Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Corcept Therapeutics (NASDAQ:CORT) presented its May 2025 corporate overview highlighting the company’s financial trajectory and expanding pipeline in cortisol modulation therapies. The presentation comes as Corcept maintains a strong cash position of $570.8 million while targeting substantial revenue growth for the year despite facing recent distribution challenges that impacted Q1 results.

The company, which specializes in developing medications that modulate cortisol effects, has established itself as a leader in treating hypercortisolism (Cushing’s Syndrome) and is expanding into oncology and other therapeutic areas. Corcept’s stock has delivered remarkable returns, with a 196.78% gain over the past year, though it experienced a 7.76% decline following its Q1 earnings release that showed mixed results.

Executive Summary

Corcept’s business model centers around three interconnected elements: a cash-generating operating model, a rich therapeutic platform, and collaborative research and development. This approach has enabled the company to transition from early-stage development to a profitable enterprise with multiple clinical programs.

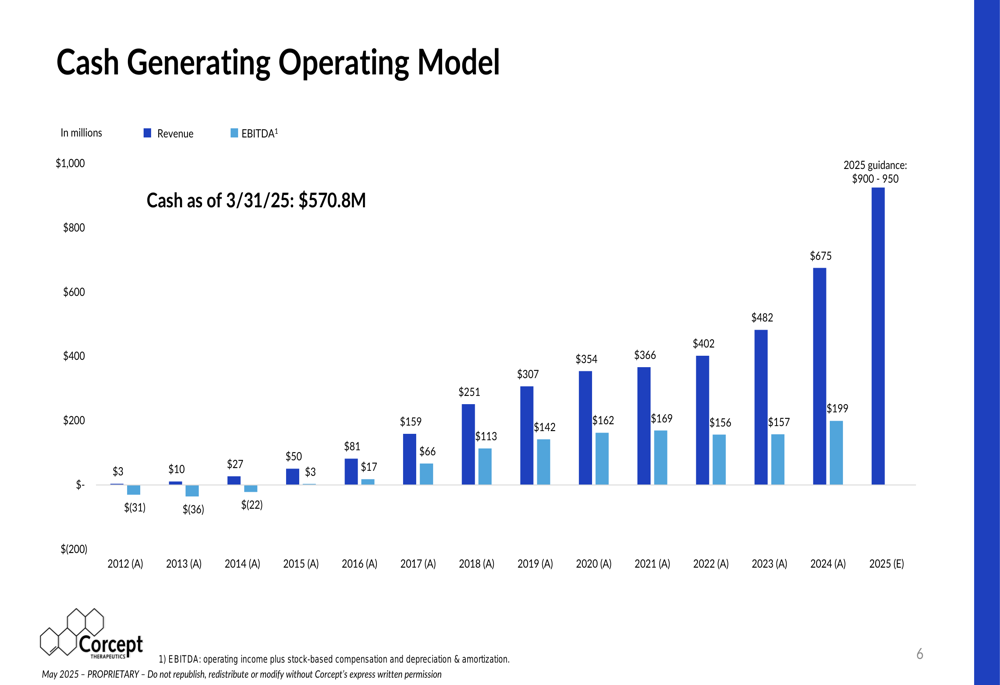

As shown in the following chart of revenue and EBITDA growth, Corcept has demonstrated consistent financial improvement since 2012, with projected 2025 revenue between $900-950 million:

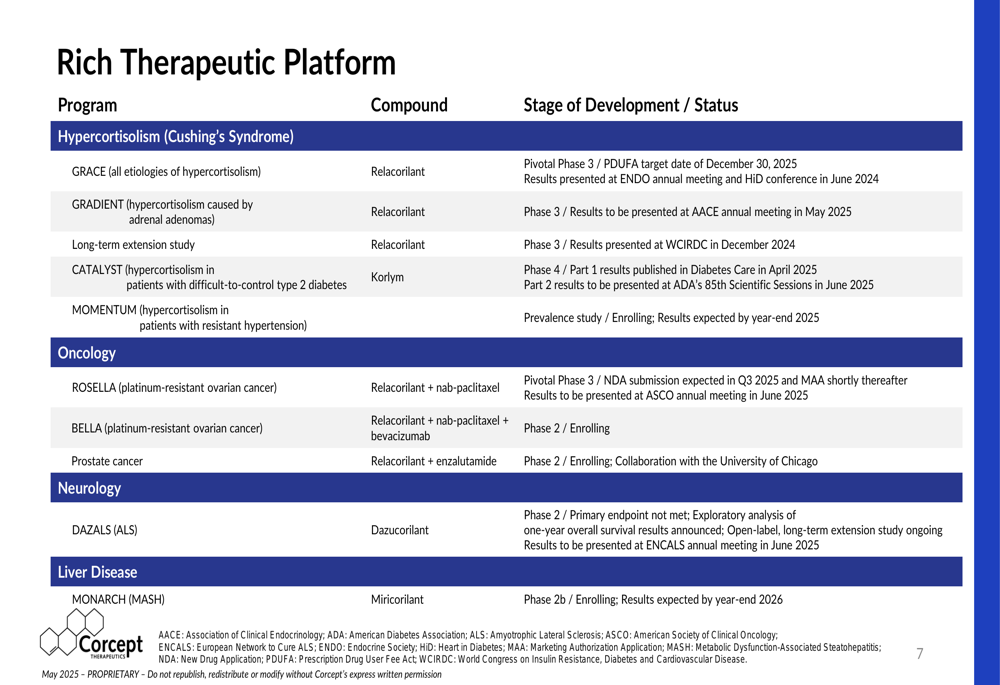

The company’s lead product, Korlym for hypercortisolism, continues to drive revenue growth, while its pipeline candidate relacorilant has completed pivotal trials and been submitted for FDA approval with a PDUFA target date of December 30, 2025. This next-generation selective cortisol modulator could potentially expand Corcept’s market reach with an improved safety profile compared to Korlym.

Financial Performance Highlights

Corcept’s financial evolution shows a remarkable transformation from a company with minimal revenue to one approaching the billion-dollar revenue mark. In 2012, the company generated just $3 million in revenue with negative EBITDA of $31 million. By 2024, revenue had grown to $675 million with EBITDA of $199 million.

For 2025, management projects revenue between $900-950 million, representing 33-41% growth over 2024. This guidance reflects confidence in overcoming the distribution challenges that affected Q1 results, when the company reported revenue of $157.2 million (missing analyst expectations of $177.94 million) and net income of $20.5 million (down from $27.8 million in Q1 2024).

Despite these short-term challenges, CEO Sean Madook expressed strong confidence during the Q1 earnings call, stating, "I have never been more confident in both our current and future commercial growth." The company’s cash position of $570.8 million provides substantial resources for continued pipeline development and potential strategic initiatives.

Pipeline Development Progress

Corcept’s pipeline spans multiple therapeutic areas, with hypercortisolism and oncology as the primary focus. The following slide illustrates the breadth of the company’s development programs:

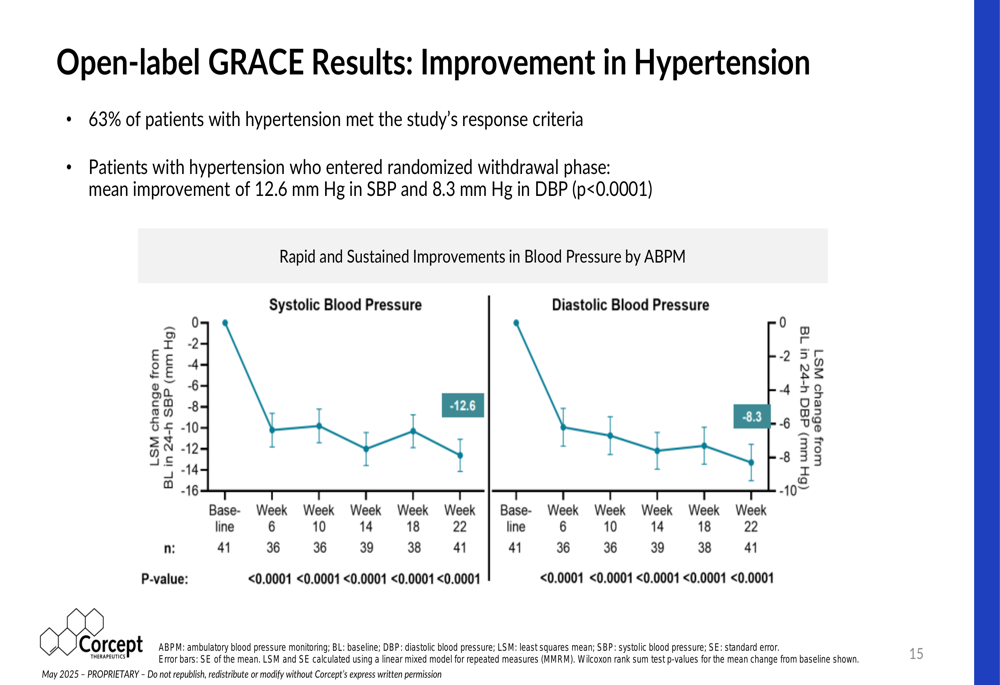

The most advanced candidate, relacorilant for hypercortisolism, has completed its pivotal Phase 3 GRACE trial, meeting its primary endpoint. The trial demonstrated that patients receiving relacorilant maintained improvements in blood pressure control compared to those on placebo.

