Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

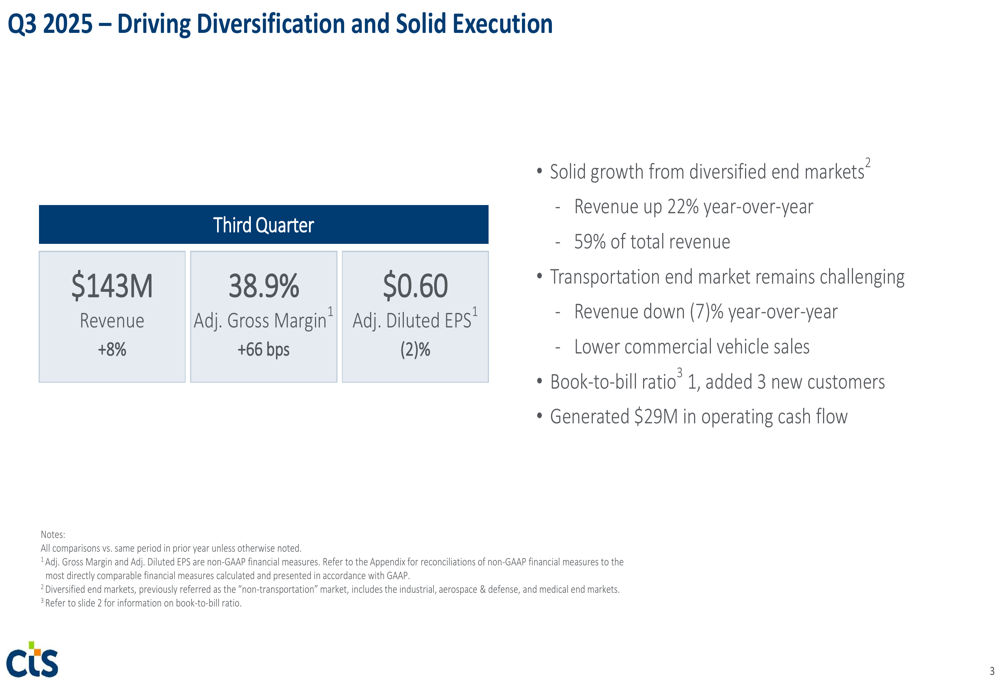

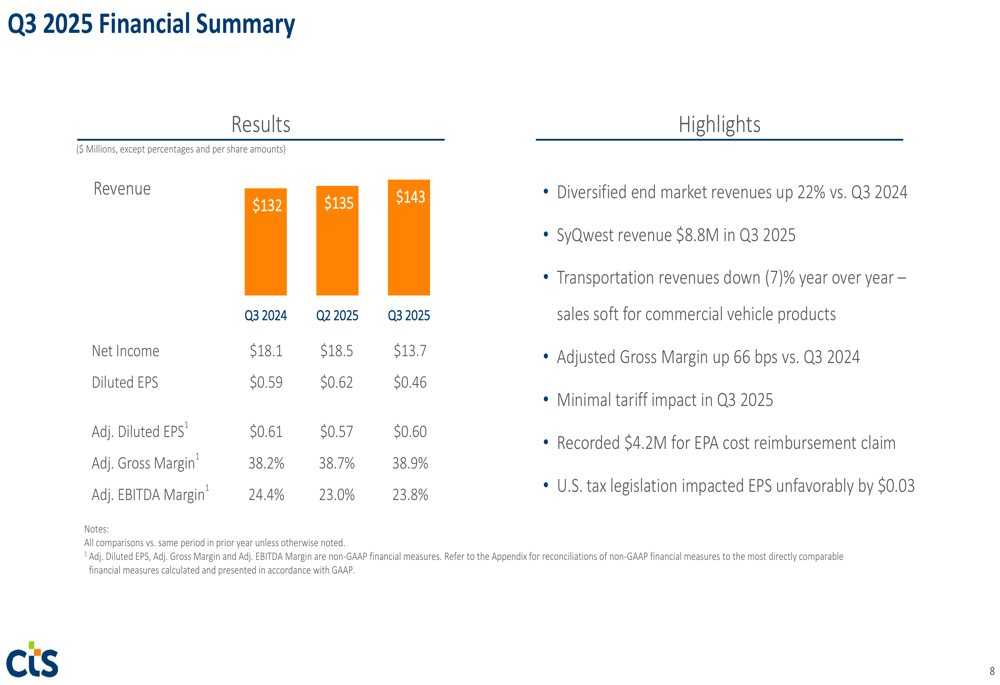

CTS Corporation (NYSE:CTS) presented its third-quarter 2025 results on October 28, highlighting continued progress in its strategic shift toward diversified end markets. The company reported 8% year-over-year revenue growth to $143 million, slightly exceeding analyst expectations of $136.4 million. However, adjusted diluted earnings per share of $0.60 fell short of the forecasted $0.61, contributing to an 8.27% drop in the company’s stock price following the announcement.

The presentation emphasized CTS’s success in growing its diversified end markets, which now represent 59% of total revenue, up from 52% in the prior year. This strategic pivot comes amid persistent challenges in the transportation segment, which continues to face headwinds, particularly in commercial vehicle products.

Quarterly Performance Highlights

CTS delivered solid financial results for Q3 2025, with several key metrics showing improvement. Revenue increased 8% year-over-year to $143 million, while adjusted gross margin expanded by 66 basis points to 38.9%. However, adjusted diluted EPS declined slightly by 2% to $0.60 compared to $0.61 in the same period last year.

