Gold prices hold sharp gains as soft US jobs data fuels Fed rate cut bets

Introduction & Market Context

Confluent , Inc. (NASDAQ:CFLT), a data streaming platform provider, presented its Q2 FY2025 investor presentation on July 30, 2025, highlighting continued revenue growth and improved profitability metrics. The company, founded by the creators of Apache Kafka, positions itself as a critical infrastructure provider for enterprises looking to leverage real-time data in an increasingly AI-driven business environment.

Despite beating analyst expectations in Q1 2025 with EPS of $0.08 versus a forecasted $0.07, Confluent’s stock has faced pressure, dropping 9.7% in aftermarket trading following its Q1 earnings release. The stock closed at $26.97 on July 30, 2025, down 2.19% for the day, and remains closer to its 52-week low of $17.79 than its high of $37.90.

Quarterly Performance Highlights

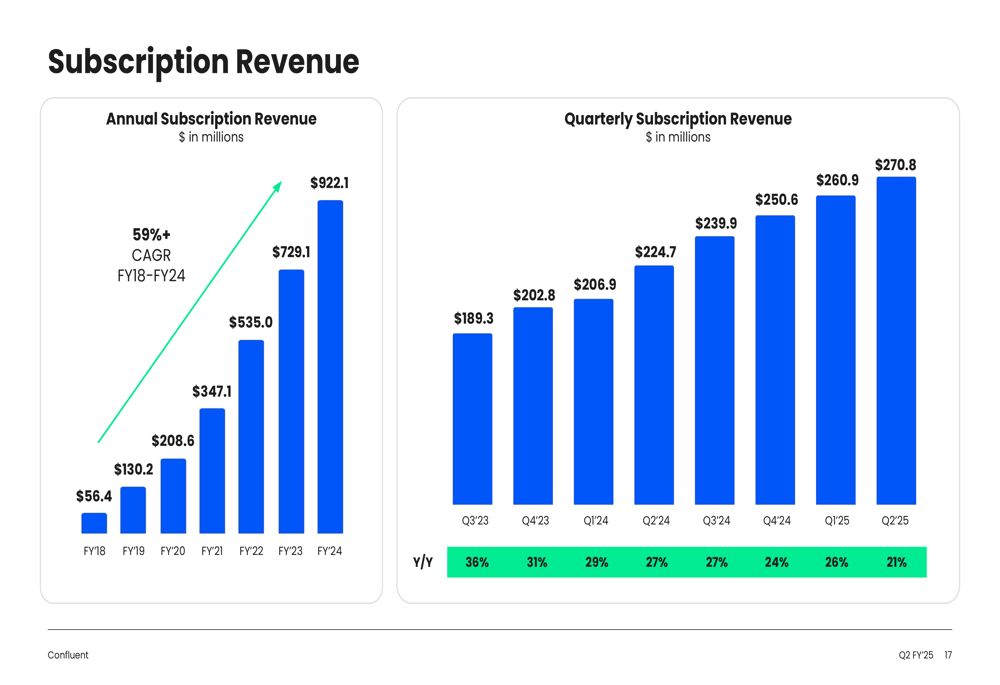

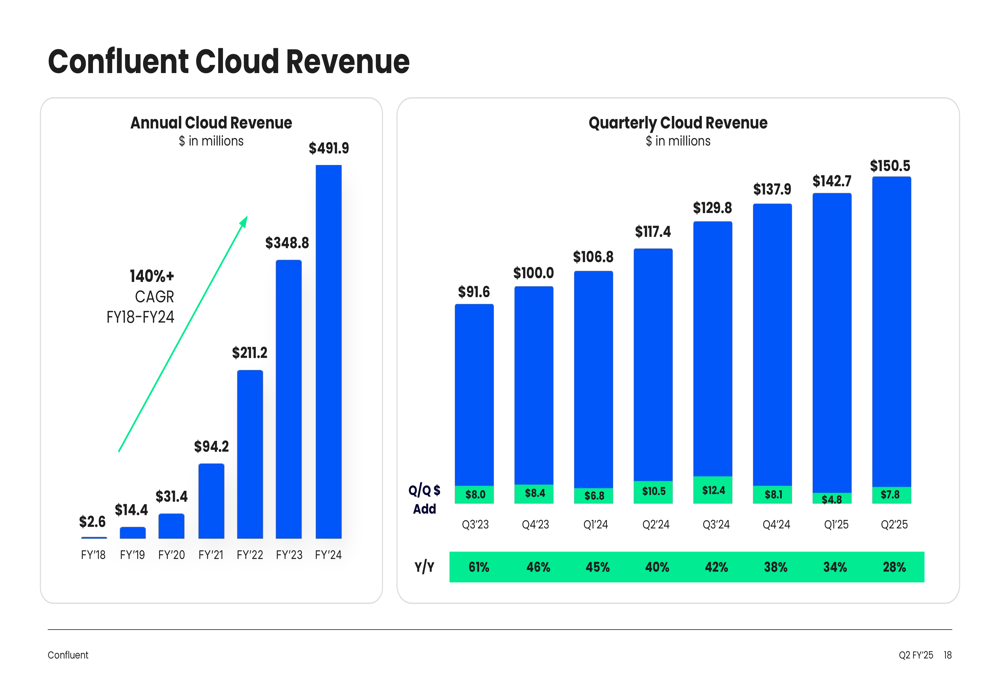

