Piper Sandler lowers Arbor Realty Trust stock price target on credit issues

Introduction & Market Context

CVB Financial Corp. (NASDAQ:CVBF), the parent company of Citizens Business Bank and the largest financial institution headquartered in Southern California’s Inland Empire region, recently shared its Q2 2025 corporate presentation. The bank continues to demonstrate remarkable consistency in a challenging banking environment, extending its streak to 193 consecutive profitable quarters—spanning more than 48 years.

Trading at $19.11 as of October 14, 2025 (up 2.96% in the latest session), CVBF operates with $15.4 billion in total assets and maintains a strong presence across California with 62 business financial centers. The bank has consistently positioned itself as a premier financial services provider for small to medium-sized businesses throughout the state.

Quarterly Performance Highlights

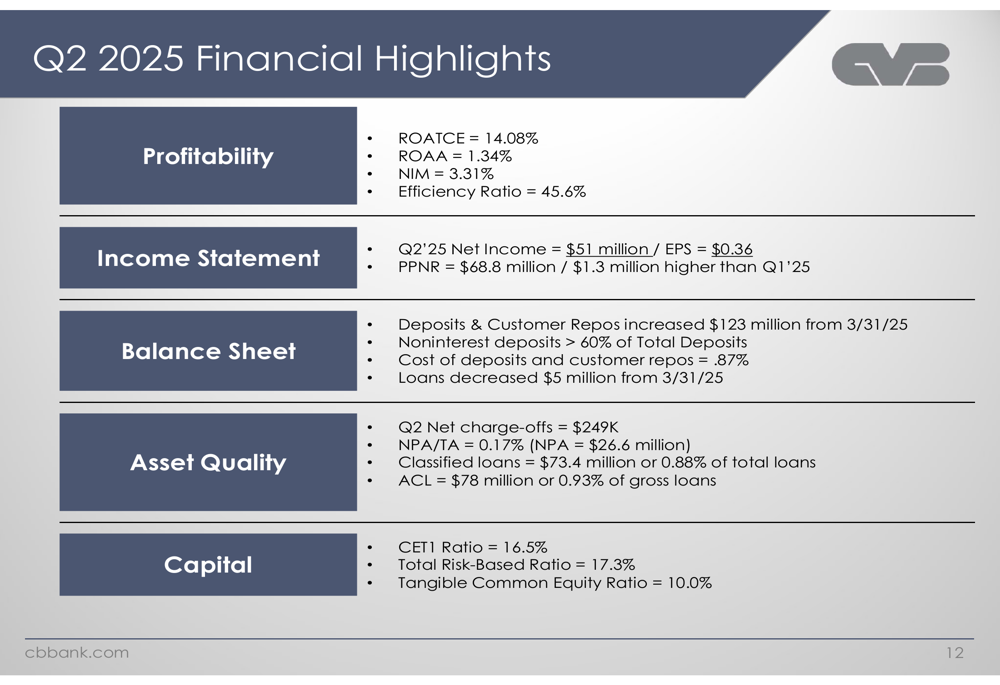

CVB Financial reported net income of $50.6 million for Q2 2025, translating to earnings per share of $0.36, consistent with the same quarter last year. The bank maintained strong profitability metrics with a return on average tangible common equity (ROATCE) of 14.08% and return on average assets (ROAA) of 1.34%.

As shown in the following financial highlights, the bank demonstrated solid performance across key metrics:

The bank’s efficiency ratio improved to 45.55% in Q2 2025 from 45.10% in the same quarter last year, reflecting effective cost management. Pre-provision net revenue (PPNR) reached $68.8 million, representing a modest increase of $1.3 million compared to Q1 2025.

Asset quality remains exceptionally strong, with net charge-offs of just $249,000 for the quarter and non-performing assets to total assets ratio (NPA/TA) at a mere 0.17%. The allowance for credit losses stands at $78 million, representing 0.93% of gross loans.

