These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Columbus McKinnon Corporation (NASDAQ:CMCO) presented its Q4 and Fiscal Year 2025 financial results on May 28, 2025, revealing a complex picture of record orders amid challenging market conditions. The industrial equipment manufacturer’s stock closed at $17.78 on May 27, up 8.28% ahead of the results, but showed a slight decline of 1.29% in after-hours trading following the presentation.

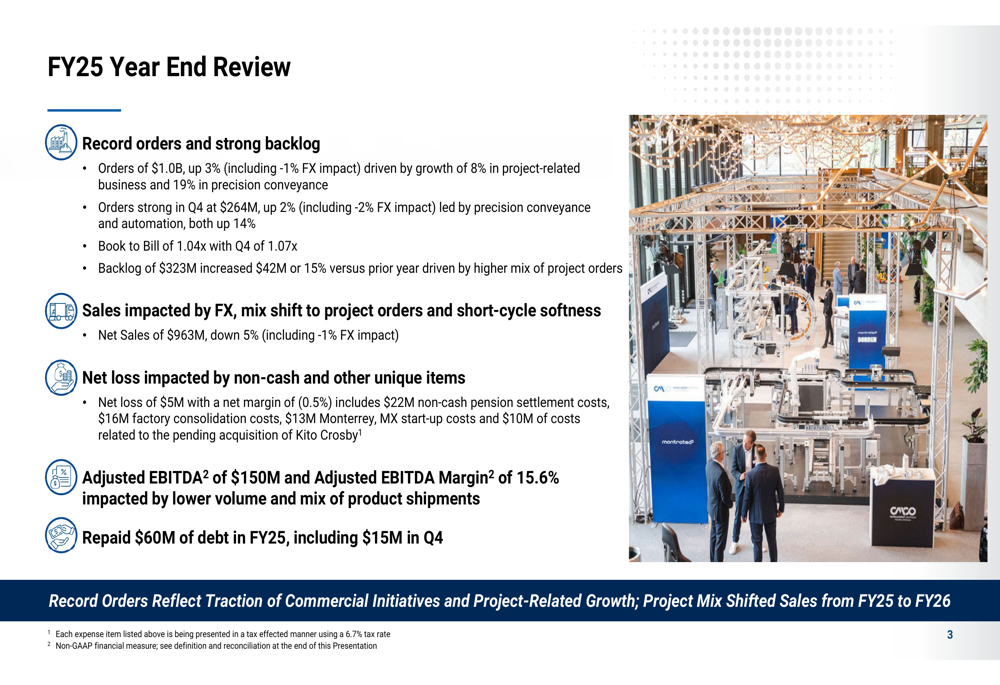

The company’s performance reflects both operational challenges and strategic positioning, with record orders of $1.0 billion for the fiscal year contrasting with declining sales and profitability. Management highlighted the significant impact of tariffs and the pending acquisition of Kito Crosby as key factors shaping the company’s future.

