ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

COPT Defense Properties (NYSE:CDP) reported strong third-quarter 2025 results, showcasing continued momentum in its specialized defense and IT-focused real estate portfolio. The company’s stock rose 3.4% to $28.20 following the announcement, reflecting investor confidence in its performance and strategic direction.

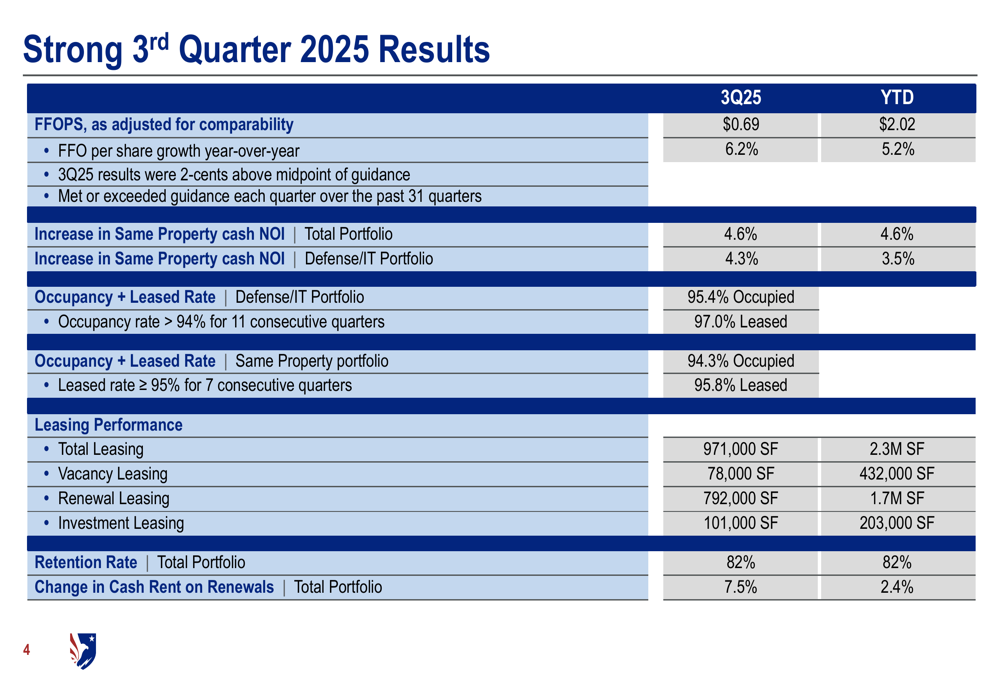

The company delivered funds from operations per share (FFOPS) of $0.69 for Q3 2025, representing a 6.2% year-over-year increase and marking its 21st consecutive quarter of FFO growth. This performance was supported by robust leasing activity, strategic acquisitions, and a favorable defense spending environment.

Quarterly Performance Highlights

COPT Defense Properties exceeded analyst expectations with earnings per share of $0.37, compared to the forecasted $0.35, and revenue of $188.8 million, surpassing the anticipated $176.36 million by 7.05%. The company’s core metrics demonstrated solid performance across its portfolio.

As shown in the following detailed performance table, CDP delivered strong results across key metrics:

The company’s same-property cash NOI increased by 4.6% year-over-year, driven by higher average occupancy, lower operating expenses, and the burn-off of free rent on development leases. The Defense/IT portfolio maintained high occupancy at 95.4% with a leased rate of 97.0%, reflecting strong demand for the company’s specialized properties.

