Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

Corsair Gaming Inc . (NASDAQ:CRSR) delivered a strong second quarter for 2025, capitalizing on the wave of PC upgrades driven by next-generation graphics cards from NVIDIA (NASDAQ:NVDA) and AMD (NASDAQ:AMD). The company’s investor presentation, released on August 7, 2025, revealed substantial revenue growth and a return to profitability after facing challenges in previous quarters.

The gaming hardware manufacturer’s stock closed at $8.86 on the presentation day, near the middle of its 52-week range of $5.60 to $13.02. While the stock has faced pressure over the past year, the latest results signal potential stabilization as Corsair navigates through what it describes as a "dynamic tariff environment."

Quarterly Performance Highlights

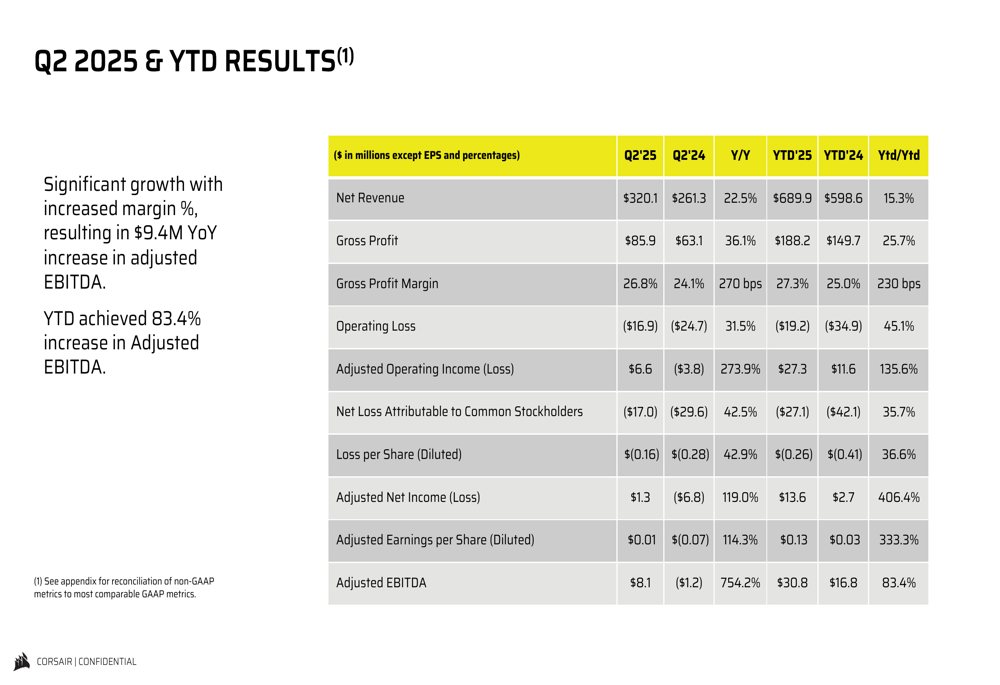

Corsair reported Q2 2025 revenue of $320.1 million, representing a 22.5% year-over-year increase. This growth was accompanied by a 36.1% jump in gross profit to $85.9 million, with gross margin expanding by 270 basis points to 26.8%.

