Boeing secures $883 million Army contract for cargo support services

Introduction & Market Context

Comfort Systems USA (NYSE:FIX), a leading provider of mechanical and electrical installation services, presented its second quarter 2025 earnings results on July 25, 2025, revealing exceptional financial performance across all key metrics. The company’s shares closed at $547.91 on July 24, up 3.12% for the day, trading near its 52-week high of $565.02.

The strong Q2 results continue the momentum from the first quarter, when Comfort Systems significantly exceeded analyst expectations with EPS of $4.75 versus the forecasted $3.71. The company’s consistent outperformance has maintained strong analyst confidence, with consensus recommendations remaining at "Strong Buy."

Quarterly Performance Highlights

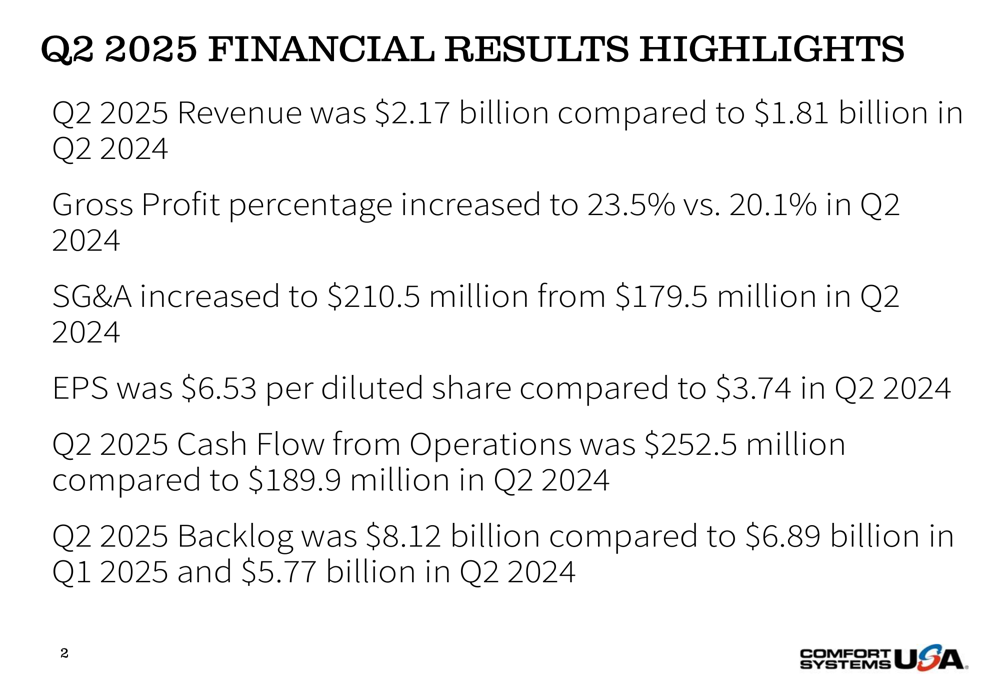

Comfort Systems reported substantial growth in Q2 2025, with revenue reaching $2.17 billion, a 20.1% increase from $1.81 billion in Q2 2024. Even more impressive was the company’s profitability, with diluted earnings per share (EPS) surging 74.6% to $6.53, compared to $3.74 in the same period last year.

As shown in the following financial highlights from the presentation:

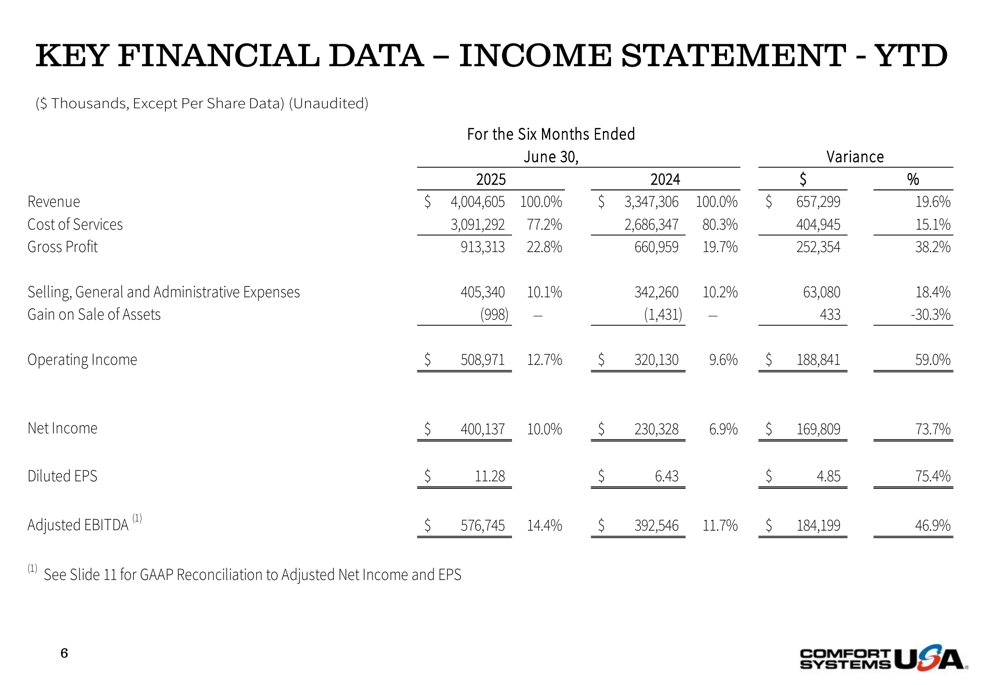

The company’s gross profit percentage improved significantly to 23.5% in Q2 2025, up from 20.1% in Q2 2024, demonstrating enhanced operational efficiency. Cash flow from operations also showed strong growth, increasing to $252.5 million from $189.9 million in the prior year period.