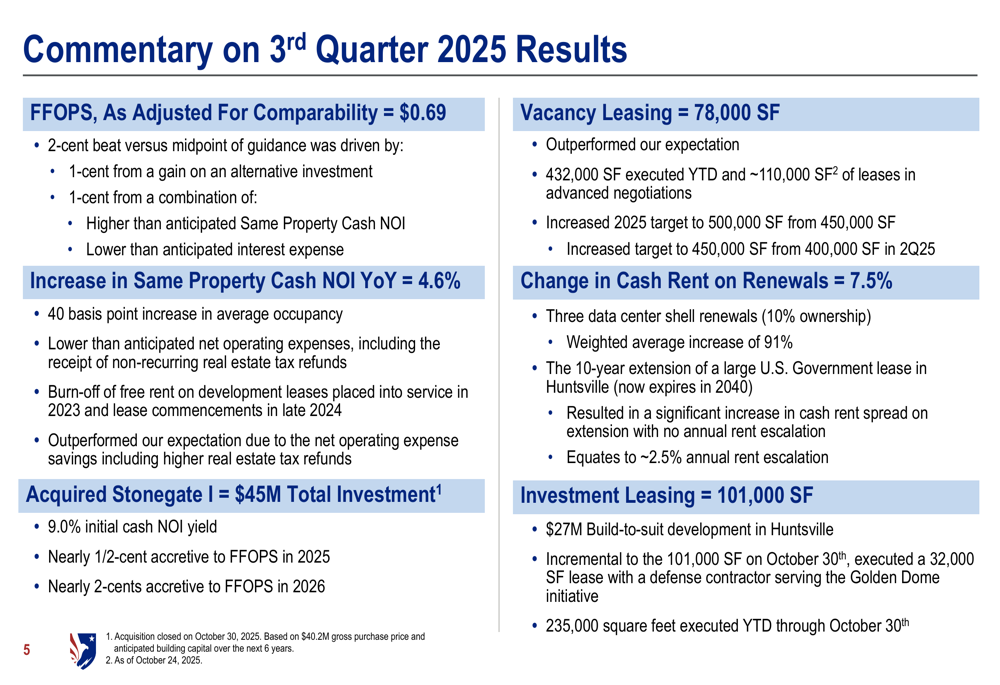

Management provided additional context for the quarter’s performance, highlighting that FFOPS beat guidance by 2 cents, with 1 cent from a gain on an alternative investment and 1 cent from a combination of higher-than-anticipated same-property cash NOI and lower interest expense:

Strategic Growth Initiatives

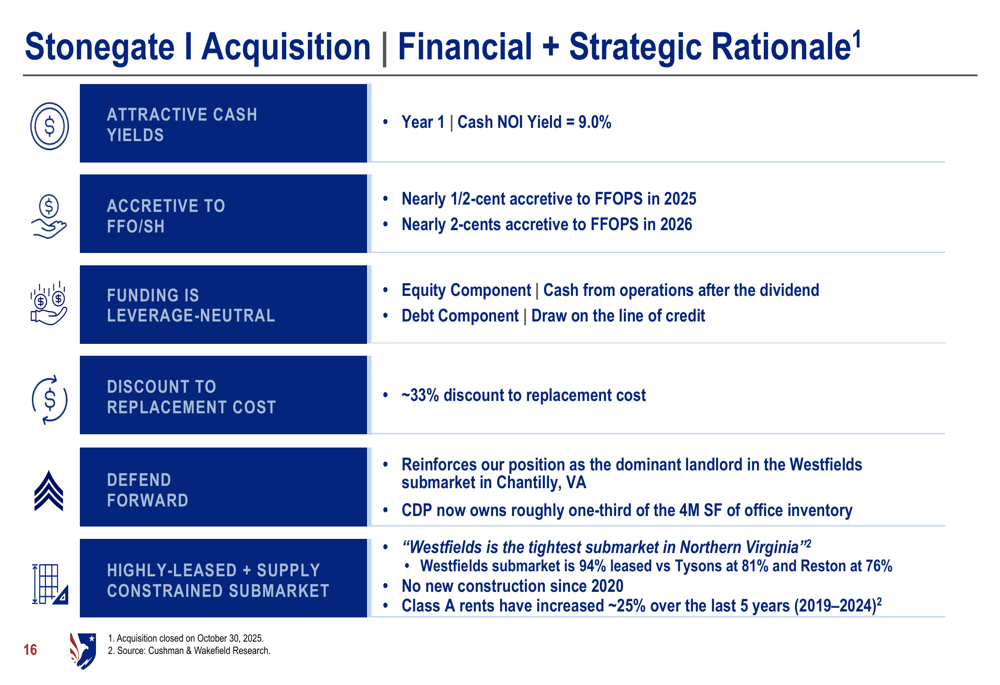

A key highlight of the quarter was the acquisition of Stonegate I, a 142,000 square foot Class A office building in Chantilly, Virginia, for a total investment of $45 million. The property is 100% leased to a top 20 U.S. defense contractor with significant SCIF (Sensitive Compartmented Information Facility) improvements and offers an attractive 9.0% initial cash NOI yield.