Confluent reported Q2 FY2025 subscription revenue of $271 million, representing 21% year-over-year growth. Cloud revenue, a key growth driver for the company, reached $151 million, up 28% year-over-year. The company maintained a net retention rate of 114%, though this represents a decline from the 117% reported in Q1 2025.

As shown in the following chart detailing subscription revenue growth, Confluent has maintained consistent quarterly revenue increases:

The company’s cloud revenue continues to be a significant growth driver, though the year-over-year growth rate has moderated from previous quarters:

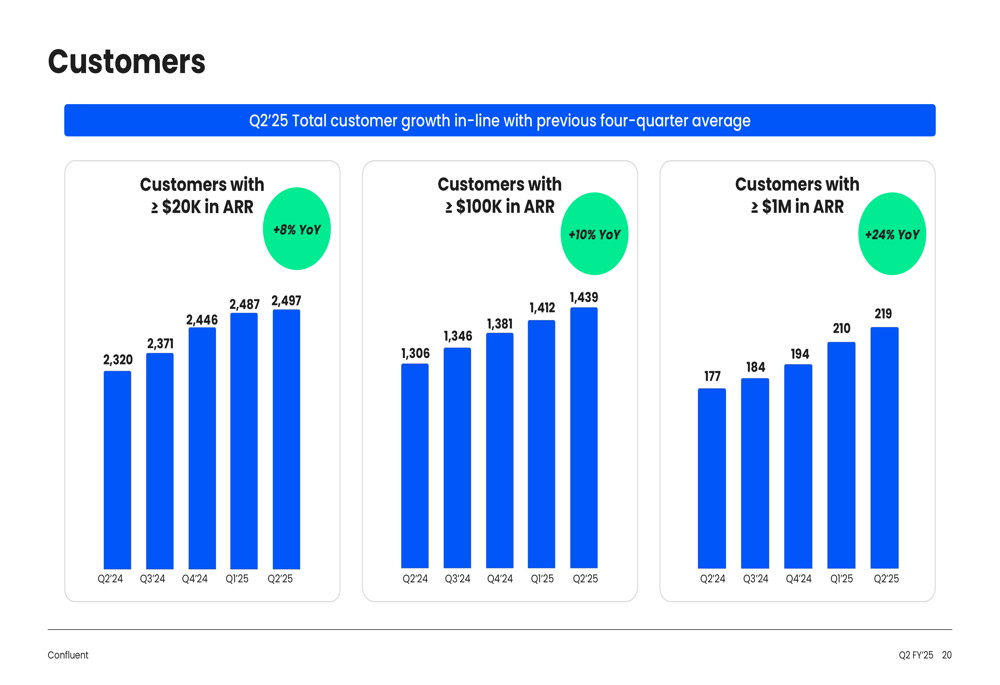

Confluent demonstrated strong progress in customer acquisition across different revenue tiers. The company now serves 2,497 customers with more than $20,000 in Annual Recurring Revenue (ARR), representing 8% year-over-year growth. More impressively, customers with over $1 million in ARR grew 24% year-over-year to 219, indicating strong traction among enterprise clients.

The following chart illustrates Confluent’s customer growth across different ARR tiers:

Strategic Initiatives & Market Positioning

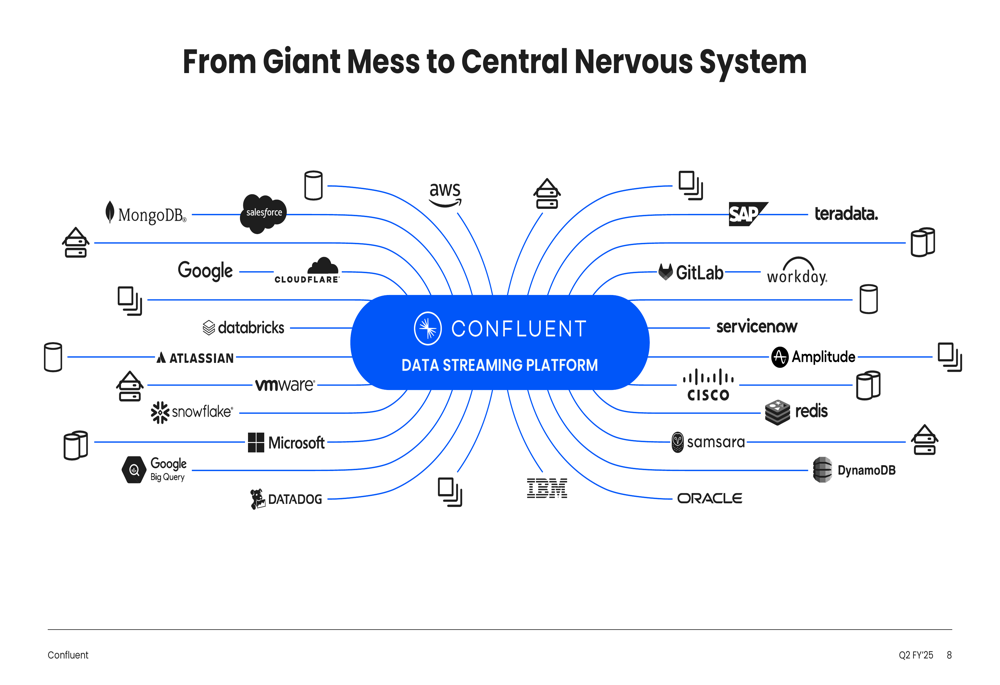

Confluent positions itself as the "central nervous system" for enterprise data, enabling organizations to move from complex, disconnected data architectures to a streamlined, real-time data platform. The company’s strategic vision is illustrated in this transformation diagram:

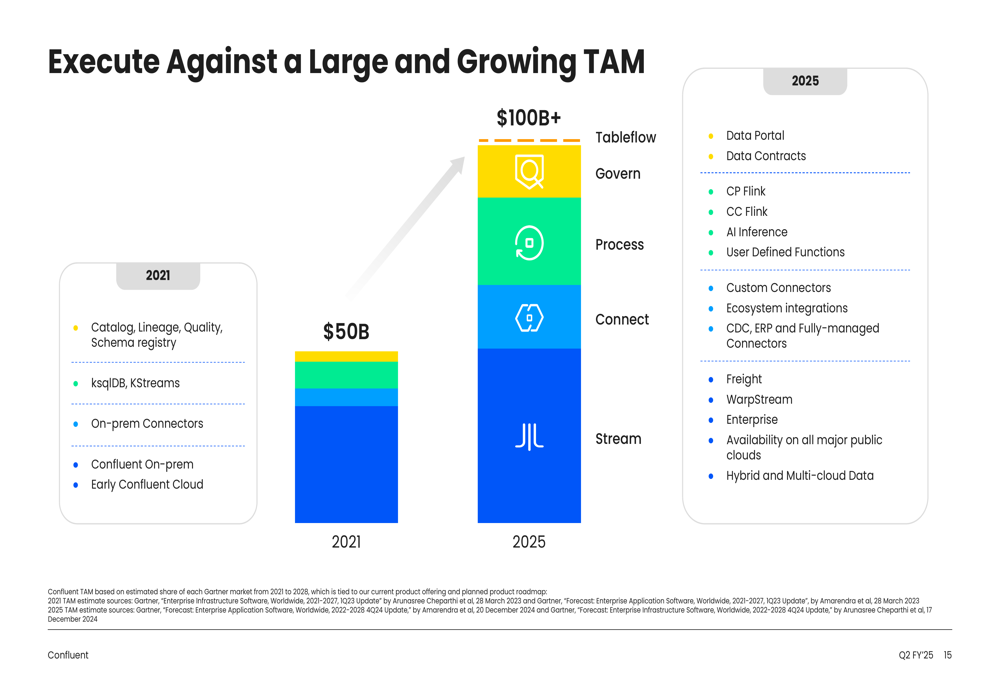

The company estimates its total addressable market (TAM) has doubled from $50 billion in 2021 to over $100 billion in 2025, driven by increasing enterprise adoption of data streaming technologies and the growing importance of real-time data processing for AI applications.

As shown in the following visualization of Confluent’s expanding market opportunity:

Confluent faces competition from legacy data infrastructure providers like Oracle (NYSE:ORCL) and IBM (NYSE:IBM), on-premises streaming solutions from Red Hat and Cloudera (NYSE:CLDR), and cloud providers including Microsoft (NASDAQ:MSFT), AWS, and Google (NASDAQ:GOOGL). However, the company emphasizes its specialized focus on data streaming and its comprehensive platform approach as key differentiators.