Quarterly Performance Highlights

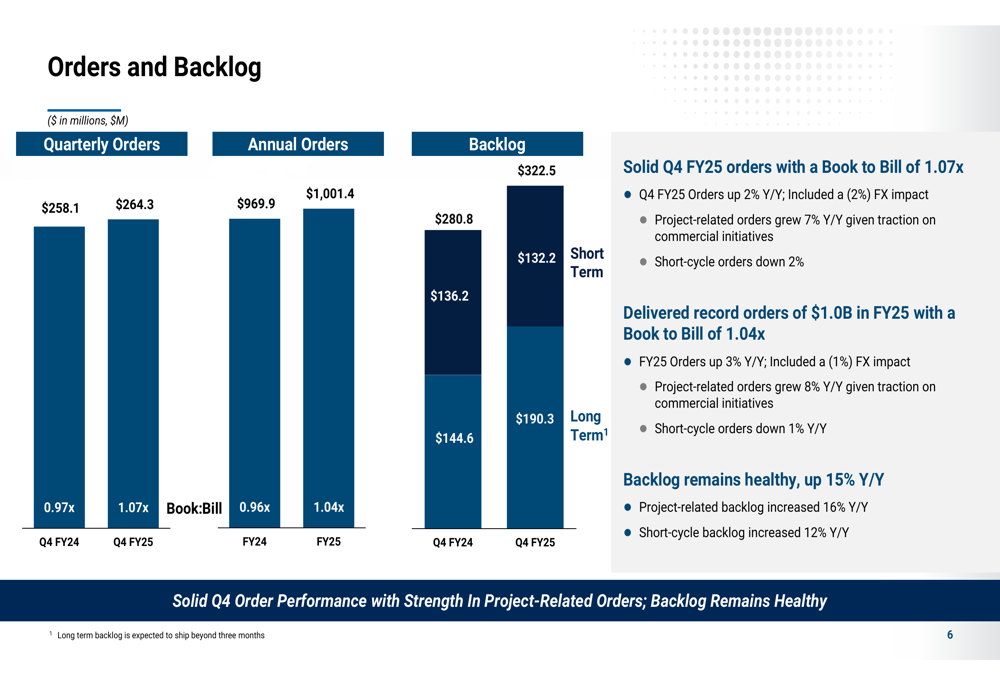

Columbus McKinnon reported solid order momentum in Q4 FY25, with orders reaching $264.3 million, up 2% year-over-year despite a 2% negative foreign exchange impact. The company achieved a book-to-bill ratio of 1.07x for the quarter, indicating strong demand relative to current sales levels.

As shown in the following chart of quarterly orders and backlog, the company’s backlog grew significantly to $322.5 million, representing a 15% increase compared to the prior year:

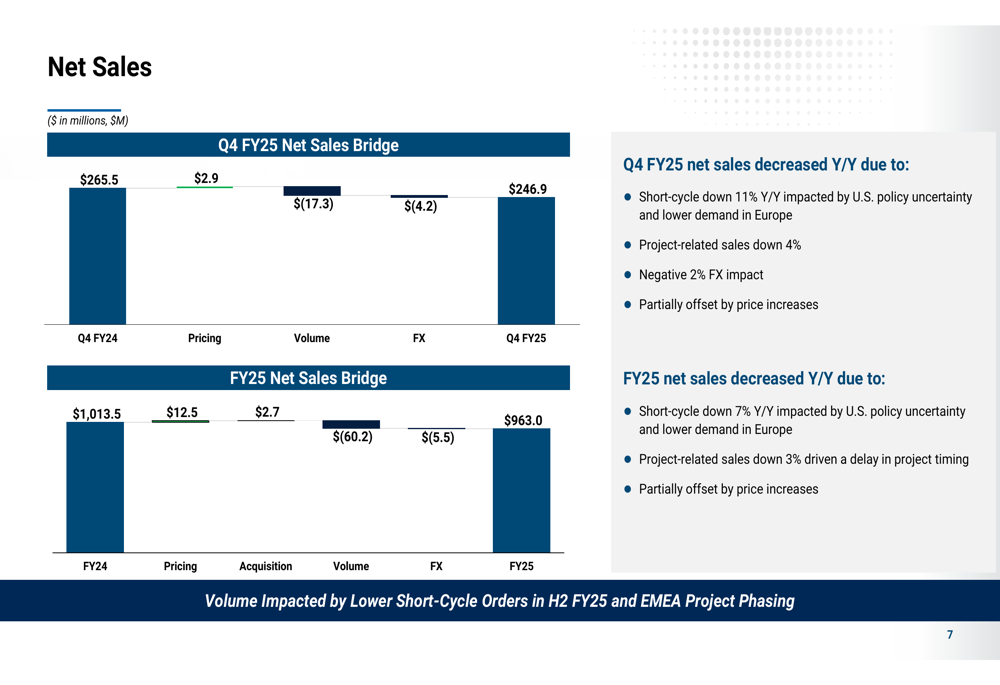

However, net sales for Q4 FY25 declined to $246.9 million, down from $265.5 million in the same period last year. The company attributed this 7% decrease to several factors, including short-cycle weakness in the U.S. and Europe, project timing, and foreign exchange headwinds.

The following waterfall chart illustrates the components of the net sales decline for both the quarter and full year:

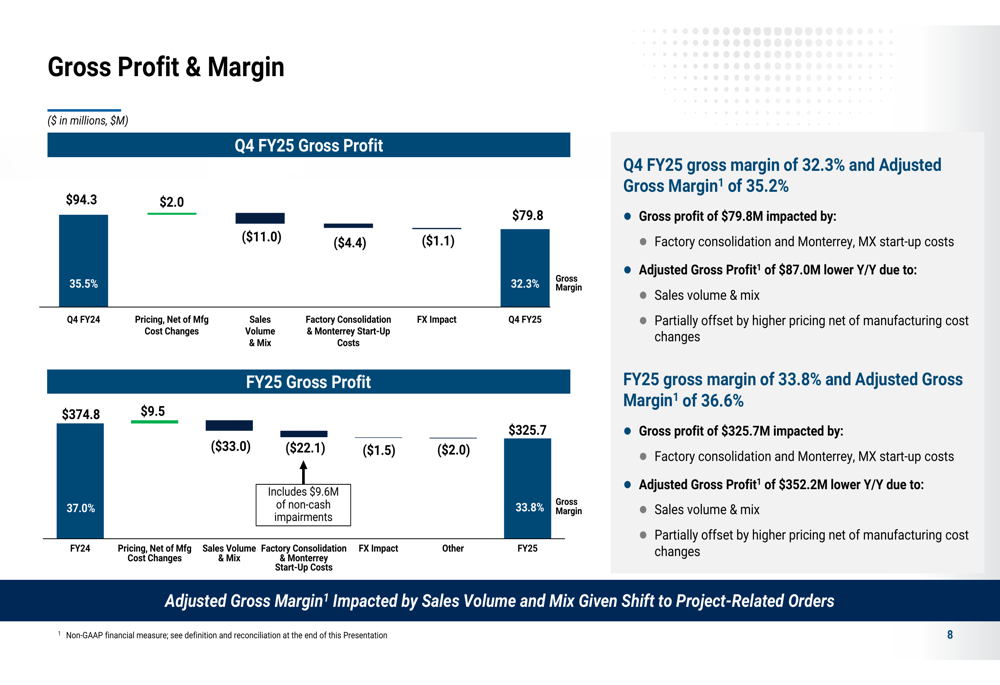

Profitability metrics showed significant pressure, with Q4 FY25 gross margin declining to 32.3% from 35.5% in the prior year period. The company reported adjusted gross margin of 35.2% for the quarter, with the difference primarily attributed to factory consolidation and start-up costs for the new Monterrey, Mexico facility.

The following chart details the factors impacting gross profit and margin:

Strategic Initiatives

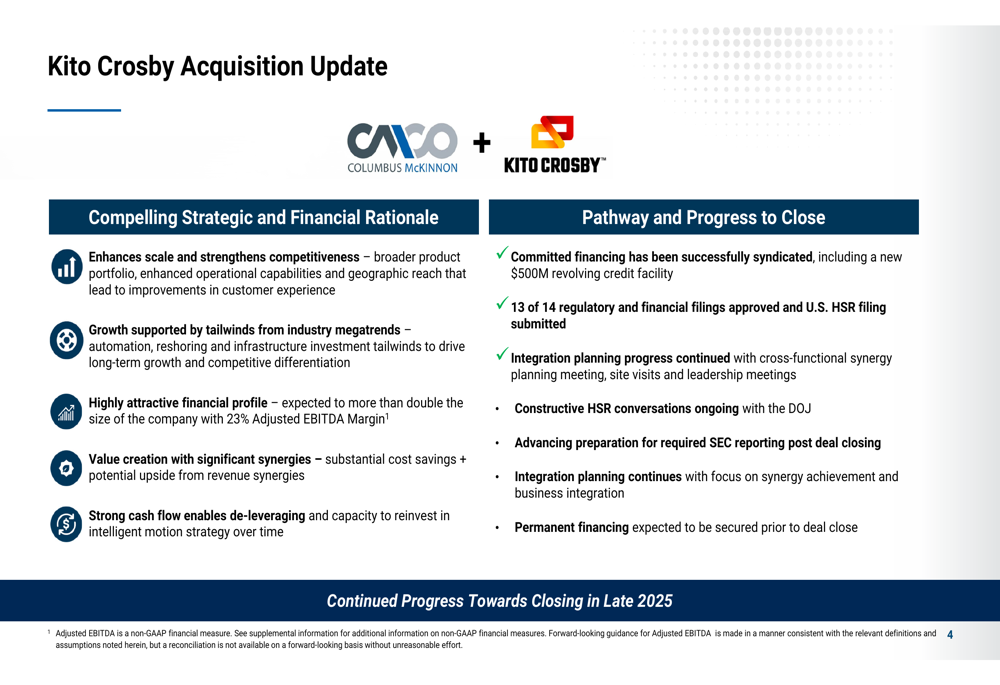

A central focus of Columbus McKinnon’s presentation was the pending acquisition of Kito Crosby, which is expected to close in late 2025. This strategic move is projected to more than double the company’s size and achieve a 23% adjusted EBITDA margin, according to management.

The company provided the following update on the acquisition progress:

Another significant strategic challenge facing Columbus McKinnon is the impact of tariffs, which the company estimates will affect EBITDA by approximately $40 million. Management outlined a comprehensive mitigation plan including surcharges, price increases, and supply chain realignment.

The company expects tariffs to negatively impact the first half of FY26 but anticipates achieving profit neutrality by the second half of the fiscal year through these mitigation efforts.