The acquisition is expected to be accretive to earnings, adding nearly half a cent to FFOPS in 2025 and nearly 2 cents in 2026. The property reinforces CDP’s dominant position in the Westfields submarket, where it now owns approximately one-third of the 4 million square feet of office inventory.

The company provided this detailed rationale for the Stonegate I acquisition:

Beyond acquisitions, CDP continues to invest in development projects, with $311 million of active developments totaling 812,000 square feet that are 68% pre-leased. The company has committed $124 million to new investments in 2025 to date and increased its guidance for capital commitment to new investments to $225-$275 million from the previous $200-$250 million.

Market Context & Industry Position

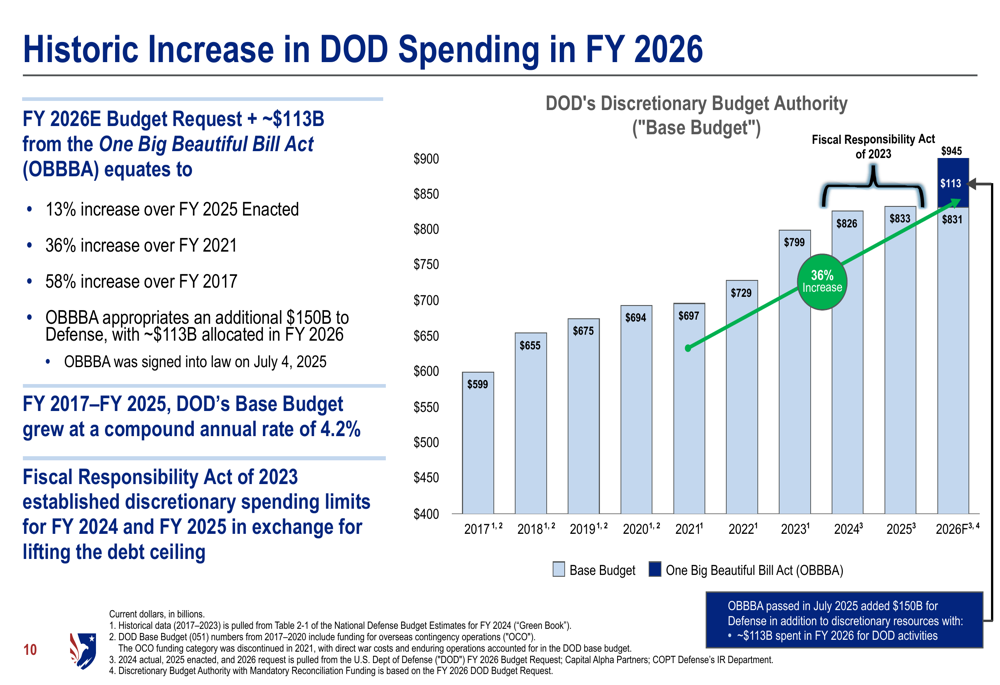

COPT Defense Properties’ strong performance is supported by a favorable defense spending environment. The presentation highlighted the historic increase in Department of Defense (DOD) spending, with the FY 2026 budget request plus additional funding from the One Big Beautiful Bill Act (OBBBA) representing a 13% increase over FY 2025 enacted levels and a 36% increase over FY 2021.

As illustrated in the following chart, defense spending is projected to continue its upward trajectory:

The company’s portfolio is strategically positioned to benefit from this increased defense spending, with 90% of its annual rental revenue coming from properties supporting defense and IT demand drivers. Key locations include the Fort Meade/BW Corridor (46% of ARR), Northern Virginia Defense/IT (13%), and Lackland AFB (10%).

CDP maintains sector-leading tenant retention rates, averaging 79% over the past five years compared to the office REIT average of 40%. This exceptional retention is driven by the company’s unique and advantaged locations, significant tenant co-investment in specialized improvements, long-term tenant relationships, and operating platform with credentialed personnel.

