Gold prices rise from 2-wk low with focus on Russia-Ukraine, Jackson Hole

Introduction & Market Context

Consensus Cloud Solutions , Inc. (NASDAQ:CCSI) presented its first quarter 2025 results on May 7, 2025, revealing a continued pattern of corporate segment growth offsetting ongoing declines in its smaller business segment. The company’s stock closed at $22.31 on the day of the presentation, up 2.83% from the previous close of $21.70.

The cloud fax and digital transformation solutions provider continues to execute its two-pronged strategy: growing its higher-margin corporate business while managing the gradual decline of its Small Office/Home Office (SoHo) segment. This approach has allowed the company to maintain relatively stable overall performance despite segment-level fluctuations.

Quarterly Performance Highlights

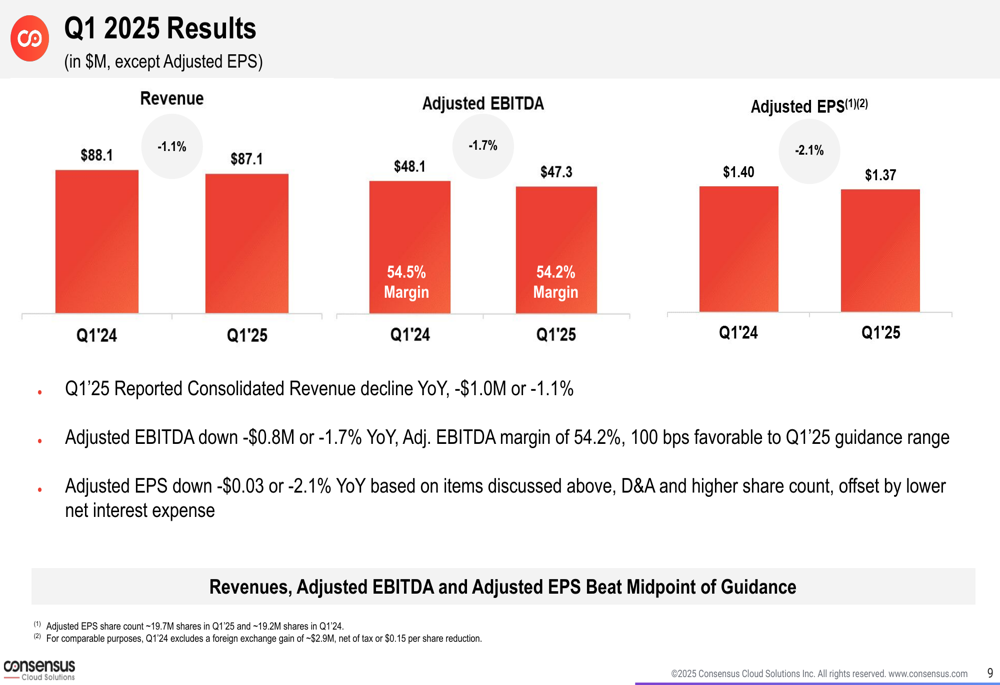

Consensus reported Q1 2025 revenue of $87.1 million, representing a slight year-over-year decline of 1.1% compared to $88.1 million in Q1 2024. Adjusted EBITDA came in at $47.3 million, down 1.7% from the prior year, though the 54.2% margin exceeded the company’s guidance range by 100 basis points.

As shown in the following comprehensive results chart:

Adjusted earnings per share reached $1.37, a 2.1% decrease from $1.40 in Q1 2024, primarily due to depreciation and amortization expenses and a higher share count, partially offset by lower net interest expense. Free cash flow for the quarter was $33.7 million, compared to $35.8 million in the same period last year.

