Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Columbia Banking System (NASDAQ:COLB) delivered stronger-than-expected third quarter 2025 results, as revealed in its October 30 earnings presentation. The west-focused regional bank reported operating earnings per share of $0.85, significantly exceeding analyst forecasts of $0.69, representing a 23.19% positive surprise. Despite these strong results, Columbia’s stock closed down 1.33% at $26.35, though it showed slight recovery in aftermarket trading.

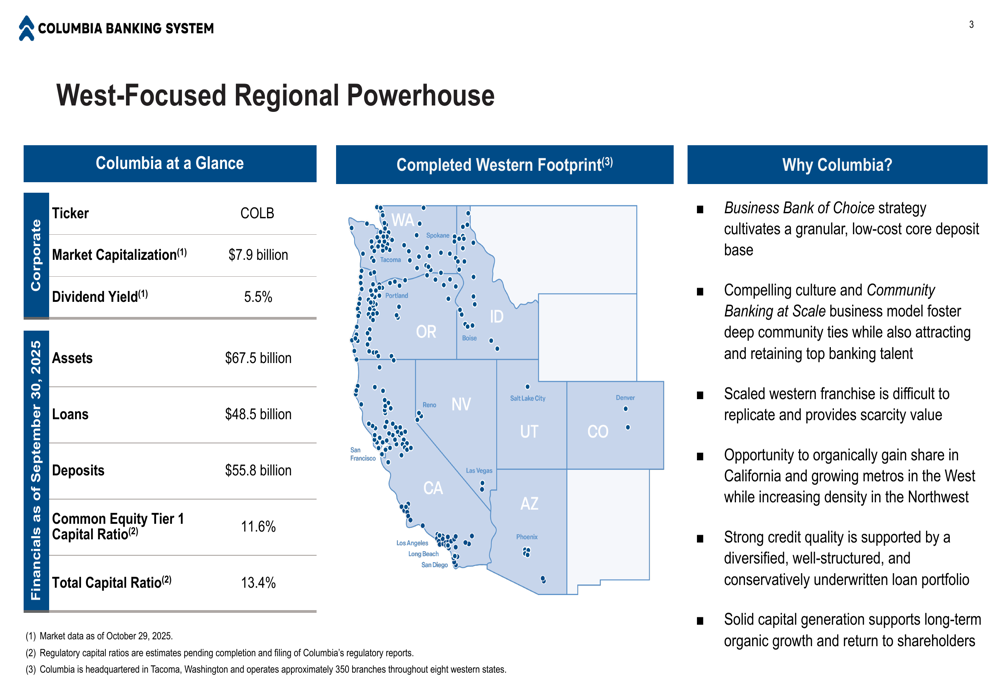

With a market capitalization of $7.9 billion and a dividend yield of 5.5%, Columbia has positioned itself as a significant player in the western United States banking landscape. The company’s recent acquisition of Pacific Premier Bancorp, which closed on August 31, 2025, has further strengthened its competitive position as the fourth largest regional bank headquartered in its footprint.

