Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Codexis Inc (NASDAQ:CDXS) shared its corporate presentation on May 14, 2025, outlining the company’s strategic focus on enzymatic RNA manufacturing solutions, particularly for siRNA therapeutics. The presentation comes as the company’s stock trades at $2.47, near the lower end of its 52-week range of $1.90-$6.08, following a Q4 2024 earnings miss where the company reported revenue of $21.5 million against forecasts of $28.2 million.

The company is positioning itself at the intersection of two key trends: the growing adoption of RNA-based therapeutics and the manufacturing challenges associated with scaling production to meet potential demand for large indications. Codexis’s presentation emphasized its transition from technology development to commercial execution in 2025.

Strategic Initiatives

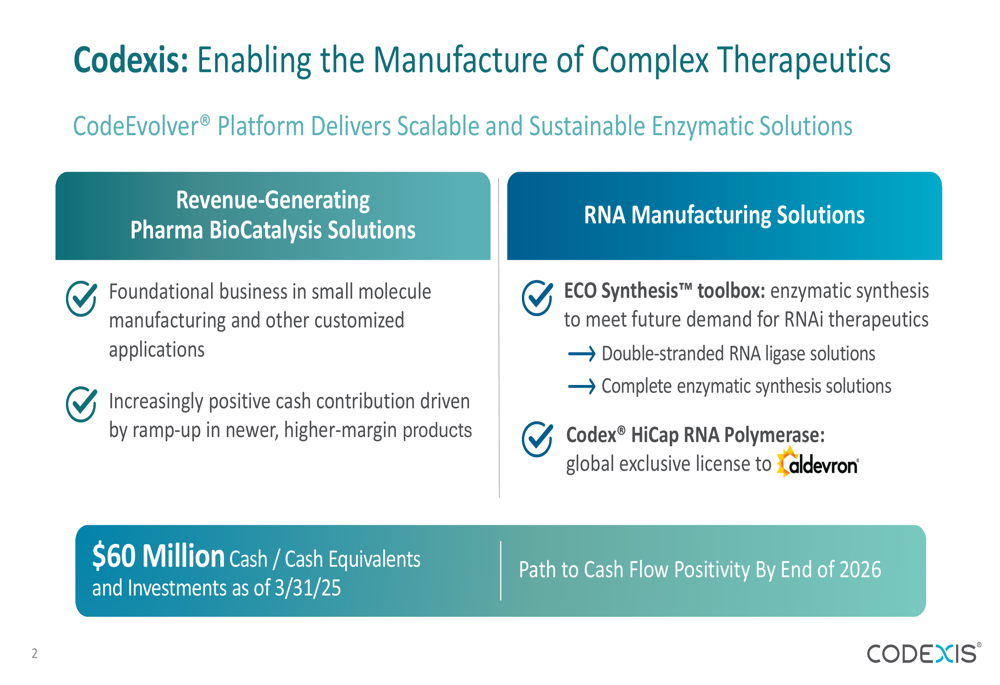

