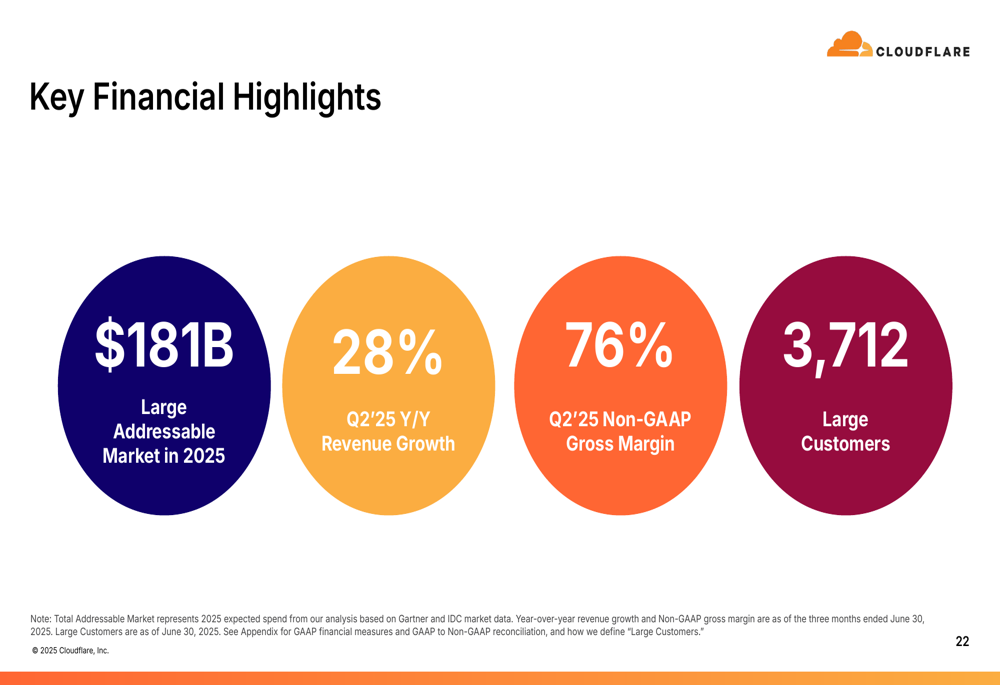

Cloudflare reported Q2 2025 revenue of $512 million, representing a 28% increase from $401 million in Q2 2024. The company crossed the $2 billion mark in annual run rate revenue, a significant milestone in its growth journey.

As shown in the following chart detailing Cloudflare’s revenue trajectory:

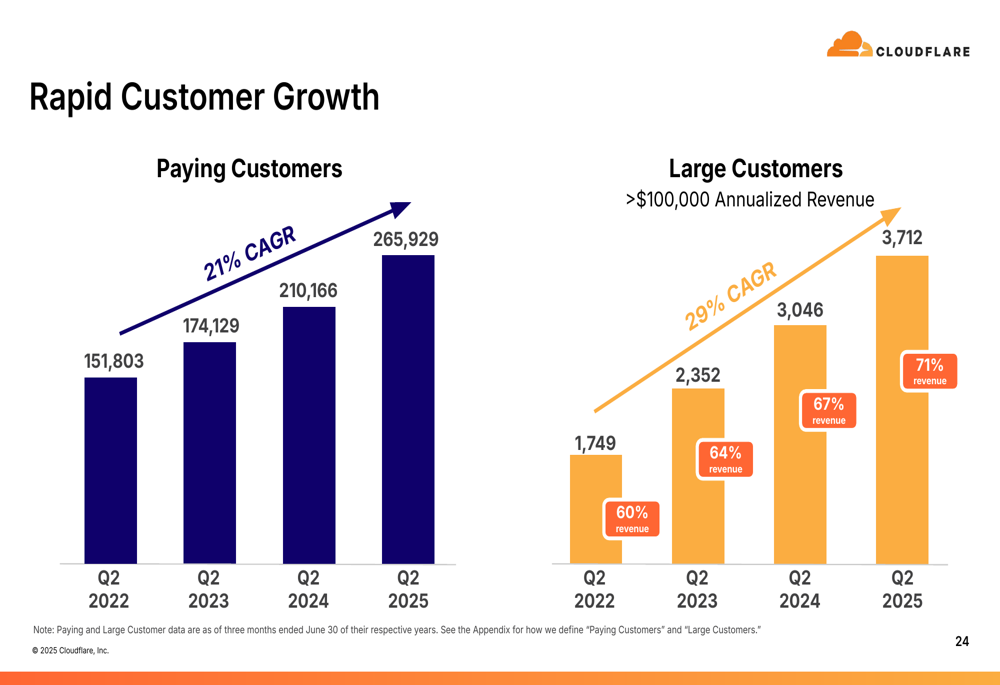

The company’s customer acquisition strategy continues to yield results, with total paying customers reaching 265,929 in Q2 2025, up from 210,166 in Q2 2024. More importantly, large customers (those spending over $100,000 annually) grew 22% year-over-year to 3,712, demonstrating Cloudflare’s success in moving upmarket.

The following chart illustrates this rapid customer growth across both segments:

Cloudflare maintained strong gross margins at 76% on a non-GAAP basis, though this represents a slight decline from 79% in the previous year. The company attributes this to its strategic investments in network expansion and AI capabilities.

Strategic Positioning

Cloudflare’s global network now spans over 330 cities in 125+ countries, providing a competitive advantage through its proximity to users. Approximately 95% of the world’s Internet-connected population is within 50 milliseconds of a Cloudflare data center, enabling faster and more reliable service delivery.

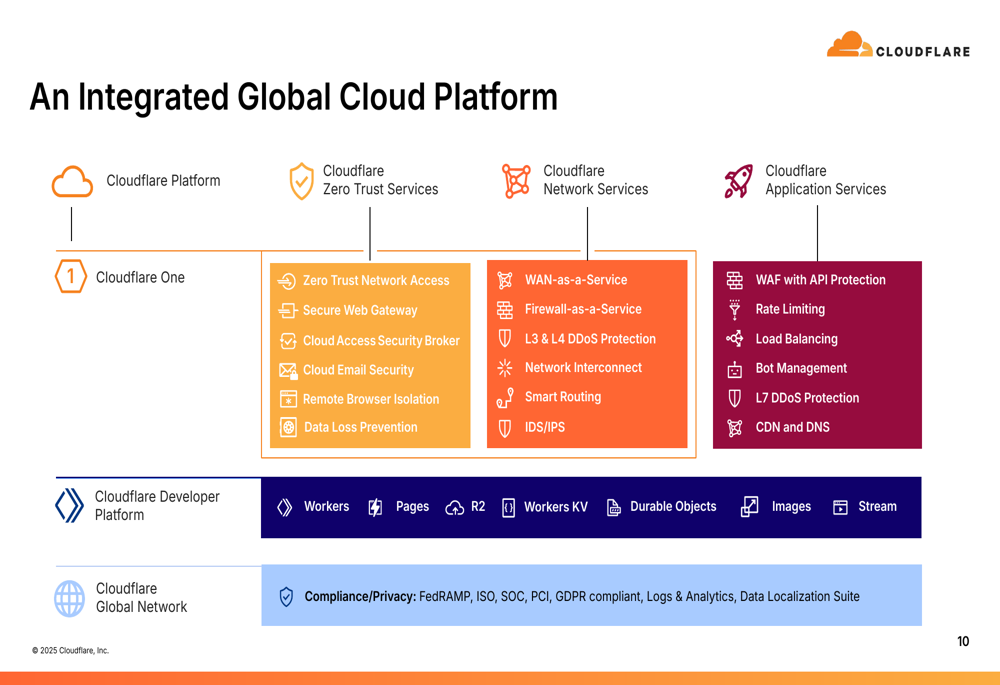

The company’s integrated global cloud platform offers a comprehensive suite of services across network security, zero trust, and application development:

Cloudflare’s serverless architecture, deployed on commodity hardware with a single software stack across its network, provides significant operational efficiencies and cost advantages over traditional hardware-based solutions. This architecture also enables rapid innovation and seamless product integration.