Quarterly Performance Highlights

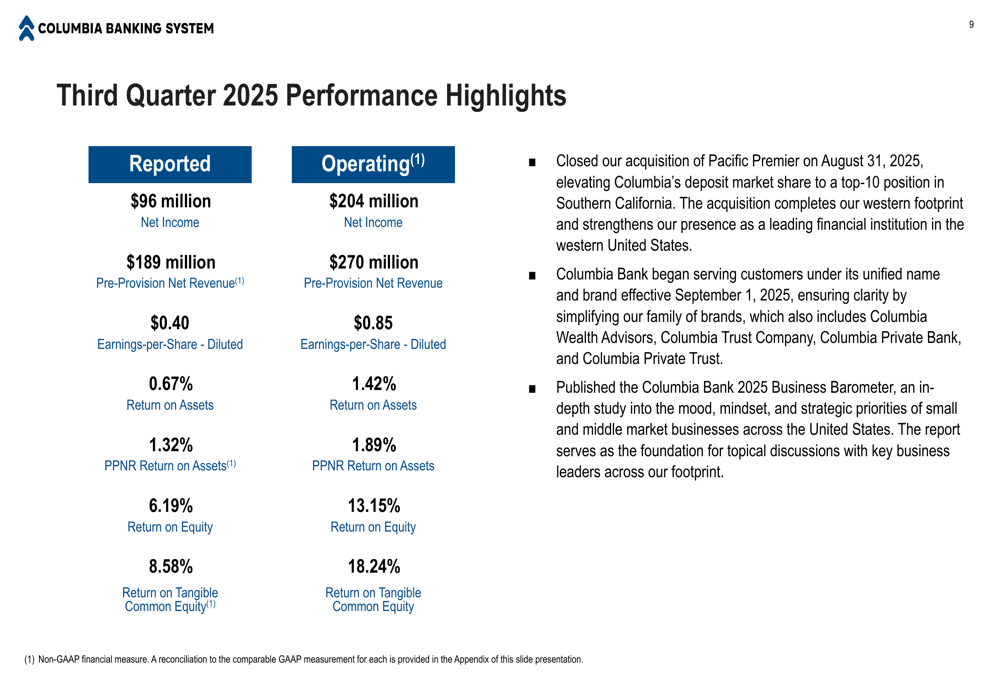

Columbia Banking’s third quarter 2025 results demonstrated substantial improvement across key metrics. The company reported operating net income of $204 million, compared to reported net income of $96 million. Operating pre-provision net revenue (PPNR) reached $270 million, while reported PPNR was $189 million.

As shown in the following performance highlights chart, the bank achieved an operating return on assets of 1.42% and an operating return on tangible common equity of 18.24%, significantly outperforming reported figures:

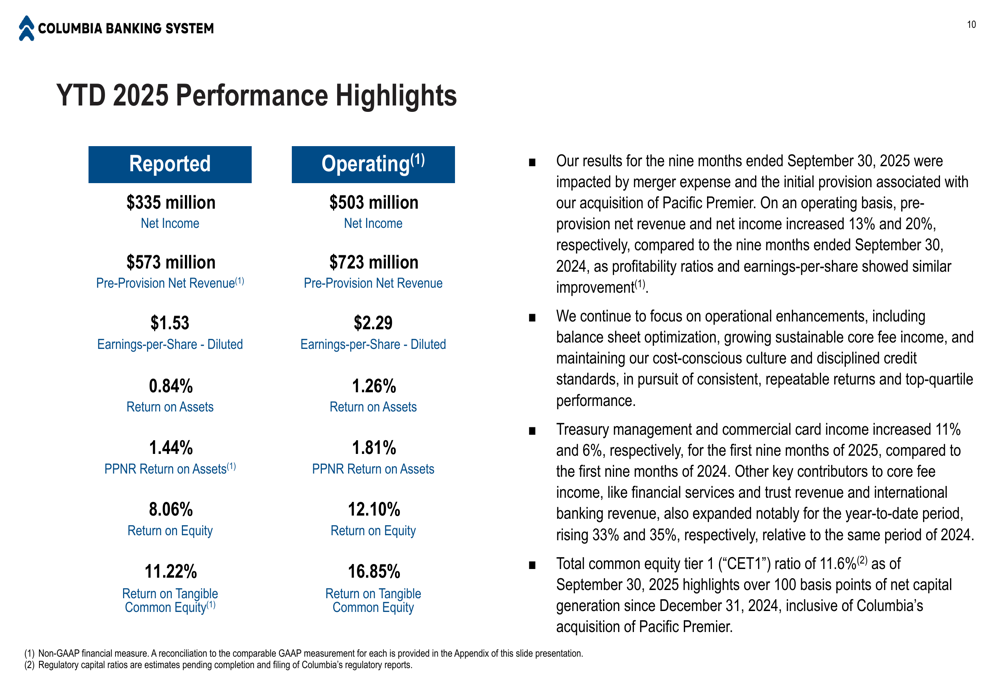

Year-to-date performance also showed strong momentum, with operating net income of $503 million and operating EPS of $2.29 for the first nine months of 2025. The operating return on tangible common equity for this period stood at 16.85%.