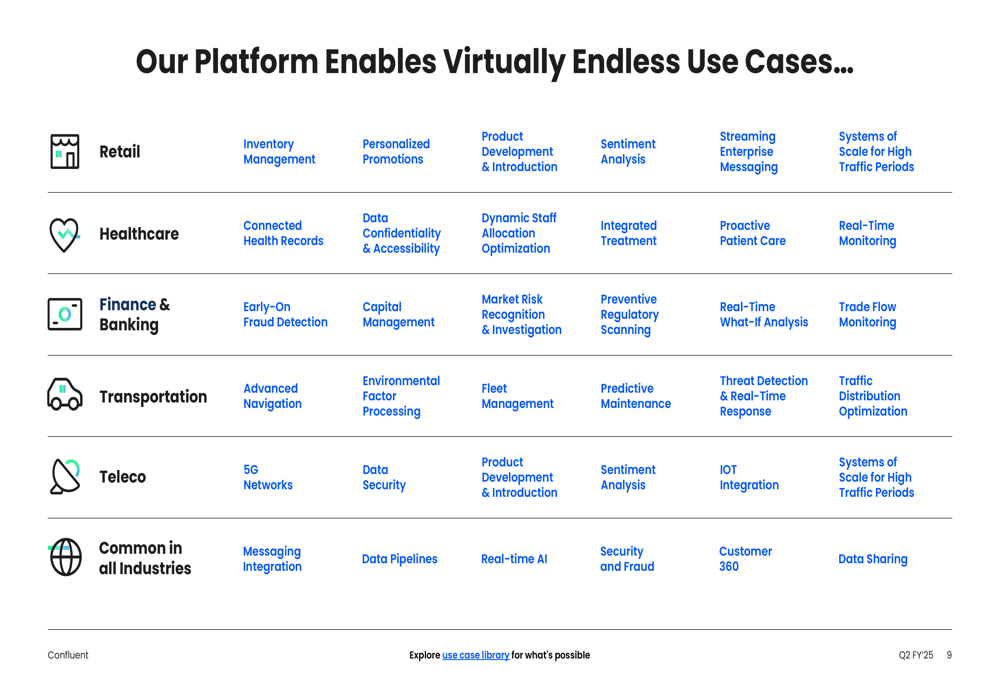

The company’s platform enables use cases across multiple industries, including retail, healthcare, finance, transportation, and telecommunications, with applications ranging from inventory management and fraud detection to real-time AI and customer 360 views.

Detailed Financial Analysis

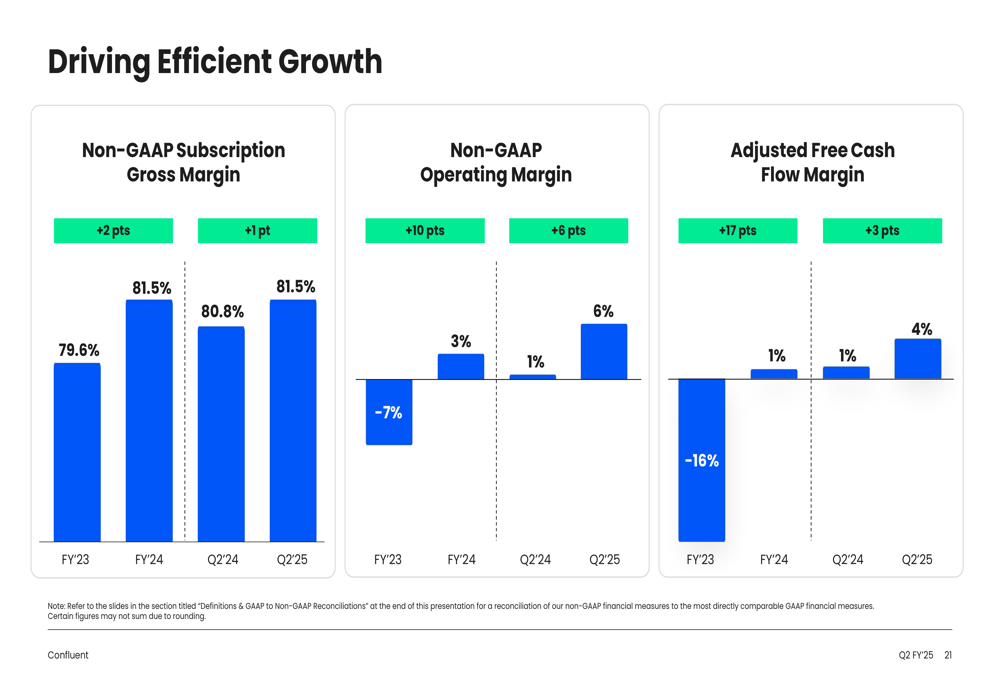

Beyond revenue growth, Confluent has made significant strides in improving profitability metrics. The company reported a non-GAAP operating margin of 6.3% in Q2 2025, an improvement of 6 percentage points year-over-year. Similarly, adjusted free cash flow margin reached 3.9%, up 3 percentage points from the previous year.

