TSX drops after Canadian index edges higher in prior session

Introduction & Market Context

Colgate-Palmolive Company (NYSE:CL) presented its second quarter 2025 earnings results on August 1, highlighting modest growth in a challenging operating environment. The $20.1 billion global consumer products company, which employs approximately 34,000 people serving over 200 countries, reported growth in both net sales and earnings per share despite facing headwinds from raw material inflation.

The company’s stock showed a slight positive reaction, rising 0.12% to $75.82 in premarket trading following the presentation. Colgate-Palmolive remains focused on its four core product categories: Oral Care, Pet Nutrition, Personal Care, and Home Care.

Quarterly Performance Highlights

In the second quarter of 2025, Colgate-Palmolive reported net sales growth of 1.0% and organic sales growth of 1.8%, which included a 0.6% negative impact from lower private label pet sales. Base Business earnings per share increased by 1%, while the company’s global toothpaste market share improved by 20 basis points on a volume basis year to date.

CEO Noel Wallace highlighted the company’s performance in his presentation statement: "We achieved another quarter of net sales, organic sales, and earnings per share growth despite difficult market conditions. Organic sales growth improved sequentially versus the first quarter, even with a negative impact from lower private label pet sales."

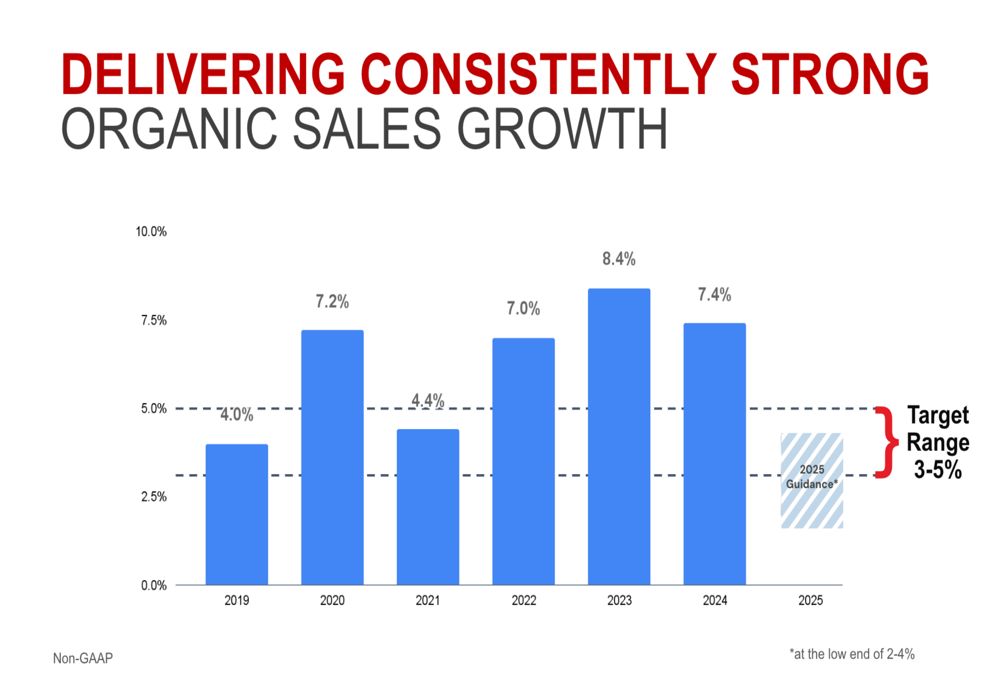

The company has maintained a consistent track record of organic sales growth over recent years, as illustrated in the following chart:

The earnings presentation data shows slightly different organic sales growth figures compared to the earnings call transcript, which mentioned 2.4% growth. This discrepancy may be due to adjustments or different calculation methodologies.

Strategic Initiatives

A key announcement in the presentation was Colgate-Palmolive’s new three-year productivity program designed to drive future growth and support the company’s 2030 strategy. The program includes initiatives to align organizational structure, optimize the global supply chain, and streamline operations to reduce overhead costs. The company projects cumulative pre-tax charges totaling between $200 and $300 million over the course of the three years.

The company is also focusing on driving operating leverage and cash flow through revenue growth management, strong funding-the-growth savings, and generating robust operating cash flow to fund dividends and share repurchases.

Raw material costs remain a challenge, with the company noting that expectations for underlying raw and packaging material cost inflation have risen due to continued increases in fats and oils, particularly palm kernel oil. However, the impact of tariffs is now expected to be approximately $75 million, down from the previous estimate of $200 million provided in April 2025.

Product Innovation Focus

Colgate-Palmolive emphasized its strategy of driving growth through science-led innovation across its product portfolio. The presentation showcased several new premium products designed to capture higher price points and improve margins.

