e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

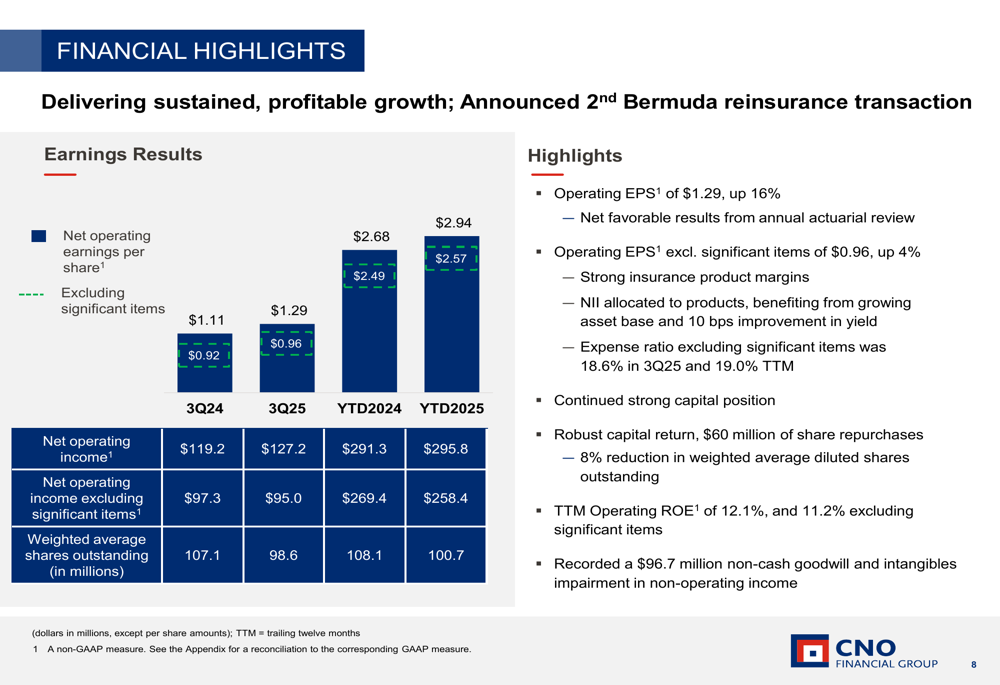

CNO Financial Group (NYSE:CNO) reported strong third-quarter results that significantly exceeded analyst expectations, with operating earnings per share of $1.29, up 16% year-over-year and surpassing forecasts by 40.22%. The company’s stock rose 4.36% to $39.59 following the announcement on November 4, 2025.