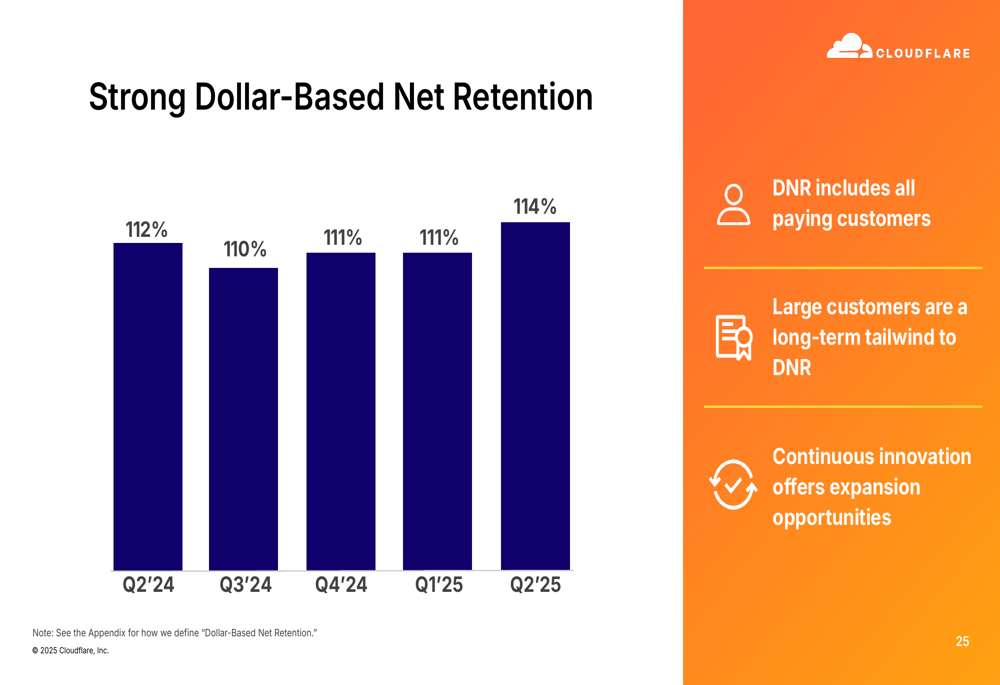

The company’s dollar-based net retention rate improved to 114% in Q2 2025, up from 112% in Q2 2024, indicating successful cross-selling and upselling to existing customers:

Market Opportunity

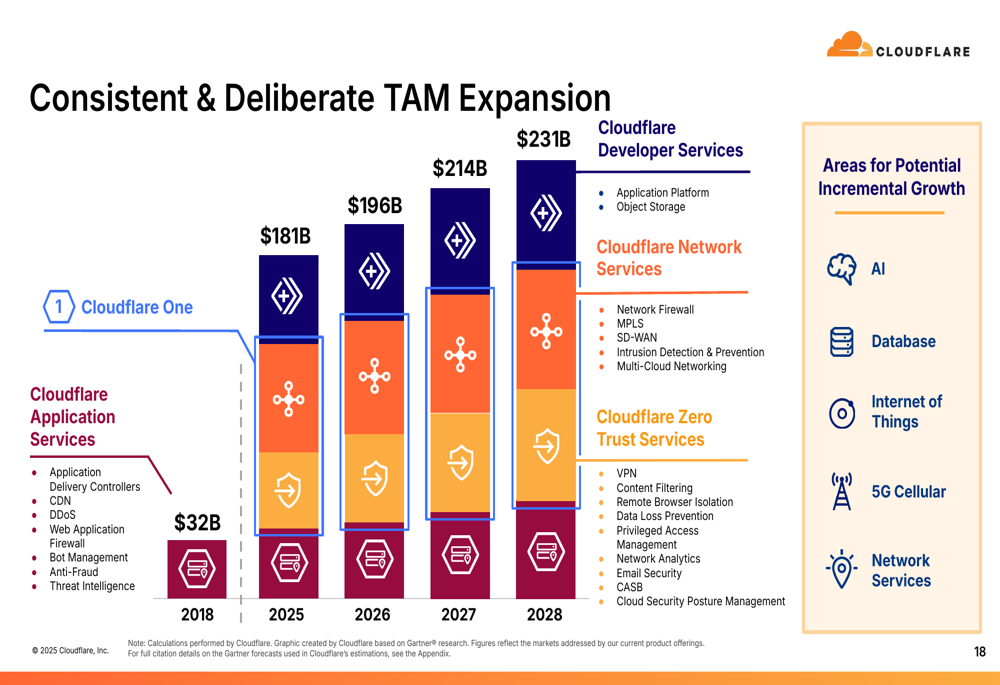

Cloudflare continues to expand its total addressable market (TAM), which has grown from $32 billion in 2018 to an estimated $181 billion in 2025, with projections reaching $231 billion by 2028. This expansion reflects the company’s entry into new service categories and the overall growth of cloud computing and cybersecurity markets.

The following chart illustrates this consistent TAM expansion:

The company highlighted its strong position in the AI market, with 80% of major AI companies as customers. Cloudflare’s Workers AI platform and other AI-focused offerings are driving additional growth opportunities as enterprises increasingly adopt AI technologies.

Financial Outlook

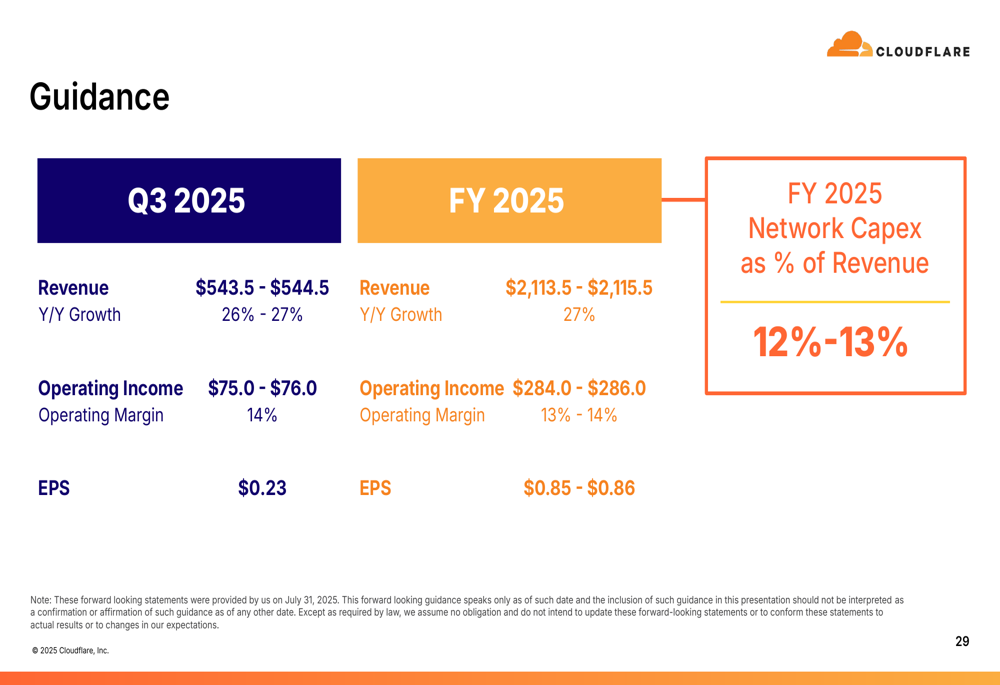

Cloudflare provided positive guidance for Q3 2025, projecting revenue between $543.5-544.5 million, representing 26-27% year-over-year growth. For the full fiscal year 2025, the company expects revenue of $2,113.5-2,115.5 million, maintaining 27% annual growth.

