ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Coeur Mining, Inc. (NYSE:CDE) reported record quarterly financial results for the third quarter of 2025, despite missing earnings per share (EPS) expectations. The company’s presentation, delivered on October 30, 2025, highlighted significant achievements in production, free cash flow, and balance sheet improvements, even as the stock fell 2.16% in regular trading and an additional 8.64% in premarket trading following the earnings release.

The precious metals miner reported adjusted EPS of $0.23, falling short of the $0.25 analyst consensus, representing an 8% negative surprise. However, revenue outperformed expectations at $554.6 million, exceeding forecasts by 6.32%, driven by strong metal prices and solid operational performance across its portfolio of North American mines.

Quarterly Performance Highlights

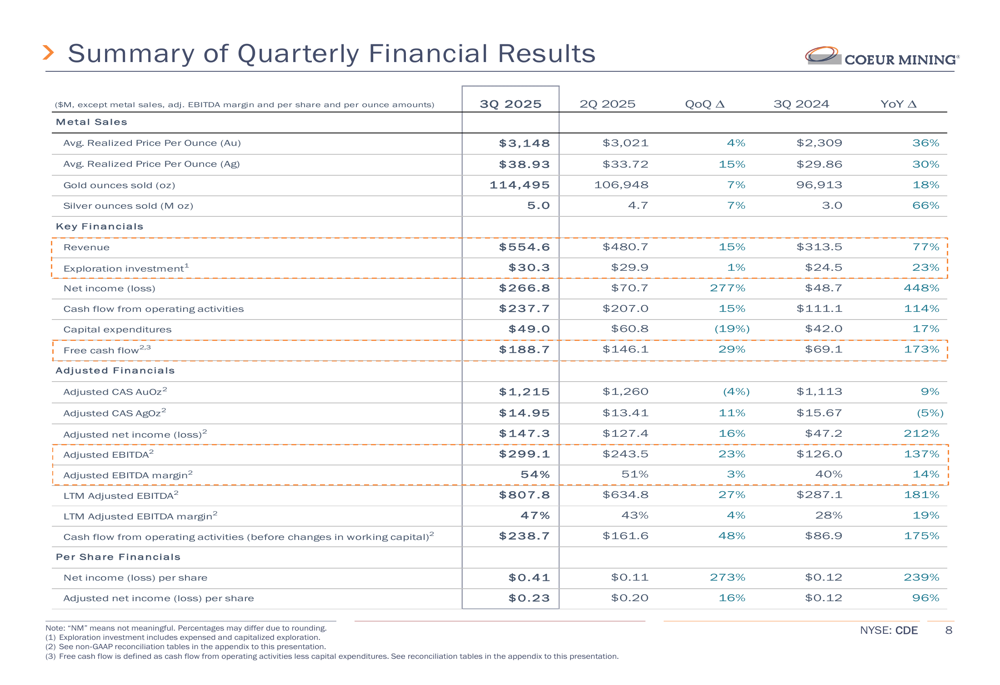

Coeur Mining achieved record quarterly production supported by solid cost performance across its operations. The company reported record quarterly net income of $266.8 million ($0.41 per share), significantly higher than the $70.7 million ($0.11 per share) reported in Q2 2025. Adjusted net income reached $147.3 million ($0.23 per share), up from $127.4 million ($0.20 per share) in the previous quarter.