Segment Analysis: Corporate Growth vs. SoHo Decline

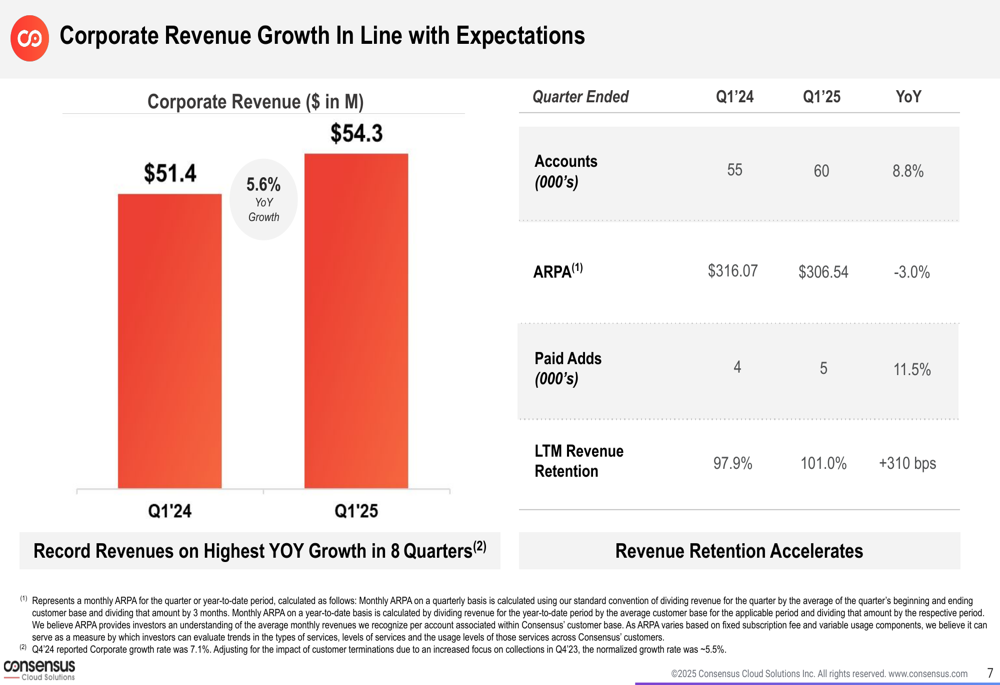

The corporate segment continued its positive trajectory, with revenue increasing 5.6% year-over-year to $54.3 million. This growth was supported by an 8.8% increase in corporate accounts to 60,000 and an improved revenue retention rate of 101%, up from 97.9% in Q1 2024. The company highlighted this as the highest year-over-year growth in eight quarters.

The following chart illustrates the corporate segment’s performance:

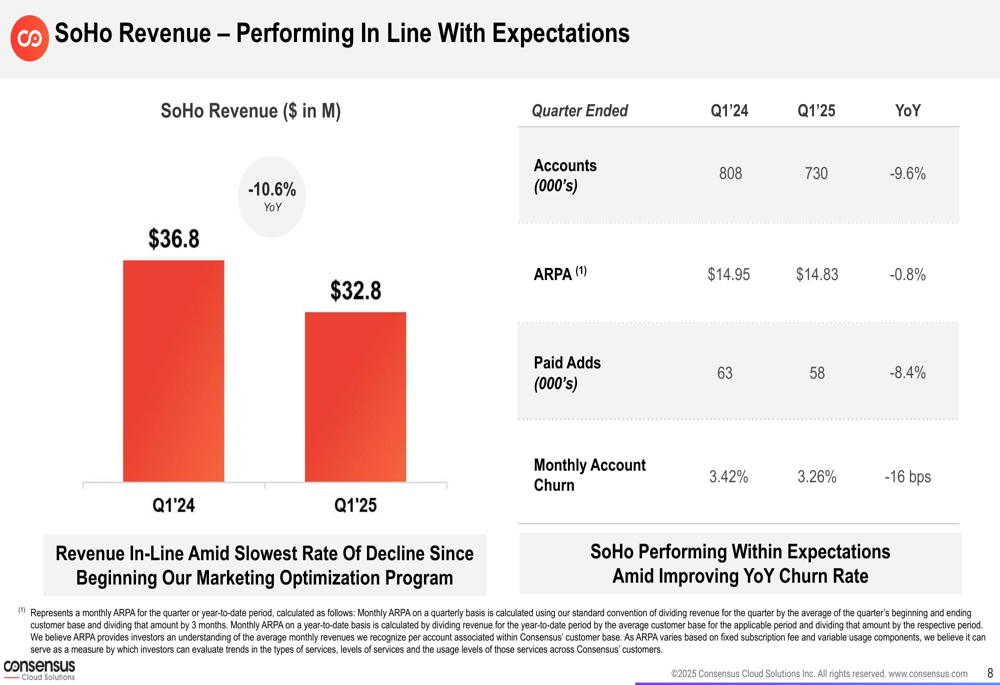

In contrast, the SoHo segment continued its expected decline, with revenue falling 10.6% year-over-year to $32.8 million. However, the company noted this represented the slowest rate of decline since beginning its marketing optimization program. The SoHo account base decreased to 730,000, down 9.6% from Q1 2024.

The SoHo segment’s performance is detailed in this chart:

Despite the revenue decline, Consensus reported encouraging signs in the SoHo business, with monthly account churn improving to 3.26%, representing the lowest churn rate in 14 quarters. This suggests the company’s efforts to optimize customer acquisition and retention are yielding positive results.

Debt Reduction Progress

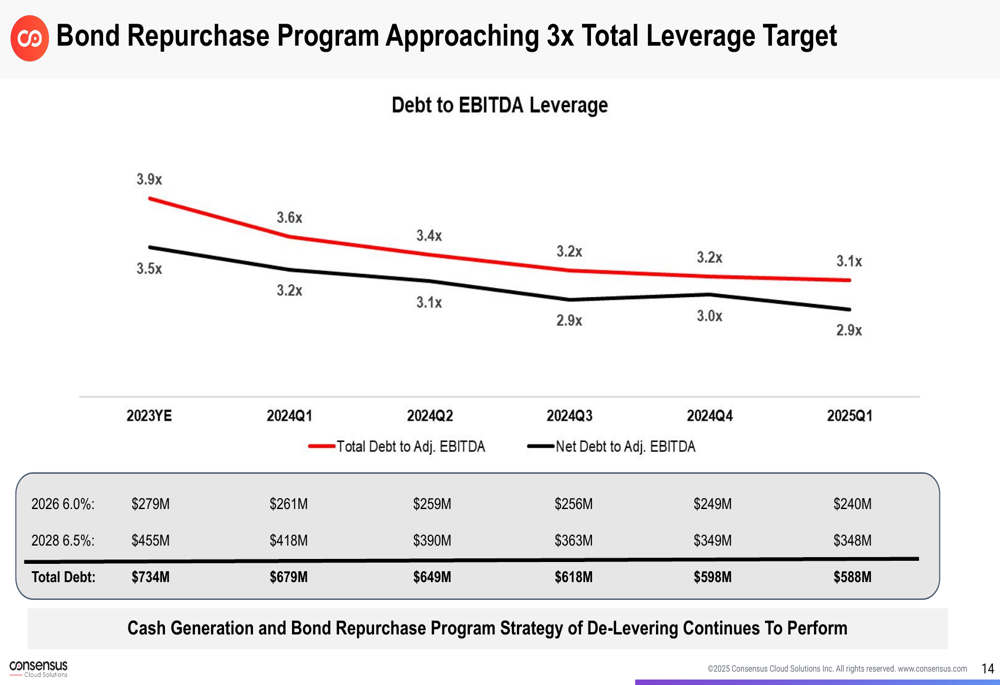

Consensus Cloud Solutions continues to prioritize debt reduction as a key component of its capital allocation strategy. During Q1 2025, the company repurchased approximately $10 million face value of bonds, bringing the program-to-date total to $223 million in bond repurchases for $209 million cash outlay.