The company’s financial guidance also shows improving profitability, with operating margins projected at 14% for Q3 2025 and 13-14% for the full year:

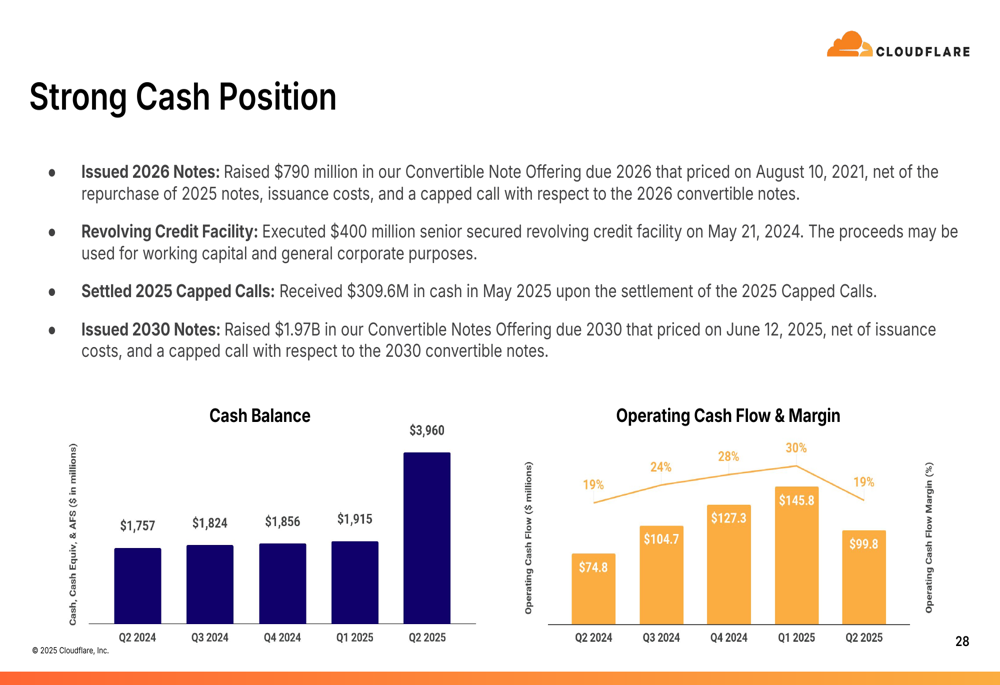

Cloudflare’s cash position has strengthened significantly, with cash and investments growing from $1.76 billion in Q2 2024 to $3.96 billion in Q2 2025, providing substantial resources for future investments and potential acquisitions:

Looking further ahead, Cloudflare’s long-term operating model targets gross margins of 75-77%, operating margins exceeding 20%, and free cash flow margins of approximately 25% or higher. The company aims to achieve a $5 billion annual run rate by FY2028, driven by continued innovation and operational efficiency.

Competitive Industry Position

Cloudflare emphasized its competitive advantages in the presentation, highlighting its network scale, ease of use, shared intelligence, and "no trade-offs" approach as key differentiators. The company now counts 36% of Fortune 500 companies as paying customers, demonstrating its growing enterprise adoption.

The company’s key financial metrics underscore its strong market position:

While Cloudflare faces competition from traditional on-premises vendors, point solution providers, and public cloud giants, its integrated platform approach and global network provide unique advantages. The company’s ability to block an average of 190 billion cyber threats daily showcases the scale and effectiveness of its security capabilities.

Despite macroeconomic pressures and intense competition in the AI and cloud service markets, Cloudflare’s strategic focus on innovation and its strong financial performance position it well for continued growth in the evolving digital landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.