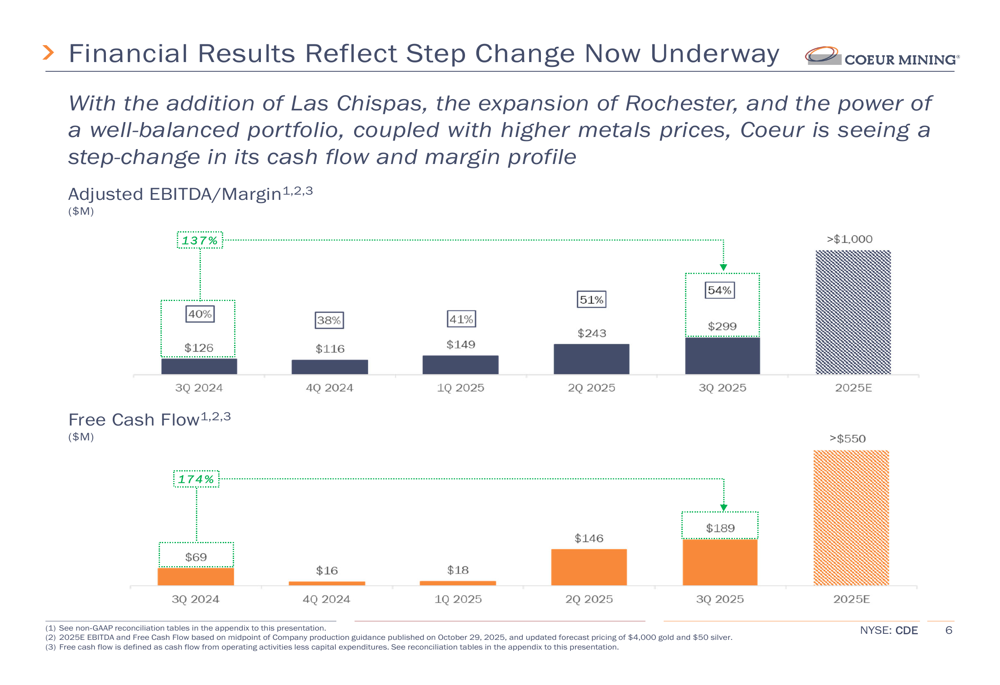

As shown in the following chart of Coeur’s financial performance, the company has experienced a substantial step-change in its results, with adjusted EBITDA reaching $299 million (54% margin) in Q3 2025, compared to $126 million (40% margin) in the same period last year:

The company’s free cash flow has also shown remarkable improvement, reaching $169 million in Q3 2025, compared to $69 million in Q3 2024. This represents approximately $2 million in free cash flow generation per day during the quarter, highlighting the company’s enhanced operational efficiency and favorable metal price environment.

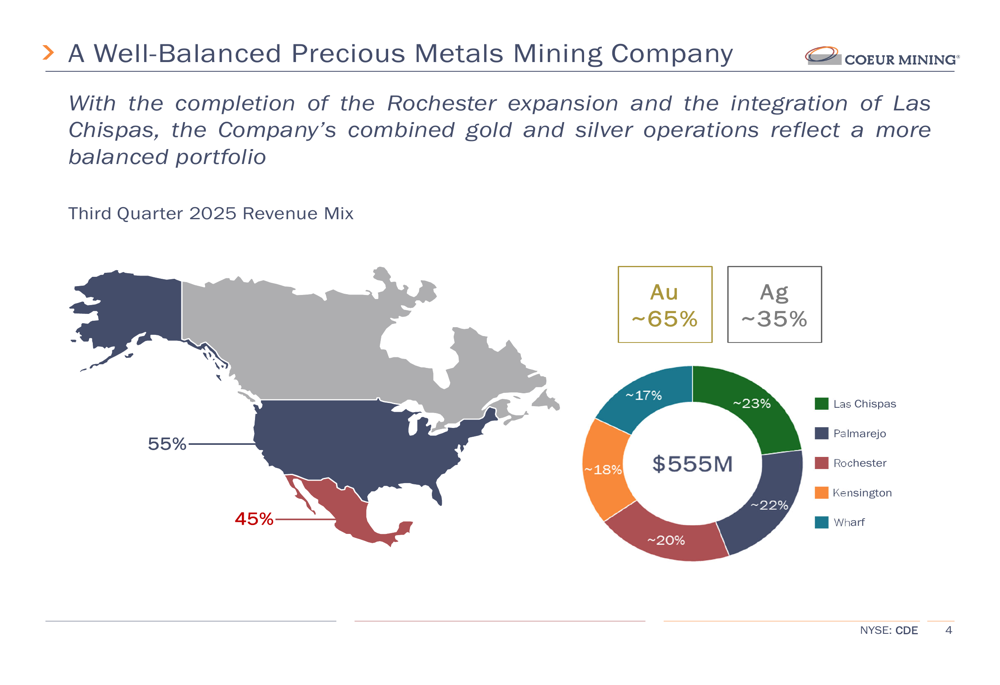

Revenue for the quarter was well-balanced across Coeur’s portfolio of mines, with gold contributing approximately 65% and silver 35% of the total $555 million. The revenue distribution by mine shows a diversified portfolio: Palmarejo (~23%), Kensington (~22%), Rochester (~20%), Wharf (~18%), and Las Chispas (~17%).

As illustrated in the following map and revenue breakdown:

Detailed Financial Analysis

The third quarter saw Coeur Mining benefit from higher realized metal prices, with gold averaging $3,148 per ounce (compared to $2,309 in Q3 2024) and silver averaging $38.93 per ounce (versus $29.86 in Q3 2024). Gold sales increased to 114,495 ounces, up from 96,913 ounces in the same period last year, while silver sales rose to 5.0 million ounces from 3.0 million ounces.