Detailed Financial Analysis

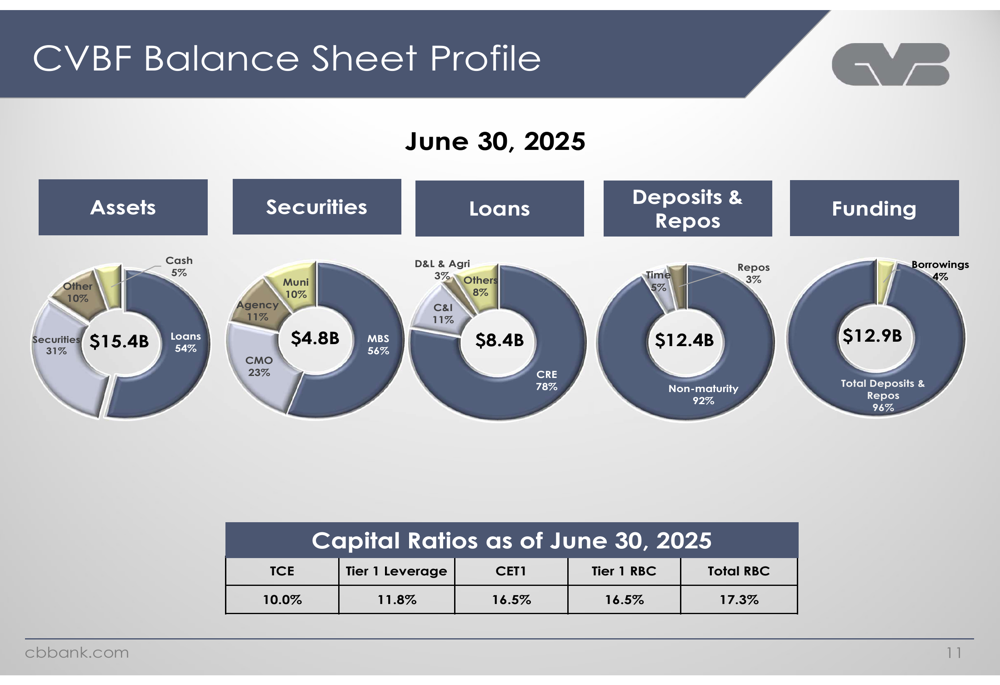

CVB Financial’s balance sheet reflects a conservative approach to banking, with a well-diversified asset mix. The following chart illustrates the bank’s balance sheet composition as of June 30, 2025:

Loans constitute 54% of total assets at $8.4 billion, with commercial real estate (CRE) representing 78% of the loan portfolio. Securities make up 31% of assets at $4.8 billion, providing liquidity and stable income. The bank maintains strong capital ratios, with a CET1 ratio of 16.5% and total risk-based capital ratio of 17.3%, well above regulatory requirements.

The bank’s funding profile remains stable, with deposits and repos accounting for 96% of total funding. Non-maturity deposits represent 92% of total deposits, providing a low-cost and stable funding base.

