Oil prices extend losses as traders downplay Russia sanction risks

Introduction & Market Context

Dana Incorporated (NYSE:DAN) presented its second-quarter 2025 earnings results on August 5, highlighting a significant strategic transformation through the planned divestiture of its off-highway business while demonstrating improved profitability despite revenue headwinds. The company’s stock surged 8.39% to close at $16.66, approaching its 52-week high of $18.05, as investors responded positively to the company’s strategic shift and improved guidance.

The presentation detailed Dana’s plans to sell its off-highway business for $2.7 billion while focusing on its light vehicle and commercial vehicle segments. Despite facing lower sales volumes and tariff challenges, Dana reported margin improvements driven by aggressive cost-saving initiatives, leading management to raise full-year guidance.

Strategic Transformation

The centerpiece of Dana’s strategic shift is the definitive agreement to sell its off-highway business, with a purchase price of $2.7 billion ($2.4 billion in net cash proceeds). The transaction is expected to close late in the fourth quarter of 2025, transforming Dana into a more focused enterprise.

As shown in the following slide detailing the "New Dana" structure:

The reconfigured company will generate approximately $7.7 billion in 2024 sales, with operations spanning 65 major manufacturing facilities across 26 countries on six continents. The business mix will shift to 70% light vehicle and 30% commercial vehicle segments, serving over 5,000 customers globally. Dana’s core technologies will center around drive systems, electrodynamic components, thermal management, and sealing solutions.

This strategic realignment positions Dana to better address evolving market demands while concentrating resources on its strongest business segments. The company plans to use proceeds from the divestiture to strengthen its balance sheet and return capital to shareholders.

Quarterly Performance Highlights

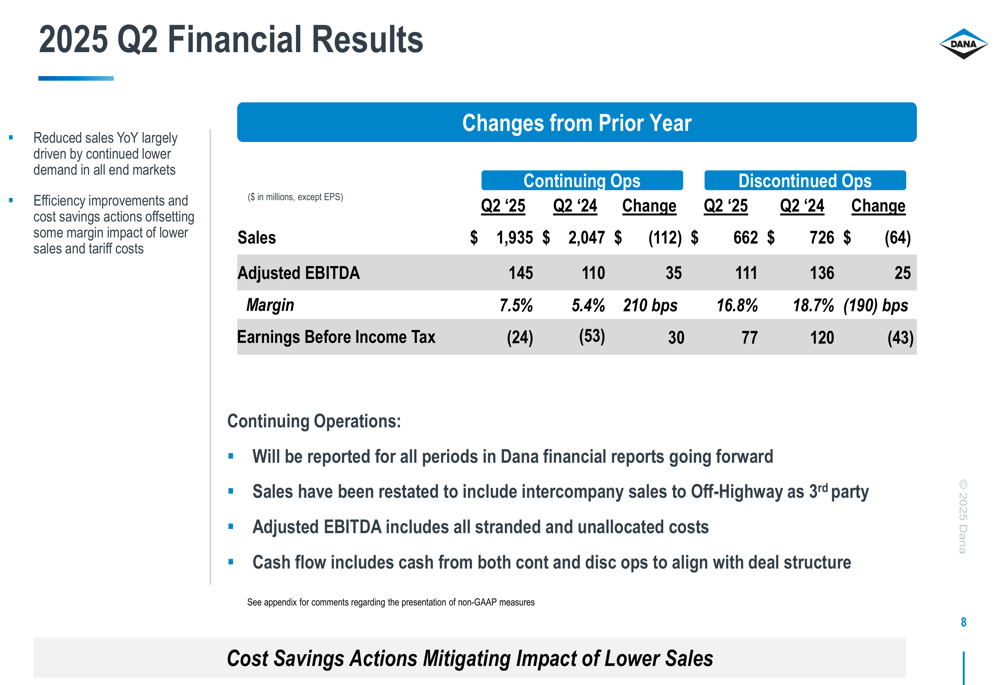

Dana’s second-quarter results demonstrated the company’s ability to improve profitability despite revenue challenges. The following slide summarizes the key financial metrics:

For continuing operations, Dana reported Q2 2025 sales of $1,935 million, down from $2,047 million in the same period last year. However, adjusted EBITDA improved significantly to $145 million (7.5% margin) compared to $110 million (5.4% margin) in Q2 2024, representing a 210 basis point improvement in margin. Earnings before income tax also improved by $30 million year-over-year.

This performance aligns with the earnings article reporting an EPS of $0.4381, which beat analyst expectations of $0.3499 by 25.21%, despite revenue falling short of forecasts. The market responded positively to these results, with Dana’s stock rising 5.4% in pre-market trading to $16.20 before closing even higher.