The company’s strong cash generation has enabled consistent progress toward its leverage target, as illustrated in the following chart:

The debt-to-EBITDA ratio improved to 3.1x in Q1 2025, down from 3.2x in Q4 2024 and approaching the company’s target of 3.0x. Net debt to adjusted EBITDA stood at 2.9x, reflecting the company’s $53 million cash balance at the end of the quarter.

Forward Guidance & Outlook

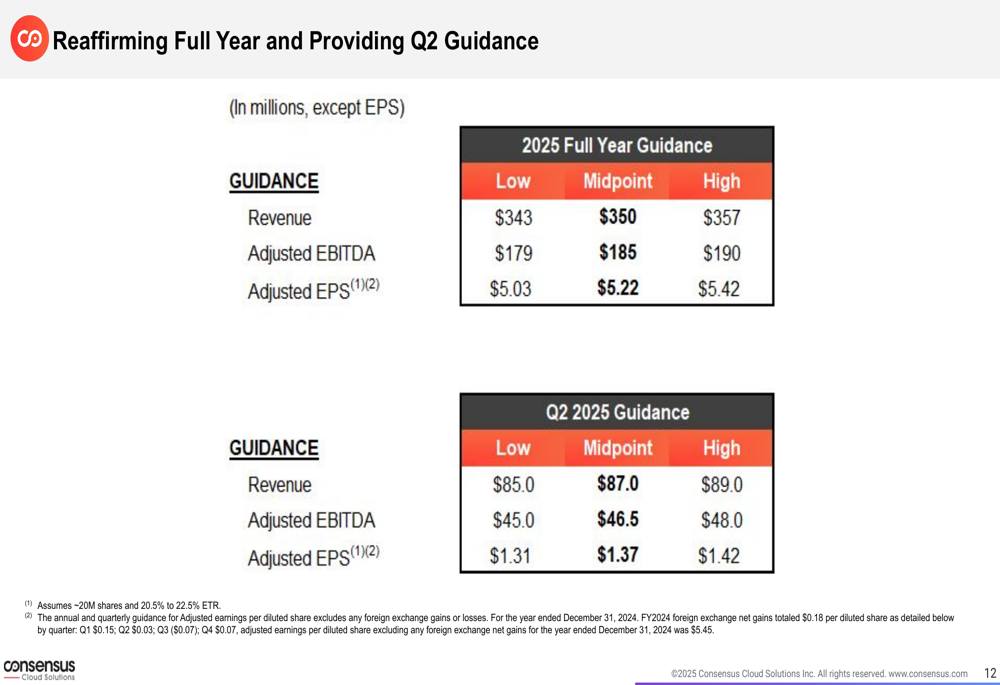

Consensus Cloud Solutions reaffirmed its full-year 2025 guidance and provided outlook for the second quarter. For the full year, the company expects:

The guidance reflects management’s confidence in continued corporate segment growth offsetting the managed decline in the SoHo business. For Q2 2025, the company projects revenue between $85.0 million and $89.0 million, with adjusted EBITDA of $45.0-$48.0 million and adjusted EPS of $1.31-$1.42.

Strategic Initiatives

The company highlighted several operational achievements during the quarter. In the corporate segment, Consensus noted sustained usage increases of cloud fax in healthcare, increased adoption of advanced products, and a successful Veterans Affairs (VA) roll-out with record usage levels.

For the SoHo business, management continues to focus on automating and optimizing customer acquisition programs while maintaining a healthy return on advertising spend and lifetime value to customer acquisition cost ratio.

Looking ahead, Consensus Cloud Solutions appears positioned to continue leveraging its strong cash flow generation to reduce debt while investing in corporate segment growth initiatives. The company’s ability to manage the SoHo segment’s decline while expanding its higher-margin corporate business will remain crucial to its overall performance throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.