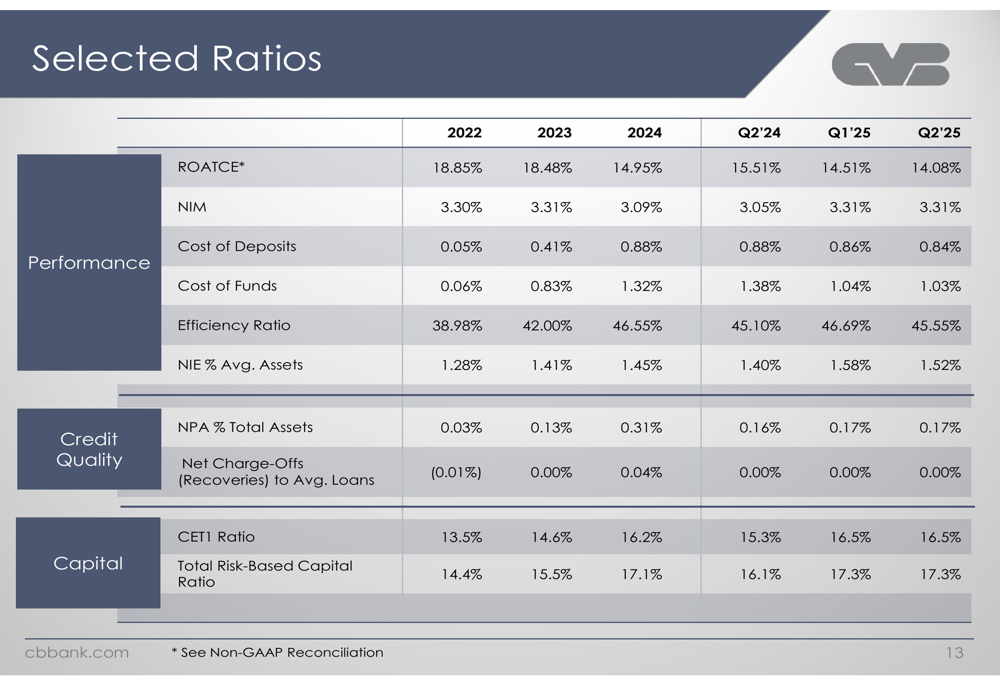

The following table presents key financial ratios over time, highlighting CVB Financial’s consistent performance:

Net interest margin (NIM) has remained stable at 3.31% in Q2 2025, unchanged from Q1 2025 but improved from 3.05% in Q2 2024. This stability is particularly noteworthy given the challenging interest rate environment facing the banking sector. The cost of deposits has declined to 0.84% in Q2 2025 from 0.88% a year earlier, contributing to margin stability.