Forward-Looking Statements

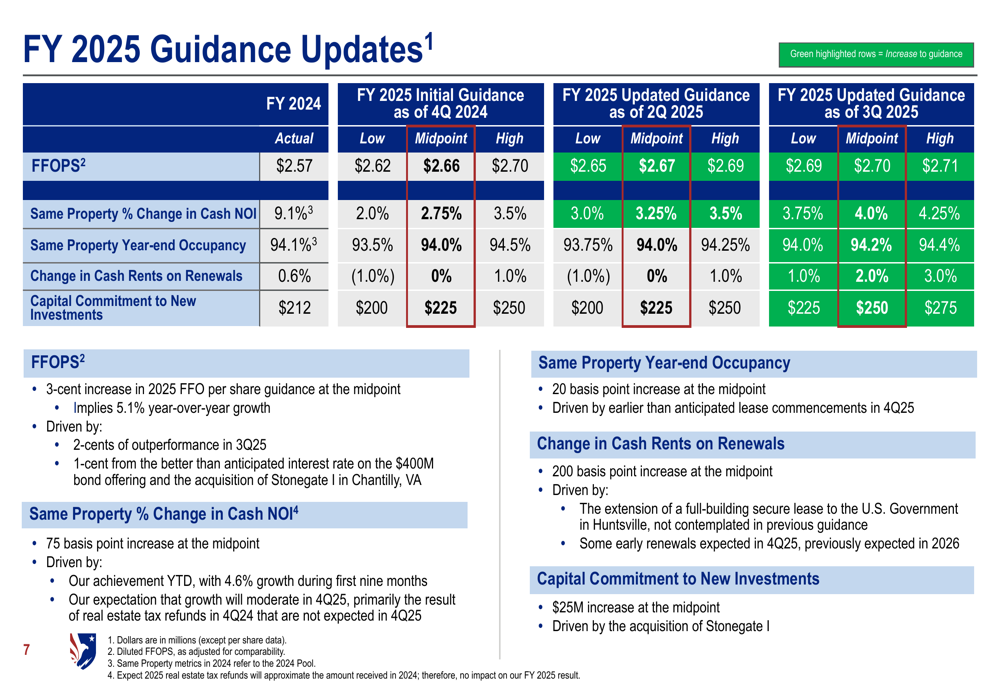

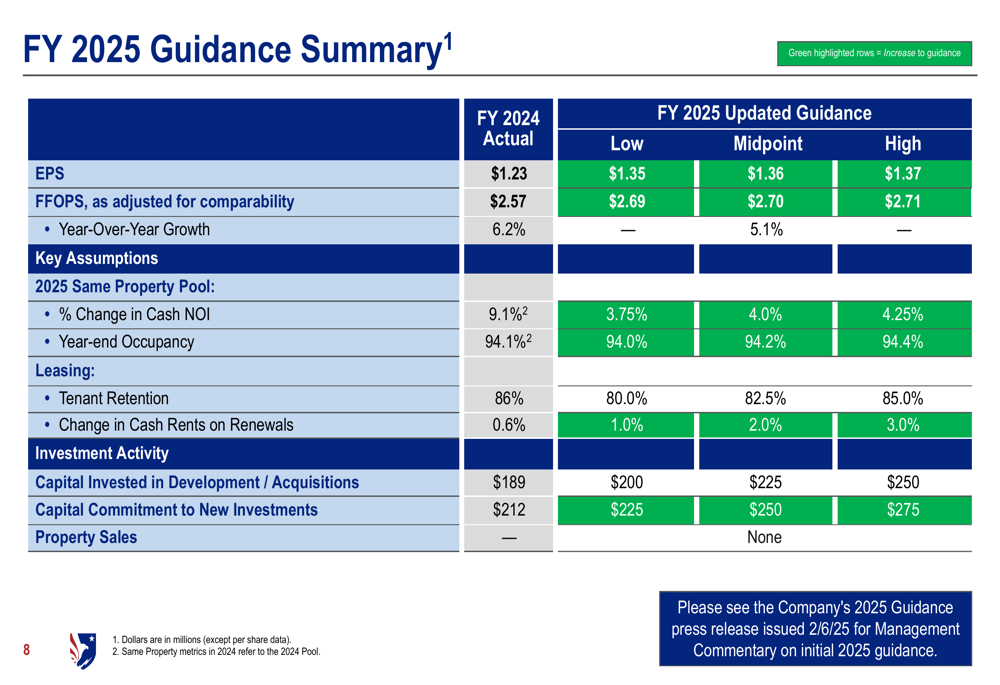

Based on its strong performance, COPT Defense Properties raised its full-year 2025 guidance. The company now expects FFOPS of $2.69-$2.71, with a midpoint of $2.70 representing 5.1% growth over 2024 results.