The comprehensive quarterly financial results show significant improvements across all key metrics:

Operating cash flow reached $237.7 million, up from $111.1 million in Q3 2024, while capital expenditures remained relatively controlled at $49.0 million compared to $42.0 million in the prior-year period. This disciplined approach to capital allocation has contributed to the company’s strong free cash flow generation.

Balance Sheet Improvements

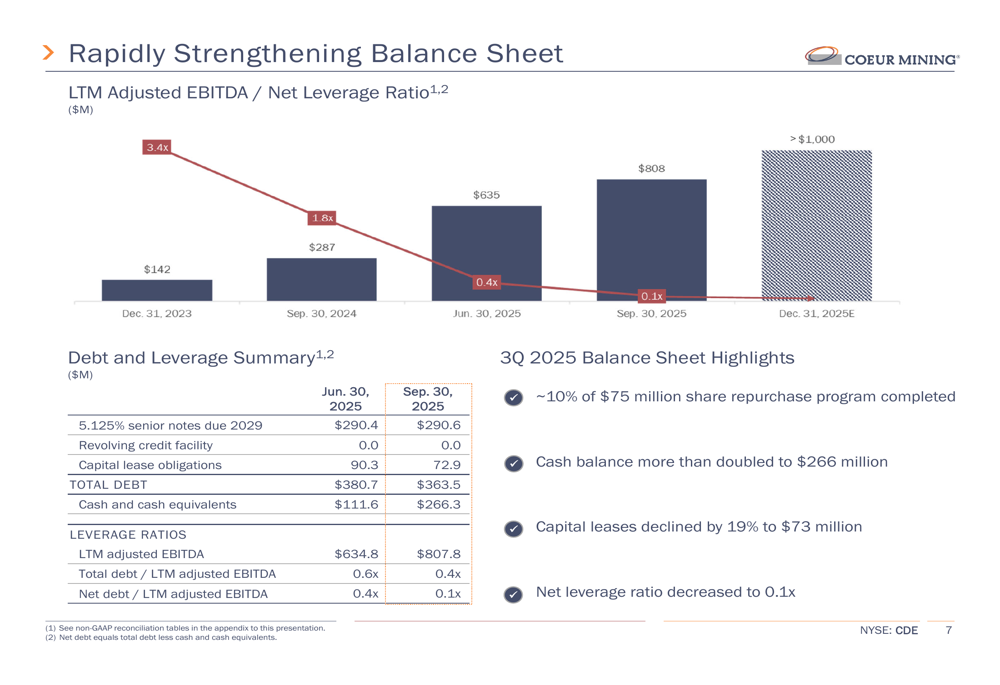

One of the most notable achievements in Q3 2025 was the significant strengthening of Coeur’s balance sheet. The cash balance more than doubled to $266.3 million from $111.6 million at the end of Q2 2025, while total debt decreased to $363.5 million from $380.7 million.

The company’s net leverage ratio fell dramatically to just 0.1x adjusted EBITDA, down from 0.4x in the previous quarter and 1.8x a year ago. This rapid deleveraging positions Coeur with substantial financial flexibility for future growth initiatives and shareholder returns.

As shown in the following chart of the company’s balance sheet evolution:

Coeur has also initiated a share repurchase program, with approximately 10% of the $75 million authorization completed during the quarter. This reflects management’s confidence in the company’s financial position and commitment to returning value to shareholders.

Operational Highlights

Gold production for Q3 2025 reached 111,364 ounces, bringing the year-to-date total to 306,617 ounces, representing 74% progress toward the company’s full-year guidance. Silver production totaled 4,756,000 ounces for the quarter and 13,207,000 ounces year-to-date, marking 73% progress toward annual guidance.