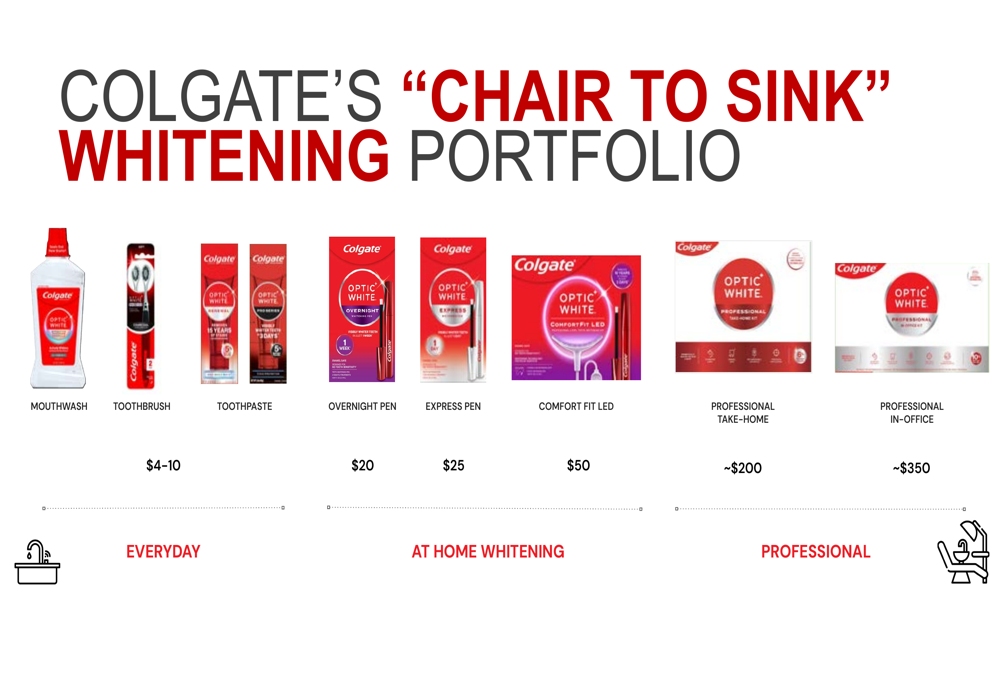

In the oral care segment, the company highlighted its comprehensive whitening portfolio, which spans from everyday products priced at $4-10 to professional in-office solutions at around $350, demonstrating the company’s range and premium positioning strategy:

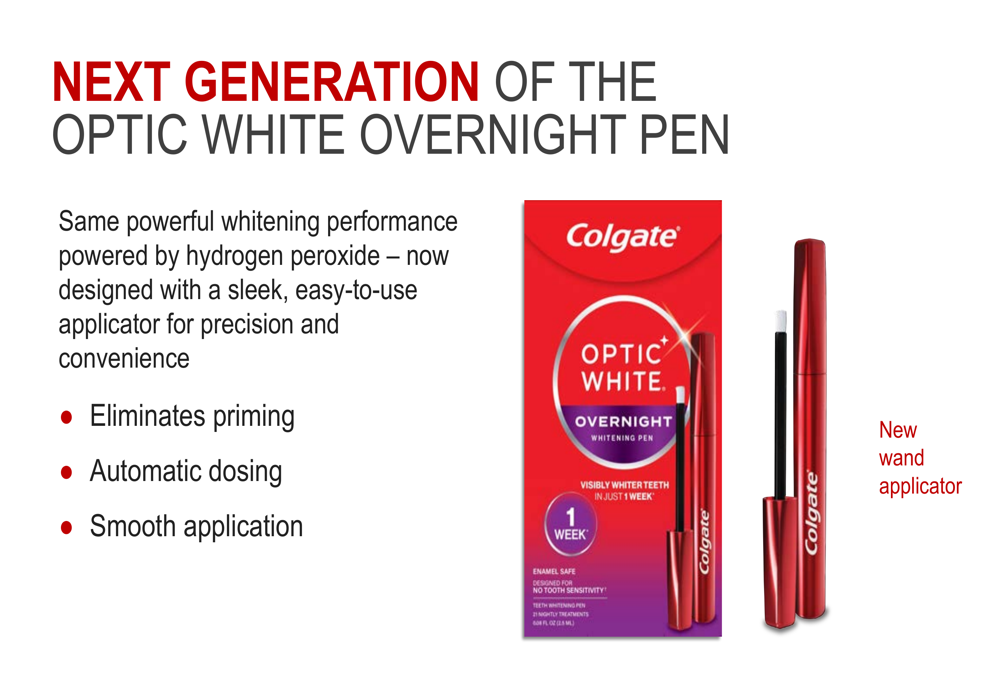

The company is introducing next-generation products like the Optic White Overnight Pen, featuring the same powerful whitening performance but with an improved applicator for precision and convenience:

Colgate-Palmolive is also accelerating whitening adoption with its Purple Range, which offers whitening capability and stain removal with an enamel-safe coating:

The presentation showcased market-specific innovations tailored to regional preferences, including the Miracle Repair Serum Toothpaste for China, Colgate Strong Teeth relaunch in India, and various personal care products like Protex Bar Soap in Latin America and Palmolive Naturals in Europe.

In the pet nutrition segment, the company highlighted the Science Diet Core Lifestage Portfolio relaunch with upgraded ActivBiome+ Multi-Benefit formula and new Prescription Diet options for complex cases. The acquisition of the Prime100 fresh pet food business, which closed on April 30, 2025, further strengthens the company’s position in this category.

Forward-Looking Statements

For 2025, Colgate-Palmolive updated its guidance, now expecting organic sales growth to be at the low end of the previously announced 2% to 4% range, including the impact of the planned exit from private label pet sales. Net sales growth is still expected to be up low single digits, including a flat to low-single-digit negative impact from foreign exchange.

The company maintained its projection for gross profit margin to be roughly flat and advertising to remain flat as a percentage of net sales. Base Business EPS is still expected to grow at a low single-digit rate.

Looking at longer-term trends, Colgate-Palmolive’s 2025 guidance target range of 3-5% organic sales growth represents a moderation from the stronger growth rates seen in recent years (7.4% in 2024 and 8.4% in 2023), reflecting the more challenging economic environment.

The company’s focus on premium innovation, productivity improvements, and strategic acquisitions demonstrates its commitment to navigating the current headwinds while positioning itself for sustainable long-term growth in its core categories.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.