SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Crane NXT Co (NYSE:CXT) presented its first quarter 2025 financial results on May 8, 2025, highlighting a 5.3% year-over-year sales increase to $330 million, with adjusted earnings per share of $0.54 in line with expectations. The company is executing a strategic shift toward authentication and security technologies while navigating mixed segment performance and global tariff challenges.

The presentation comes as Crane NXT continues its transformation into a more diversified security and payment solutions provider, recently completing the acquisition of De La Rue (LON:DLAR) Authentication Solutions and maintaining its full-year adjusted EPS guidance of $4.00 to $4.30 despite headwinds.

Quarterly Performance Highlights

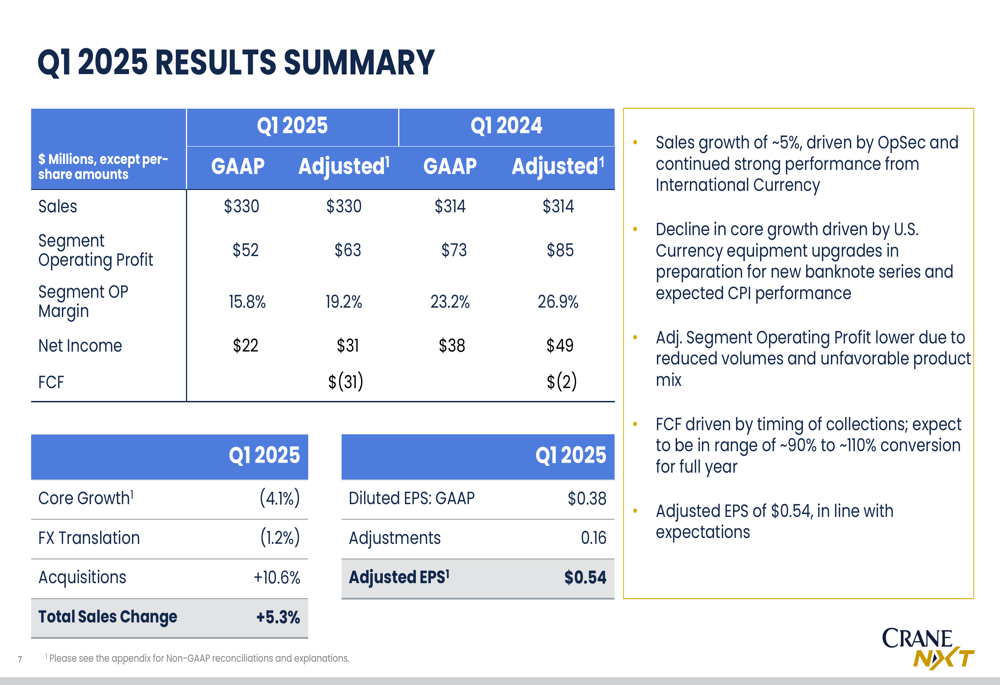

Crane NXT reported Q1 2025 sales of $330 million, representing a 5.3% increase from $314 million in Q1 2024. However, core sales declined by 4.1%, with growth primarily driven by acquisitions contributing 10.6%, partially offset by a 1.2% negative impact from foreign exchange translation.

As shown in the following summary of Q1 2025 results:

Net income for the quarter decreased to $22 million (GAAP) or $31 million (adjusted) from $38 million (GAAP) or $49 million (adjusted) in the prior year period. Diluted EPS was $0.38 on a GAAP basis and $0.54 on an adjusted basis, compared to $0.66 and $0.85 respectively in Q1 2024.

Segment operating profit margins declined significantly to 15.8% (GAAP) or 19.2% (adjusted) from 23.2% (GAAP) or 26.9% (adjusted) in the prior year period, reflecting lower U.S. Currency volumes and dilution from recent acquisitions.

