TSX runs higher on rate cut expectations

Introduction & Market Context

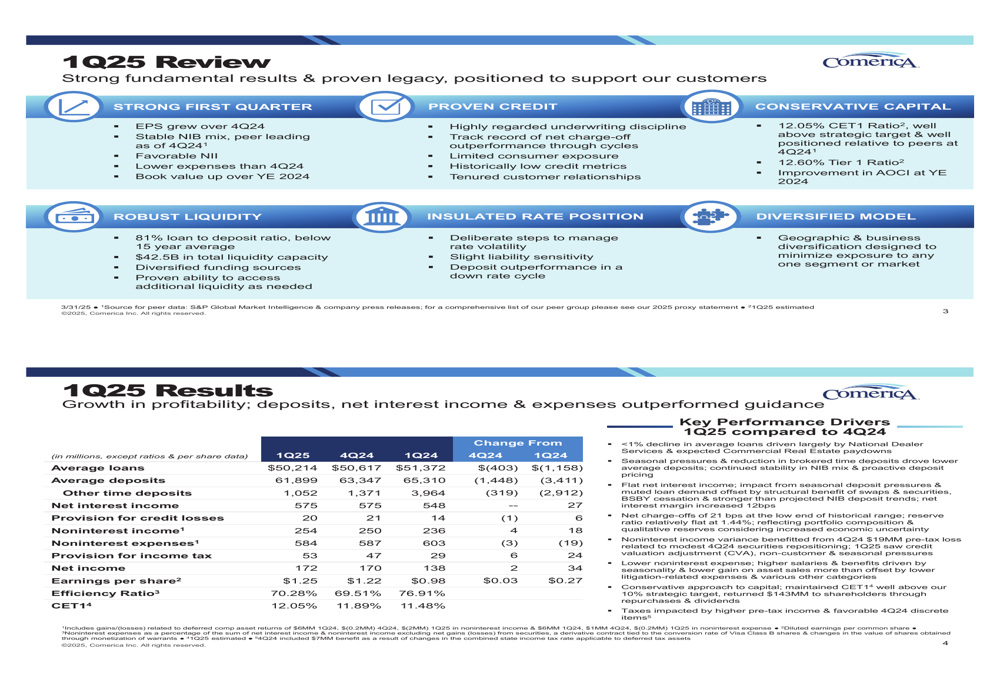

Comerica Incorporated (NYSE:CMA) released its first quarter 2025 financial results on April 21, 2025, showing improved earnings despite continued balance sheet contraction. The bank reported earnings per share of $1.25, up $0.03 from the previous quarter and $0.27 from the same period last year. Despite these improvements, Comerica’s stock fell 3.65% to $52.95 following the presentation, suggesting investors may be concerned about the ongoing decline in loans and deposits.

The Q1 results come after Comerica missed earnings expectations in Q3 2024, which had previously pressured the stock. While the current quarter shows sequential improvement, the market appears focused on the bank’s shrinking balance sheet and high efficiency ratio of 70.28%.

Quarterly Performance Highlights

Comerica reported net income of $172 million for Q1 2025, representing a modest increase of $2 million from Q4 2024 and a more substantial $34 million improvement from Q1 2024. The bank’s net interest income remained flat quarter-over-quarter at $575 million but improved by $27 million year-over-year.

As shown in the following comprehensive performance summary:

Average loans decreased to $50,214 million, down $403 million from the previous quarter and $1,158 million from Q1 2024. Similarly, average deposits declined to $61,899 million, representing a $1,448 million reduction from Q4 2024 and a $3,411 million drop year-over-year. Despite these declines, the bank maintained a stable noninterest-bearing deposit mix at 38% of total deposits.

Noninterest income increased by $4 million quarter-over-quarter to $254 million, while noninterest expenses decreased by $3 million to $584 million, demonstrating some expense discipline. The provision for credit losses remained relatively stable at $20 million.