Competitive Industry Position

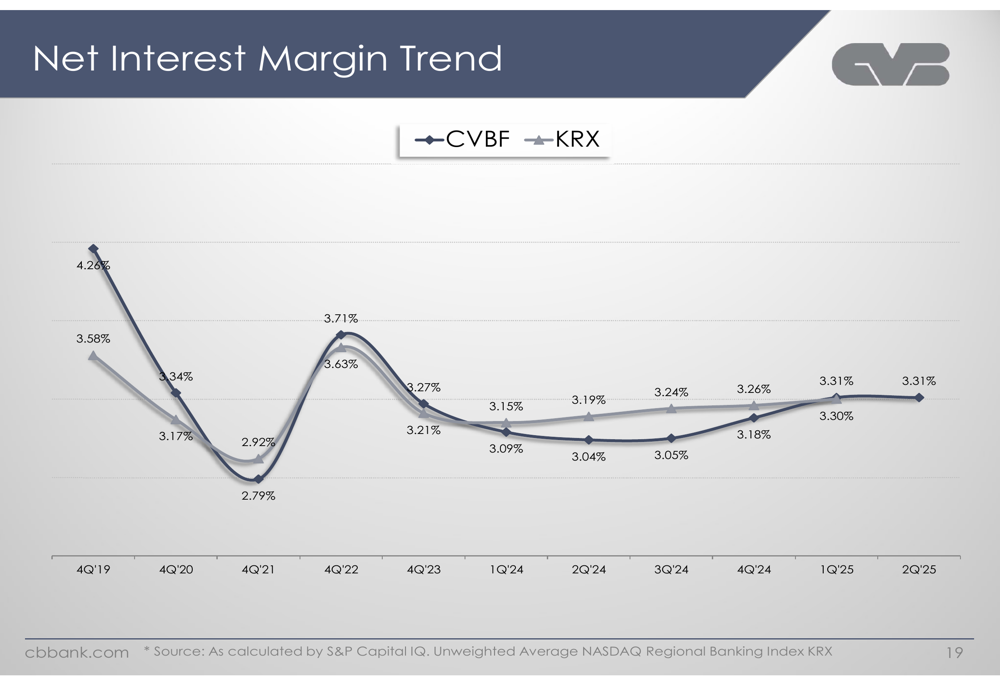

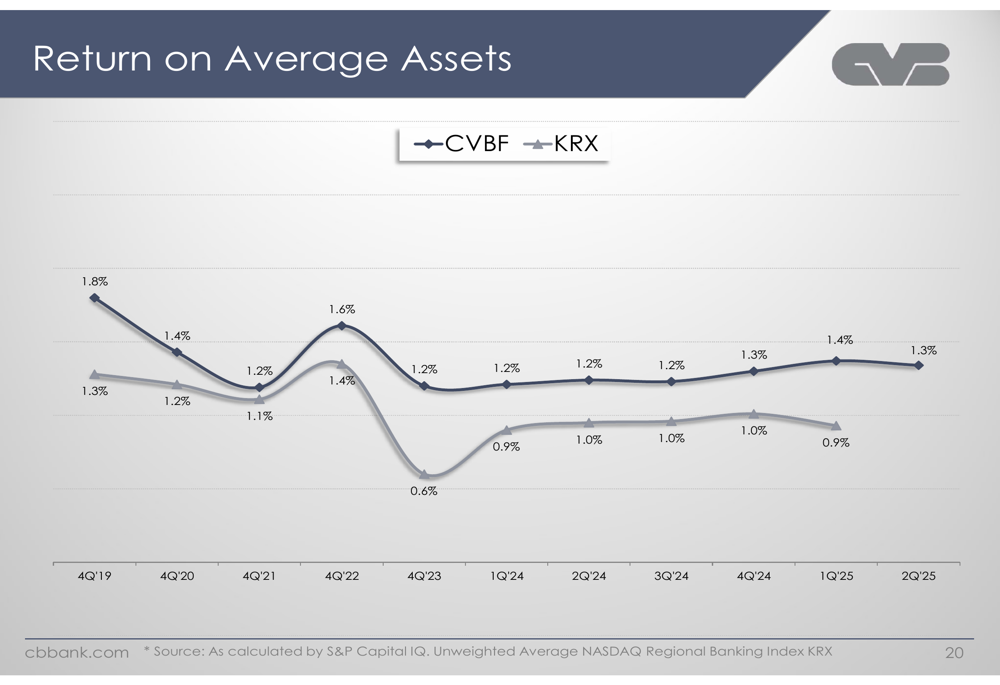

CVB Financial consistently outperforms its peers in the NASDAQ Regional Banking Index (KRX) on key performance metrics. The following chart illustrates the bank’s net interest margin compared to the KRX index:

Similarly, CVB Financial’s return on average assets has consistently exceeded the industry benchmark:

These comparisons demonstrate CVB Financial’s superior performance relative to regional banking peers, with ROAA at 1.3% in Q2 2025 compared to the KRX average of 0.9%. This outperformance highlights the effectiveness of the bank’s business model and strategic focus.