Segment Performance Analysis

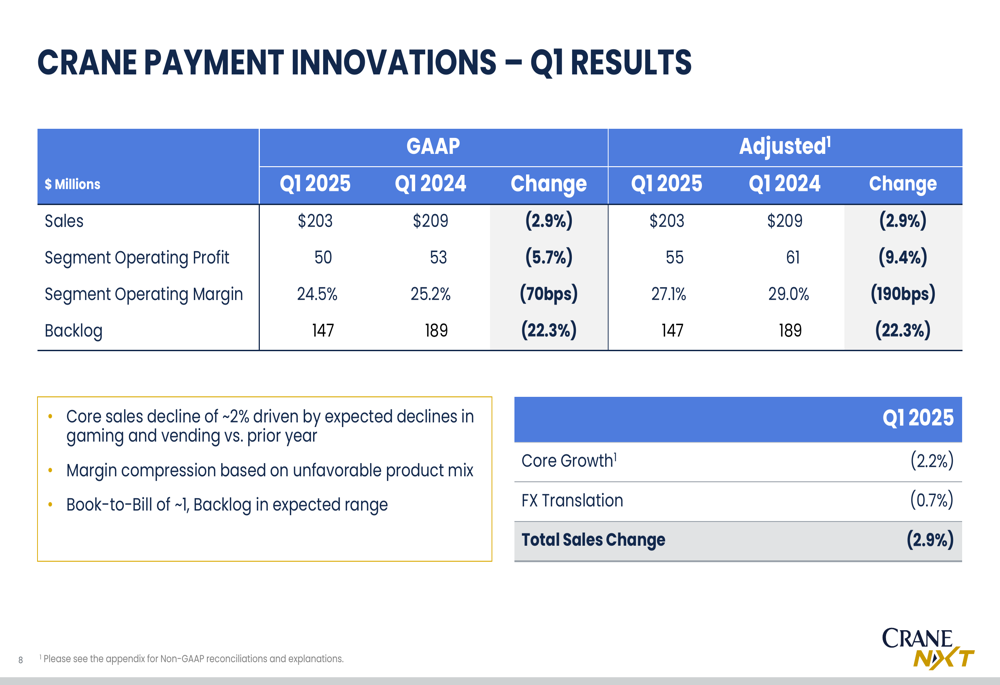

Crane NXT’s performance varied significantly between its two main segments. The Crane Payment Innovations (CPI) segment experienced a 2.9% sales decline to $203 million, with core sales down 2.2% and foreign exchange having a 0.7% negative impact. The segment’s operating profit decreased by 5.7% to $50 million, with margins contracting by 70 basis points to 24.5%.

As illustrated in the CPI segment results:

Management attributed the CPI segment’s decline to expected softness in gaming and vending markets compared to the prior year, with margin compression resulting from unfavorable product mix. The segment’s backlog decreased by 22.3% to $147 million, though the company noted a book-to-bill ratio of approximately 1.0.

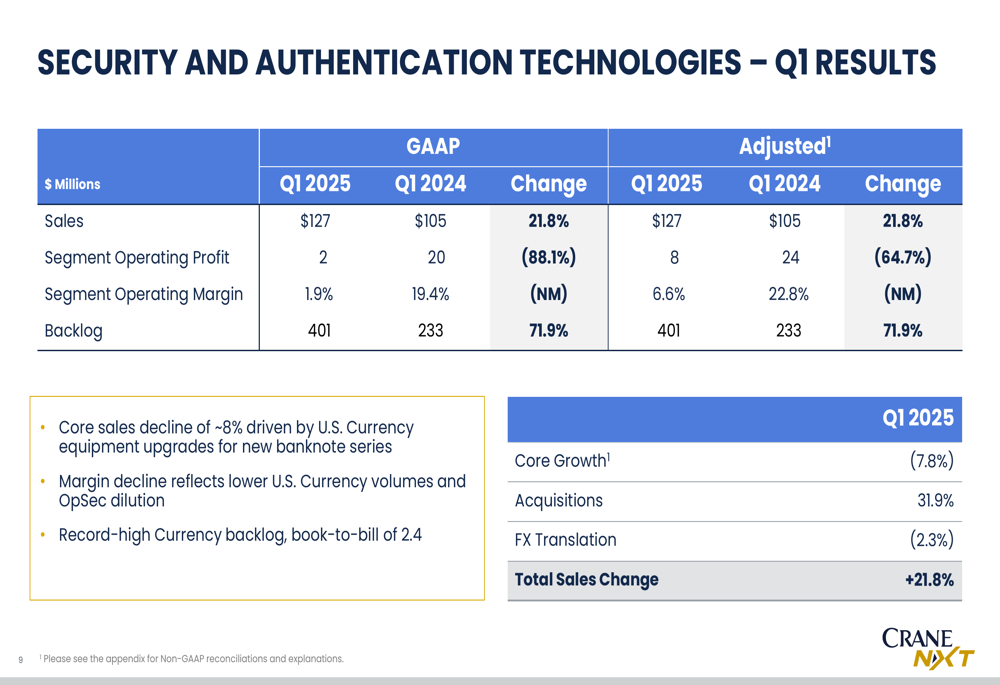

In contrast, the Security and Authentication Technologies (SAT) segment saw sales increase by 21.8% to $127 million, driven primarily by acquisitions (+31.9%), while core sales declined by 7.8% and foreign exchange had a 2.3% negative impact.

