ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Columbus McKinnon Corporation (NASDAQ:CMCO), a global leader in intelligent motion solutions for material handling, reported strong second-quarter fiscal 2026 results on October 30, 2025, exceeding analyst expectations. The company delivered 8% revenue growth despite facing regional challenges, particularly in Europe, the Middle East, and Africa (EMEA).

The industrial equipment manufacturer’s performance comes amid ongoing global supply chain adjustments and varying regional economic conditions. The company continues to make progress on its pending Kito Crosby acquisition, which is expected to significantly expand its scale and market presence.

Quarterly Performance Highlights

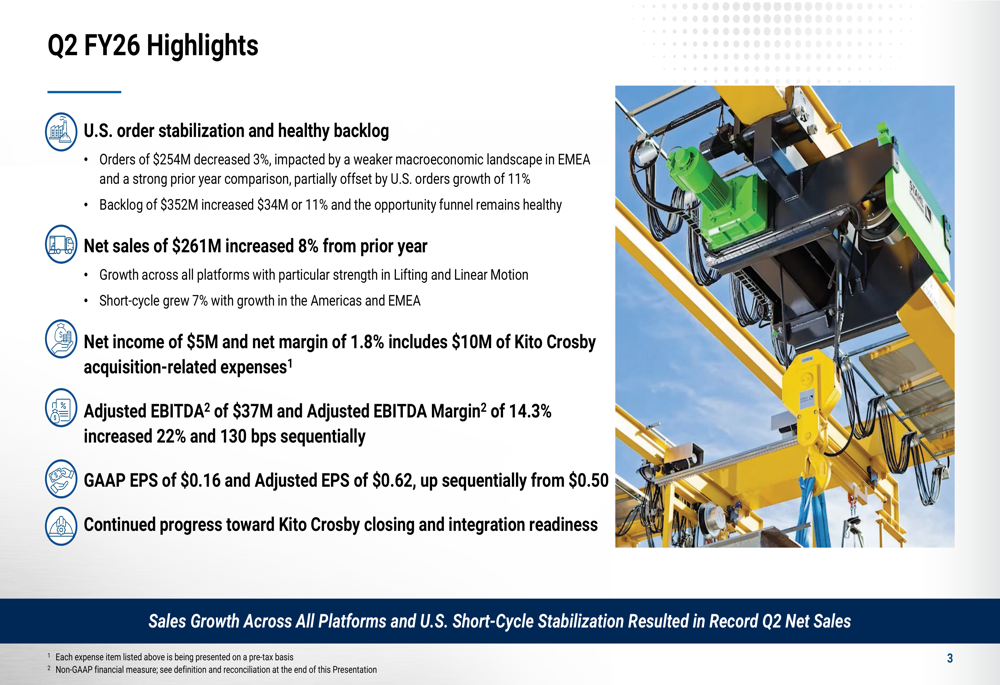

Columbus McKinnon reported net sales of $261 million in Q2 FY26, representing an 8% increase from the prior year. This growth was driven by strength across all platforms, with particular momentum in Lifting and Linear Motion segments. The company’s short-cycle business grew 7%, with growth concentrated in the Americas and EMEA regions.

As shown in the following quarterly highlights chart:

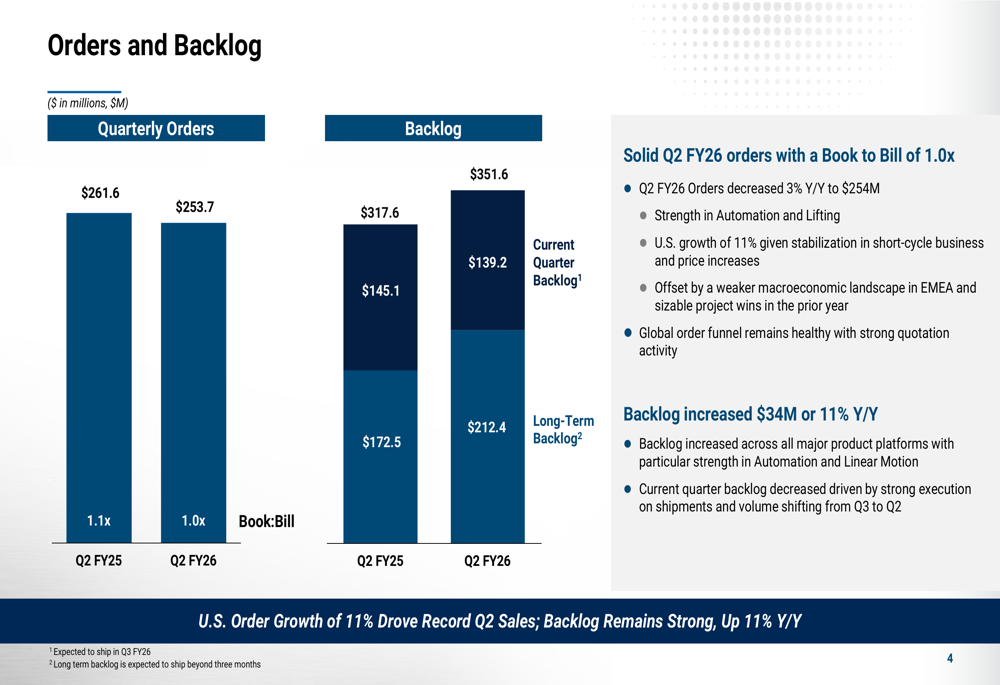

Orders decreased 3% year-over-year to $254 million, impacted by a weaker macroeconomic landscape in EMEA and a strong prior year comparison. However, U.S. orders grew 11%, indicating stabilization in this key market. The company’s backlog increased 11% to $351.6 million, suggesting continued demand for its products.

The following chart illustrates the company’s orders and backlog trends:

Net income for the quarter was $5 million with a net margin of 1.8%, which included $10 million of Kito Crosby acquisition-related expenses. Adjusted EBITDA reached $37 million with a margin of 14.3%, representing a 22% sequential increase and 130 basis points of margin expansion from the previous quarter.

GAAP earnings per share came in at $0.16, while adjusted EPS reached $0.62, up from $0.50 in the previous quarter. According to the earnings report, this significantly exceeded analyst expectations of $0.53 per share, representing a 16.98% surprise.