The updated guidance reflects increased expectations for same-property cash NOI growth (3.75%-4.25%), year-end occupancy (94.0%-94.4%), and capital commitment to new investments ($225-$275 million):

A more comprehensive summary of the company’s 2025 guidance is provided below:

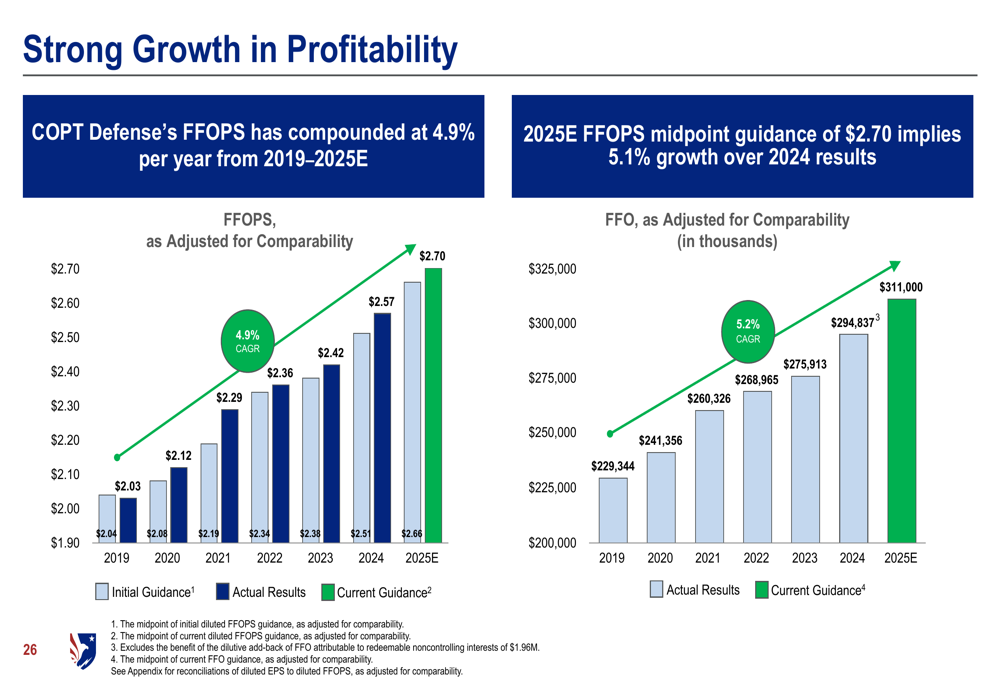

The company’s long-term growth trajectory remains strong, with FFOPS having compounded at 4.9% annually from 2019 to 2025E:

Management expects this growth momentum to continue, supported by strong leasing demand, development opportunities, and increasing defense budgets. The company anticipates that FFO per share will grow over 4% on a compounded basis between 2023 and 2026.

Financial Position

COPT Defense Properties maintains a strong balance sheet to support its growth initiatives. The company recently recast its revolving credit facility, upsizing it by $200 million to $800 million and extending the maturity by three years to 2030. Additionally, CDP entered into a $200 million secured revolving credit agreement to fund development.

The company’s debt maturity schedule is well-staggered, providing stability and flexibility. CDP pre-funded its 2026 bond maturity by issuing $400 million of 4.50% Senior Notes due 2030 on October 2, 2025. The company maintains a conservative leverage profile with a debt-to-EBITDA ratio of 6.1x as of Q3 2025.

Conclusion

COPT Defense Properties’ Q3 2025 results demonstrate the company’s continued success in capitalizing on strong demand for specialized defense and IT real estate. With robust quarterly performance, strategic acquisitions, and a favorable defense spending environment, CDP is well-positioned for sustained growth.

The company’s raised guidance for 2025, combined with its strong balance sheet and development pipeline, suggests continued positive momentum. As defense budgets continue to grow and demand for specialized facilities increases, COPT Defense Properties appears strategically positioned to benefit from these tailwinds while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.