Detailed Financial Analysis

For the full fiscal year 2025, Columbus McKinnon reported net sales of $963 million, down 5% from $1,013.5 million in FY24. Despite price increases of $12.5 million, volume declined by $60.2 million, and foreign exchange had a negative $5.5 million impact.

The company reported a net loss of $5 million for FY25, with a net margin of (0.5%), significantly impacted by non-cash pension settlement costs of $22 million, factory consolidation costs of $16 million, Monterrey start-up costs of $13 million, and $10 million related to the pending Kito Crosby acquisition.

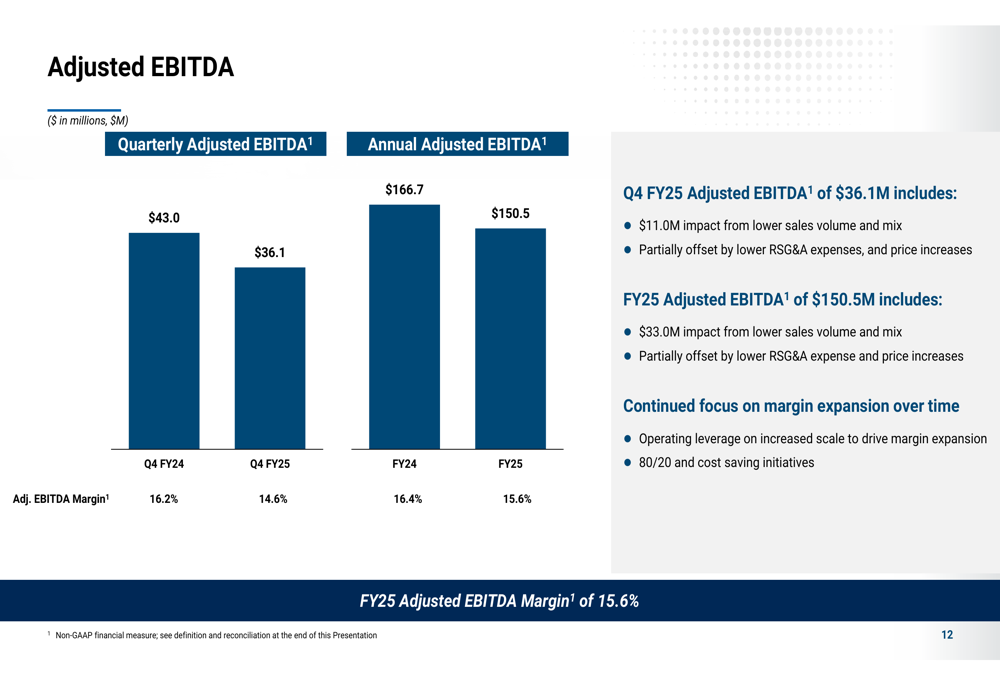

Adjusted EBITDA for FY25 was $150.5 million with a margin of 15.6%, down from $166.7 million and 16.4% in FY24, as shown in the following chart:

Operating income showed similar pressure, declining to $54.6 million for FY25 from $120.7 million in the prior year. Adjusted operating income was $102.3 million, compared to $107.1 million in FY24.