Detailed Financial Analysis

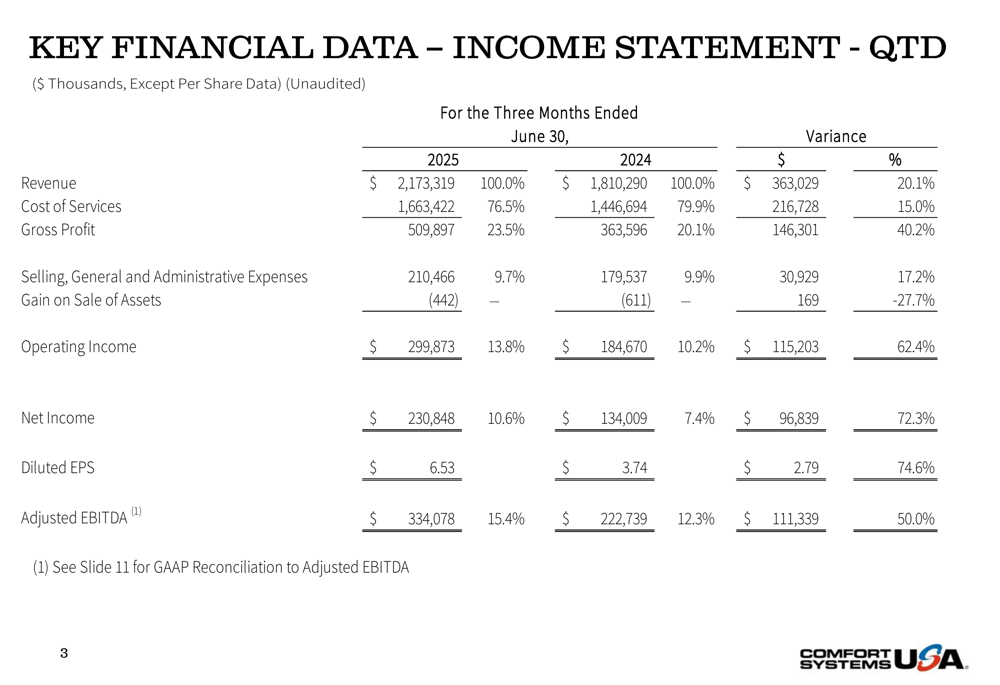

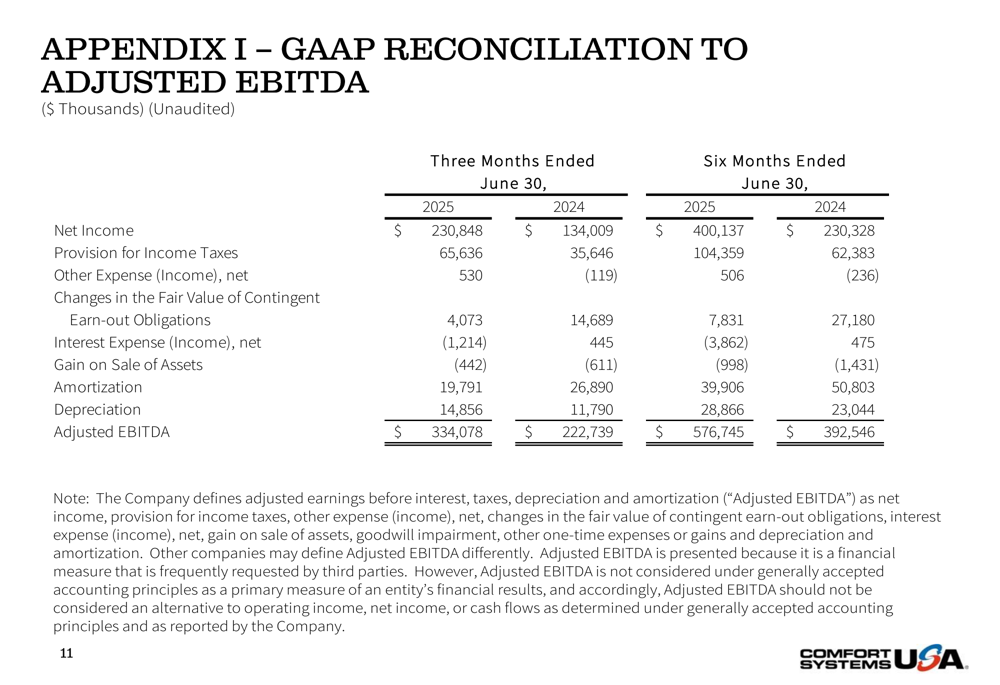

A deeper look at Comfort Systems’ income statement reveals impressive growth across all key financial metrics. Operating income increased by 62.4% to $299.9 million, while net income jumped 72.3% to $230.8 million. The company’s adjusted EBITDA reached $334.1 million, a 50.0% increase from Q2 2024.

The detailed income statement comparison illustrates the scale of improvement:

While selling, general and administrative expenses increased by 17.2% to $210.5 million, this growth was significantly outpaced by revenue expansion, contributing to the substantial improvement in operating margins.

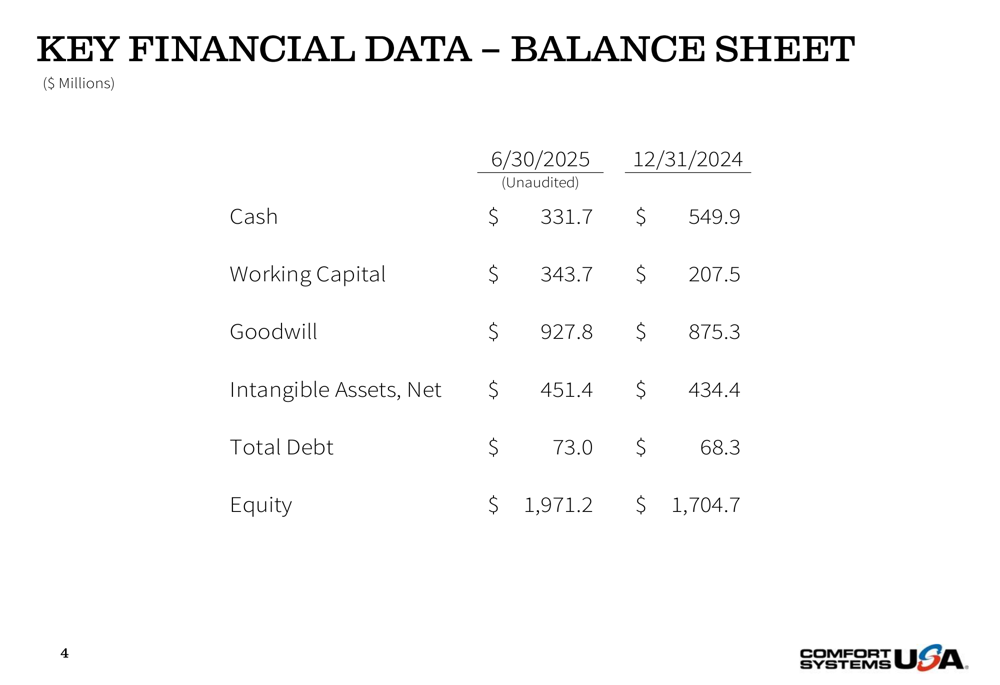

The company’s balance sheet as of June 30, 2025, showed a cash position of $331.7 million, down from $549.9 million at the end of 2024. However, working capital increased to $343.7 million from $207.5 million, suggesting investments in operations to support growth. Total (EPA:TTEF) debt remained relatively stable at $73.0 million, while equity grew to $1.97 billion.