The SAT segment results reveal both growth and challenges:

Despite the sales increase, the SAT segment’s operating profit plummeted by 88.1% to just $2 million, with margins collapsing from 19.4% to 1.9%. The company attributed this decline to lower U.S. Currency volumes as it completed equipment upgrades for new banknote series, along with dilution from the OpSec acquisition. However, the segment’s backlog surged by 71.9% to $401 million, with a book-to-bill ratio of 2.4, indicating strong future demand.

Strategic Acquisitions and Diversification

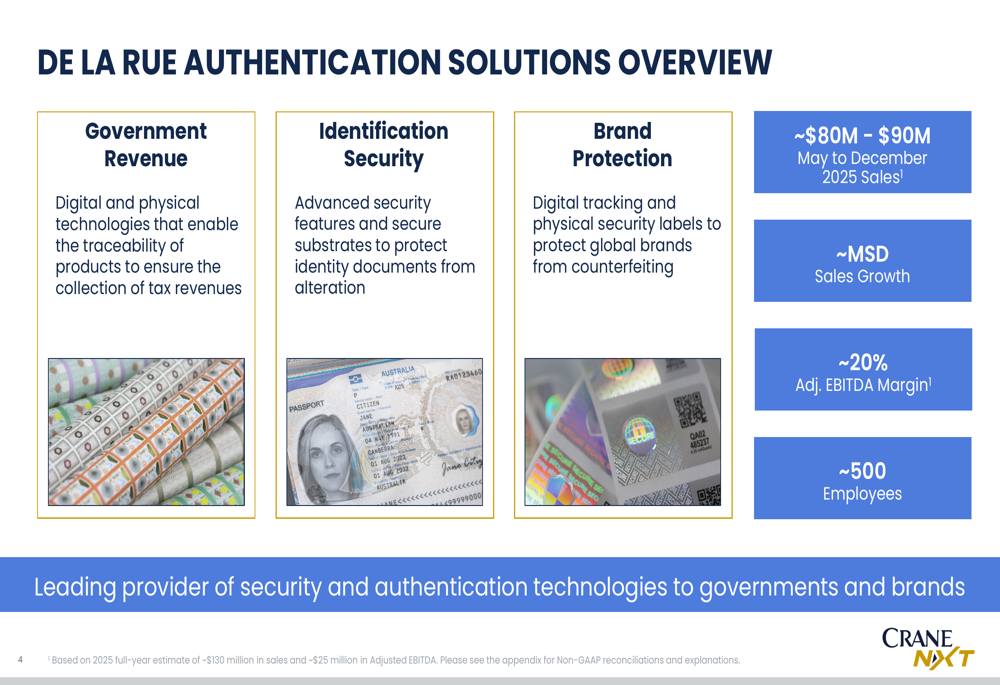

A central theme of Crane NXT’s presentation was its strategic diversification through acquisitions, particularly in the authentication and security space. The company recently completed the acquisition of De La Rue Authentication Solutions, which provides security technologies for government revenue, identification security, and brand protection.

The following overview highlights De La Rue Authentication Solutions’ capabilities and financial profile:

De La Rue Authentication Solutions is expected to contribute approximately $80-90 million in sales from May to December 2025, with mid-single-digit sales growth and approximately 20% adjusted EBITDA margins. The business employs around 500 people and serves as a leading provider of security and authentication technologies to governments and brands.