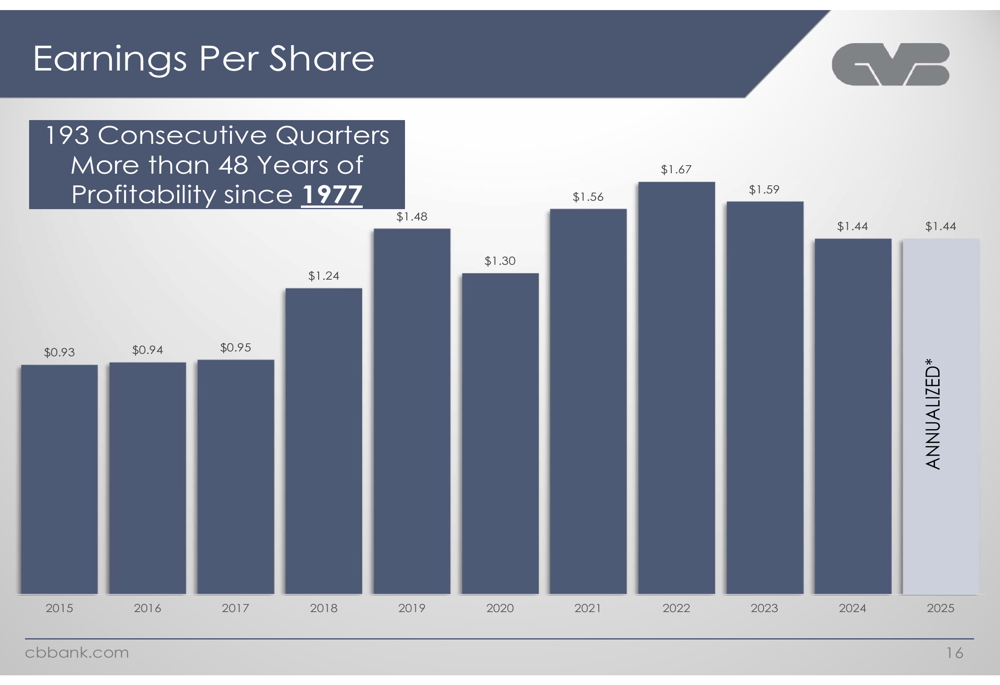

Long-Term Performance Trends

CVB Financial has demonstrated remarkable consistency in both earnings and shareholder returns over the past decade. The following chart shows the bank’s earnings per share trend from 2015 to 2025:

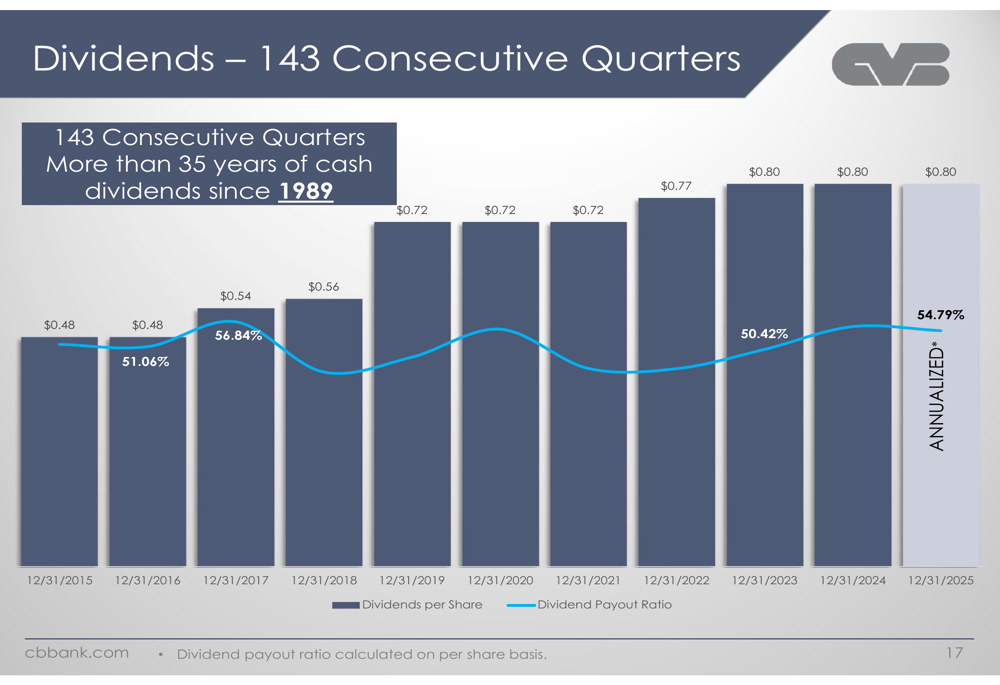

The bank has also maintained a strong commitment to shareholder returns through consistent dividend payments. As shown in the following chart, CVB Financial has increased its dividend from $0.48 per share in 2015 to $0.80 per share in 2025, while maintaining a prudent payout ratio:

The bank has now paid cash dividends for 143 consecutive quarters, spanning more than 35 years since 1989. This consistent return of capital to shareholders underscores the bank’s stable business model and long-term focus.