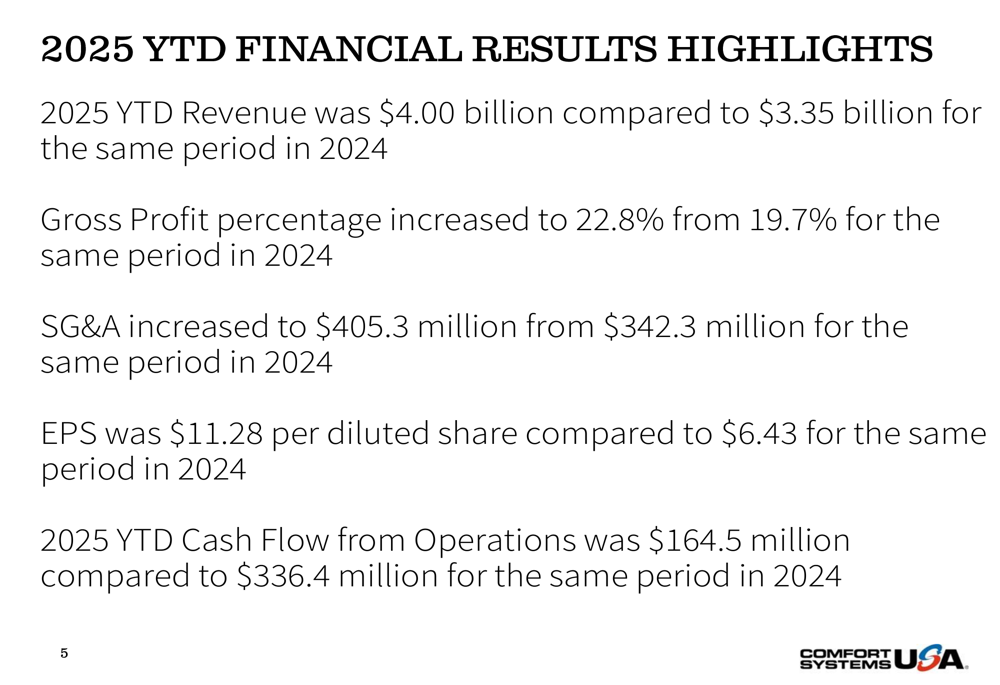

For the first half of 2025, Comfort Systems reported revenue of $4.00 billion, up from $3.35 billion in the same period of 2024. Year-to-date EPS reached $11.28, a substantial increase from $6.43 in the first half of 2024.

Backlog and Future Outlook

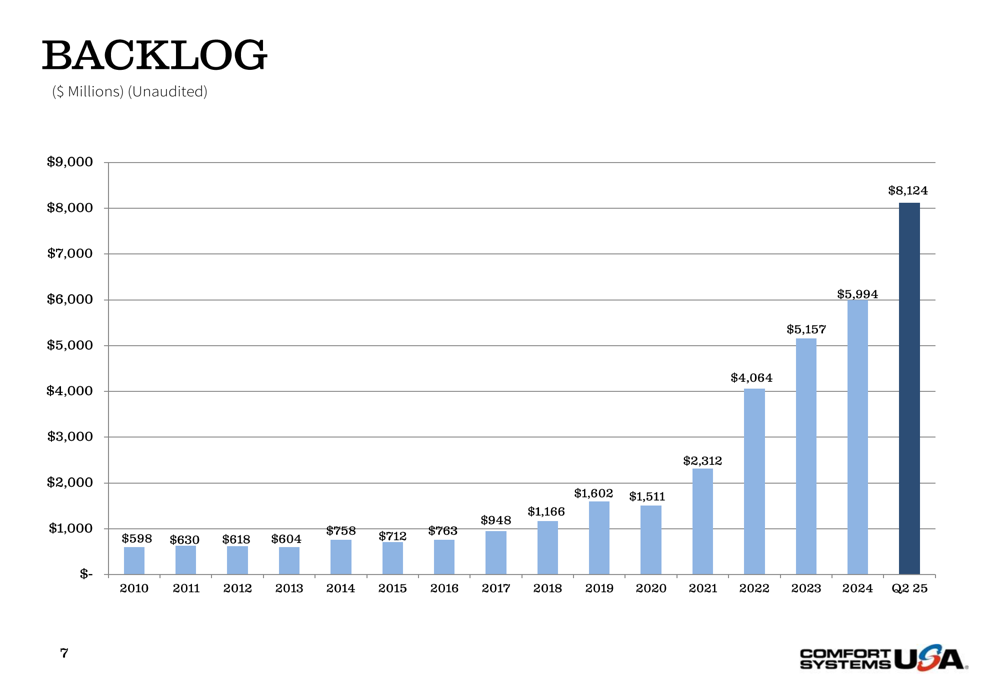

Perhaps the most compelling indicator of Comfort Systems’ future growth potential is its record backlog, which reached $8.12 billion in Q2 2025, representing a 40.7% increase from $5.77 billion in Q2 2024 and an 18% sequential increase from $6.89 billion in Q1 2025.

