BofA update shows where active managers are putting money

Introduction & Market Context

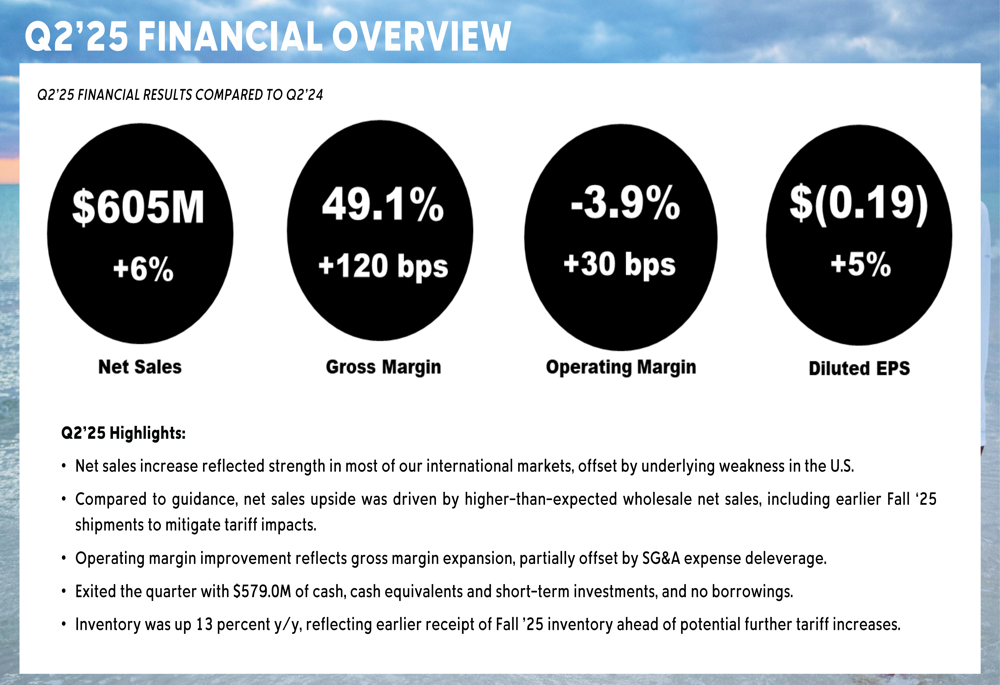

Columbia Sportswear Company (NASDAQ:COLM) released its second quarter 2025 financial results on July 31, showing modest growth driven by international markets while continuing to face challenges in its domestic business. The company reported a 6% increase in net sales to $605 million, slightly narrowing its quarterly loss compared to the same period last year.

Despite the improved quarterly performance, Columbia’s stock has struggled, trading near its 52-week low of $56.34. The shares closed at $58.40 on July 31, down 3.13% for the day, with an additional 0.34% decline in after-hours trading, reflecting ongoing investor concerns about tariffs and market uncertainties.