Detailed Financial Analysis

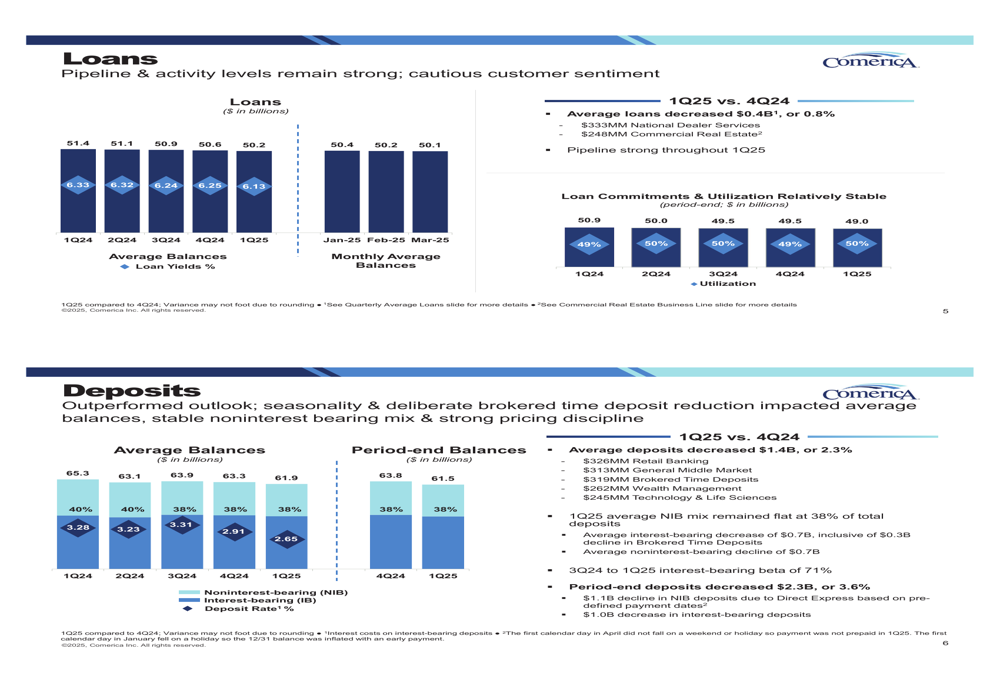

Comerica’s loan portfolio continues to face headwinds, though the bank notes that pipeline and activity levels remain strong. The following chart illustrates the declining trend in average loan balances from Q1 2024 through Q1 2025, along with corresponding loan yields:

The bank’s deposit base has also contracted, with average deposit balances declining from $65.3 billion in Q1 2024 to $61.9 billion in Q1 2025. However, Comerica highlights its deposit outperformance with stable noninterest-bearing mix and strong pricing discipline. The interest-bearing beta from Q3 2024 to Q1 2025 was 71%.