The following chart illustrates the company’s remarkable backlog growth trajectory since 2010:

This substantial backlog provides Comfort Systems with significant revenue visibility and suggests continued strong performance in the coming quarters. The consistent upward trend in backlog since 2010 demonstrates the company’s ability to secure new projects even as it completes existing ones, with particularly accelerated growth since 2021.

Revenue Breakdown by Customer and Activity Type

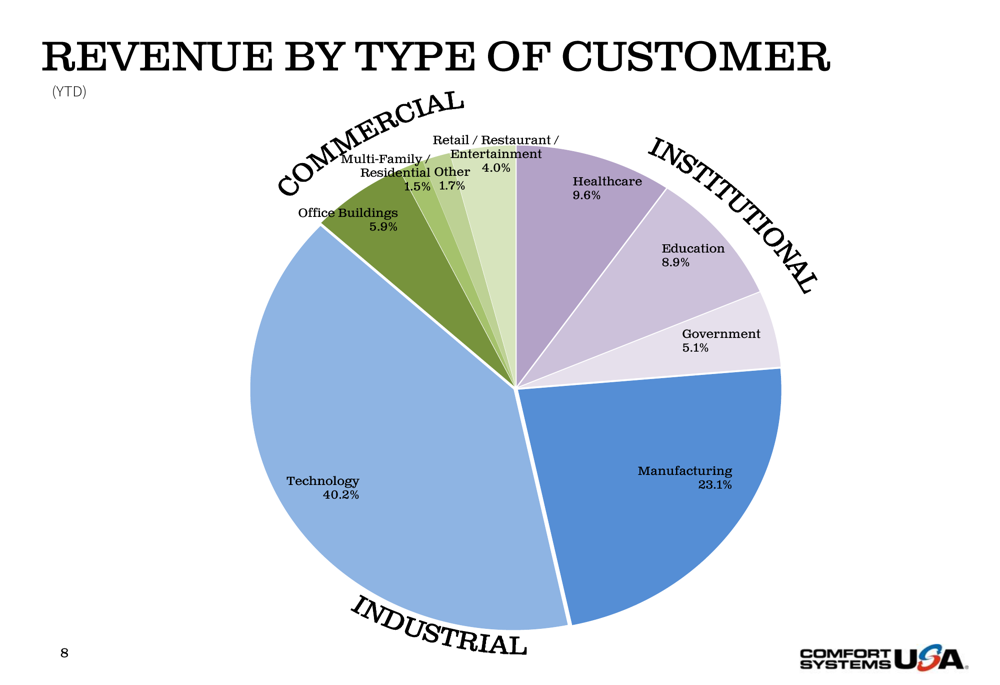

Comfort Systems’ revenue is well-diversified across various customer segments, with technology representing the largest portion at 40.2% of year-to-date 2025 revenue. Manufacturing accounts for 23.1%, while institutional customers (healthcare, education, and government) collectively represent 23.6%. Commercial segments, including office buildings, retail, and residential, make up the remaining 13.1%.

The customer revenue breakdown is illustrated in the following chart:

In terms of activity type, new construction continues to dominate Comfort Systems’ business, accounting for 58.0% of revenue in the first half of 2025, a slight increase from 56.7% for the full year 2024. Existing building construction represents 27.5% of revenue, while service projects and maintenance collectively account for 14.5%.

The comparison between YTD 2025 and Annual 2024 revenue by activity type shows minimal shifts in the company’s business mix:

The stability in revenue distribution by activity type, combined with the strong growth in overall revenue, suggests that Comfort Systems is experiencing broad-based demand across its service offerings rather than shifting its business model.

Financial Reconciliations

For investors focused on non-GAAP metrics, Comfort Systems provided detailed reconciliations of GAAP net income to adjusted EBITDA. For Q2 2025, the company reported adjusted EBITDA of $334.1 million, representing a 50.0% increase from $222.7 million in Q2 2024.

The company also reconciled GAAP cash from operating activities to free cash flow, which reached $222.2 million in Q2 2025, up from $167.3 million in Q2 2024. However, for the first half of 2025, free cash flow was $113.1 million, down from $289.9 million in the same period of 2024, potentially reflecting increased investments in working capital to support the company’s growth.

Comfort Systems’ Q2 2025 results demonstrate exceptional financial performance and strong momentum, with the record backlog suggesting continued growth in the coming quarters. The company’s diversified customer base, with significant exposure to the technology and manufacturing sectors, positions it well to capitalize on ongoing demand for mechanical and electrical installation services.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.