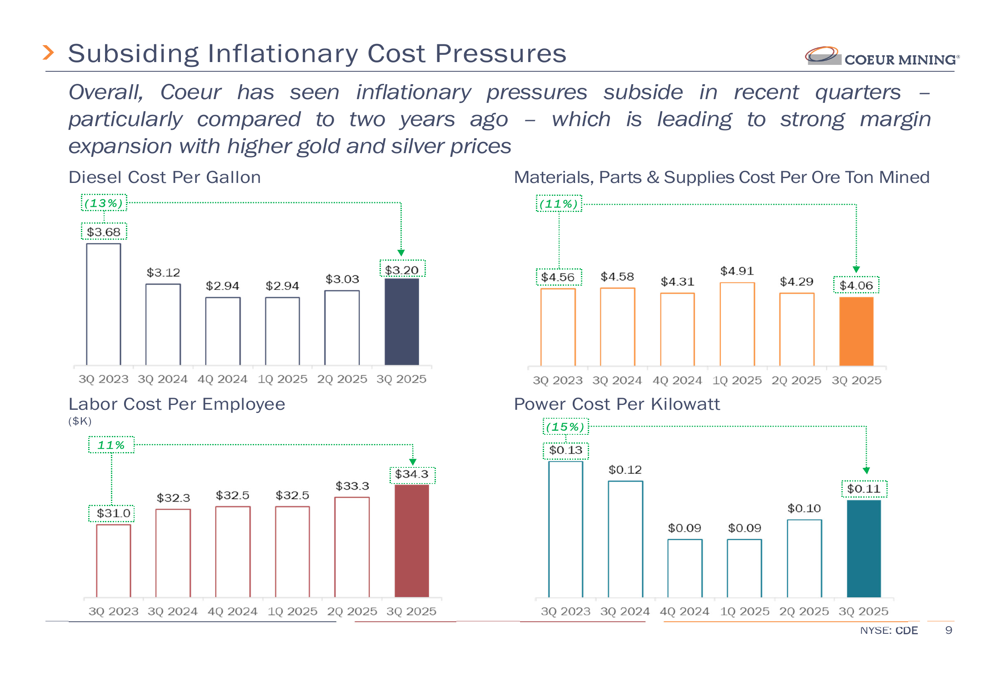

The company has benefited from subsiding inflationary cost pressures across most categories, helping to maintain competitive cost structures. As illustrated in the following chart:

While labor costs have seen a modest increase, materials, parts, and supplies costs per ore ton mined have decreased to $4.06 in Q3 2025 from $4.56 in Q3 2023. Power costs have also declined slightly year-over-year, contributing to overall cost stability.

The Rochester expansion, a significant growth project for Coeur, is now operational and showing improving performance with increasing free cash flow. The mine generated $29.6 million in free cash flow during Q3 2025, a substantial improvement from a negative $6.9 million in Q3 2024.

Strategic Initiatives

Coeur Mining continues to invest in exploration to drive organic growth, with a planned investment of $85 million for 2025, significantly higher than in previous years. This strategic focus on exploration aims to extend mine lives and identify new opportunities within the company’s existing property portfolio.

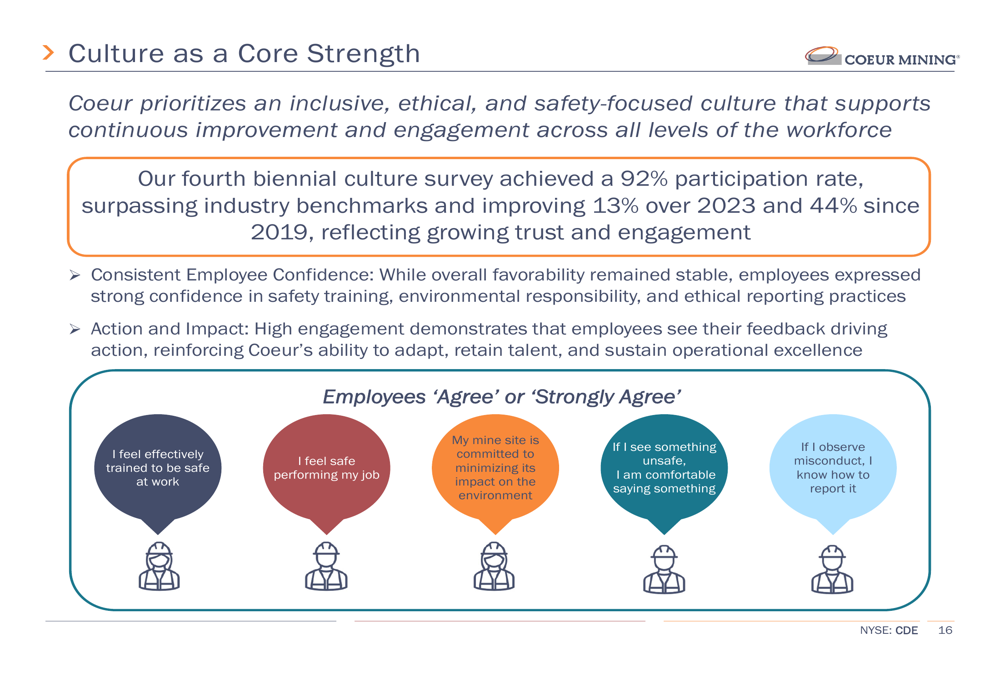

The company also emphasizes its strong corporate culture as a core competitive advantage. The recent biennial culture survey achieved a 92% participation rate, surpassing industry benchmarks and improving 13% over 2023 and 44% since 2019, reflecting growing trust and engagement among employees.