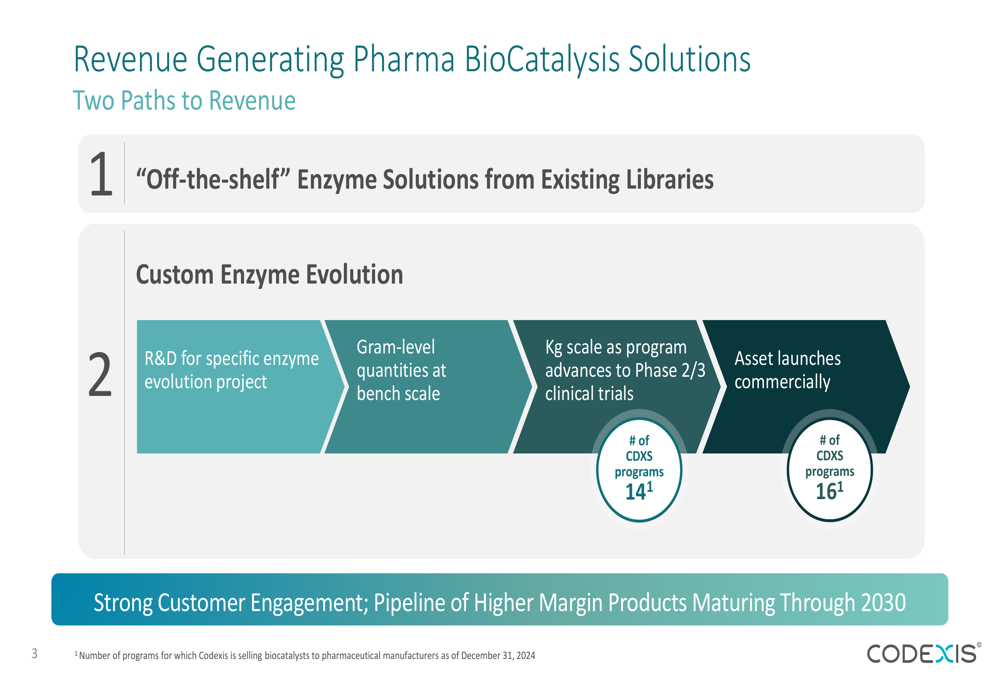

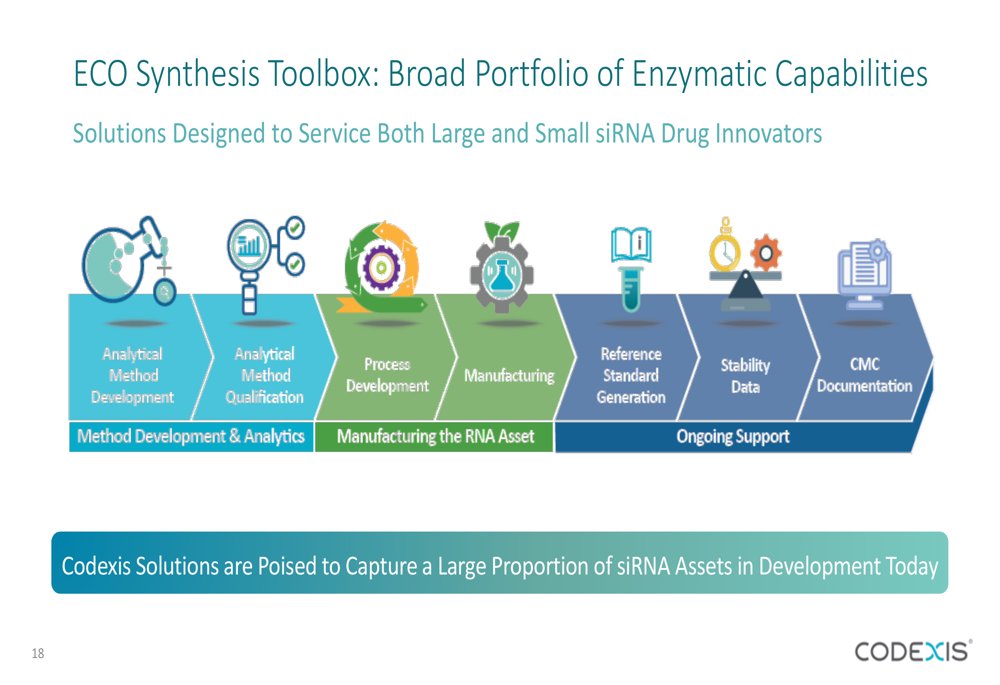

Codexis is focusing on two key business areas: Revenue-Generating Pharma BioCatalysis Solutions and RNA Manufacturing Solutions. The company highlighted its ECO Synthesis Toolbox, which includes technologies for RNA ligation, core technology for sequential incorporation of modified building blocks, raw materials production, and conjugation capabilities.

As shown in the following slide detailing the company’s business focus:

The ECO Synthesis Toolbox is designed to generate multiple revenue streams, including customized dsRNA ligases, siRNA production, process development fees, and eventually GMP material production. The company has completed construction of its ECO Synthesis Innovation Lab in December 2024, which will enable in-house manufacture of GLP-grade material for customers’ preclinical studies.