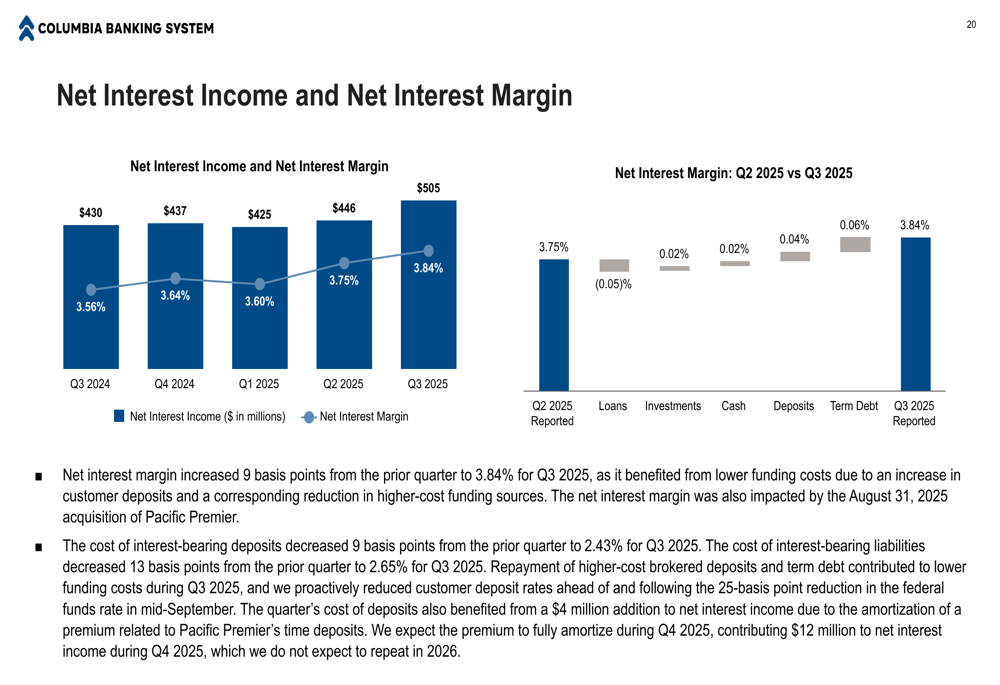

Net interest income and margin showed consistent improvement throughout 2025, with the net interest margin increasing to 3.84% in Q3 2025 from 3.75% in the previous quarter. This expansion was driven by higher yields on loans and improved funding mix following the Pacific Premier acquisition.

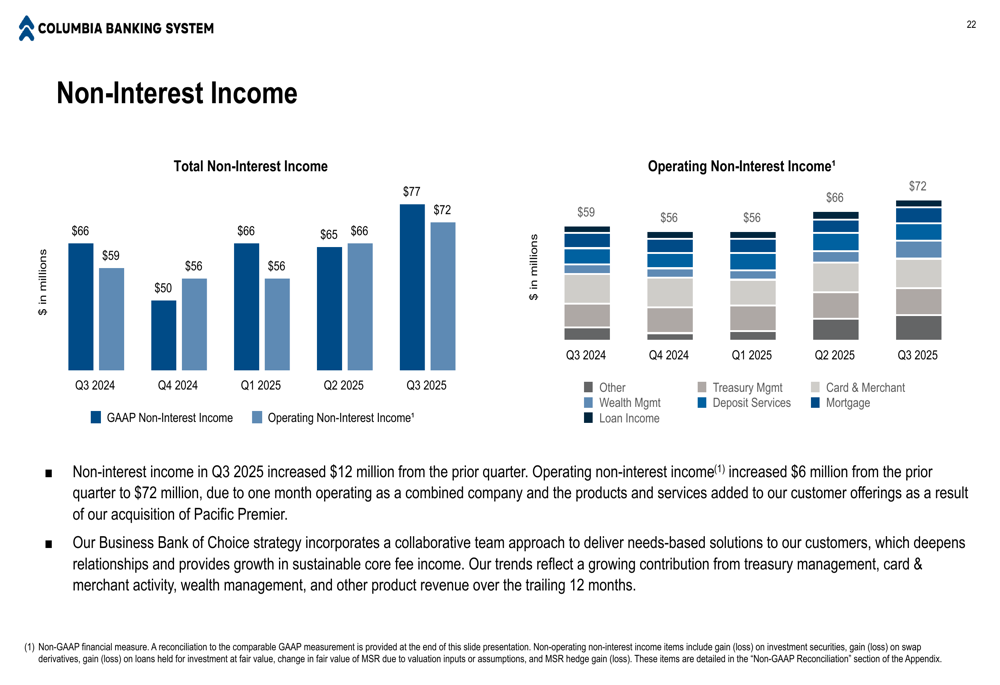

Non-interest income also showed positive momentum, increasing to $77 million in Q3 2025 from $65 million in the previous quarter. This growth reflects Columbia’s success in implementing its "Business Bank of Choice" strategy, which focuses on delivering needs-based solutions to customers.