Quarterly Performance Highlights

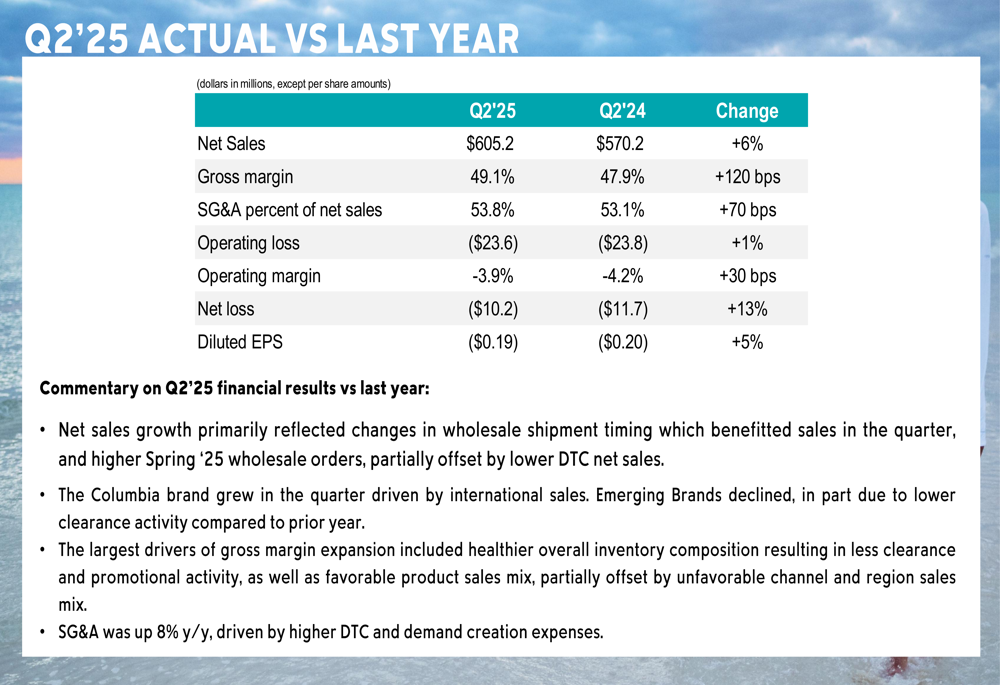

Columbia’s Q2 2025 results showed improvements across several key metrics compared to the same period in 2024. The company reported net sales of $605.2 million, up 6% year-over-year, while reducing its operating loss to $23.6 million, a 1% improvement. Diluted loss per share improved 5% to $(0.19) from $(0.20) in the prior year.

As shown in the following financial overview:

Gross margin expanded by 120 basis points to 49.1%, reflecting healthier inventory composition and reduced clearance activity. Operating margin improved by 30 basis points to -3.9%, though SG&A expenses as a percentage of net sales increased by 70 basis points to 53.8%.

The detailed year-over-year comparison reveals the specific improvements in Columbia’s financial performance:

Regional and Brand Performance

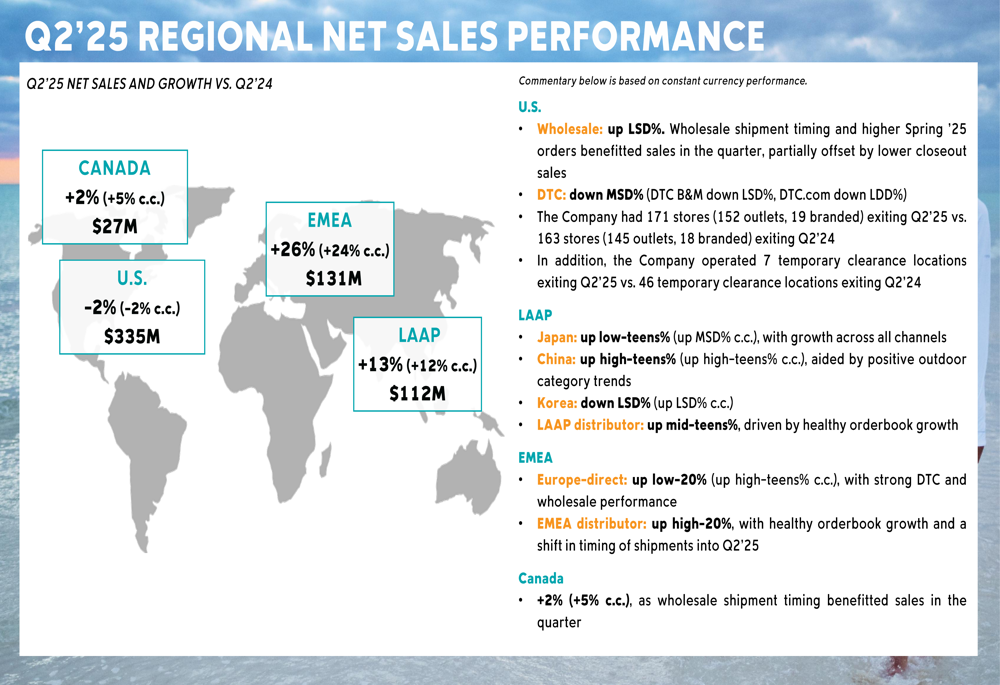

Columbia’s international markets drove growth in Q2 2025, with particularly strong performance in EMEA and LAAP regions, which grew 26% and 13% respectively. Meanwhile, the U.S. market continued to face challenges, with net sales declining 2% year-over-year.

