Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Concentra Group Holdings Parent Inc (NYSE:CON) released its first quarter 2025 results on May 7, showing solid growth and prompting the company to raise its full-year guidance. The stock responded positively in premarket trading, rising 5.58% to $23.09 after closing at $21.87 the previous day.

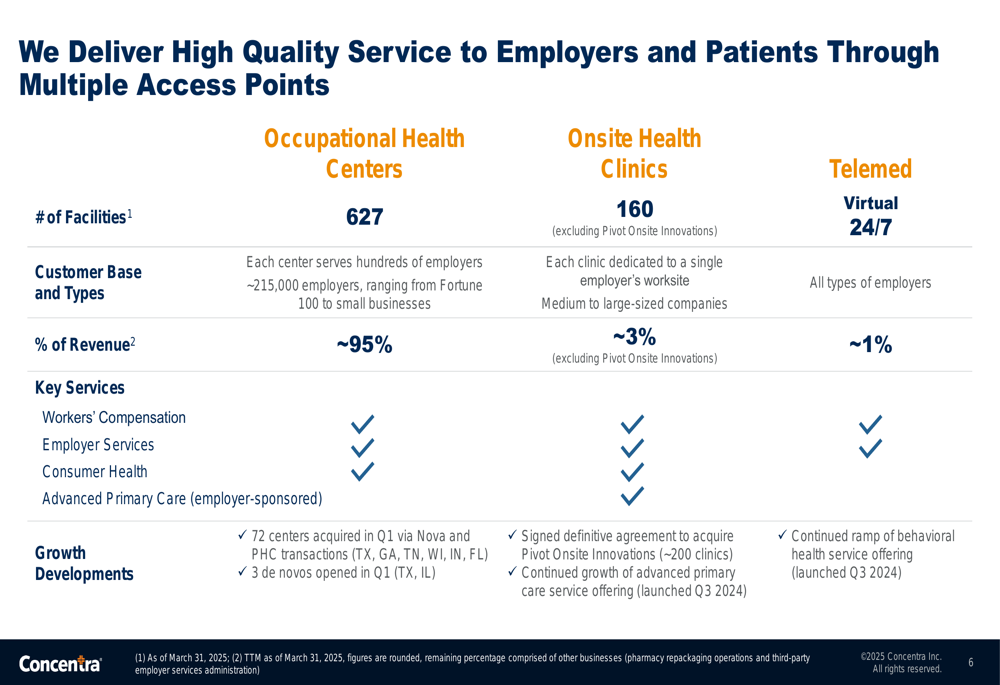

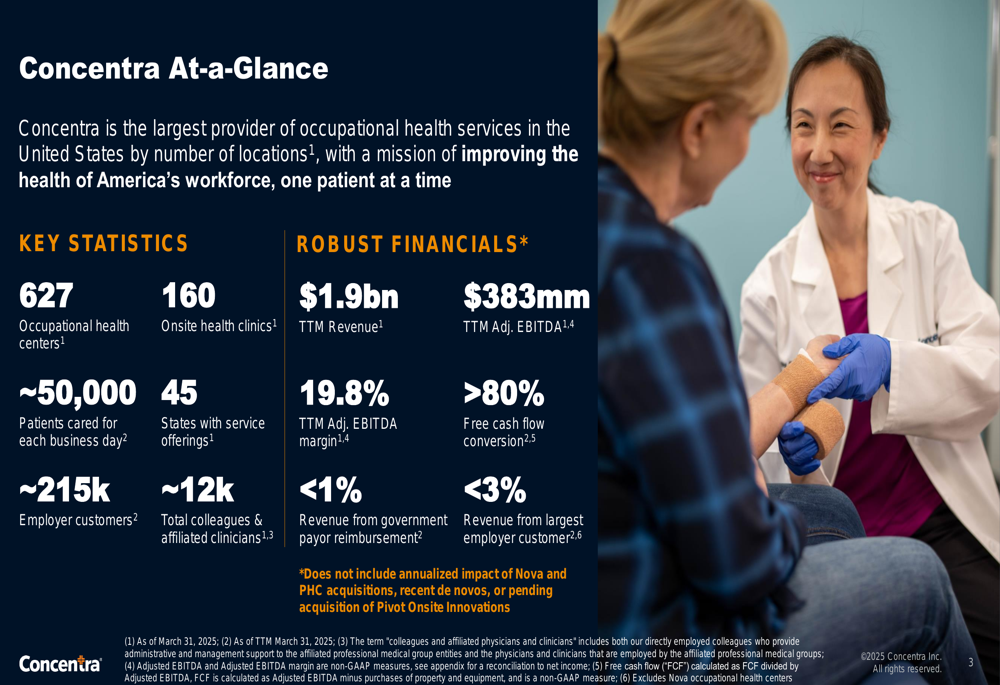

As the largest provider of occupational health services in the United States, Concentra operates 627 occupational health centers and 160 onsite health clinics across 45 states, serving approximately 50,000 patients each business day. The company’s diverse customer base includes around 215,000 employers ranging from Fortune 100 companies to small businesses.

Quarterly Performance Highlights

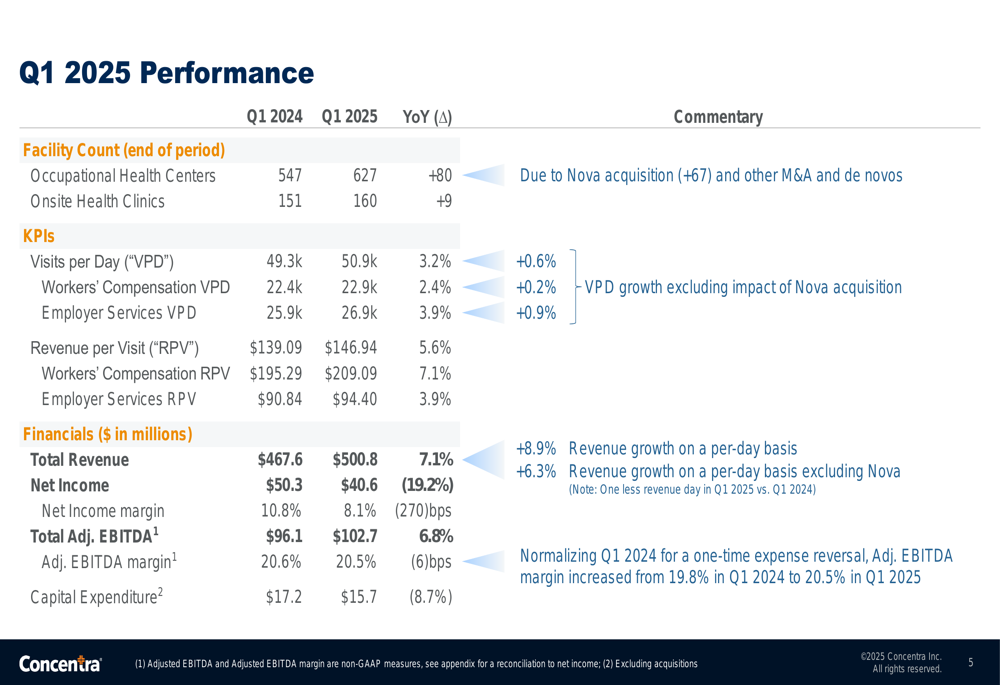

Concentra reported robust year-over-year growth in Q1 2025, with revenue increasing 7.1% to $500.8 million and Adjusted EBITDA rising 6.8% to $102.7 million, despite having one less revenue day compared to the same period last year. On a per-day basis, revenue growth was even stronger at 8.9%.

The company’s patient visits per day increased 3.2% to 50,900, with positive growth trends continuing into the second quarter. Notably, when normalizing Q1 2024 for a one-time expense reversal, Adjusted EBITDA margin improved from 19.8% to 20.5% in Q1 2025.

As shown in the following detailed performance breakdown:

However, net income decreased from $50.3 million in Q1 2024 to $40.6 million in Q1 2025. Capital expenditures also declined slightly from $17.2 million to $15.7 million year-over-year.

Strategic Initiatives & Acquisitions

Concentra’s growth strategy combines acquisitions, de novo center openings, and expansion of service offerings. During Q1 2025, the company completed the acquisitions of Nova, adding 67 centers, and PHC, adding 5 centers, with integration progressing smoothly.