Pacific Premier Acquisition Impact

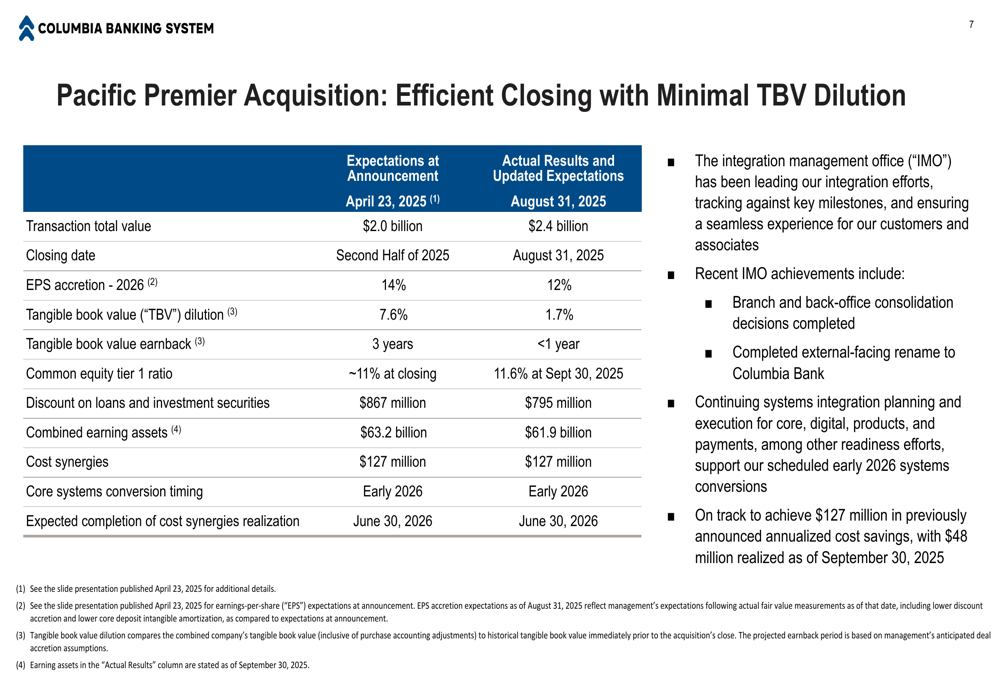

A significant highlight of the quarter was the successful completion of Columbia Banking’s acquisition of Pacific Premier Bancorp. The transaction, which closed on August 31, 2025, performed better than initially projected with tangible book value dilution of just 1.7%, considerably lower than the 7.6% anticipated at announcement in April 2025.

The acquisition details reveal that while the transaction value increased from $2.0 billion at announcement to $2.4 billion at closing, the EPS accretion for 2026 is expected to be 12%, slightly lower than the initially projected 14%:

This strategic acquisition has expanded Columbia’s footprint across eight western states, enhancing its position as a regional powerhouse. The combined entity now boasts $67.5 billion in assets, $48.5 billion in loans, and $55.8 billion in deposits.