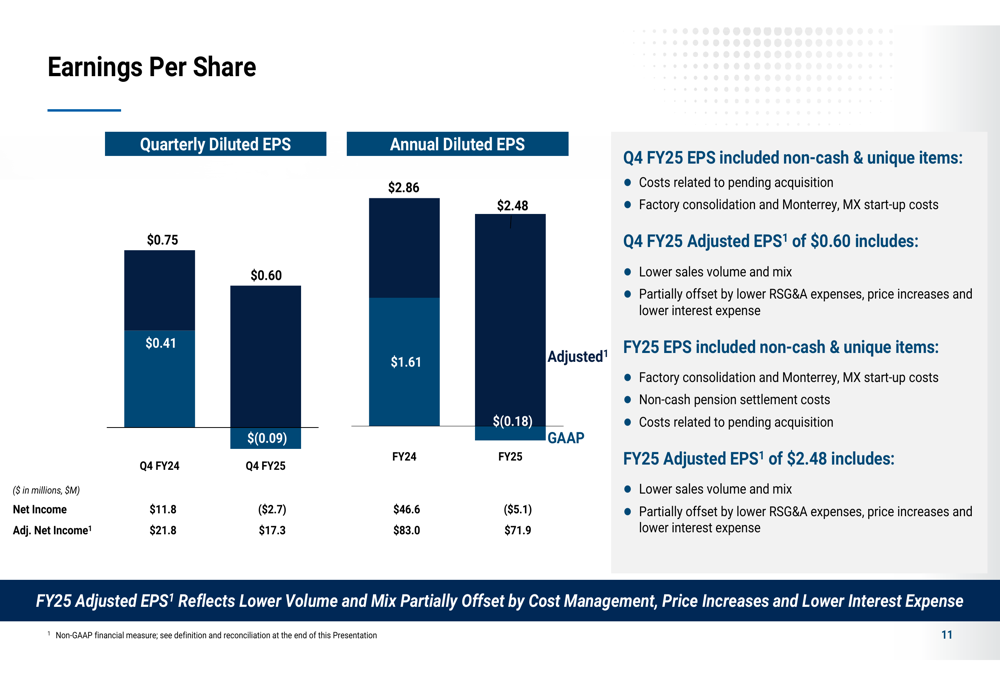

The earnings per share data further illustrates the financial challenges:

Cash flow generation was also affected, with free cash flow decreasing to $24.2 million in FY25 from $42.4 million in FY24. The company attributed this decline to timing of unbilled revenue recognition on large projects and higher inventory levels due to large orders and footprint consolidation efforts.

Despite these challenges, Columbus McKinnon repaid $60 million of debt during FY25, including $15 million in Q4, and reported a credit agreement net leverage ratio of 3.1x.

Forward-Looking Statements

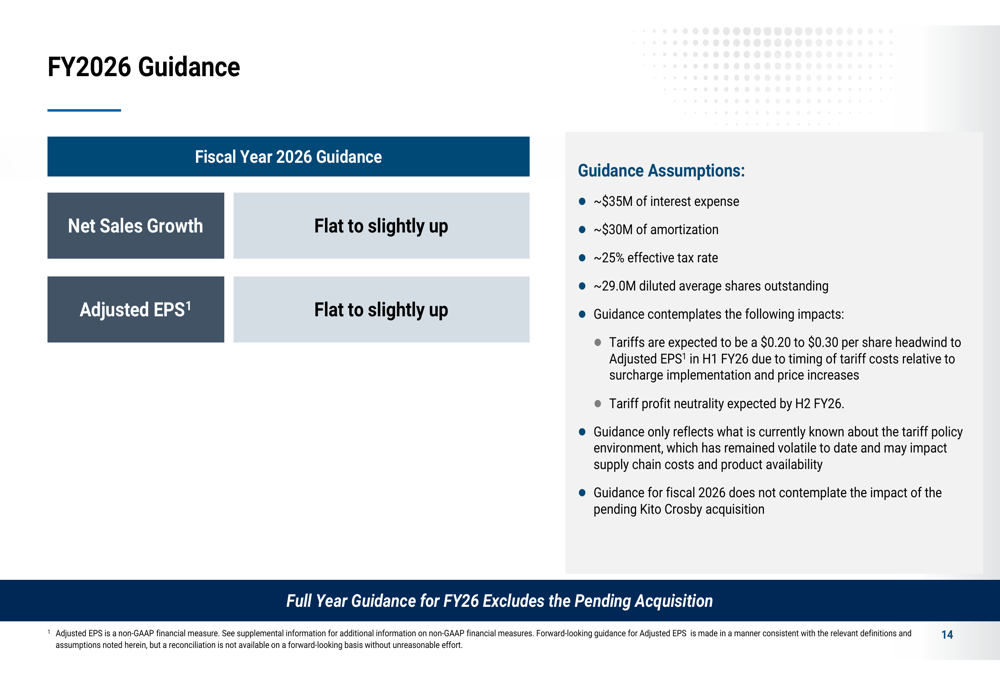

Looking ahead to fiscal year 2026, Columbus McKinnon provided cautious guidance, projecting flat to slightly up net sales growth and adjusted EPS. This outlook does not include the impact of the pending Kito Crosby acquisition.

The company’s guidance for FY26 incorporates several key assumptions:

Management emphasized that tariffs are expected to be a significant headwind in the first half of FY26, impacting adjusted EPS by $0.20 to $0.30 per share before achieving profit neutrality in the second half through pricing actions and supply chain adjustments.

The guidance reflects only currently known tariff policies, with management noting the volatile policy environment could further impact supply chain costs and product availability.

Columbus McKinnon’s year-end review highlighted both the challenges and opportunities facing the company:

While the company faces near-term headwinds from tariffs and operational transitions, management remains focused on long-term strategic initiatives, including the transformative Kito Crosby acquisition and ongoing efforts to optimize the manufacturing footprint and supply chain. Investors will be watching closely to see if the strong order book and backlog translate into improved financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.