The following chart illustrates Confluent’s progress in driving efficient growth:

Confluent’s revenue mix has remained relatively stable, with international markets accounting for 58% of revenue in Q2 2025, down slightly from 61% in Q2 2024. The company’s revenue by offering shows a continued shift toward services, which represented 53% of revenue in Q2 2025 compared to 50% in Q2 2024.

The company is also focused on managing stock-based compensation (SBC) and net dilution. SBC represented 41% of revenue in FY2024, but Confluent aims to reduce this to approximately 25% by FY2027 and to mid-teens in the long term. Similarly, net dilution is targeted to decrease from approximately 3% in FY2024 to under 2% in the long term.

Forward-Looking Statements

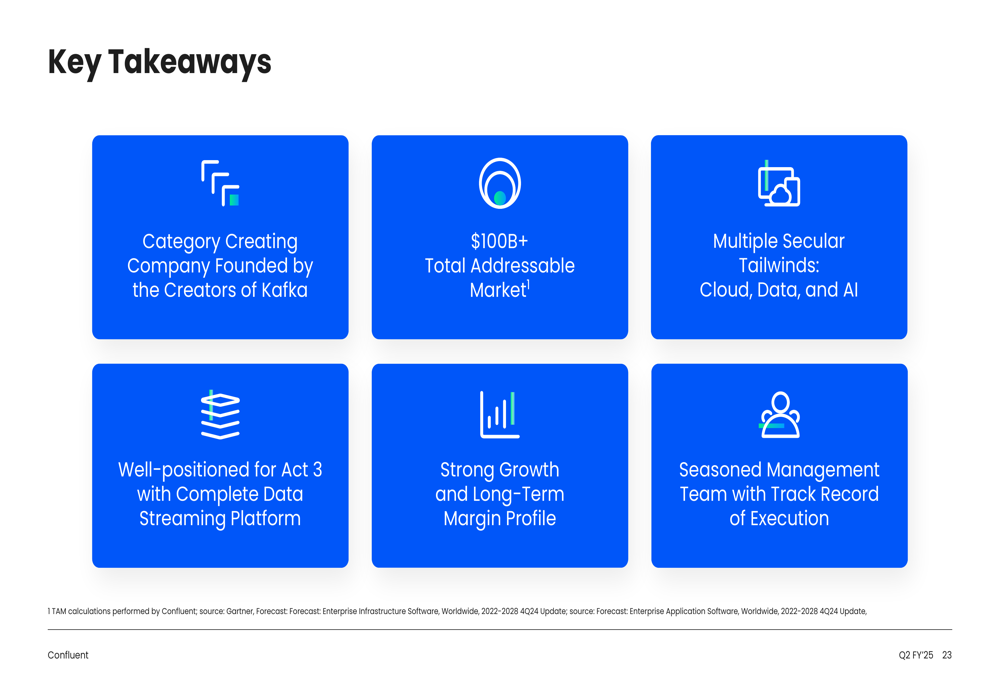

Confluent’s presentation highlights several growth drivers for its next phase of expansion, which it calls "Act 3." These include the broader streaming opportunity, its comprehensive data streaming platform, AI adoption, and an expanding partner ecosystem.

The company’s key takeaways emphasize its position as a category-creating company with a large addressable market and multiple secular tailwinds from cloud, data, and AI adoption:

However, these forward-looking statements should be viewed in context with recent market reactions and challenges noted in the Q1 earnings call. Despite beating analyst expectations, Confluent’s stock fell after Q1 earnings, possibly reflecting investor concerns about a consumption slowdown among larger cloud customers observed in March and macroeconomic uncertainties.

The company has provided conservative guidance due to these uncertainties, projecting FY2025 subscription revenue between $1.100 billion and $1.110 billion (19-20% growth) and targeting an adjusted free cash flow margin of approximately 6%.

While Confluent continues to demonstrate revenue growth and improving profitability metrics, investors should monitor key indicators like cloud revenue growth rates, net retention rates, and customer acquisition trends in upcoming quarters to assess the company’s execution against its ambitious long-term vision.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.