Loan and Deposit Portfolio Analysis

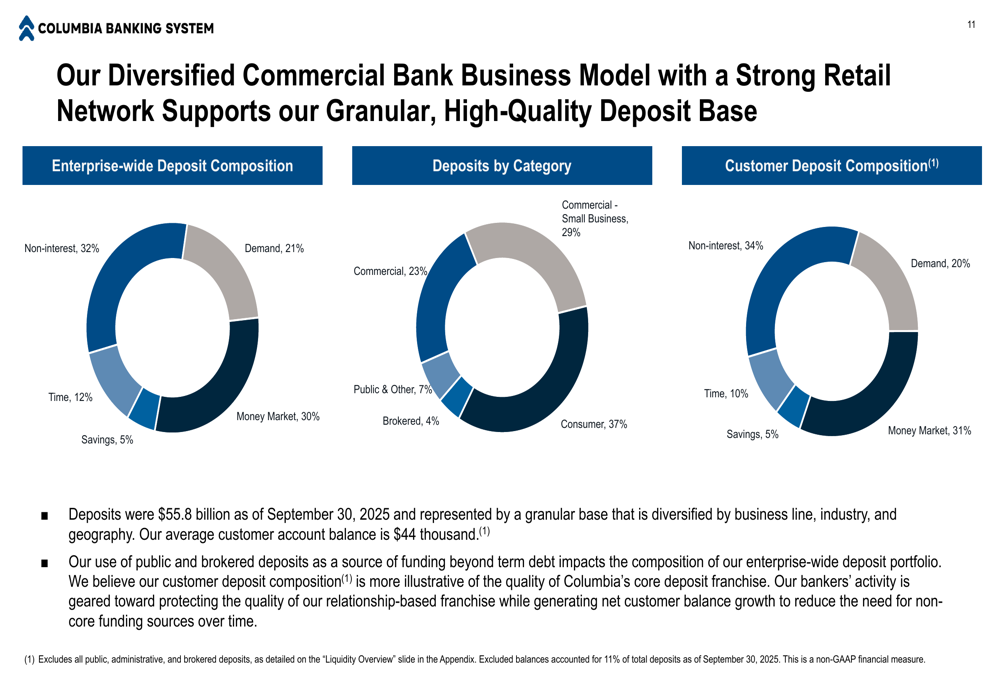

Columbia Banking’s presentation highlighted its diversified commercial bank business model, with a balanced deposit composition. Non-interest bearing deposits comprise 32% of the total deposit base, while money market accounts represent 30%. This favorable deposit mix provides the bank with a stable, low-cost funding source.

The loan portfolio is similarly diversified, with a focus on high-quality assets across multiple segments including commercial real estate, commercial and industrial, and residential mortgages. The presentation emphasized the bank’s prudent underwriting standards, with relatively low loan-to-value ratios across its portfolio.

CEO Clint Stein noted during the earnings call, "We are uniquely positioned in our region for organic growth opportunities," highlighting the company’s strategic focus on expanding its presence in western markets where household income averages 106% of the national average.

Credit Quality and Capital Position

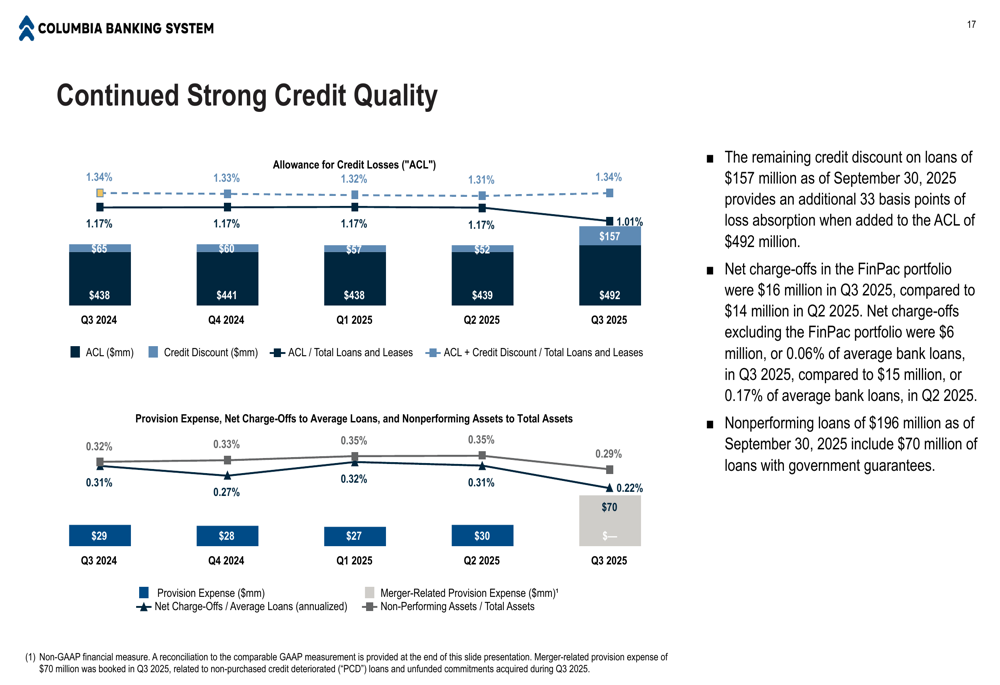

Columbia Banking maintained strong credit quality metrics during the quarter, with the allowance for credit losses (ACL) at 1.01% of loans in Q3 2025, down from 1.34% in Q3 2024. The company also reported declining non-performing assets to total assets ratio, reflecting its conservative credit culture.