Detailed Financial Analysis

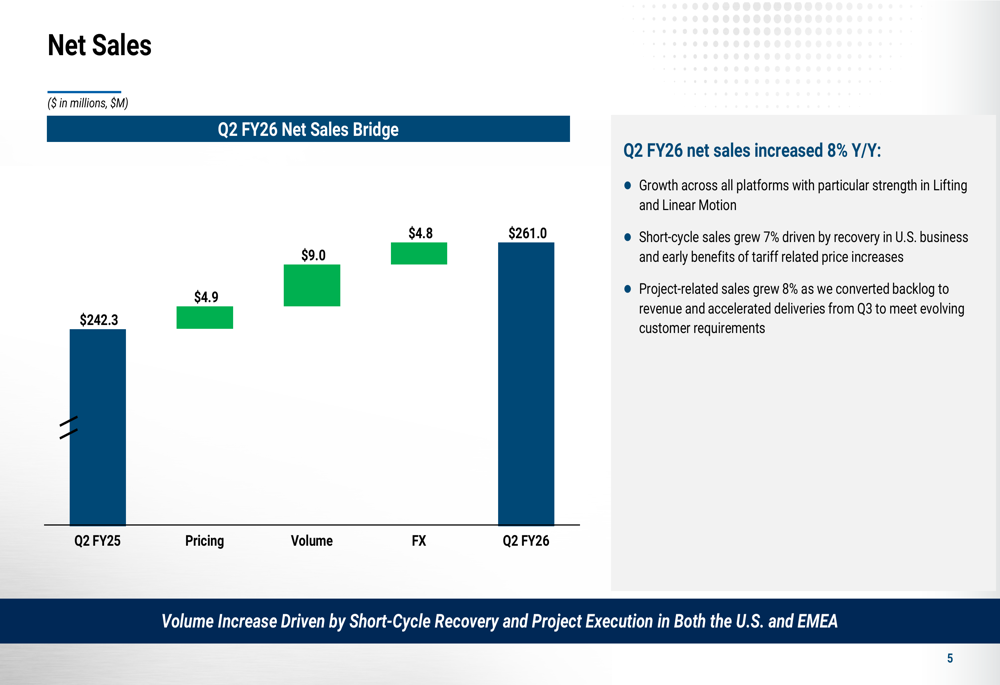

A closer examination of Columbus McKinnon’s sales growth reveals multiple contributing factors. As illustrated in the following sales bridge:

The $18.7 million increase in net sales from Q2 FY25 to Q2 FY26 was driven by $4.9 million from pricing actions, $9.0 million from volume growth, and $4.8 million from favorable foreign exchange impacts.

Operating income improved to $12.2 million from $10.8 million in the prior year period, while adjusted operating income was $25.2 million compared to $27.0 million. The adjusted operating margin of 9.7% reflected ongoing investments in growth initiatives and integration preparations.

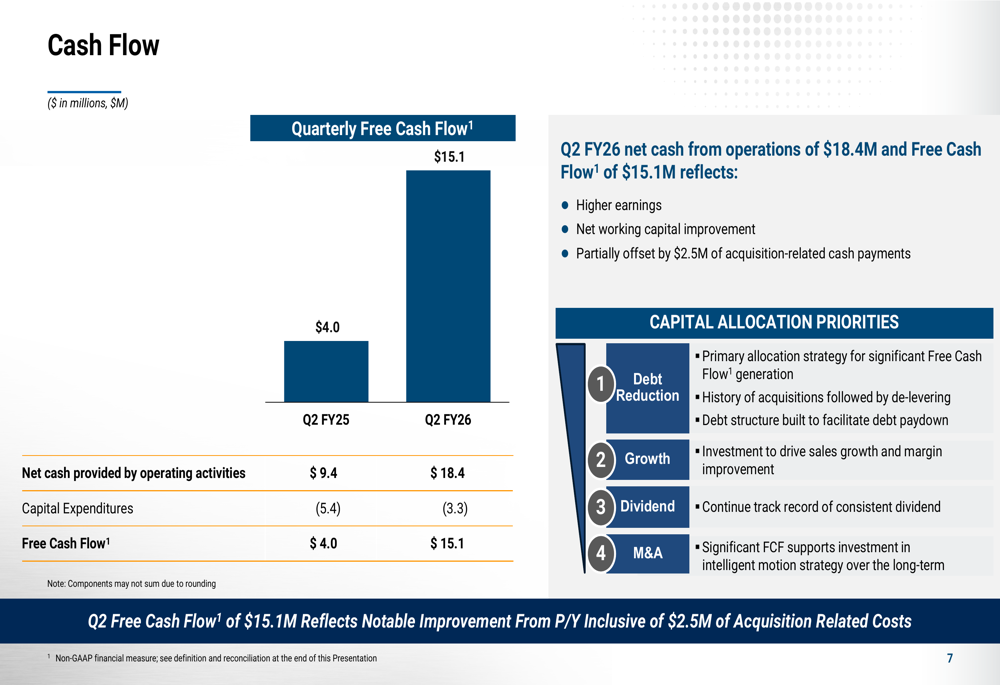

The company significantly improved its cash generation, with free cash flow of $15.1 million in Q2 FY26 compared to $4.0 million in Q2 FY25. This improvement reflects higher earnings, better working capital management, and was partially offset by $2.5 million of acquisition-related cash payments.

The following chart demonstrates this cash flow improvement:

Gross profit increased to $90.2 million, up 21% year-over-year, with adjusted gross margin at 35.3%. This performance reflects the company’s pricing discipline and operational improvements, despite ongoing inflationary pressures.

