e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Curbline Properties Corp (NYSE:CURB) presented its third quarter 2025 earnings results on October 28, highlighting an accelerated acquisition strategy, strong leasing performance, and an improved outlook for funds from operations. The company reported earnings per share of $0.09 and operating funds from operations (OFFO) of $0.28 per share, while raising its full-year OFFO guidance.

Quarterly Performance Highlights

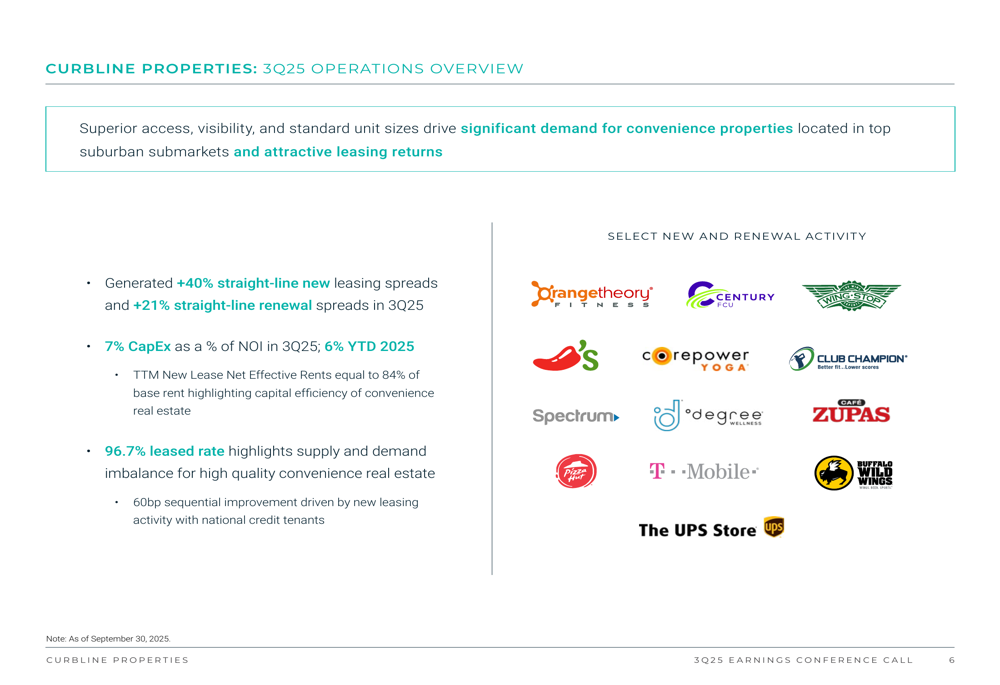

Curbline reported solid operational results for Q3 2025, with same-property net operating income (NOI) growth of 3.7% year-to-date. The company’s leased rate improved to 96.7%, up 60 basis points sequentially, demonstrating strong demand for its convenience-oriented retail properties.

"We continue to lead this unique capital-efficient sector with a clear first-mover advantage," CEO David Lukes stated during the earnings call, emphasizing the company’s strategic focus on convenience retail.

Leasing spreads were particularly impressive, with new lease spreads of +39.7% and renewal spreads of +21% on a straight-line basis, resulting in a blended lease spread of +27.4% for the quarter.

As shown in the following summary of key financial metrics:

The company’s operational performance was bolstered by new leasing activity with national credit tenants, including Orangetheory Fitness, CorePower Yoga, T-Mobile, Buffalo Wild Wings, and The UPS Store, among others.