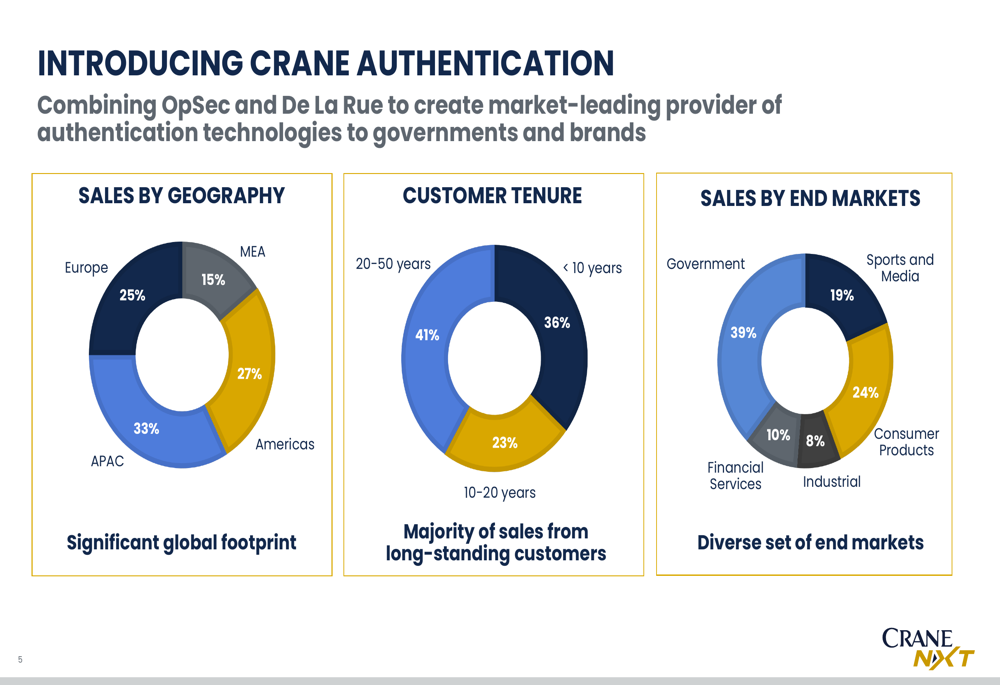

Crane NXT is combining De La Rue Authentication with its previously acquired OpSec business to form "Crane Authentication," creating a market-leading provider with a diverse global footprint:

The newly formed Crane Authentication division boasts a geographically diverse revenue stream, with 33% from Asia-Pacific, 27% from the Americas, 25% from Europe, and 15% from the Middle East and Africa. The business serves multiple end markets, including government (39%), consumer products (24%), sports and media (19%), financial services (10%), and industrial (8%). Notably, 41% of customers have relationships spanning 20-50 years, demonstrating strong customer retention.

This strategic evolution is transforming Crane NXT’s business mix, as illustrated in the following slide:

Tariff Challenges and Mitigation

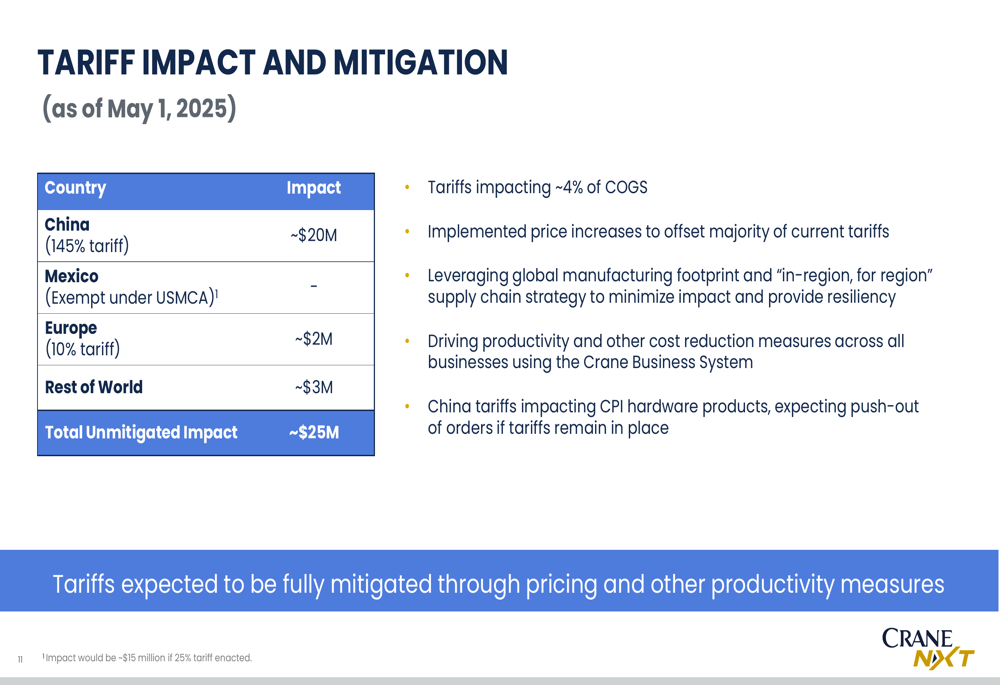

Crane NXT addressed the impact of recent tariff implementations, particularly the 145% tariff on Chinese imports, which represents a significant challenge for the company. The total unmitigated impact of global tariffs is estimated at approximately $25 million.