Quarterly Performance Highlights

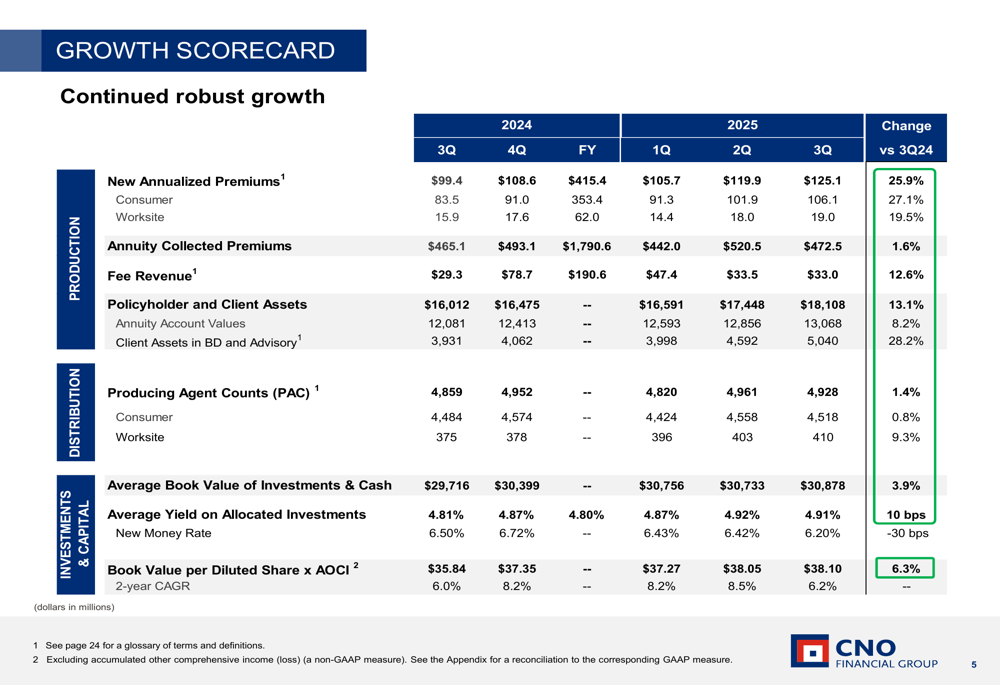

CNO reported its 13th consecutive quarter of strong insurance sales growth, with total new annualized premiums up 25.9% compared to the same period last year. The company’s direct-to-consumer channel showed particularly impressive results with a 56% increase in new annualized premiums.

"We remain focused on growing earnings and improving profitability," CEO Gary Bhojwani stated during the earnings call, emphasizing the company’s commitment to long-term growth.

The presentation highlighted consistent growth across multiple business segments:

The Consumer Division maintained its momentum with life and health new annualized premiums up 27%, including a 33% increase in life insurance sales and a 21% rise in health insurance sales. Medicare Supplement sales were particularly strong, up 33% year-over-year.

Worksite Division also performed well, with record life and health new annualized premiums up 20%, including life insurance sales up 24% and hospital indemnity sales up 53%.

Strategic Initiatives

A significant strategic development announced in the presentation was CNO’s decision to streamline its Worksite Division by exiting the fee services business to focus on high-growth core insurance offerings. This move, planned for completion by mid-2026, aligns with the company’s strategy to concentrate on its most profitable segments.

"We decided to streamline our Worksite Division by exiting the fee services business, sharpening our focus on the high-growth core insurance offerings," the company noted in its presentation. According to the earnings call, this exit could incur charges of 15 to 20 million dollars but is expected to improve long-term profitability.

Financial Analysis

CNO’s financial performance showed strength across multiple metrics, with operating EPS excluding significant items at $0.96, up 4% year-over-year. The company attributed this growth to strong insurance product margins and improved net investment income.

As shown in the following financial highlights:

The company reported a trailing twelve-month operating return on equity of 12.1%, or 11.2% excluding significant items. Book value per diluted share excluding accumulated other comprehensive income increased 6% to $38.10.

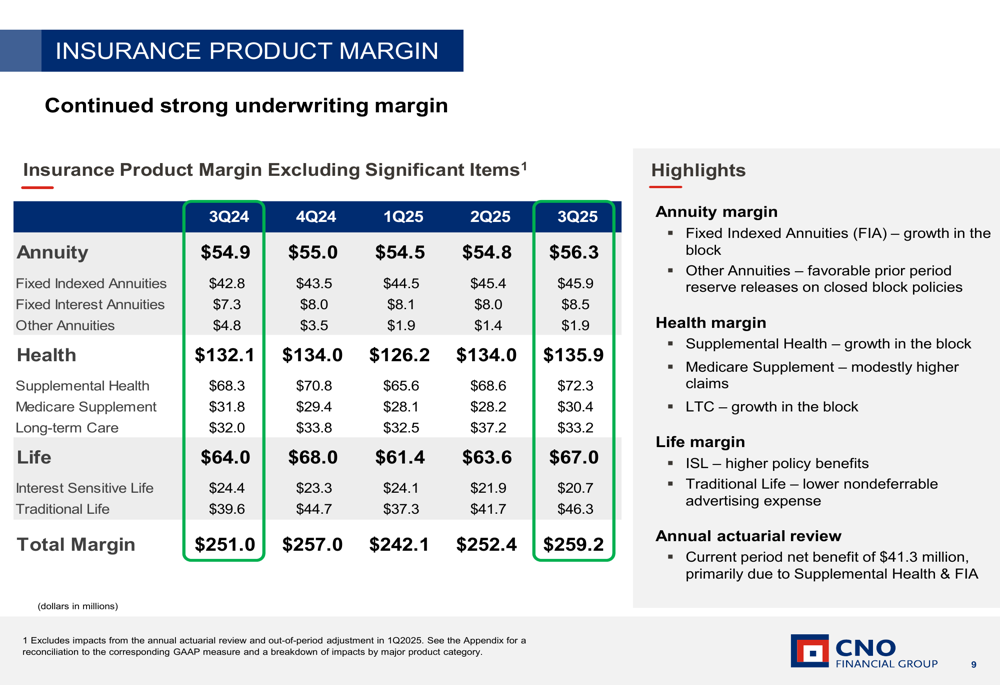

Insurance product margins remained strong across all product lines:

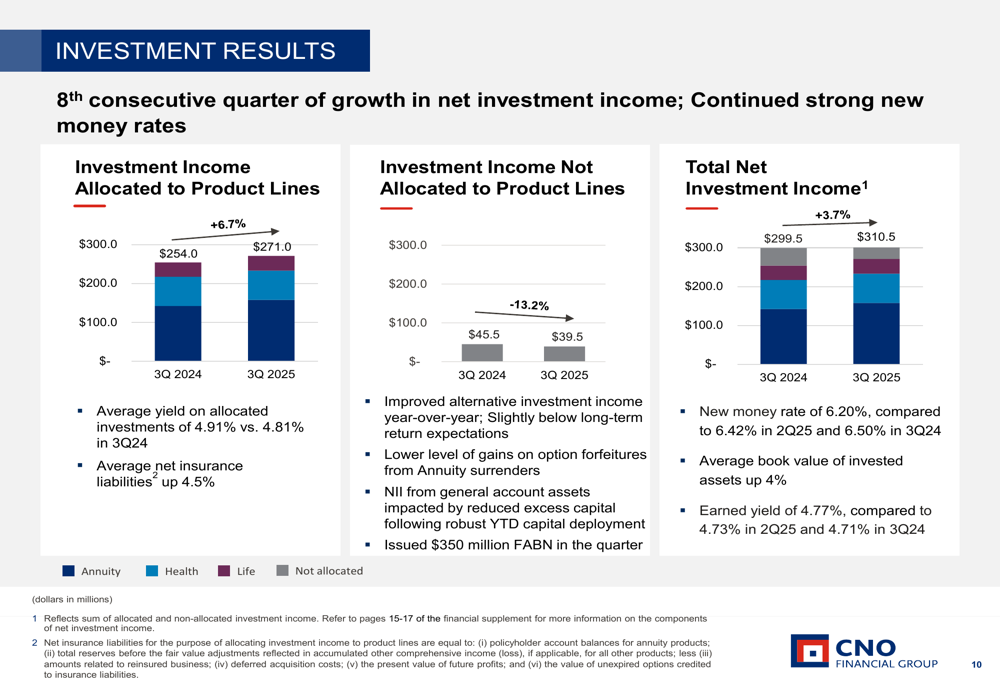

Investment performance was also solid, with net investment income growing for the eighth consecutive quarter:

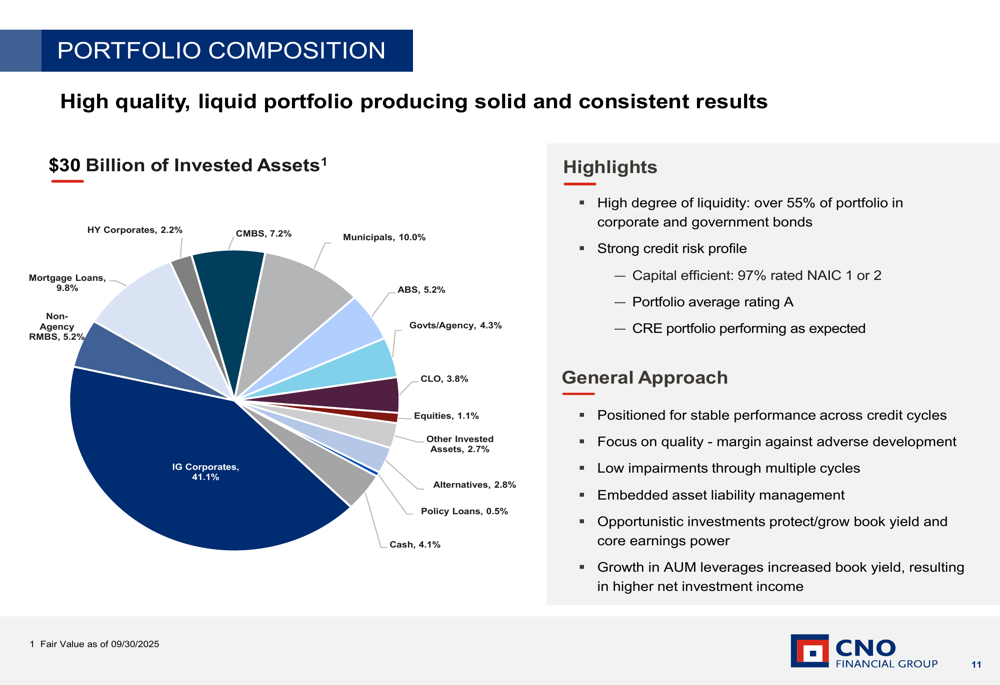

The company maintains a high-quality, liquid investment portfolio of approximately $30 billion, with investment-grade corporate bonds comprising the largest allocation at 41.1%:

Capital Management & Outlook

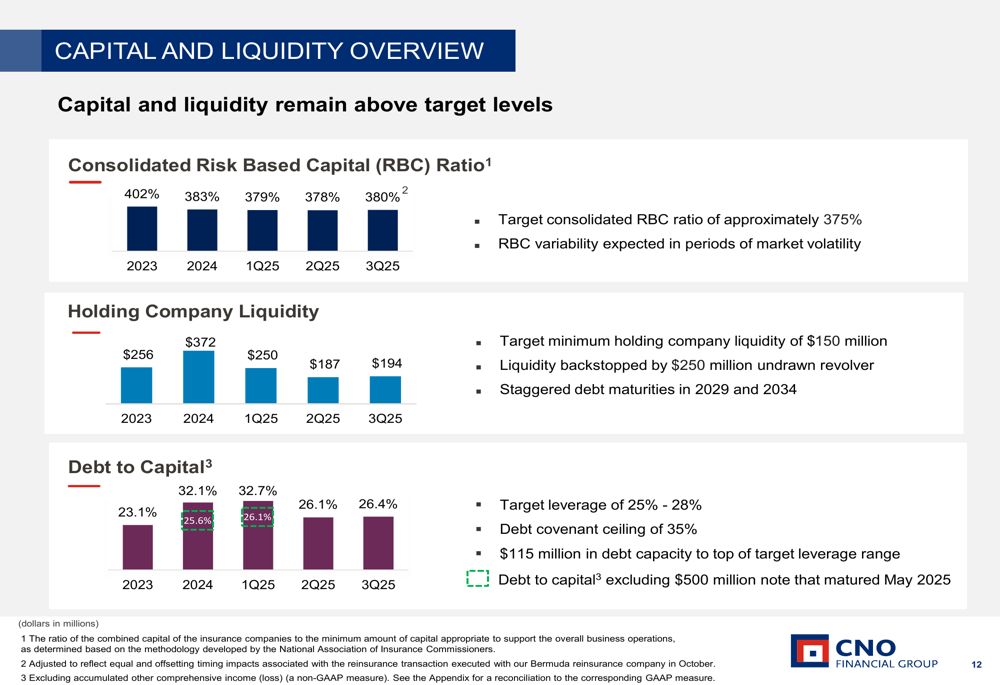

CNO maintained a strong capital position with a consolidated risk-based capital ratio of 380%, slightly above its target of approximately 375%. The company returned $76 million to shareholders in the quarter through dividends and share repurchases, bringing the year-to-date total to $310 million.

Looking forward, CNO provided updated guidance, targeting a 200 basis point improvement in run-rate operating ROE through 2027. For 2025, the company expects operating EPS of $3.75-$3.85 and excess cash flow to the holding company of $365-$385 million.

CFO Paul McDonough highlighted ongoing efforts to explore Bermuda reinsurance opportunities during the earnings call, noting the execution of a second reinsurance transaction with a Bermuda affiliate in October, which could enhance financial flexibility.

Market Reaction

Following the earnings announcement, CNO’s stock price rose by 4.36%, closing at $39.59, reflecting investor confidence in the company’s financial health and growth prospects. The stock remains within its 52-week range of $34.63 to $43.20, suggesting potential for further growth.

The company’s consistent execution, focus on the underserved middle-income market, and strong financial performance continue to position it favorably within the insurance sector, despite challenges such as market shifts from Medicare Advantage to Medicare Supplement and impairment charges on past acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.