Bitcoin price today: slides below $100k, enters bear market amid valuation jitters

Introduction & Market Context

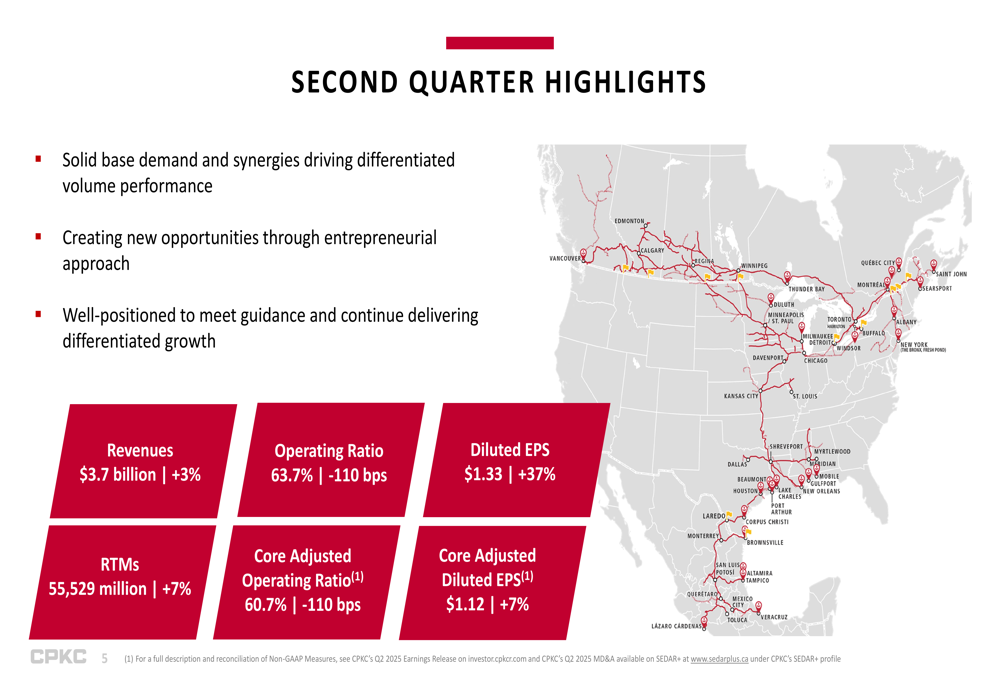

Canadian Pacific Kansas City (NYSE:CP) released its second quarter 2025 earnings presentation on July 30, 2025, revealing a 3% revenue increase to $3.7 billion and a 37% jump in diluted earnings per share to $1.33. The railroad operator demonstrated its ability to drive volume growth while improving operational efficiency, despite facing integration challenges in its southern U.S. network.

The company’s performance comes amid a period of continued transformation following the merger between Canadian Pacific and Kansas City Southern, with management emphasizing their "differentiated volume performance" driven by synergies and new business opportunities.

Quarterly Performance Highlights

CPKC reported solid financial results for the second quarter, with revenues reaching $3.7 billion, a 3% increase year-over-year. The company achieved a 110 basis point improvement in its operating ratio to 63.7%, while core adjusted operating ratio also improved by the same margin to 60.7%. Diluted EPS surged 37% to $1.33, with core adjusted diluted EPS increasing 7% to $1.12.

As shown in the following comprehensive overview of the quarter’s key metrics:

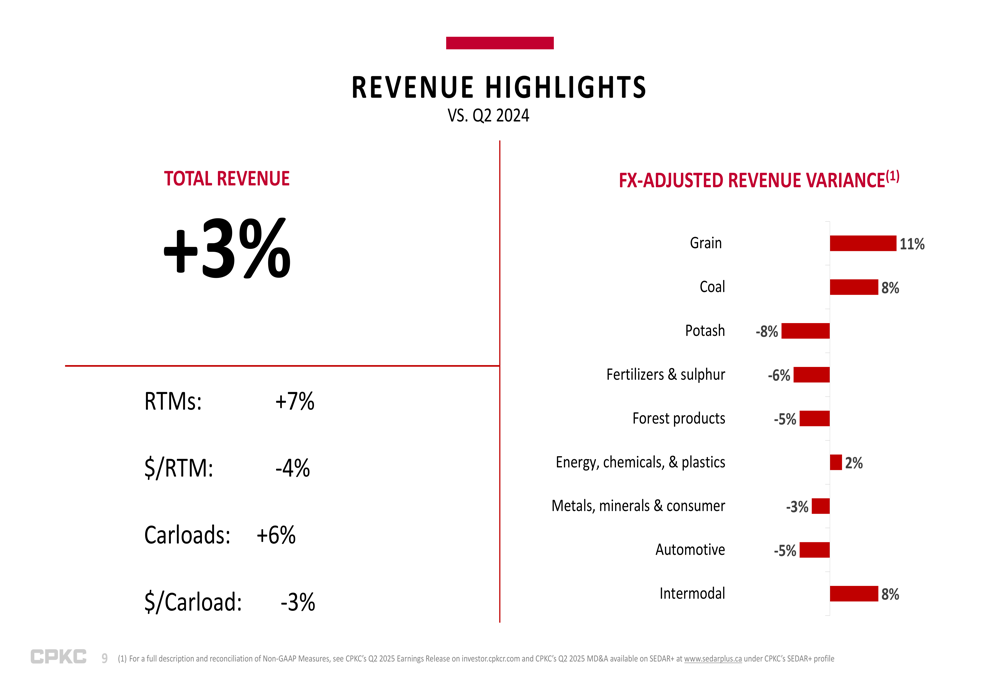

The company’s volume growth was particularly impressive, with Revenue Ton Miles (RTMs) increasing 7% year-over-year to 55,529 million. This volume growth was partially offset by a 4% decline in revenue per RTM, reflecting some pricing pressure across certain segments.

Segment Analysis

CPKC’s revenue performance varied significantly across commodity groups. The strongest performers were Grain (+11%), Coal (+8%), and Intermodal (+8%), which helped offset weakness in Potash (-8%), Fertilizers & Sulphur (-6%), Forest Products (-5%), and Automotive (-5%).

The following chart illustrates the revenue variance by commodity:

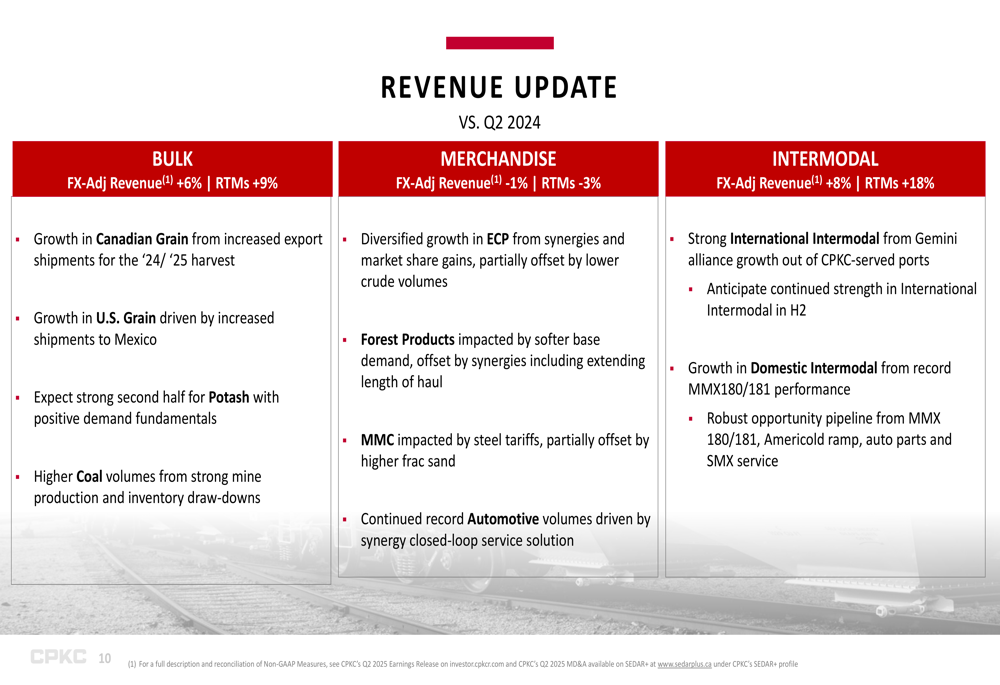

In the Bulk segment, which saw FX-adjusted revenue growth of 6% and RTM growth of 9%, Canadian Grain benefited from increased export shipments for the 2024/2025 harvest, while U.S. Grain was driven by increased shipments to Mexico. Coal volumes increased due to strong mine production and inventory draw-downs.