As shown in the following chart, patients in the open-label phase of the GRACE trial experienced significant improvements in hypertension:

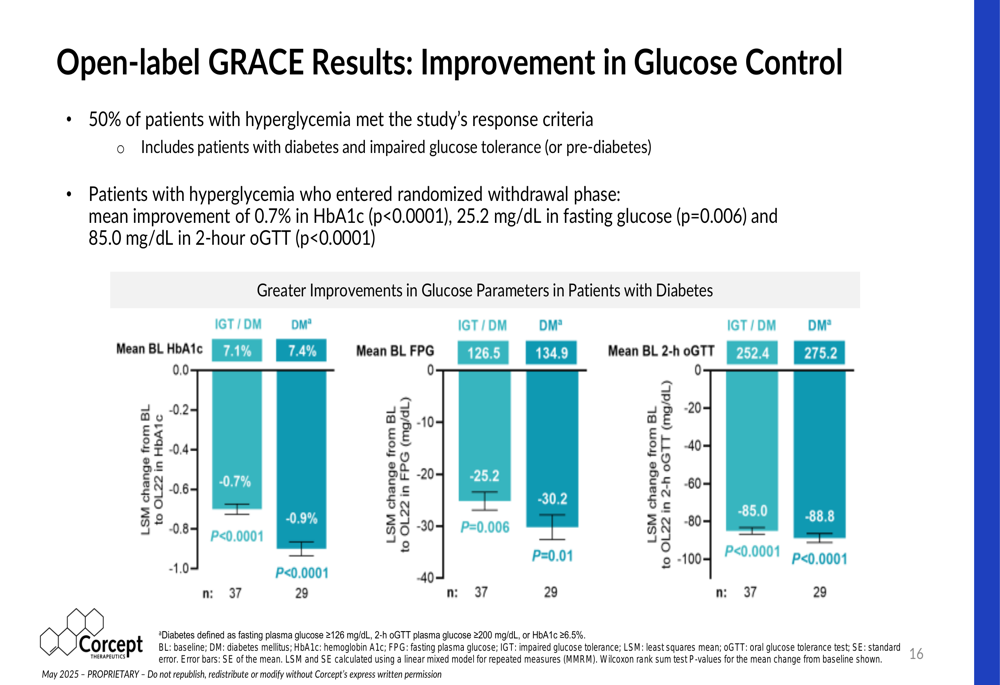

Similarly, patients with hyperglycemia showed meaningful improvements in glucose control parameters:

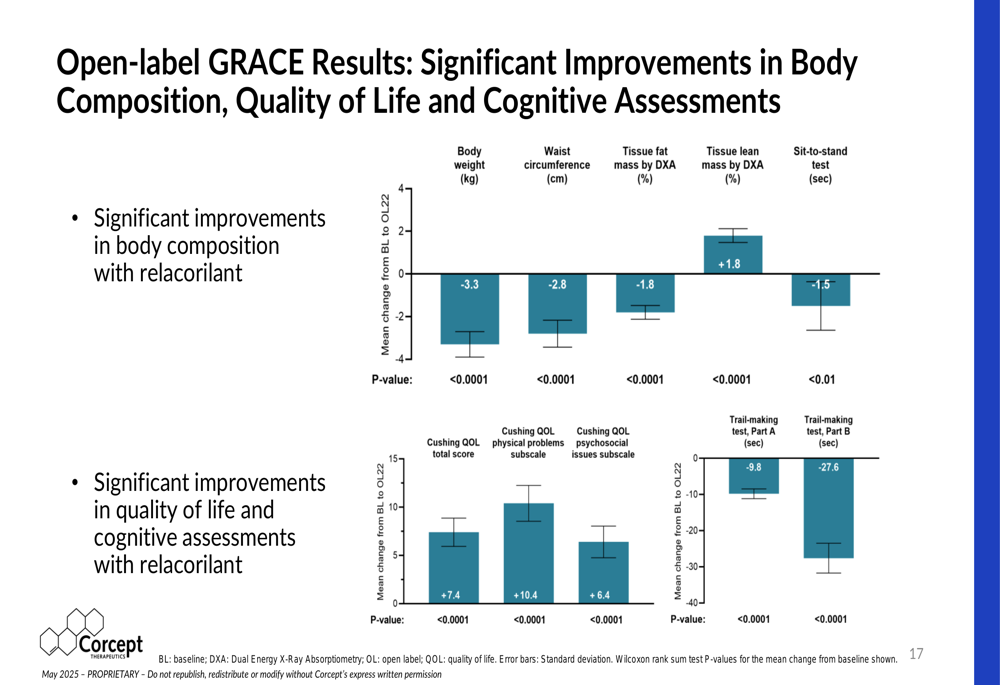

Beyond these primary endpoints, the GRACE trial demonstrated broad benefits across multiple health parameters, including body composition, quality of life, and cognitive function:

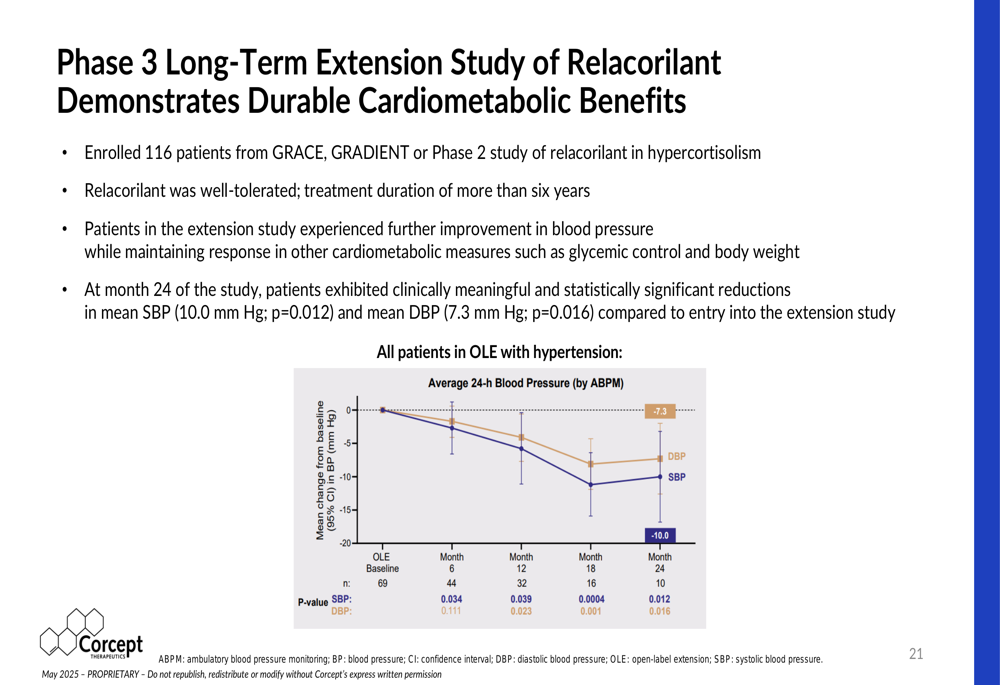

Importantly, a long-term extension study showed that these benefits were durable over time, with patients experiencing continued improvement in blood pressure while maintaining responses in other cardiometabolic measures:

Strategic Growth Initiatives

Corcept’s growth strategy extends beyond hypercortisolism into oncology and other therapeutic areas. The company’s ROSELLA trial for platinum-resistant ovarian cancer has progressed to the point where an NDA submission is expected in Q3 2025.

During the Q1 earnings call, Roberto Vieira highlighted the potential of this program, stating, "Relacorilant plus nabupac TAC cell is poised to become a new standard of care in platinum-resistant ovarian cancer."

The company’s commercial capabilities are designed to support this growth, with a focus on specialized medical professionals:

Corcept has also built a strong intellectual property position to protect its market opportunities. For Korlym, method of use patents extend to 2038, though the company faces generic competition from Teva, Sun, and Hikma. For relacorilant, composition of matter patents extend to 2038, with additional method of use, formulation, and manufacturing patents extending to 2040.

Forward-Looking Statements

Corcept’s presentation highlights the broad potential of cortisol modulation across multiple diseases. The company is exploring applications in various cancers, neurodegenerative diseases, liver disease, and metabolic disorders.

The CATALYST study, which examined patients with difficult-to-control type 2 diabetes, found that 23.8% had hypercortisolism, suggesting a significant untapped market opportunity. The study showed that patients with hypercortisolism who received Korlym experienced a 1.47% reduction in HbA1c compared to a 0.15% reduction in patients who received placebo.

Similarly, the ongoing MOMENTUM study is examining the prevalence of hypercortisolism in patients with resistant hypertension, with results expected by year-end 2025. These studies could potentially expand the addressable market for Corcept’s cortisol modulators.

While the company faces near-term challenges with pharmacy distribution issues and generic competition for Korlym, the pending approval of relacorilant and expansion into oncology provide significant growth opportunities. The stock’s current trading price of $70.06 (as of June 16, 2025) reflects investor confidence in the company’s long-term prospects, despite the recent post-earnings pullback.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.