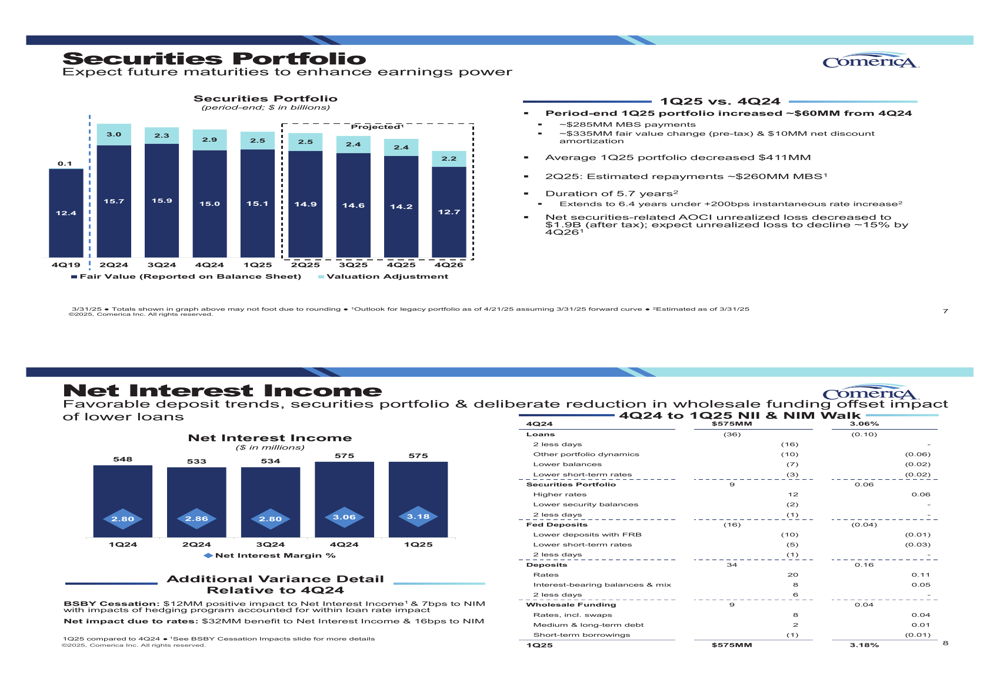

Comerica’s securities portfolio is positioned to enhance earnings power through future maturities. The fair value of the securities portfolio stood at approximately $14.2 billion in Q1 2025, with projected declines to approximately $12.7 billion by Q4 2026. The bank expects the net securities-related AOCI unrealized loss to decline by approximately 15% by Q4 2026.

The following chart shows the securities portfolio trajectory and net interest income trends:

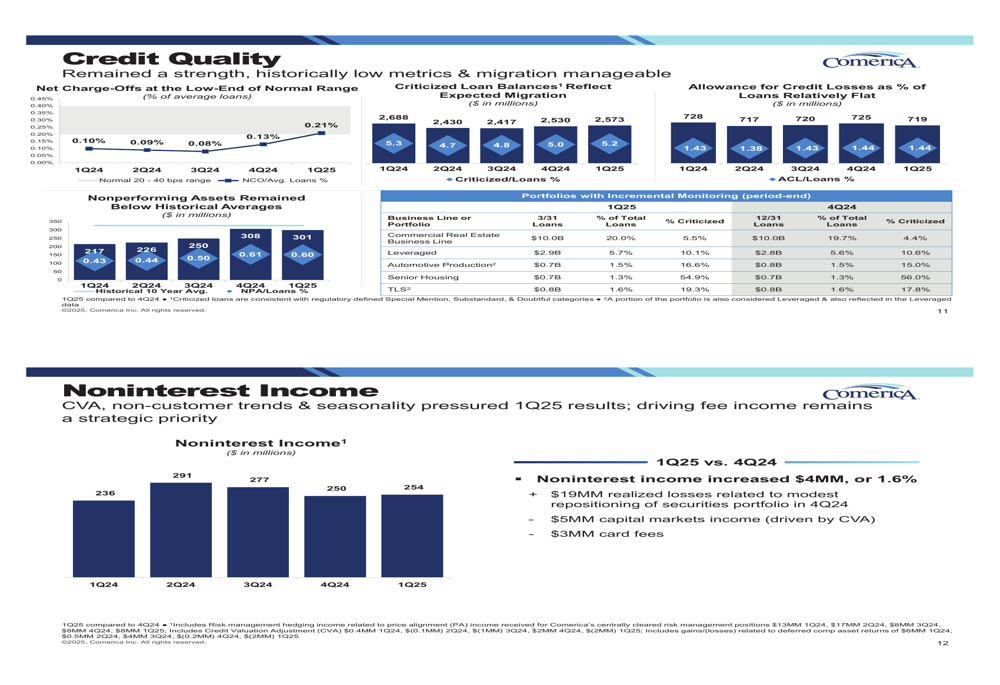

Credit quality remains a strength for Comerica, with net charge-offs at the low end of the normal range at 0.13% for Q1 2025. The Allowance for Credit Losses as a percentage of loans remained relatively flat at 1.44%. The following credit quality metrics demonstrate the bank’s consistent performance in this area:

Strategic Positioning

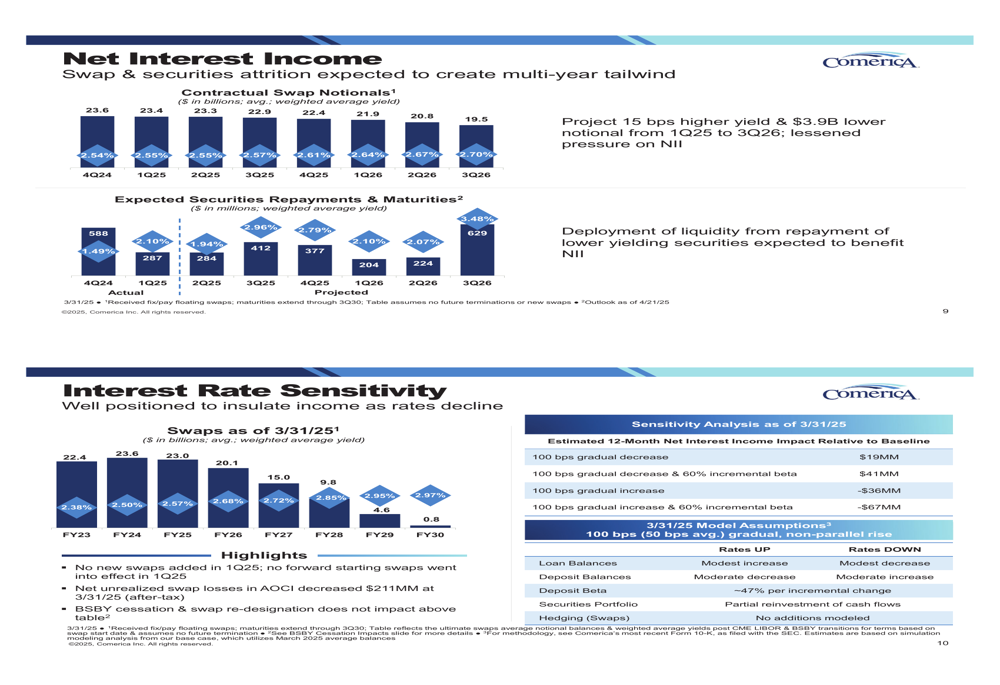

Comerica has strategically positioned itself to benefit from a declining interest rate environment. The bank describes itself as "slightly liability sensitive," which should help insulate net interest income as rates decline. This positioning is achieved through a combination of swaps, securities portfolio management, and balance sheet composition.

The following analysis illustrates Comerica’s interest rate sensitivity as of March 31, 2025:

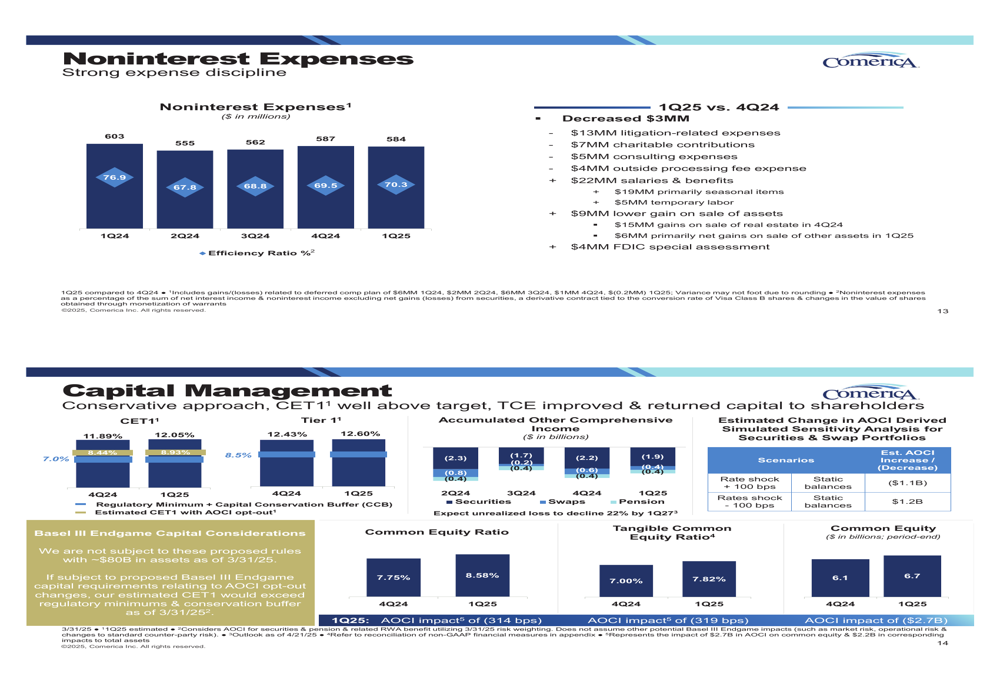

Capital management remains conservative, with a CET1 ratio of 12.05%, well above the bank’s target of 10%. This strong capital position provides flexibility for potential share repurchases and loan growth opportunities. The bank’s tangible common equity improved during the quarter, partly due to favorable movement in AOCI.