The Merchandise segment experienced a slight decline with FX-adjusted revenue down 1% and RTMs down 3%. However, this segment showed mixed results with Energy, Chemicals & Plastics (ECP) seeing growth from synergies and market share gains, partially offset by lower crude volumes. Automotive continued to show record volumes despite revenue challenges, driven by synergy closed-loop service solutions.

The Intermodal segment was a standout performer with FX-adjusted revenue up 8% and RTMs surging 18%. This growth was driven by strong International Intermodal performance from the Gemini alliance at CPKC-served ports and robust Domestic Intermodal growth from the MMX180/181 service.

The detailed segment breakdown is illustrated in the following slide:

Operational Challenges and Improvements

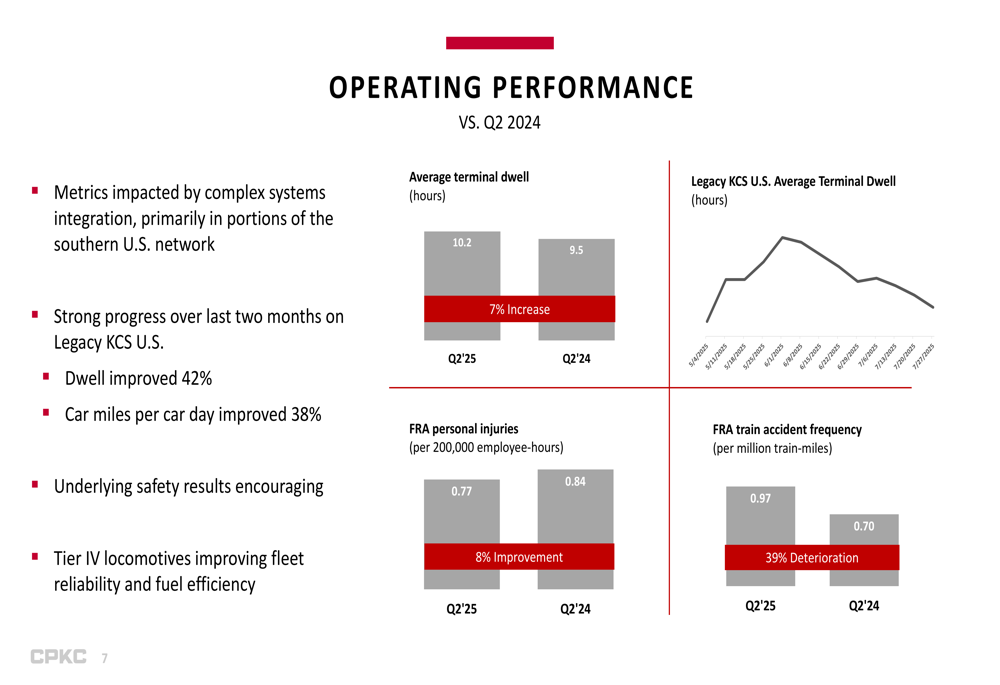

CPKC acknowledged operational challenges related to complex systems integration, primarily in portions of the southern U.S. network. Despite these challenges, the company reported strong progress over the last two months on the Legacy KCS U.S. operations, with dwell time improving 42% and car miles per car day improving 38%.

Safety metrics showed mixed results, with FRA Personal Injuries improving 8% to 0.77 per 200,000 employee-hours, while FRA Train Accident Frequency deteriorated 39% to 0.97 per million train-miles.

The following operational performance metrics provide additional context:

Chief Operating Officer Mark Redd highlighted that the underlying safety results were encouraging and noted that Tier IV locomotives were improving fleet reliability and fuel efficiency.