Acquisition Strategy and Portfolio Growth

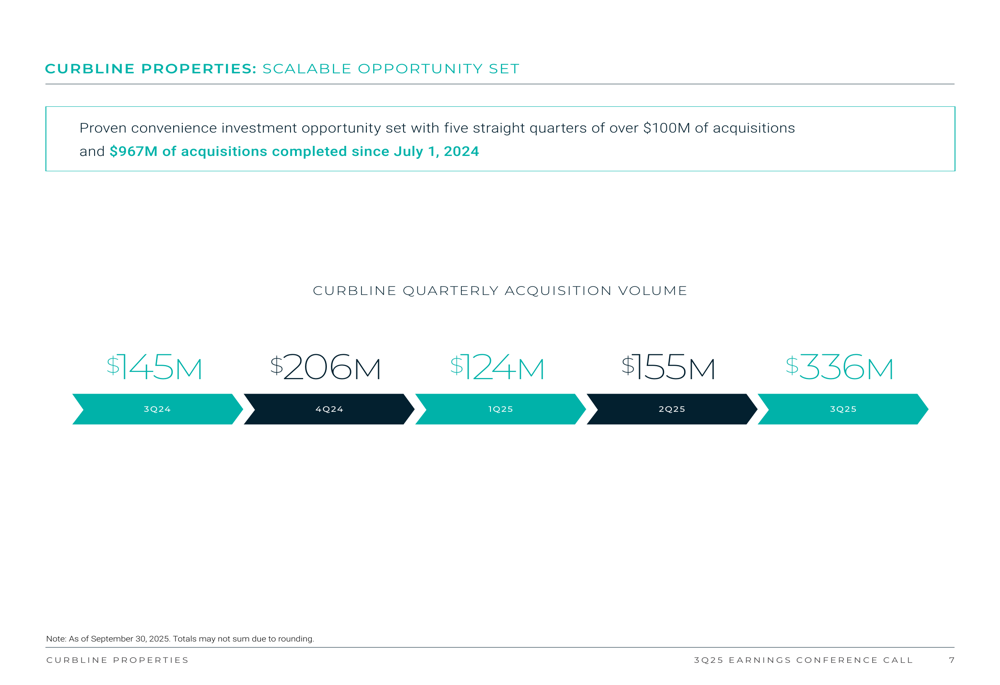

Curbline’s most notable achievement in Q3 was its accelerated acquisition pace. The company acquired 37 properties for $336 million during the quarter, bringing year-to-date acquisitions to 69 properties for $644 million. This marks the fifth consecutive quarter with over $100 million in acquisitions, with a total of $967 million in properties acquired since July 2024.

The following chart illustrates the company’s consistent and growing acquisition volume over the past five quarters:

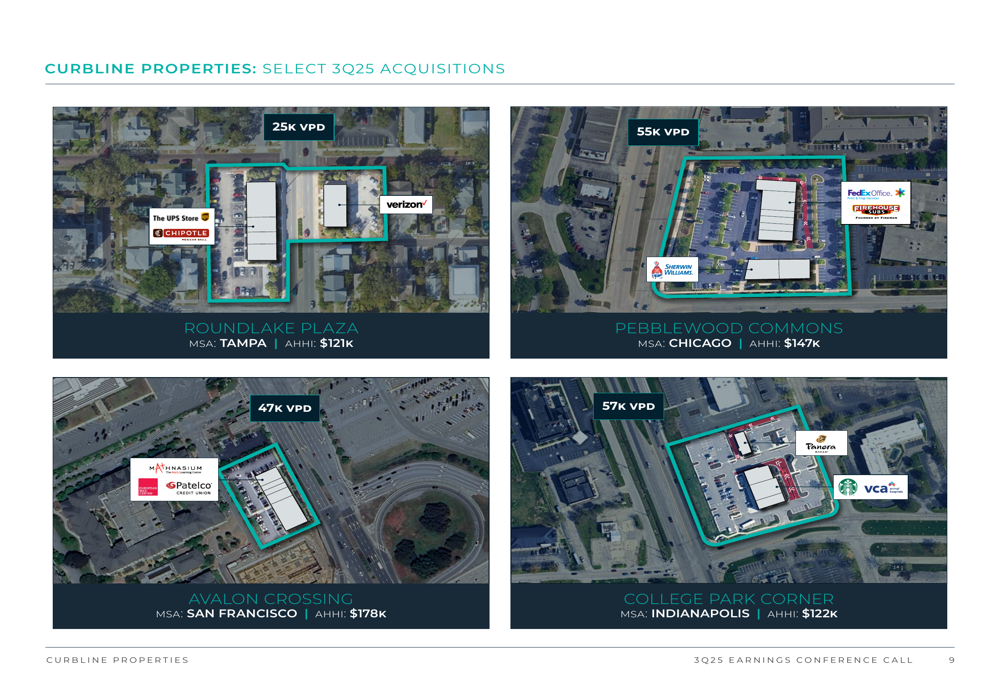

The company’s acquisition strategy focuses on convenience properties in wealthy submarkets, targeting locations with high average household incomes and strong traffic counts. Selected acquisitions from Q3 include properties in major metropolitan areas with average household incomes ranging from $121,000 to $178,000.

As illustrated in these examples of recent acquisitions:

During the earnings call, analysts inquired about Curbline’s acquisition cap rates, which management indicated range from low 5% to high 6%. The company emphasized that it focuses more on internal rate of return (IRR) than cap rates, highlighting a disciplined growth approach.

Balance Sheet and Financial Position

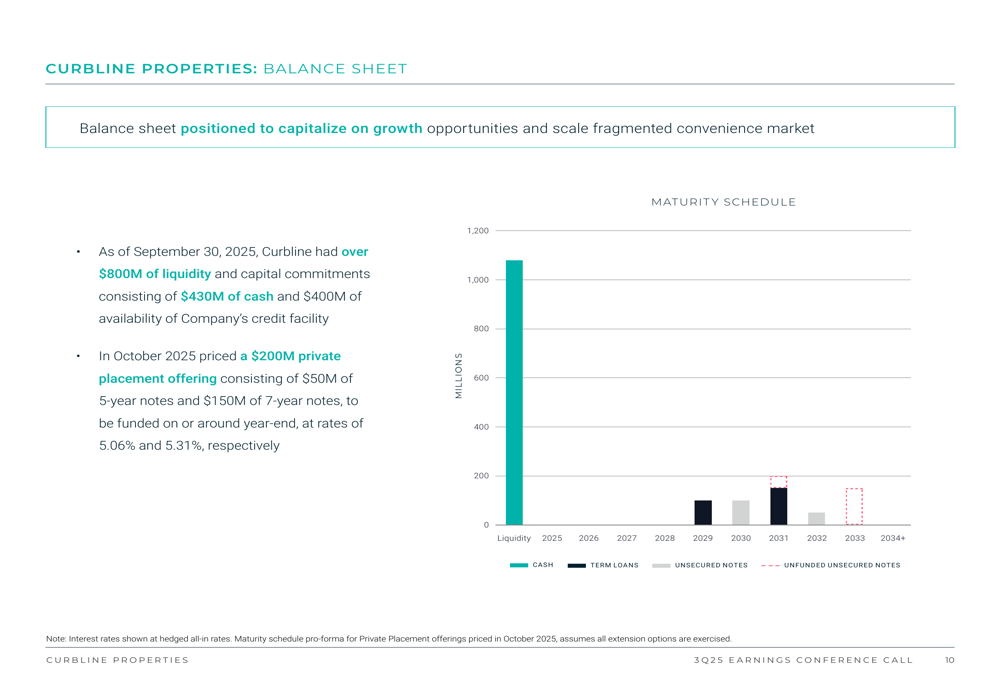

Curbline maintains a strong balance sheet with over $800 million in liquidity as of September 30, 2025, including $430 million in cash and $400 million available under its credit facility. This financial flexibility supports the company’s aggressive acquisition strategy while maintaining conservative leverage.

In October 2025, the company priced a $200 million private placement consisting of $50 million in 5-year notes and $150 million in 7-year notes, to be funded around year-end at rates of 5.06% and 5.31%, respectively.