The regional breakdown of net sales performance illustrates these contrasting trends:

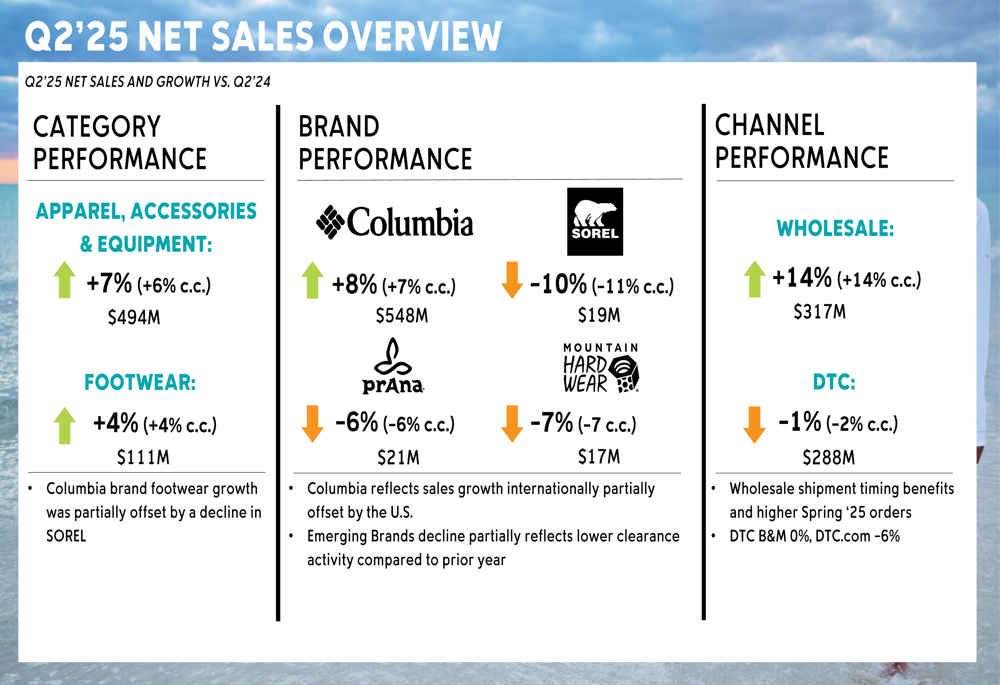

By brand, Columbia saw mixed results across its portfolio. The flagship Columbia brand grew 8%, while the company’s specialty brands all experienced declines: SOREL (-10%), prAna (-6%), and Mountain Hardwear (-7%). From a channel perspective, wholesale net sales increased 14%, partially offset by a 1% decline in direct-to-consumer (DTC) sales.

The following breakdown shows performance across categories, brands, and channels:

Margin and Expense Analysis

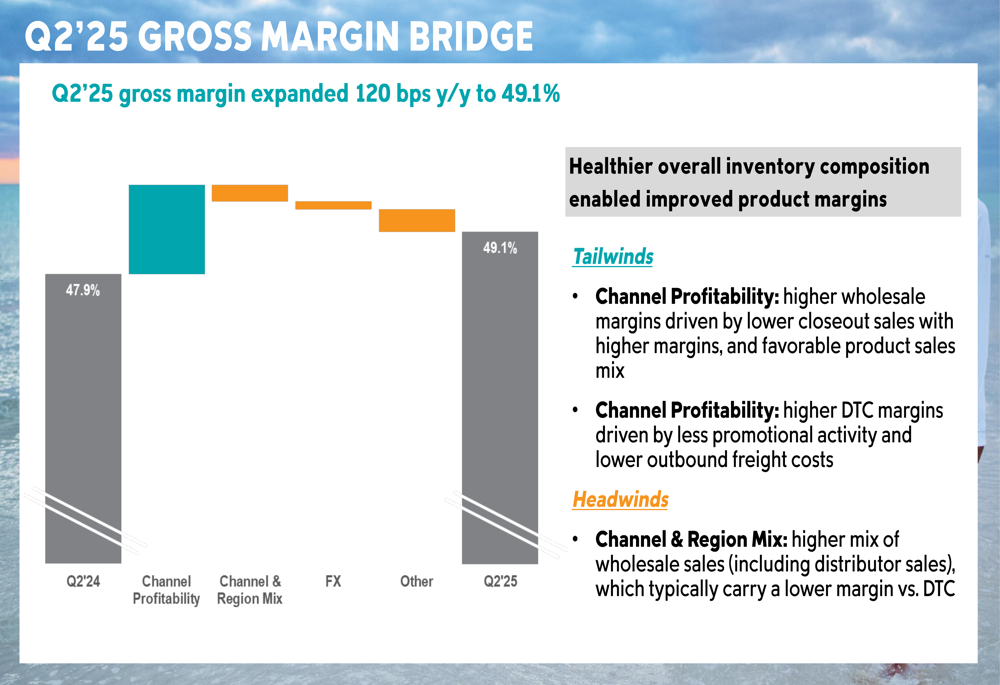

Columbia’s gross margin expanded by 120 basis points to 49.1% in Q2 2025, driven primarily by healthier inventory composition resulting in less clearance and promotional activity, as well as favorable product sales mix. These positive factors were partially offset by unfavorable channel and region sales mix.

The following gross margin bridge illustrates the key factors driving this improvement:

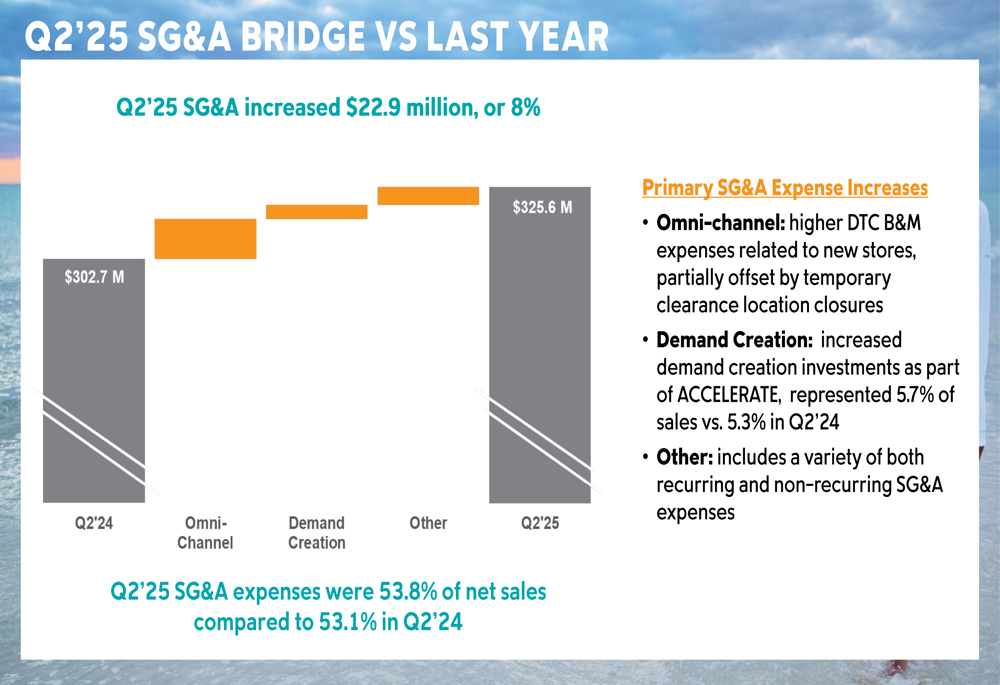

SG&A expenses increased by $22.9 million or 8% year-over-year to $325.6 million, primarily due to higher DTC and demand creation expenses. This resulted in SG&A deleverage of 70 basis points as a percentage of net sales.