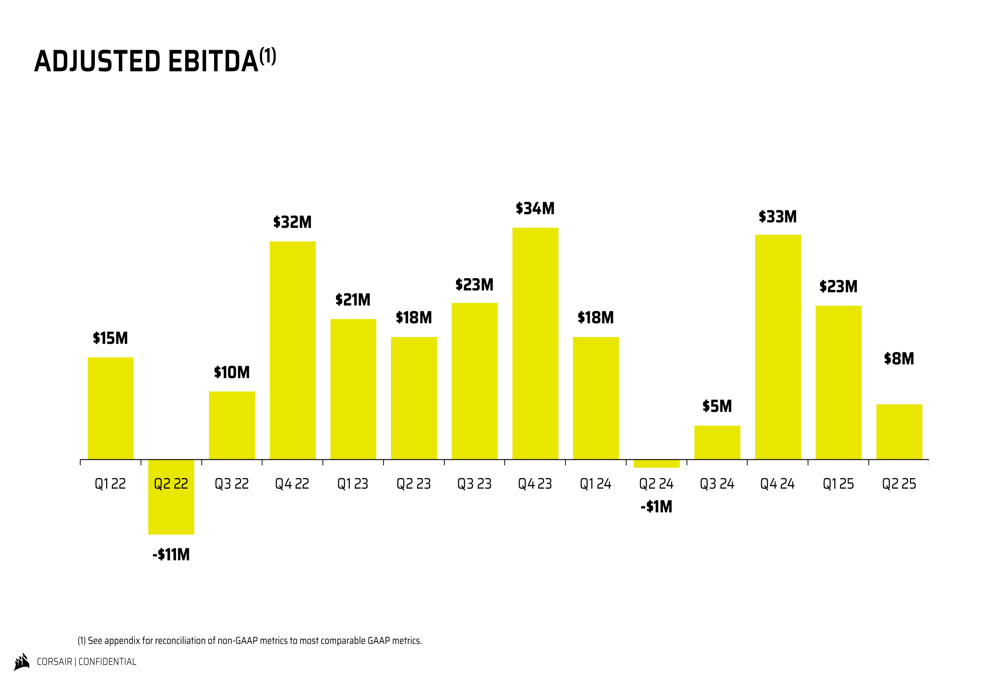

The company returned to profitability on an adjusted basis, posting adjusted operating income of $6.6 million compared to a loss of $3.8 million in the same period last year. Adjusted EBITDA showed significant improvement at $8.1 million versus a negative $1.2 million in Q2 2024, while adjusted earnings per share reached $0.01, up from a loss of $0.07 a year ago.

As shown in the following comprehensive financial results:

Segment Performance Analysis

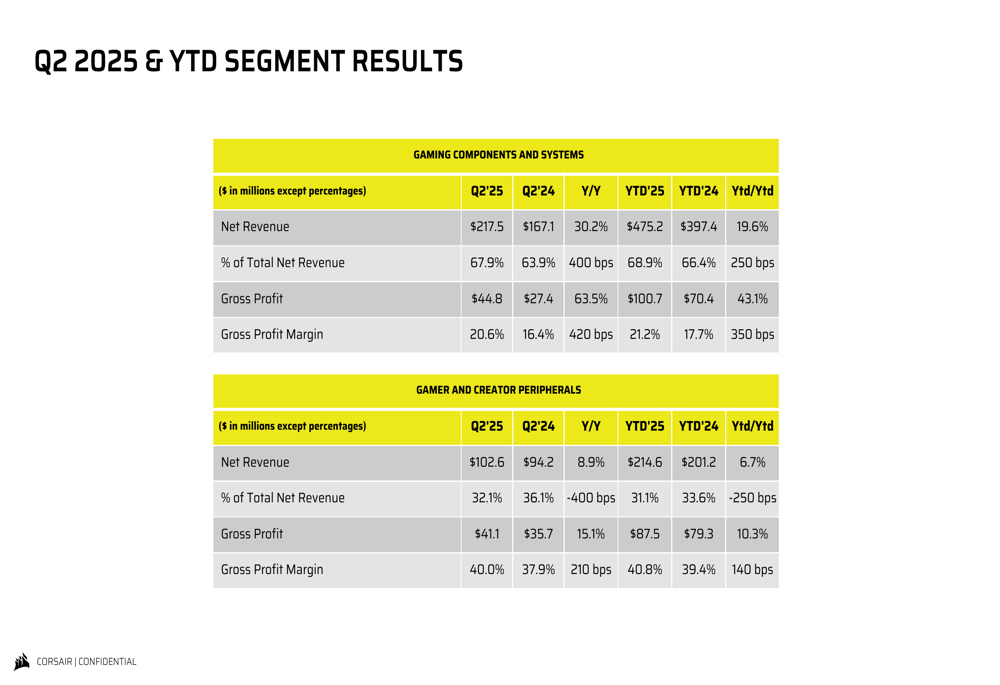

Corsair’s performance was led by its Gaming Components and Systems segment, which grew 30.2% year-over-year to $217.5 million in Q2 2025. This segment, representing 67.9% of total revenue, benefited significantly from the launch of NVIDIA’s 5000 series and AMD’s 9000 series GPUs, which drove a wave of PC upgrades and new builds. Gross profit for this segment surged 63.5% to $44.8 million, with margin expanding by 420 basis points to 20.6%.

The Gamer and Creator Peripherals segment delivered more modest but still solid growth of 8.9% year-over-year, reaching $102.6 million in Q2 2025. This segment maintained higher profitability with a gross margin of 40.0%, up 210 basis points from the prior year, and gross profit increased 15.1% to $41.1 million.

The detailed segment breakdown shows the continuing shift toward components in Corsair’s revenue mix:

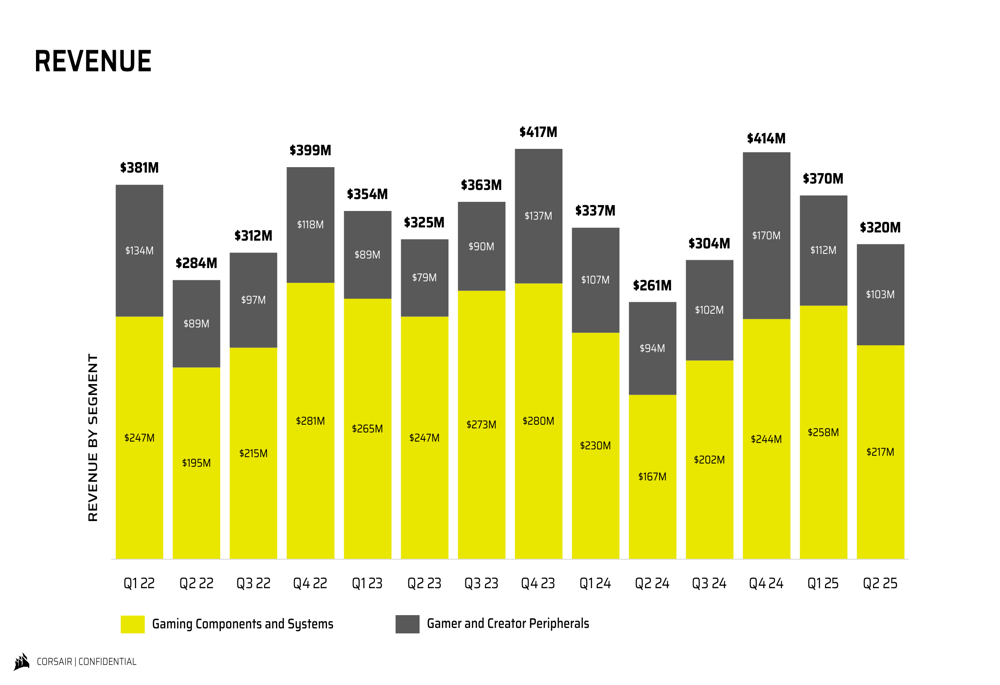

The company’s quarterly revenue trend shows recovery from previous quarters, though still below the peak levels seen in late 2022 and 2023:

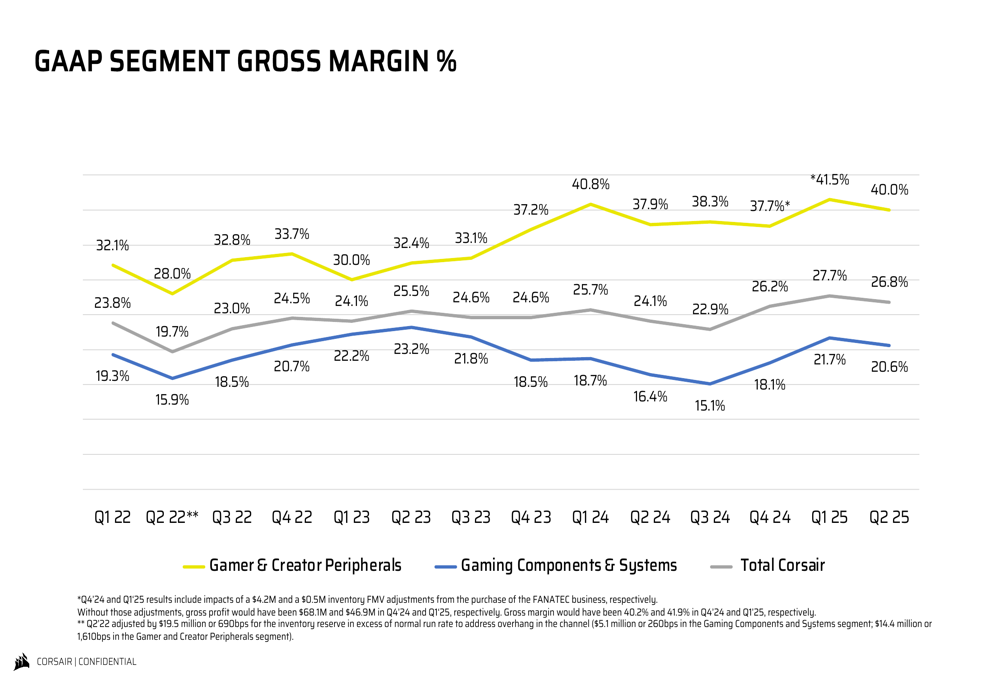

Corsair has maintained its focus on margin improvement across both segments, with particular progress in the Gaming Components and Systems business:

Strategic Initiatives and Product Innovation

Corsair highlighted several strategic initiatives and product launches that contributed to its Q2 performance. The company received multiple "Best of Computex 2025" awards for its AIR 5400 PC case, demonstrating continued innovation in its core components business.

In the peripherals segment, Corsair gained market share in both keyboard and headset categories according to third-party analysts. The company showcased several award-winning products, including the Corsair Virtuoso Max gaming headset and the Corsair MAKR 75 keyboard, which received the prestigious Red Dot Best of the Best 2025 award.

The company’s diverse brand portfolio continues to be a key strategic asset:

Corsair is also expanding into new growth areas, notably with the launch of the AI WORKSTATION 300, a compact workstation designed for developers requiring local AI inference capabilities without cloud resources. This move positions the company to capitalize on the growing demand for AI development tools.

Strategic partnerships remain important to Corsair’s growth strategy, with the company announcing collaborations with Bethesda for DOOM: The Dark Ages products and expanding its partnership with Activision (NASDAQ:ATVI) for Call of Duty: Warzone collections.

Financial Position and Outlook

Corsair continues to strengthen its balance sheet, reducing its term loan by $24 million in Q2 to $125 million. The company successfully refinanced its debt with Bank of America under an Amended and Restated Credit Agreement, which provides a $125 million term loan and a $100 million revolving credit line. Since its IPO, Corsair has reduced its total debt from $550 million to $125 million.

The company’s cash position stands at $104.6 million as of June 30, 2025, resulting in a net debt of just $20.4 million. This improved financial flexibility should help Corsair navigate market uncertainties and potential investment opportunities.

For the full year 2025, Corsair provided revenue guidance of $1.4 billion to $1.6 billion, suggesting confidence in continued growth despite tariff-related uncertainties that had previously led the company to withhold guidance in Q1.

The adjusted EBITDA trend shows volatility but overall improvement compared to the previous year:

Looking ahead, Corsair appears well-positioned to benefit from the ongoing PC hardware refresh cycle, strategic partnerships, and expansion into new product categories like AI workstations. However, the company will need to navigate tariff challenges and maintain its margin improvement trajectory to sustain its return to profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.