As illustrated in the following culture survey results:

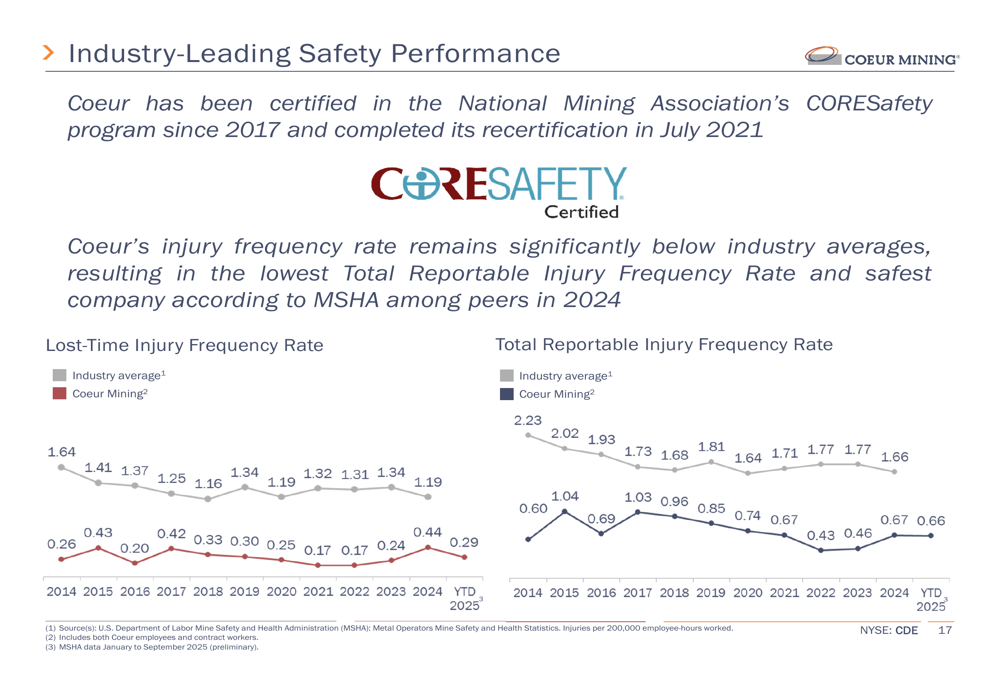

Safety performance remains a priority for Coeur, with injury frequency rates consistently below industry averages. The company has maintained certification in the National Mining Association’s CORESafety program since 2017 and completed its recertification in July 2021.

The following chart demonstrates Coeur’s industry-leading safety performance:

Forward-Looking Statements

Based on the strong performance through the first nine months of 2025, Coeur has increased its full-year EBITDA target to exceed $1 billion and its free cash flow target to exceed $550 million. The company has also refined its production guidance ranges, particularly for Las Chispas, where gold production guidance has been increased to 50,000-58,000 ounces (from 42,500-52,500 ounces previously).

Key deliverables for the fourth quarter of 2025 include:

- Maintaining sector-leading safety performance

- Continuing to deliver higher crushing rates at targeted particle size distribution at Rochester

- Building cash and further strengthening the balance sheet

- Delivering results from high-return exploration investments

- Carrying out exploration program at Silvertip to support Initial Assessment

- Continuing share repurchases under the $75 million program

Analyst Perspectives

Despite the strong operational and financial performance, analysts expressed concerns about the EPS miss during the earnings call. Questions focused on challenges at the Rochester mine, potential mergers and acquisitions, tax asset implications, and processing strategies for lower-grade ore.

The market reaction to the earnings release was notably negative, with the stock trading down significantly in both regular and premarket sessions. This suggests investors may have been focused on the earnings miss rather than the record operational performance and strengthened balance sheet.

The stock’s current trading level represents a significant discount to its 52-week high of $23.615, potentially reflecting ongoing concerns about the sustainability of current metal prices and the company’s ability to consistently meet earnings expectations despite strong operational performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.