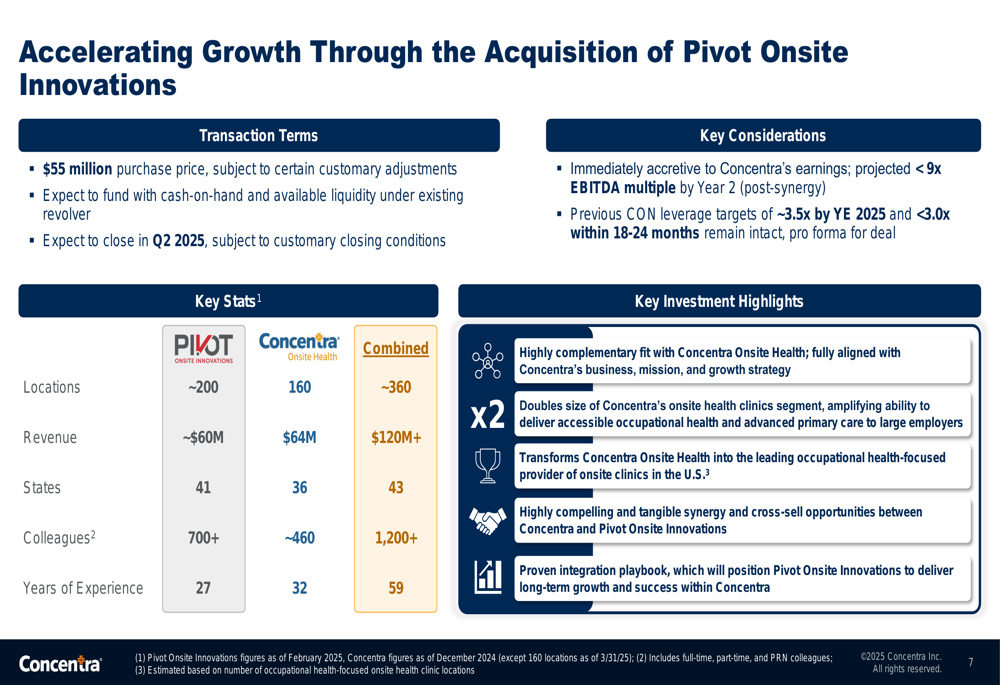

On April 21, Concentra announced the acquisition of Pivot Onsite Innovations for $55 million, which will add over 200 onsite health clinics to its portfolio. This strategic move will double the size of Concentra’s onsite health clinic segment and position the company as the leading occupational health-focused provider of onsite clinics in the United States.

The following slide details the transformative impact of the Pivot acquisition:

In addition to acquisitions, Concentra opened three de novo centers in Q1 2025 and expects to open 3-4 more by the end of the year, further expanding its geographic footprint.