Financial Position and Cash Flow

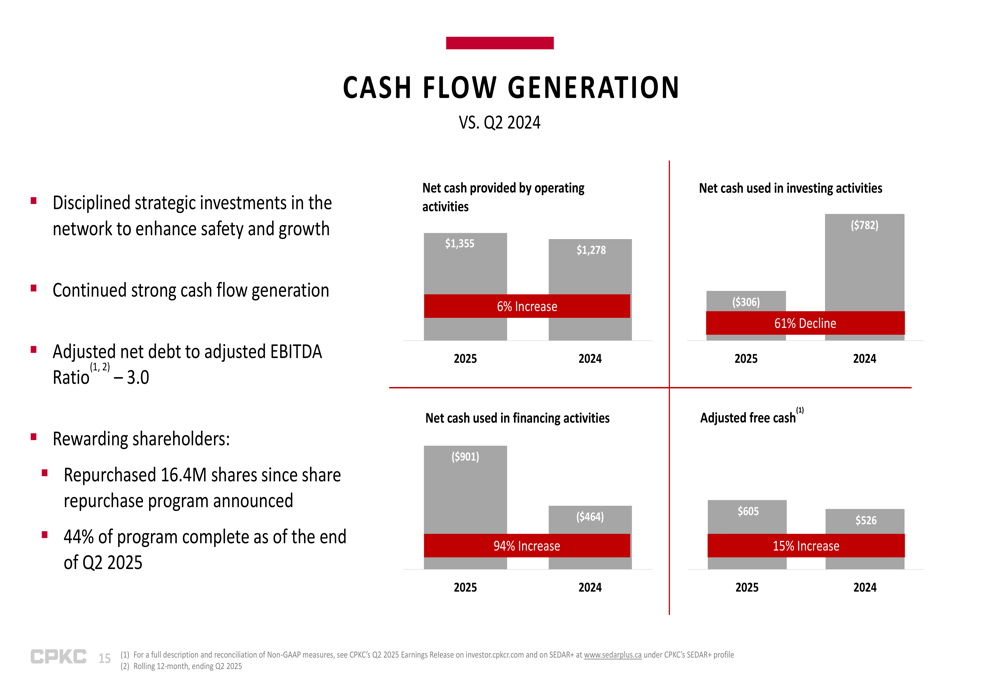

CPKC demonstrated strong financial discipline and cash generation during the quarter. Net cash provided by operating activities increased 6% to $1,355 million, while adjusted free cash flow grew 15% to $605 million. The company maintained an adjusted net debt to adjusted EBITDA ratio of 3.0.

The cash flow generation is illustrated in the following chart:

CFO Nadeem Velani emphasized the company’s disciplined approach to strategic investments in the network to enhance safety and growth. CPKC continued to reward shareholders through its share repurchase program, having repurchased 16.4 million shares since the program was announced, with 44% of the program complete as of the end of Q2 2025.

The detailed financial performance metrics show consistent improvement across key indicators:

Operating expenses increased only 1% to $2,356 million despite the 7% increase in volumes, demonstrating the company’s ability to control costs while handling higher traffic. Fuel expenses decreased 13% to $405 million, helping to offset increases in other expense categories such as materials (+28%) and equipment rents (+26%).