Comerica’s noninterest expenses and capital position are illustrated in the following chart:

Forward-Looking Statements

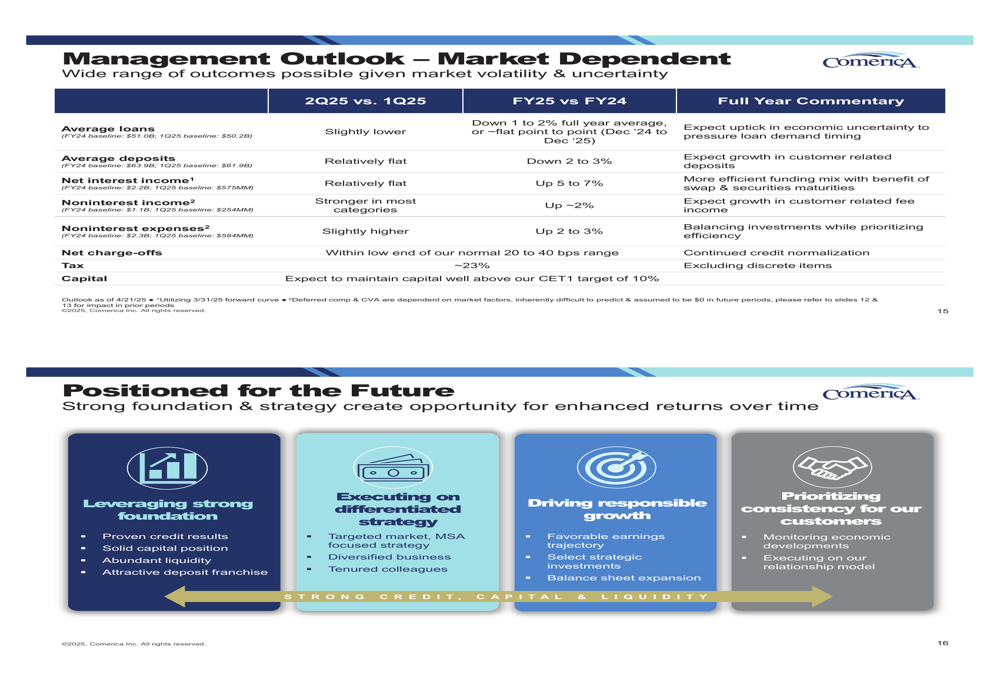

Management’s outlook for the remainder of 2025 indicates cautious optimism, with expectations for modest improvement in several key areas. For Q2 2025 compared to Q1, the bank projects average loans to be slightly lower and average deposits to be relatively flat. Net interest income is expected to remain relatively flat, while noninterest income should be stronger in most categories.

For the full year 2025 compared to 2024, Comerica forecasts:

- Average loans down 1-2%

- Average deposits down 2-3%

- Net interest income up 5-7%

- Noninterest income up 2%

- Noninterest expenses up 2-3%

- Net charge-offs within the low end of the normal 20-40 basis point range

The following management outlook provides a comprehensive view of Comerica’s expectations:

Comerica emphasizes its strong foundation, differentiated strategy, and focus on responsible growth. The bank highlights its proven credit results, solid capital position, abundant liquidity, and attractive deposit franchise as key strengths. Management remains focused on executing a targeted market strategy while prioritizing consistency for customers.

Competitive Industry Position

Comerica continues to leverage its specialized business segments to differentiate itself in the market. The bank’s Wealth Management division represents approximately 27% of its noninterest income and manages approximately $195 billion in Assets Under Administration. This diversification helps offset some of the pressure on traditional banking revenue streams.

The bank’s Shared National Credit (SNC) relationships demonstrate better credit quality than the portfolio average, with only 2% of SNCs criticized compared to 5.2% for the overall loan portfolio. These relationships span 680 borrowers with period-end loans of $11.4 billion, providing additional diversification to Comerica’s credit exposure.

Comerica’s environmental services business, including its renewables team formed in 2022, has shown strong growth and represents a strategic focus area for the bank. This specialized lending category grew during the quarter, demonstrating the bank’s ability to capitalize on niche market opportunities.

Despite the challenges of declining loan and deposit balances, Comerica’s focus on relationship banking and specialized business segments positions it to navigate the current economic environment while maintaining solid profitability. However, investors appear to remain cautious about the bank’s growth prospects, as reflected in the negative stock price reaction following the presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.