The following slide details the tariff impact and mitigation strategies:

Management outlined several mitigation strategies, including price increases to offset the majority of current tariffs, leveraging the company’s global manufacturing footprint with an "in-region, for region" supply chain strategy, and implementing productivity and cost reduction measures across all businesses using the Crane Business System. The company expressed confidence that tariffs would be fully mitigated through pricing and other productivity measures.

Forward Guidance and Outlook

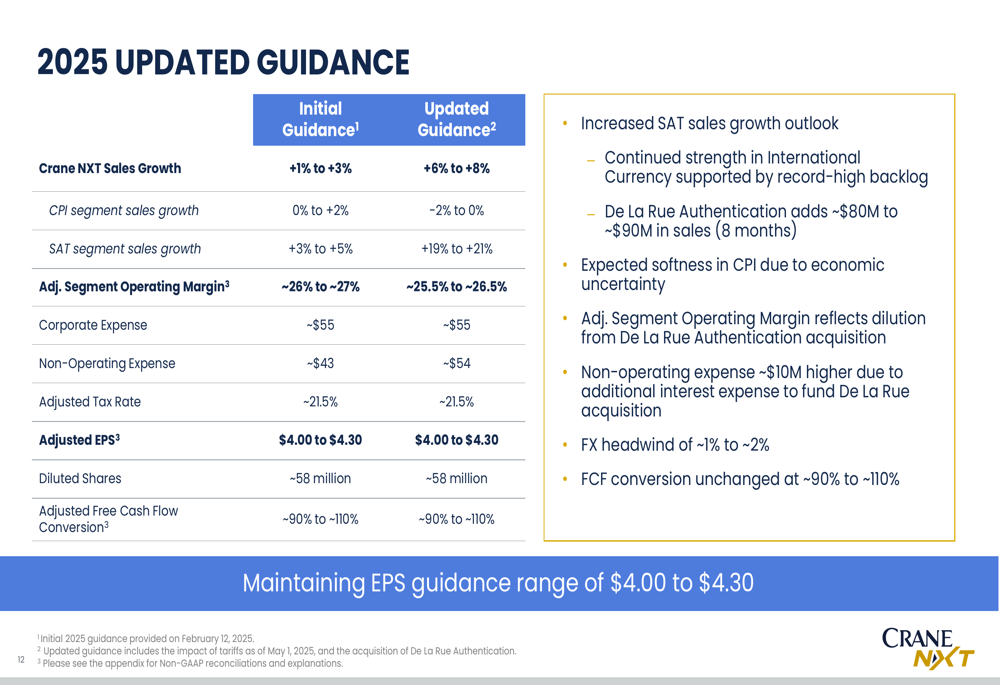

Despite the challenges, Crane NXT reaffirmed its full-year adjusted EPS guidance of $4.00 to $4.30 while raising its sales growth outlook from 1-3% to 6-8%, primarily due to the De La Rue acquisition.

The updated guidance reflects the following changes:

The company revised its segment sales growth expectations, with CPI now projected at -2% to 0% (down from 0% to +2%) and SAT increased to +19% to +21% (up from +3% to +5%). Adjusted segment operating margin guidance was lowered slightly to 25.5-26.5% from 26-27%, reflecting dilution from the De La Rue Authentication acquisition.

Management highlighted several positive factors supporting their outlook, including a record-high International Currency backlog, completed U.S. Currency upgrades in preparation for new banknotes, and continued growth in CPI Services winning new business beyond legacy equipment.

The company’s capital structure will shift following the De La Rue acquisition, with net leverage expected to increase from approximately 1.7x as of March 31, 2025, to approximately 2.3x by June 30, 2025. However, management emphasized that the company maintains strong liquidity and ample capacity for further M&A activity.

In concluding remarks, Crane NXT positioned itself as agile and resilient through economic uncertainty, with momentum building in key strategic growth areas and a disciplined capital allocation approach to expand its market-leading positions, all aimed at driving long-term shareholder value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.