Boeing secures $883 million Army contract for cargo support services

Introduction & Market Context

Columbia Banking System (NASDAQ:COLB) presented its second quarter 2025 earnings results on July 24, 2025, reporting improved financial performance as the company prepares to complete its acquisition of Pacific Premier Bancorp (NASDAQ:PPBI). Despite the positive operating results, Columbia’s stock declined 4.22% on the day of the presentation, closing at $24.38.

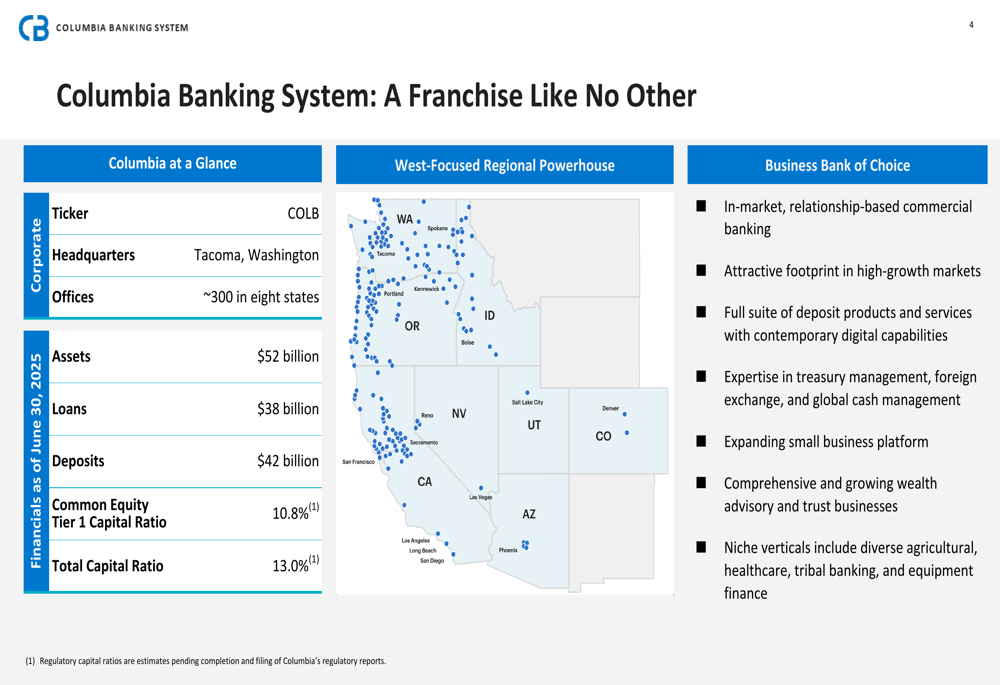

The Tacoma, Washington-based regional bank reported operating earnings per share of $0.76 for Q2 2025, continuing the positive momentum from Q1 when it beat analyst expectations with EPS of $0.67. The company’s presentation highlighted its position as a regional powerhouse in the Western United States with approximately $52 billion in assets.

As shown in the following overview of Columbia Banking System’s franchise:

Quarterly Performance Highlights

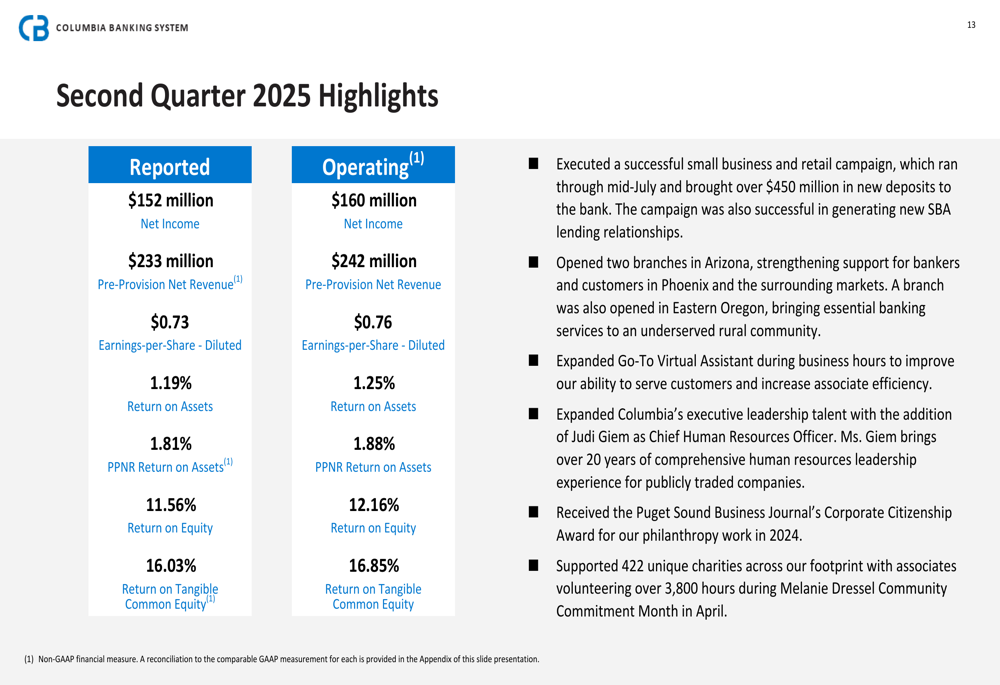

Columbia reported Q2 2025 net income of $152 million, or $0.73 per diluted share, while operating net income reached $160 million, or $0.76 per diluted share. The company’s return on assets improved to 1.19% (reported) and 1.25% (operating), while return on tangible common equity reached 16.03% (reported) and 16.85% (operating).

For the first half of 2025, Columbia reported net income of $239 million ($1.14 per share), while operating net income totaled $300 million ($1.43 per share). The company’s pre-provision net revenue (PPNR) reached $233 million for Q2 and $384 million year-to-date.

The following chart details Columbia’s second quarter 2025 financial performance:

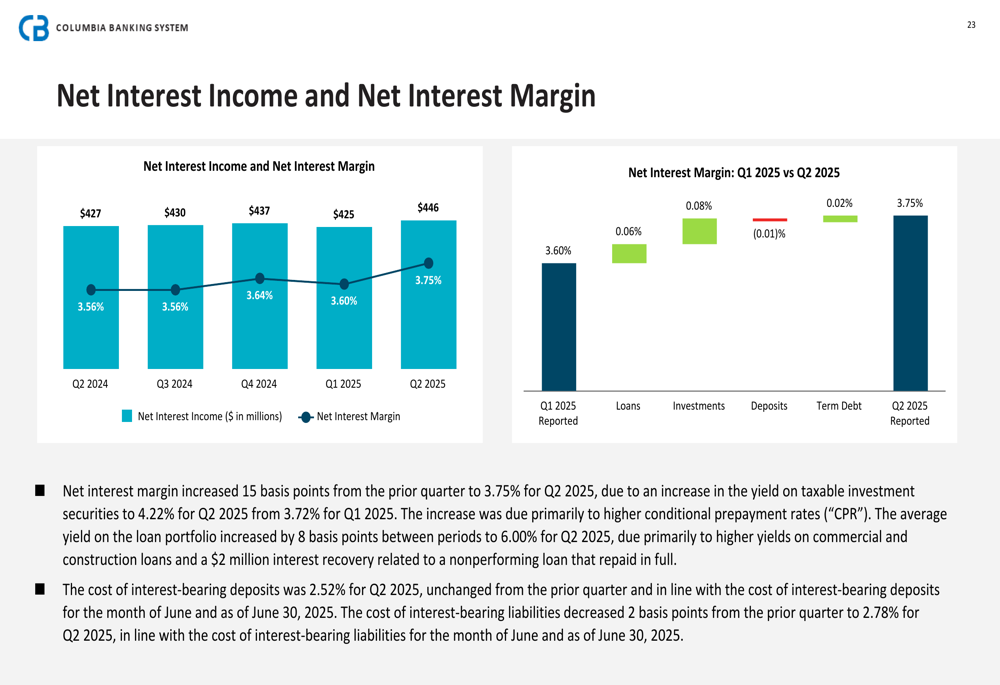

Net interest margin, a key profitability metric for banks, increased 15 basis points from the prior quarter to 3.75% for Q2 2025. This improvement was driven by higher yields on earning assets, while the cost of interest-bearing liabilities decreased 2 basis points to 2.78%.

As illustrated in this chart showing the net interest income and margin trends:

Strategic Initiatives

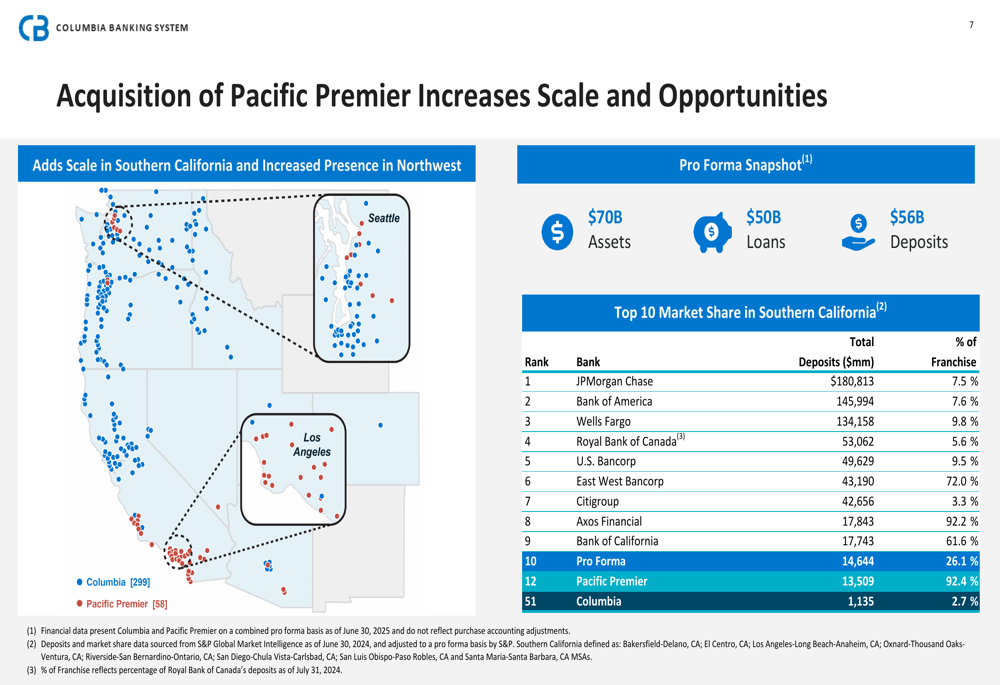

The most significant strategic development highlighted in Columbia’s presentation is the pending acquisition of Pacific Premier Bancorp, expected to close on September 1, 2025. This 100% common stock transaction will create a combined organization with approximately $70 billion in assets, operating under the Columbia Bank brand.

The acquisition is designed to accelerate Columbia’s Southern California expansion strategy and enhance its competitive position throughout the Western United States. Management projects the deal will provide 14% EPS accretion in 2026, with initial tangible book value dilution recovered within three years.

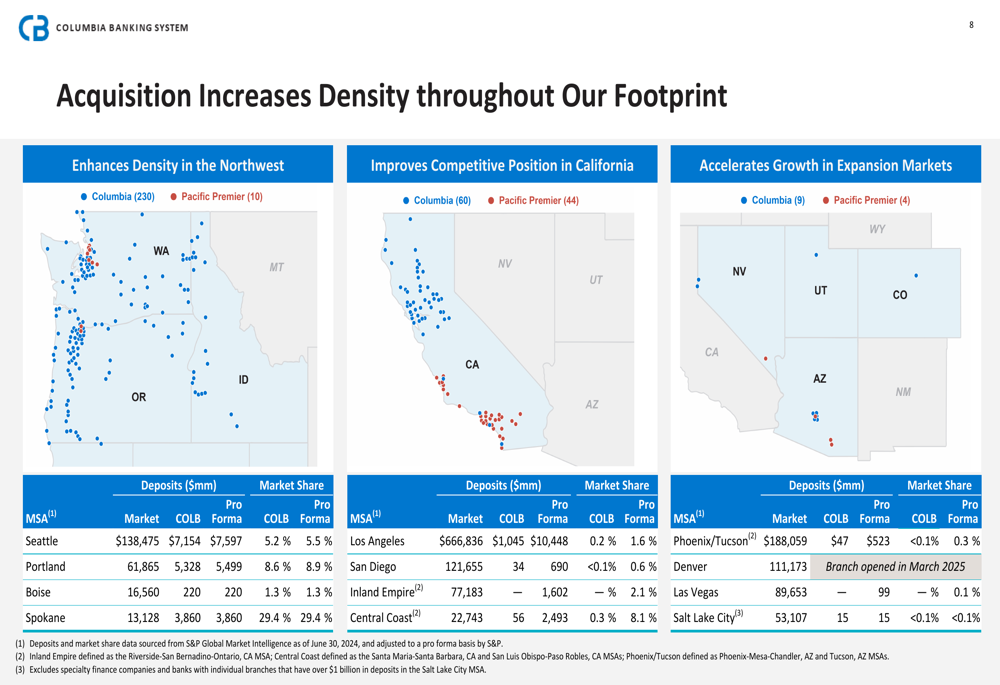

The following map illustrates how the acquisition will strengthen Columbia’s presence in key markets:

The combined entity will significantly improve Columbia’s competitive position in California markets, particularly in Los Angeles where its deposit market share will increase from 0.2% to 1.6%. The acquisition also enhances density in the Northwest, where Columbia already holds a strong position as the fifth-largest bank by market share.