Forward-Looking Statements

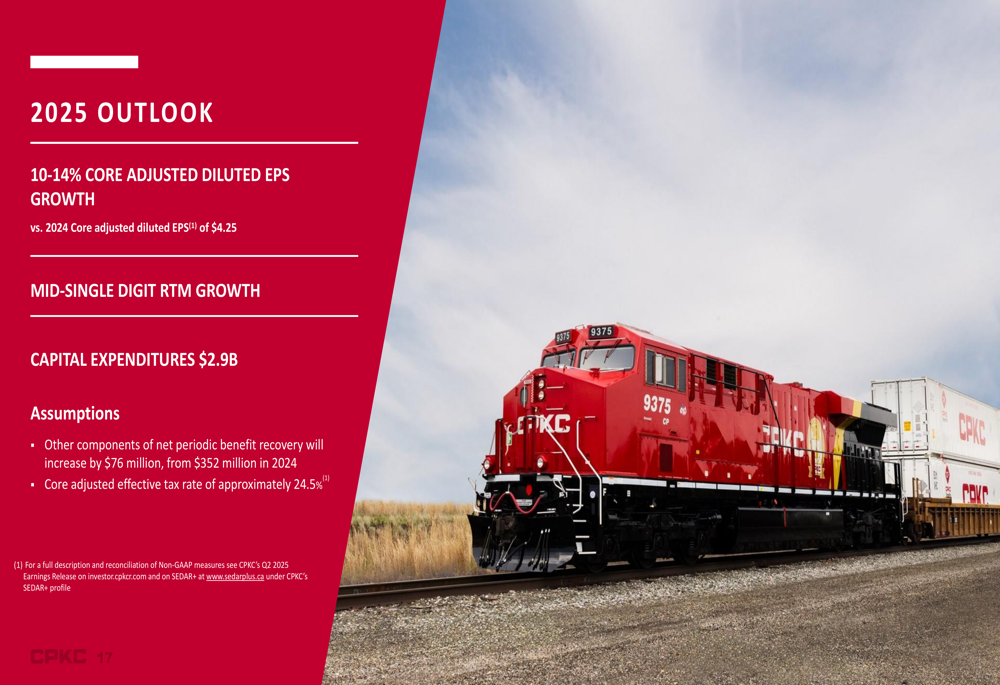

CPKC maintained its 2025 outlook, projecting 10-14% core adjusted diluted EPS growth compared to the 2024 core adjusted diluted EPS of $4.25. The company expects mid-single-digit RTM growth for the year, with capital expenditures of $2.9 billion.

The detailed 2025 outlook is presented in the following slide:

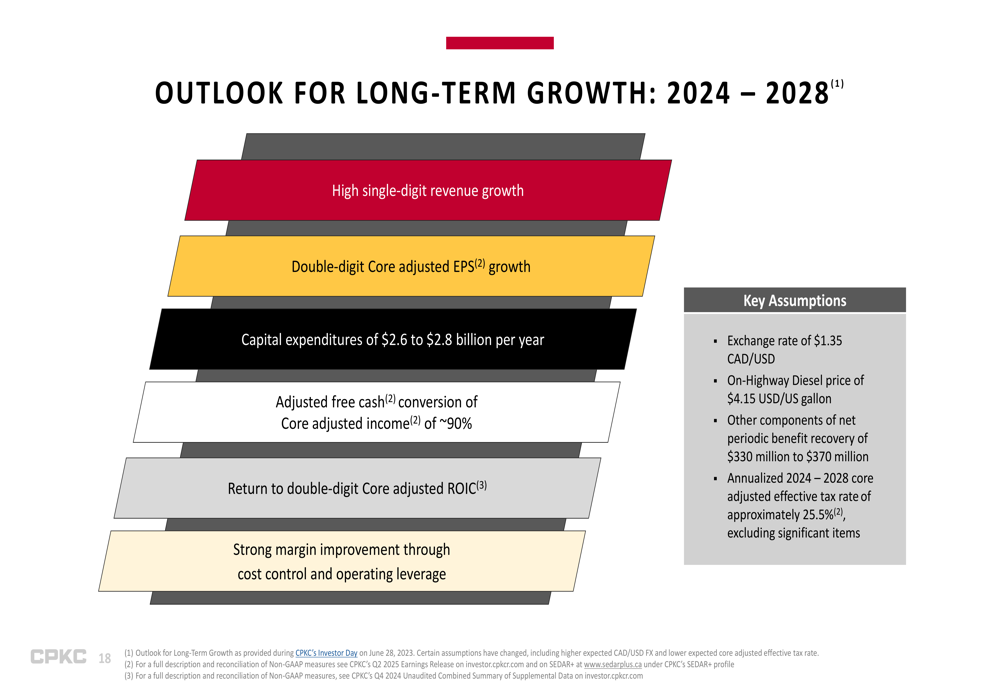

Looking further ahead, CPKC outlined its long-term growth expectations for 2024-2028, including high single-digit revenue growth, double-digit core adjusted EPS growth, and a return to double-digit core adjusted return on invested capital (ROIC). The company expects capital expenditures of $2.6 to $2.8 billion per year and adjusted free cash conversion of core adjusted income of approximately 90%.

CEO Keith Creel expressed confidence in the company’s position, stating that solid base demand and synergies were driving differentiated volume performance, while the company’s entrepreneurial approach was creating new opportunities. He emphasized that CPKC is well-positioned to meet guidance and continue delivering differentiated growth.

The company also highlighted its sustainability leadership, continuing to make progress on its hydrogen locomotive program and investing in communities across its network.

With its integrated North American network, strong operational improvements, and clear growth strategy, CPKC appears well-positioned to navigate the current transportation landscape while delivering on its financial targets for 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.