As shown in the following performance overview:

The company generated $29 million in operating cash flow during the quarter and maintained a book-to-bill ratio of 1.0, suggesting stable order patterns. CTS also added three new customers during the period, further diversifying its client base.

A notable development affecting the quarterly results was a $4.2 million recorded for EPA cost reimbursement claims. Additionally, recent U.S. tax legislation had an unfavorable impact of $0.03 on earnings per share, as highlighted in the financial summary:

Segment Performance Analysis

The divergent performance across CTS’s end markets illustrates the company’s ongoing transformation. Diversified end markets, comprising medical, aerospace & defense, and industrial segments, grew revenue by 22% year-over-year and now account for 59% of total revenue.

The medical segment showed strong momentum with Q3 sales of $22 million, up 22% year-over-year, and bookings increasing by 8%. The company added two customers for diagnostic ultrasound applications and received orders for therapeutics, pacemakers, and ophthalmology applications.

Similarly, the aerospace & defense segment delivered impressive results with Q3 sales of $25 million, up 23% year-over-year, and bookings surging by 29%. A significant highlight was SyQwest’s sole source award of $5 million with follow-on potential.

The following chart illustrates the growth trajectory in these key diversified markets:

The industrial segment also performed well, with Q3 sales of $37 million representing a 21% year-over-year increase and bookings up 29%. The company secured multiple wins for industrial printing, EMC, and temperature sensing applications, while adding a new customer for position sensing.

In contrast, the transportation segment continued to face challenges, with Q3 sales declining by 7% year-over-year to $59 million, primarily due to soft sales for commercial vehicle products. Despite this weakness, CTS secured a new brake sensing application award and a large extension award for actuators with a North American customer for 2028-2030 revenue.

The following chart shows the contrasting performance between the growing industrial segment and the declining transportation segment:

Financial Position and Cash Flow

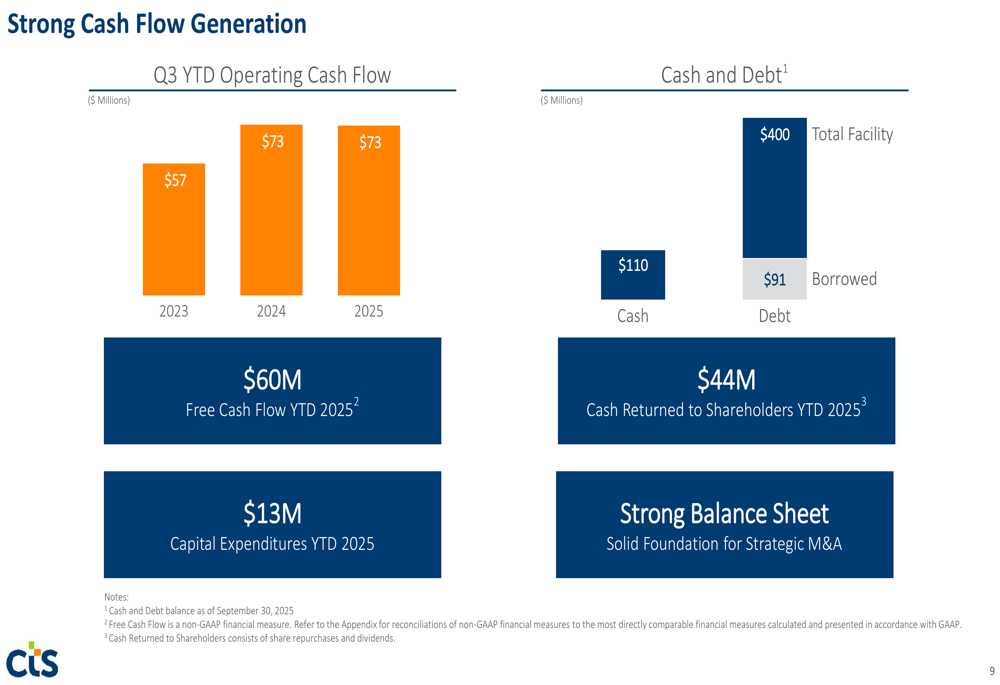

CTS maintained a strong financial position with $110 million in cash and $91 million in borrowed debt as of September 30, 2025. The company generated $73 million in operating cash flow year-to-date, consistent with the prior year, and $60 million in free cash flow after $13 million in capital expenditures.

Notably, CTS returned $44 million to shareholders year-to-date through share repurchases and dividends, demonstrating its commitment to shareholder returns while maintaining financial flexibility for strategic initiatives.

The following chart illustrates the company’s consistent cash flow generation and strong balance sheet position:

Forward Guidance and Outlook

Looking ahead, CTS maintained its full-year 2025 guidance with expected revenue of $545 million and adjusted diluted EPS of $2.25. This represents a modest improvement from 2024 levels and continues the recovery trend from the lows of 2023-2024.

The company’s key outlook assumptions include the continuation of current market conditions, ongoing monitoring of tariff impacts and the geopolitical environment, continued progress in diversified end markets growth, and an expected tax rate of 21-23% excluding discrete items.

The following chart presents CTS’s revenue and adjusted EPS trajectory since 2020, including the 2025 forecast:

CTS’s financial summary for the quarter provides additional context for its performance trajectory, showing sequential improvement in key metrics such as adjusted gross margin and adjusted EBITDA margin:

While the company faces ongoing challenges in its transportation segment, the continued strong performance in diversified end markets supports management’s strategic direction. The company’s ability to maintain margins and generate consistent cash flow while navigating market challenges demonstrates operational resilience. However, investors appear concerned about the slight earnings miss and potential headwinds, as reflected in the stock’s negative reaction following the earnings announcement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.