Business Diversification & Resilience

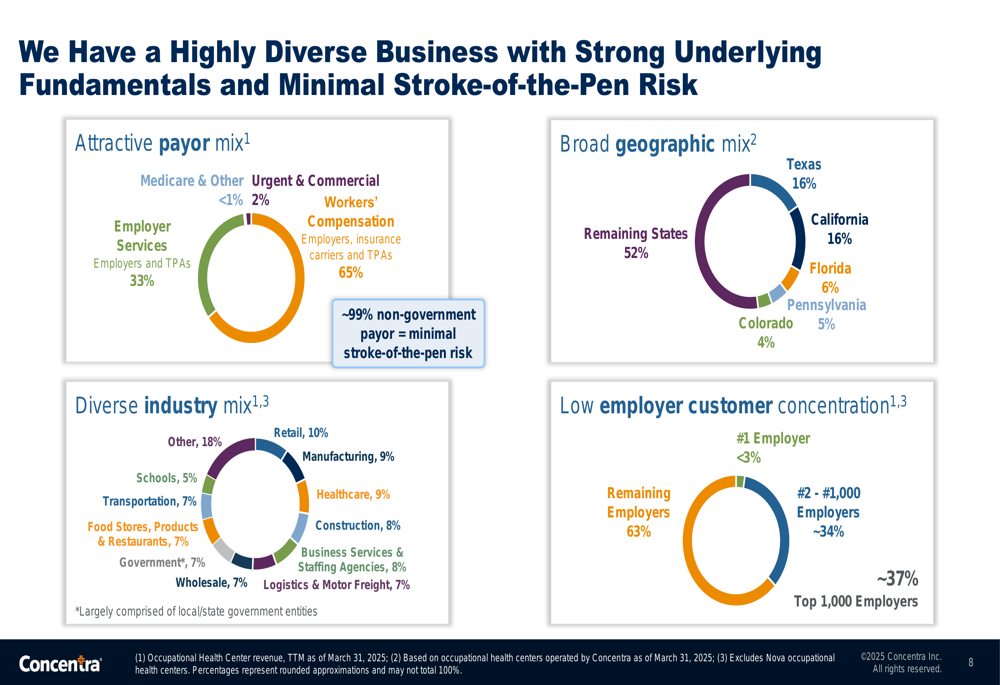

A key strength of Concentra’s business model is its diversification across payor sources, geographic regions, and industries, which helps insulate the company from economic volatility and regulatory changes.

The company derives 65% of its revenue from employers and insurance carriers, 33% from employers and TPAs, and less than 1% from government payor reimbursement. Geographically, Concentra’s revenue is spread across Texas (16%), California (16%), Florida (6%), Pennsylvania (6%), and Colorado (5%), with the remaining 51% coming from other states.

This diversification is illustrated in the following breakdown:

Concentra’s service delivery model includes multiple access points, with occupational health centers generating approximately 95% of revenue, onsite health clinics accounting for 3%, and telemedicine services representing 1%. This multi-channel approach allows the company to serve employers of all sizes with varying needs.

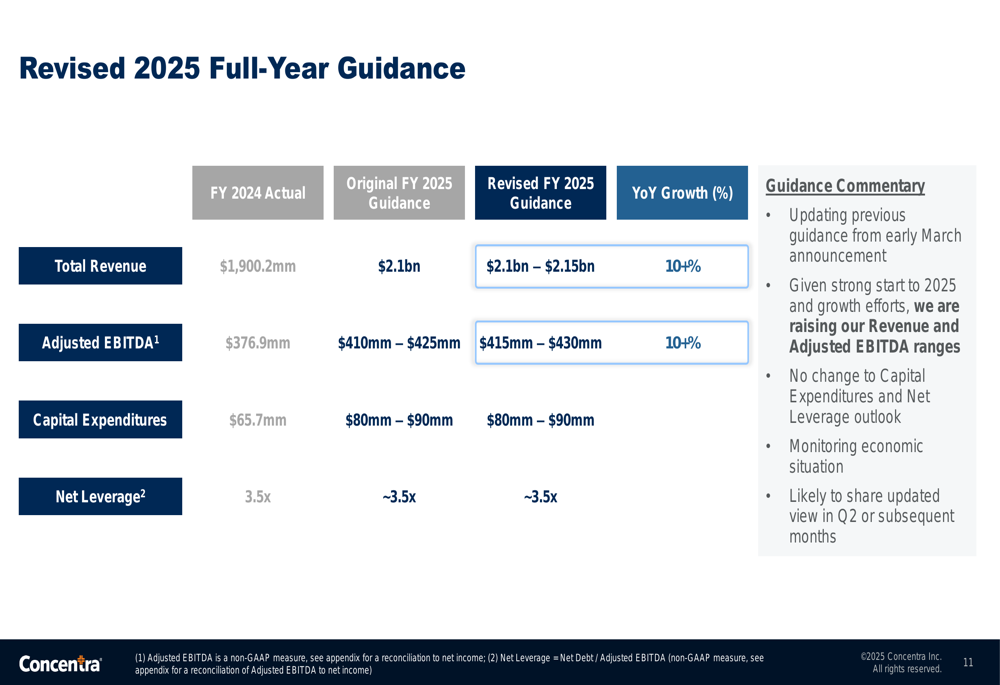

Financial Outlook & Guidance

Based on strong Q1 performance, Concentra has raised its full-year 2025 guidance. The company now expects revenue between $2.100 billion and $2.150 billion, representing over 10% year-over-year growth from the $1.900 billion reported in 2024. Adjusted EBITDA guidance has been increased to between $415 million and $430 million, also reflecting more than 10% growth from $376.9 million in 2024.