Strategic Initiatives & Forward Outlook

Columbus McKinnon continues to make progress toward closing the Kito Crosby acquisition and integration readiness. This strategic move is expected to significantly expand the company’s scale and market presence, with projected post-acquisition sales of $2 billion according to the earnings report.

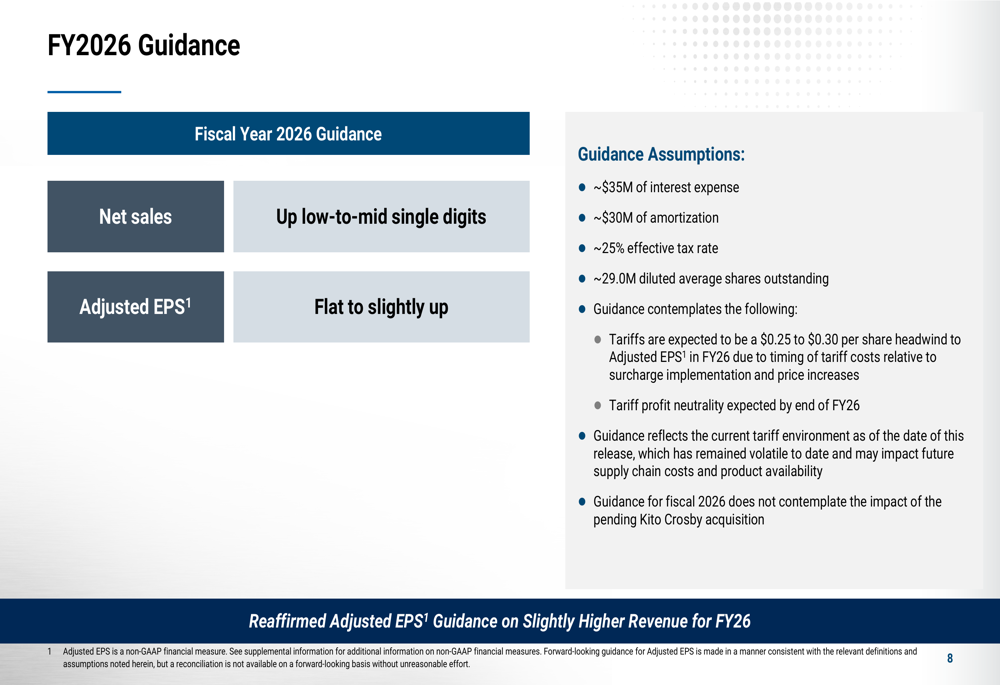

For fiscal year 2026, management provided the following guidance:

The company expects net sales to increase in the low-to-mid single digits, with adjusted EPS projected to be flat to slightly up. This guidance incorporates approximately $35 million of interest expense, $30 million of amortization, a 25% effective tax rate, and 29.0 million diluted average shares outstanding.

Management noted that tariffs are expected to be a $0.25 to $0.30 per share headwind to adjusted EPS in FY26, but the company anticipates achieving tariff profit neutrality by the end of the fiscal year through various mitigation strategies.

The guidance does not include the impact of the pending Kito Crosby acquisition, which is expected to close by the end of the fiscal year.

Market Reaction & Analyst Perspectives

The market responded positively to Columbus McKinnon’s Q2 results, with the stock surging 11.69% in pre-market trading to $16.81. By market close, the stock had extended gains to 16.21%, closing at $17.49, well above its 52-week low of $11.78 but still significantly below its 52-week high of $41.05.

CEO David Wilson was quoted in the earnings report stating, "We delivered a solid Q2 with 8% sales growth," while CFO Greg Rustowicz expressed enthusiasm about the pending acquisition, noting, "We remain enthusiastic about the pending acquisition and our ability to achieve our stated long-term objectives."

The company’s ability to deliver strong results despite regional challenges and tariff headwinds has bolstered investor confidence. With a healthy backlog, stabilizing U.S. orders, and strategic growth initiatives underway, Columbus McKinnon appears well-positioned to navigate the current macroeconomic environment while preparing for significant expansion through its pending acquisition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.