The SG&A expense bridge shows the main components of this increase:

Balance Sheet and Capital Overview

Columbia maintained a strong balance sheet with $579 million in cash, cash equivalents, and short-term investments as of June 30, 2025, with no borrowings. Inventory levels increased 13% year-over-year to $926.9 million, primarily reflecting earlier receipt of Fall ’25 inventory ahead of potential further tariff increases.

The company reported negative year-to-date operating cash flow of $63 million and capital expenditures of $30 million. Columbia continued its shareholder return program with $132 million in share repurchases year-to-date and declared a quarterly dividend of $0.30 per share.

Forward Outlook and Strategy

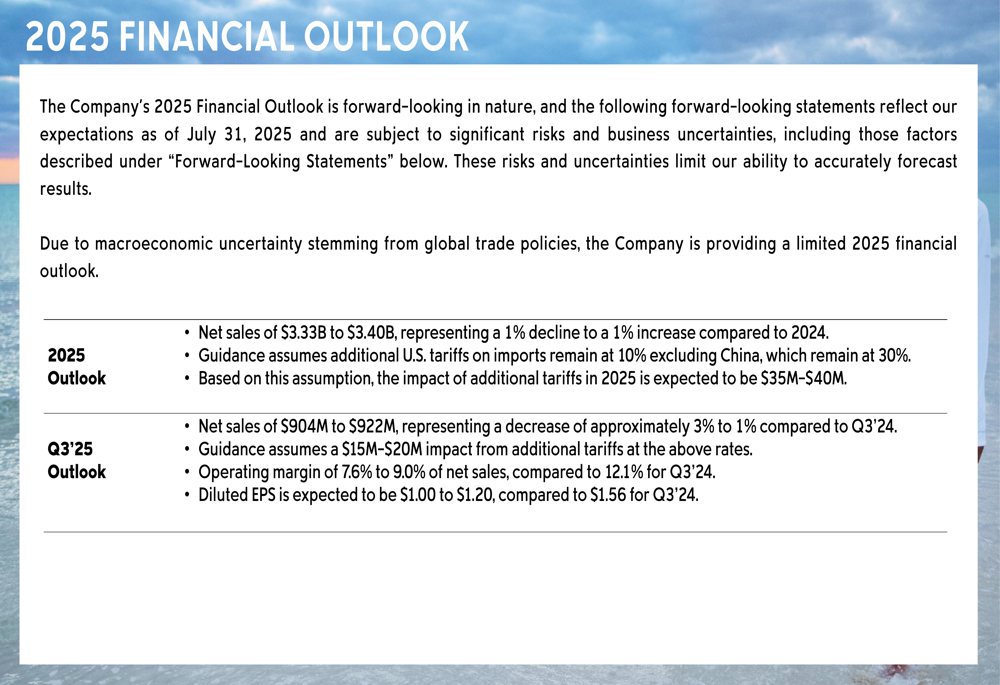

Columbia provided a cautious outlook for the remainder of 2025, projecting full-year net sales between $3.33 billion and $3.40 billion, representing a range from a 1% decline to a 1% increase compared to 2024. For Q3 2025, the company expects net sales between $904 million and $922 million, with diluted EPS of $1.00 to $1.20.

The company’s financial outlook incorporates the assumption that additional U.S. tariffs on imports will remain at 10% excluding China, which remain at 30%. The impact of these additional tariffs in 2025 is expected to be $35-40 million.

As illustrated in the company’s financial outlook:

Columbia’s growth strategy focuses on acquiring new customers and strengthening core segments through product innovation, marketing, and elevating consumer perception:

The company also reported that its Profit Improvement Plan has exceeded the original $125-150 million target set in 2024, with continued efforts to identify additional cost savings opportunities.

Market Challenges and Outlook

Columbia faces several significant challenges, including ongoing weakness in the U.S. market, the impact of additional tariffs, and broader economic uncertainties. The company is managing these challenges through strategic inventory management, cost-saving initiatives, and focusing on international growth opportunities.

Despite these headwinds, Columbia’s strong balance sheet, established brand portfolio, and international growth provide some resilience. The company’s ability to expand gross margins and exceed cost-saving targets demonstrates operational discipline, though continued pressure on the stock price suggests investors remain cautious about the company’s near-term prospects amid challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.