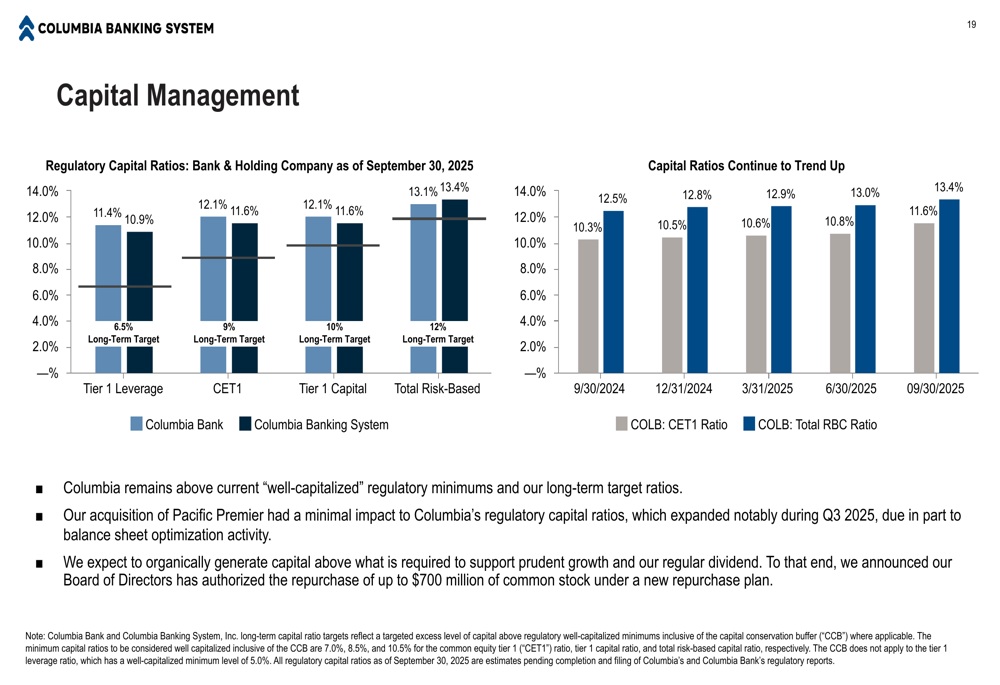

The bank’s capital position remains robust, with a Common Equity Tier 1 (CET1) ratio of 11.6% and a total capital ratio of 13.4% as of September 30, 2025. These levels exceed regulatory requirements and the bank’s long-term target ratios, providing flexibility for future growth opportunities and shareholder returns.

CFO Ron Farnsworth emphasized the company’s commitment to shareholder value during the earnings call, stating, "The greatest investment we can make is in our own stock, our own company." This sentiment is reflected in the recently authorized $700 million share repurchase program mentioned in the earnings discussion but not explicitly detailed in the presentation.

Strategic Positioning and Outlook

Columbia Banking’s presentation outlined its strategic focus on leveraging technology to improve collaboration and performance. The bank is investing in AI capabilities, enhancing its small business offerings, and continuing to develop payment technologies to drive operational efficiencies and revenue generation.

The company sees significant opportunities to increase density and gain market share throughout its footprint, particularly in key metropolitan areas across the western United States. With 240 branches in the Northwest, 104 in California, and 13 in other western markets, Columbia is well-positioned to capitalize on the region’s strong economic growth.

Looking forward, management expects stable net interest income of approximately $390 million in Q4 2025, with modest loan growth and core deposit expansion. The bank’s strong capital generation capabilities and diversified business model provide a solid foundation for sustainable growth in the coming quarters.

Despite the positive outlook, investors should consider potential risks including integration challenges from the Pacific Premier acquisition, macroeconomic conditions affecting interest rates, and competitive pressures in the banking sector. However, Columbia’s strategic positioning in high-growth western markets and its demonstrated ability to execute on acquisitions suggest the bank is well-equipped to navigate these challenges successfully.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.