Strategic Initiatives

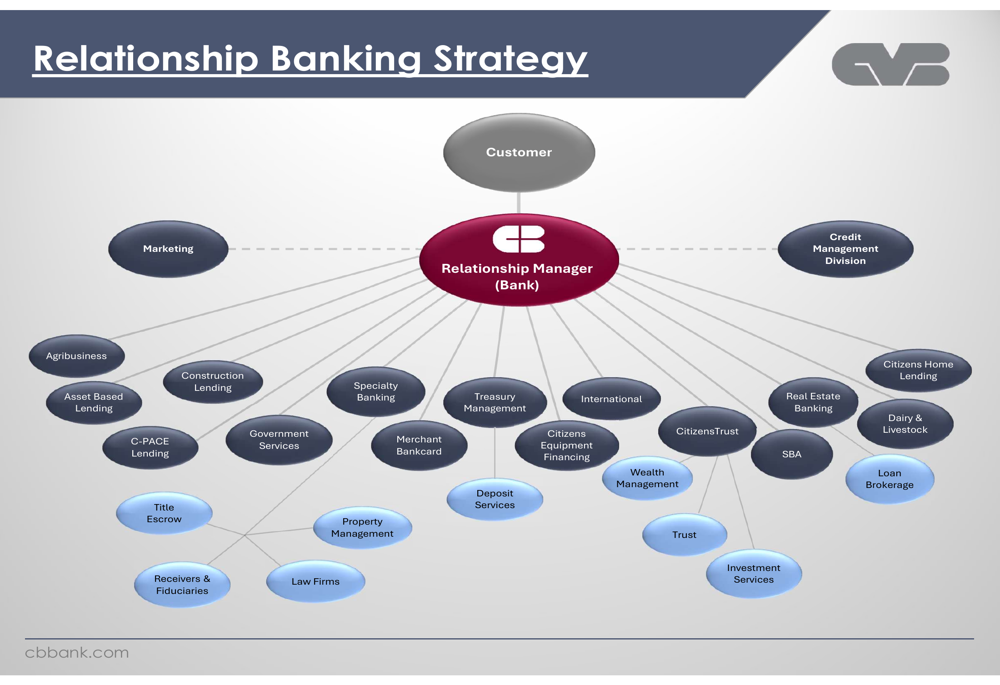

CVB Financial’s relationship banking strategy is central to its business model, placing the relationship manager at the hub of comprehensive client services. The following diagram illustrates this approach:

The bank pursues three primary growth strategies: opening new locations (DeNovo), increasing same-store sales, and strategic acquisitions. Recent DeNovo locations include San Diego (2014, 2017), Oxnard (2015), Santa Barbara (2015), Stockton (2018), and Modesto (2020). The bank’s acquisition strategy targets financial institutions with $1-10 billion in assets in both existing and new markets.

CVB Financial maintains a clear focus on its target customer profile: privately-held and family-owned businesses with annual revenues between $1-300 million that rank in the top 25% of their respective industries. This targeted approach has enabled the bank to build long-term relationships with high-quality clients.

Forward-Looking Statements

During the recent earnings call, CEO David A. Brager emphasized the bank’s consistent performance across various economic environments, stating, "Citizens Business Bank continues to perform consistently in all operating environments." Management also highlighted competitive loan pricing, noting that loans are "priced at 130 to 170 over treasuries."

Looking ahead, CVB Financial anticipates potential M&A activity by year-end and is considering expansion beyond its California base. The bank expects loan originations to outpace payoffs in coming quarters and foresees normalized loan utilization, which could drive future revenue growth.

Analysts project earnings per share of $1.48 for full-year 2025, with an increase to $1.55 expected in FY2026. Revenue is forecasted to grow from $516.32 million in FY2025 to $541 million in FY2026.

However, the bank faces several challenges, including an economic slowdown with GDP expected to remain below 1% until H2 2026, rising unemployment projected to reach 5% by early 2026, and declining commercial real estate prices that could impact loan portfolios. Competition from larger regional banks may also pressure loan spreads going forward.

Despite these headwinds, CVB Financial’s consistent performance, strong capital position, and relationship-based banking model position it well to navigate the challenging economic environment while continuing its remarkable streak of profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.