The company’s RNA manufacturing solutions are detailed in this comprehensive overview:

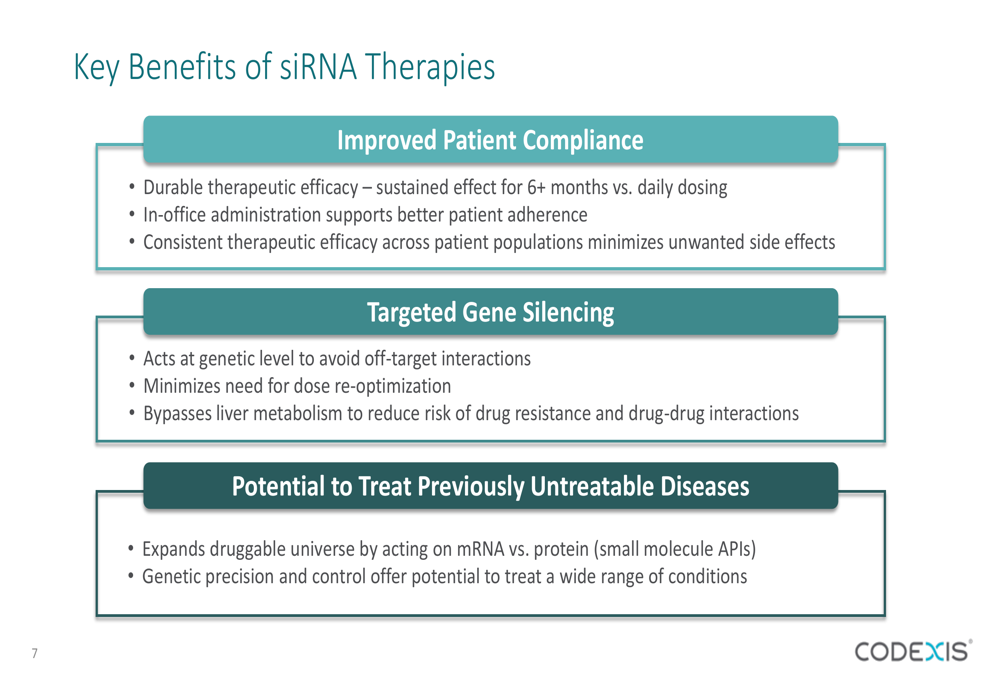

Codexis is particularly focused on siRNA therapeutics, noting that seven siRNA therapies have already received regulatory approval across multiple indications. The company highlighted that Inclisiran, approved in 2021 for hypercholesterolemia, was the first siRNA drug approved for a large indication affecting tens of millions of patients.

The following slide illustrates the current landscape of approved siRNA therapies:

Competitive Industry Position

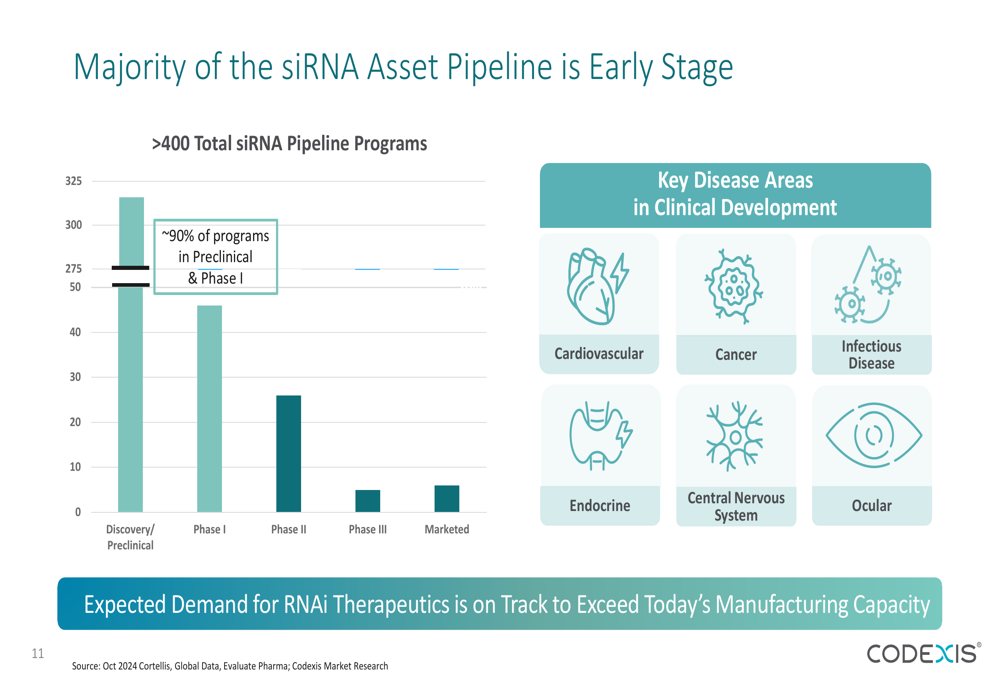

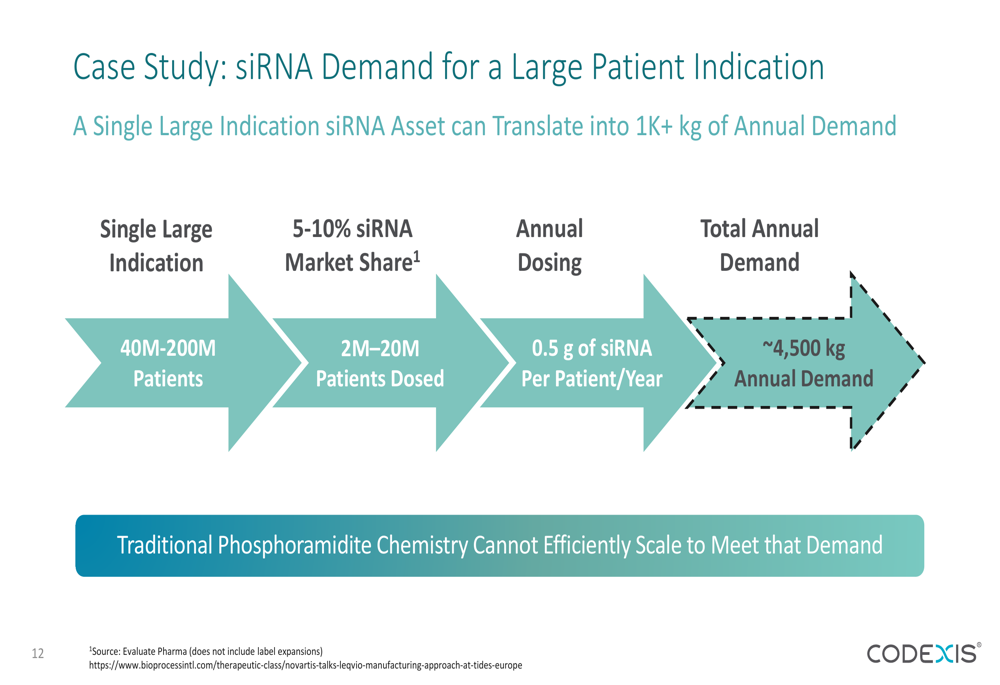

A central theme of Codexis’s presentation was the limitations of traditional chemical synthesis for RNA production and how its enzymatic approach offers significant advantages. The company presented a case study showing that a single large indication siRNA asset could translate into over 1,000 kg of annual demand, which would be difficult to meet using traditional methods.

This case study demonstrates the potential scale requirements for siRNA production:

Codexis emphasized that the capital expenditure required for chemical synthesis is prohibitively high, with $725 million needed for facilities capable of producing 1,000 kg of RNAi per year. The company cited Agilent (NYSE:A)’s real-world investment of $725 million for such capacity and projected that $10-20 billion in infrastructure investment would be needed to meet anticipated annual demand of approximately 30,000 kg by 2030.

The following slide details the CapEx challenges with traditional chemical synthesis:

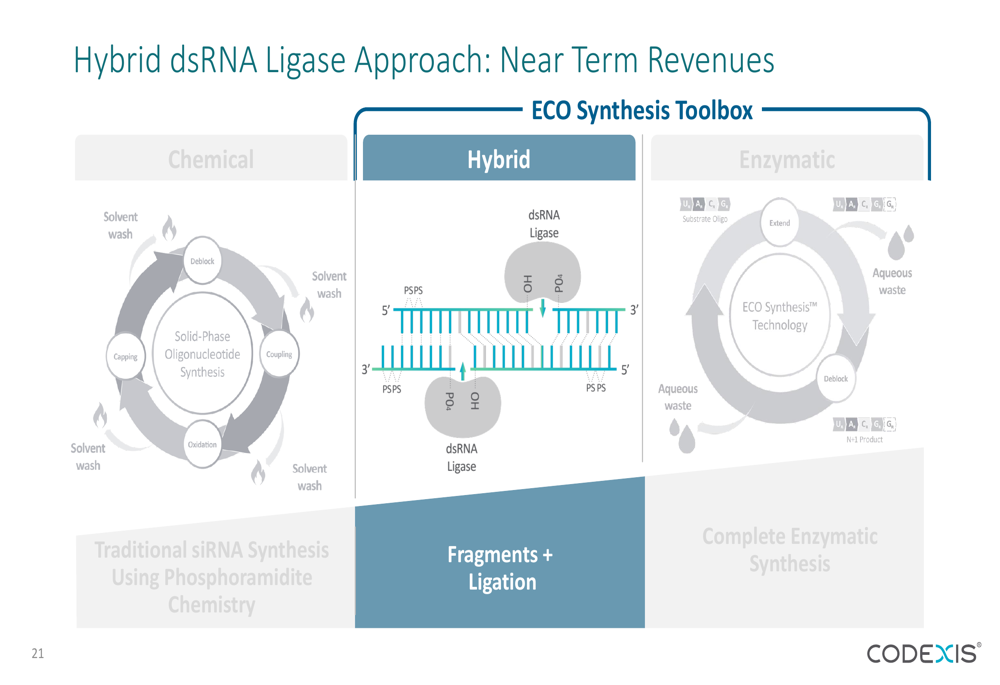

In contrast, Codexis claims its ECO Synthesis approach offers significant advantages, including 5x+ larger batch sizes (25-50 kg vs. 5-10 kg), 50% faster production time (6-11 months vs. 12-22 months), and 70% lower capital expenditure requirements ($150-210 million vs. $500-700 million).

The direct comparison between ECO Synthesis and traditional chemistry is presented here:

The company also highlighted the technical advantages of its engineered dsRNA ligases, which it claims dramatically outperform wild-type ligases. According to Codexis, its engineered ligases achieve target conversion rates of over 90% for all nicks in substrate design, compared to wild-type ligases that do not efficiently convert all nicks.

This technical advantage is illustrated in the following slide:

Financial Analysis

Despite the optimistic outlook presented in the corporate slides, Codexis’s recent financial performance has been challenging. The company reported a Q4 2024 EPS of -$0.13, missing the forecast of -$0.04, with revenue of $21.5 million falling short of the expected $28.2 million. Full-year 2024 revenue was $59.3 million, down from $62 million in 2023, though the net loss improved to $65.3 million from $84.4 million in 2023.

The presentation noted a cash position of $60 million as of March 31, 2025, and projected a path to cash flow positivity by the end of 2026. For 2025, the company has provided revenue guidance of $64-68 million, anticipating double-digit growth with significant revenue increases expected in the second half of the year.

Forward-Looking Statements

Codexis outlined several anticipated milestones for 2025, including:

- Achieving pilot scale production with the ECO Synthesis Innovation Lab for GLP material

- Signing a GMP scale-up partnership

- Securing the ECO Synthesis raw materials supply chain

- Presenting at TIDES USA & Europe annual meetings

- Converting a pipeline of 7+ potential customers into revenue-generating contracts

The company believes it is well-positioned to win in the enzymatic synthesis of RNAi therapeutics, citing its CodeEvolver platform, 20-year history in engineering solutions for complex therapeutics, and first-mover advantage in enzymatic RNA synthesis.

The following slide summarizes Codexis’s competitive positioning:

Analyst Perspectives

According to the earnings article, three analysts have recently revised their earnings estimates upward for Codexis, with price targets ranging from $3 to $11 per share, suggesting potential upside from current levels. The stock maintains a beta of 2.12, indicating higher volatility than the broader market.

The company’s strategic shift from bulk enzyme supply to more value-added drug supply and partnership services indicates a focus on long-term growth, though investors appear cautious given the recent earnings miss and the company’s continued net losses. The success of Codexis’s RNA manufacturing pivot will likely depend on its ability to convert its technological advantages into sustainable revenue growth and achieve its projected path to profitability by the end of 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.