As shown in this detailed breakdown of market density improvements:

Detailed Financial Analysis

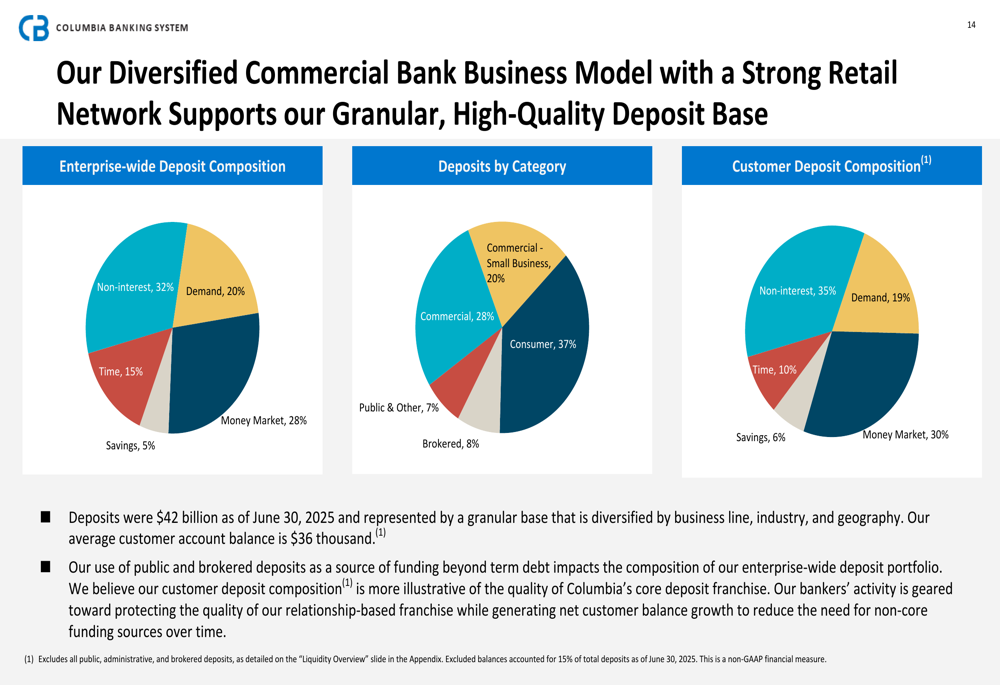

Columbia maintains a diversified deposit base with 35% non-interest bearing deposits among customer accounts. The bank’s average customer account balance is $36,000, reflecting its focus on relationship-based commercial banking and small business services.

The following chart illustrates Columbia’s deposit composition:

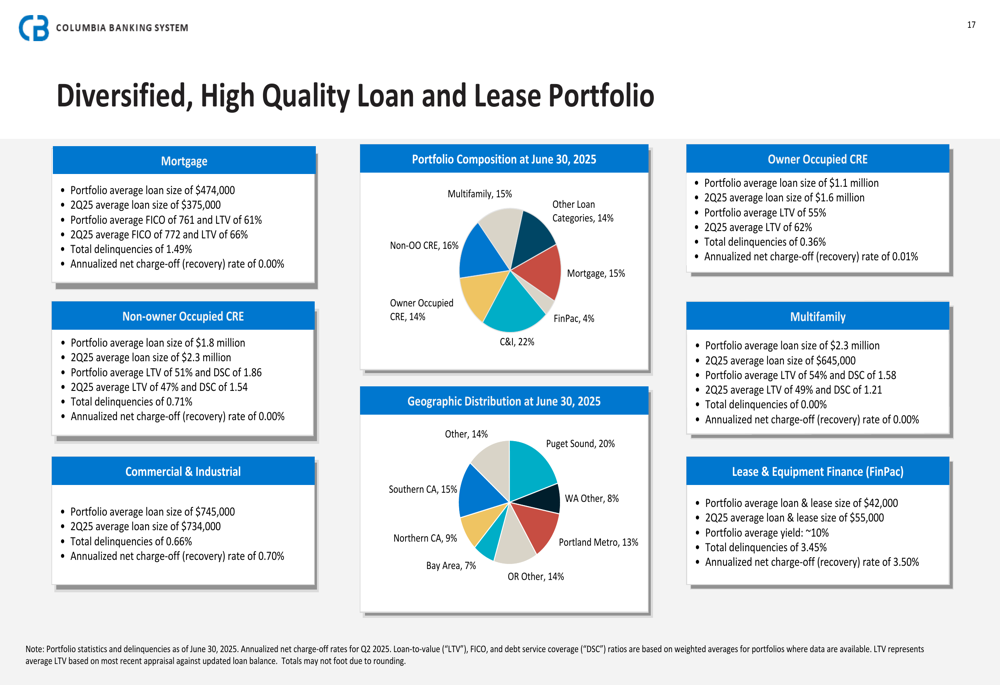

The bank’s loan portfolio remains diversified and of high quality, with strong metrics across mortgage, commercial real estate, commercial & industrial, and lease & equipment finance segments. The portfolio is geographically distributed across the Western United States, with significant concentrations in the Puget Sound, Portland Metro, and California regions.