The updated guidance is detailed in the following slide:

For capital expenditures, Concentra projects $80-90 million for 2025, up from $65.7 million in 2024, reflecting investments in growth initiatives and facility improvements.

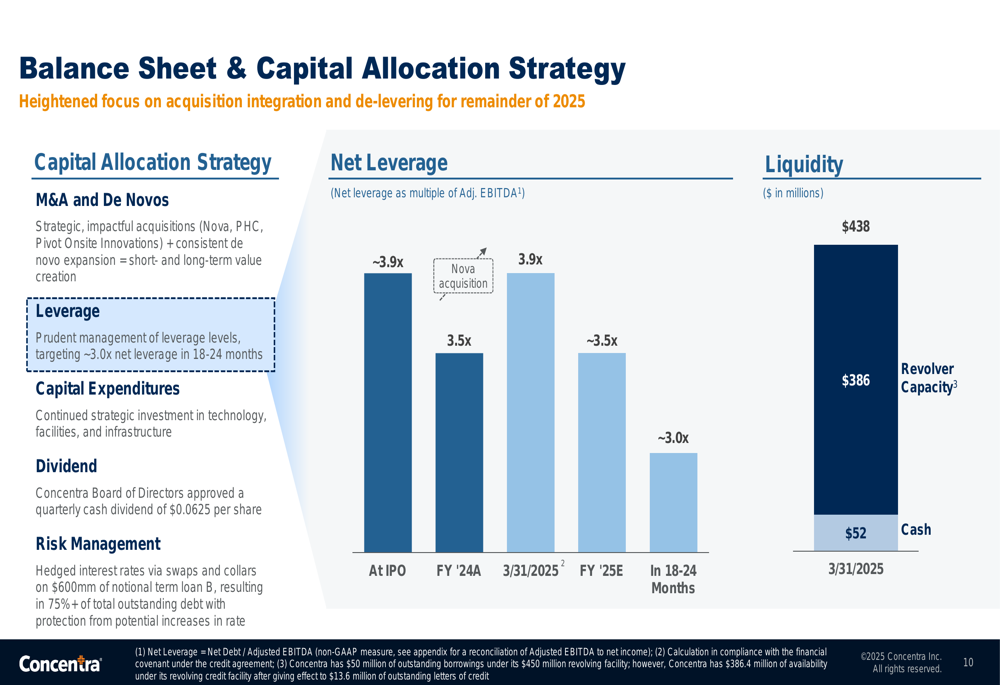

Balance Sheet & Capital Allocation

Concentra’s capital allocation strategy balances growth investments, deleveraging, and shareholder returns. The company has reiterated its deleveraging target of approximately 3.5x net leverage by year-end 2025 and approximately 3.0x within 18-24 months.

During the quarter, Concentra successfully refinanced and repriced its senior debt while upsizing its revolving credit facility. The company also hedged interest rates on $600 million of notional term loan B, resulting in more than 75% of its total outstanding debt being at fixed rates or hedged.

The company maintained its quarterly dividend of $0.0625 per share, continuing to return value to shareholders while investing in growth and reducing leverage.

Looking beyond 2025, Concentra has established long-term financial targets including mid-to-high single-digit revenue growth, continued improvement in Adjusted EBITDA margin above 20%, and robust free cash flow generation with greater than 80% annual conversion.

Market Position & Competitive Advantages

Concentra’s scale and nationwide presence provide significant competitive advantages in the occupational health services market. With 627 occupational health centers and 160 onsite clinics, the company serves approximately 215,000 employer customers, with no single customer accounting for more than 3% of revenue.

The company’s comprehensive overview highlights its market leadership:

This diversified business model with minimal exposure to government reimbursement helps insulate Concentra from regulatory changes and reimbursement pressures that affect many healthcare providers.

As occupational health services continue to be a critical component of employer healthcare strategies, Concentra’s expanded footprint and multi-channel approach position the company for sustained growth in 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.