The following chart shows Curbline’s debt maturity schedule and liquidity position:

This strong financial position has enabled Curbline to fund $300 million of debt in Q3 2025 while maintaining significant liquidity for future acquisitions. According to the earnings call, the company anticipates ending the year with over $250 million in cash on hand.

Forward Guidance and Outlook

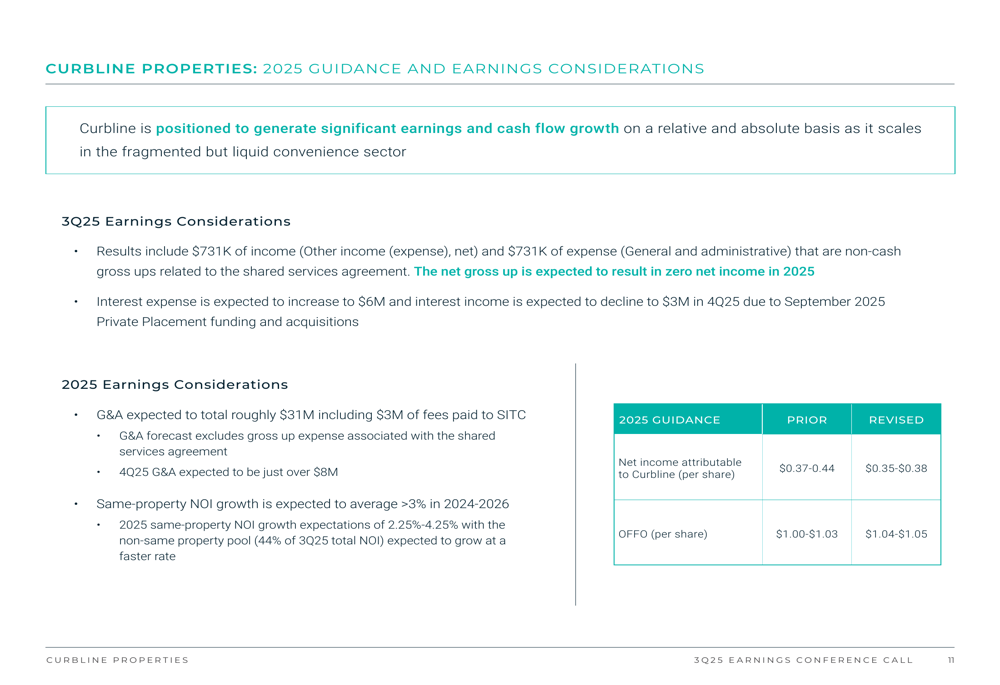

Curbline has revised its full-year 2025 guidance, slightly lowering its net income projection while raising its OFFO outlook. The company now expects net income attributable to Curbline of $0.35-$0.38 per share (down from $0.37-$0.44) and OFFO of $1.04-$1.05 per share (up from $1.00-$1.03).

The guidance revision reflects several factors, including increased interest expense expected to reach $6 million in Q4 (with interest income declining to $3 million) due to the September 2025 private placement funding and recent acquisitions. General and administrative expenses are projected to total approximately $31 million for the year, including $3 million in fees paid to SITC.

Looking ahead, Curbline expects same-property NOI growth to average more than 3% from 2024 to 2026, indicating confidence in the company’s operational strategy. Total investment activity for 2025 is projected at approximately $750 million, with a focus on maintaining occupancy around 97%.

The company’s stock closed at $24.75 on October 27, 2025, showing a modest increase of 0.98% in the aftermarket session following the earnings release. This places the stock near its 52-week high of $25.69, reflecting positive investor sentiment about the company’s growth trajectory and operational performance.

While Curbline’s presentation highlighted its strong positioning and growth potential, investors should consider potential risks including market saturation in the convenience retail sector, macroeconomic pressures that could affect consumer spending, and interest rate fluctuations that might impact financing costs and investment returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.