As shown in this breakdown of Columbia’s loan portfolio:

Credit quality remains strong, with the allowance for credit losses at appropriate levels relative to the portfolio risk. Net charge-offs in the FinPac portfolio were $14 million in Q2 2025, while nonperforming loans of $177 million included $68 million of loans with government guarantees.

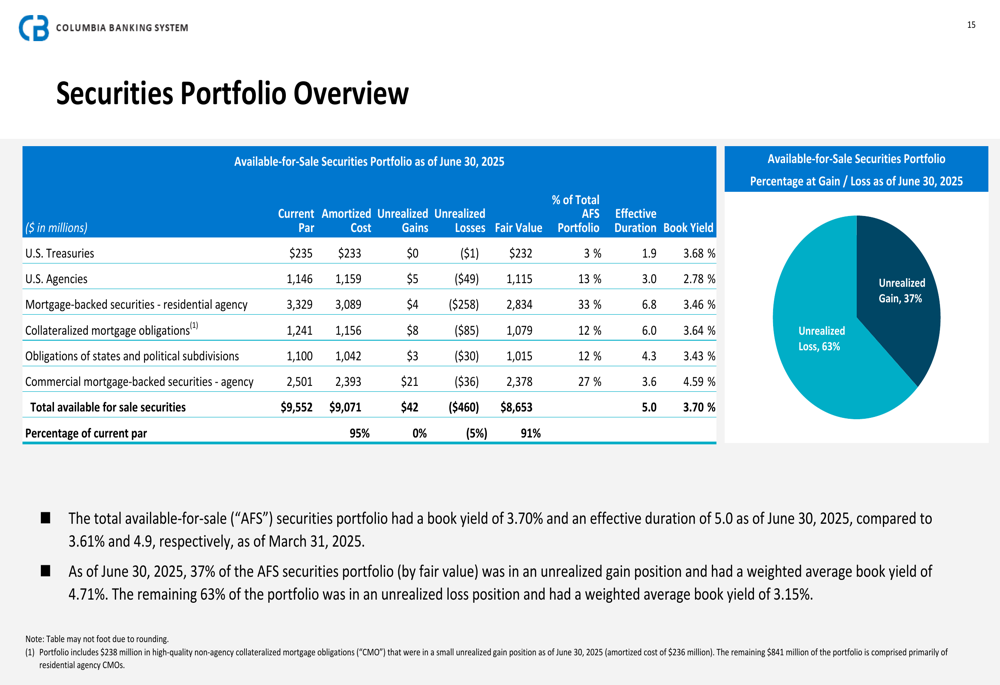

The securities portfolio shows 37% of available-for-sale securities in an unrealized gain position with a weighted average book yield of 4.71%, while 63% remain in an unrealized loss position with a weighted average book yield of 3.15%.

Forward-Looking Statements

Columbia’s capital position remains strong, with a Common Equity Tier 1 (CET1) ratio of 10.8% and a total capital ratio of 13.0% as of June 30, 2025. Management emphasized that the bank has generated over 85 basis points of net capital during the period, supporting its long-term organic growth and shareholder returns.

The company continues to expand its physical presence, having opened two branches in Arizona during Q2 while also enhancing its digital capabilities. Columbia is leveraging technology to improve operational efficiencies, enhance customer experience, and drive revenue generation through AI-powered "Smart Leads" and new payment technologies.

Looking ahead, Columbia is focused on successfully integrating Pacific Premier Bancorp while continuing to execute its Business Bank of Choice strategy. The company expects to benefit from operating in high-growth Western markets, where current household income is 106% of the national average with a five-year growth rate of 9.0%.

As illustrated in this overview of Columbia’s attractive Western markets:

While the presentation highlights numerous positive aspects of the Pacific Premier acquisition, investors should note potential integration challenges as mentioned in previous earnings discussions. The company’s stock performance may continue to face pressure despite strong operating results as the market assesses the execution risks associated with the acquisition and broader economic uncertainties affecting the banking sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.