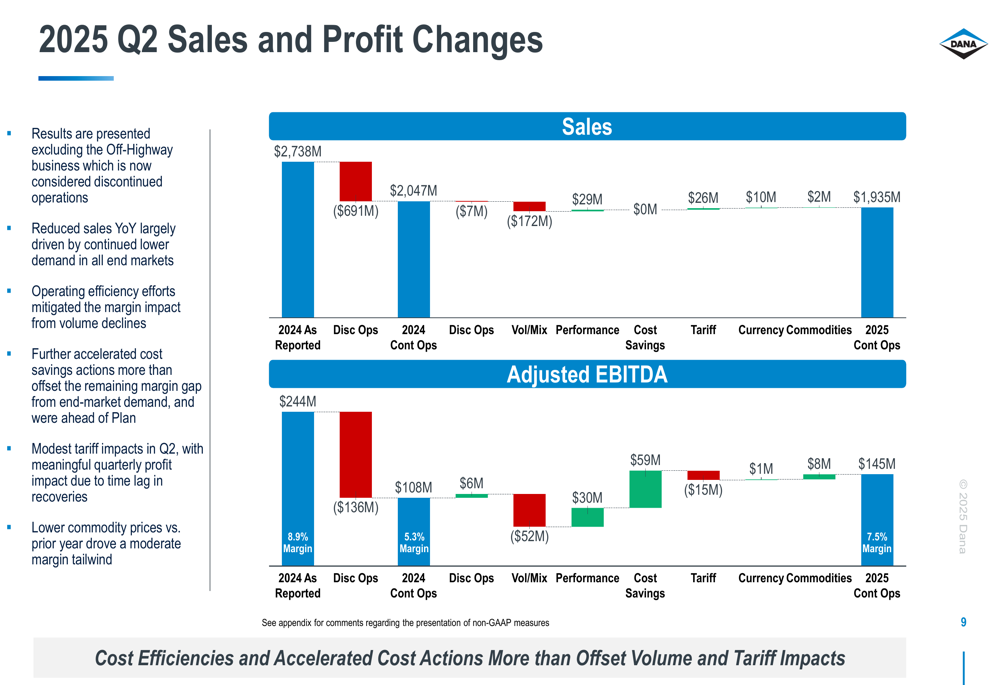

The following waterfall chart provides a detailed breakdown of the factors affecting Q2 sales and profit:

As illustrated, while volume and mix negatively impacted sales by $172 million and adjusted EBITDA by $52 million, these headwinds were more than offset by performance improvements ($30 million), cost savings ($59 million), and commodity benefits ($8 million). The company’s aggressive cost-cutting measures proved effective in mitigating the impact of lower volumes and tariff-related costs.

Detailed Financial Analysis

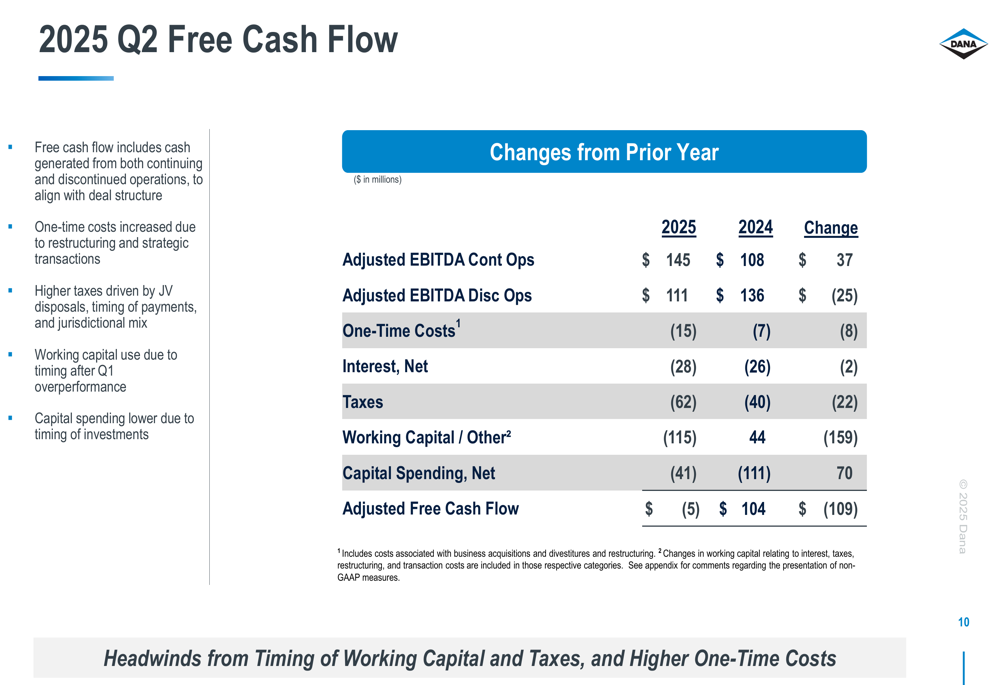

Dana’s free cash flow performance in Q2 faced some challenges, as shown in the following slide:

The company reported an adjusted free cash flow of -$5 million for Q2 2025, compared to $104 million in Q2 2024. This decline was primarily driven by working capital timing issues (-$159 million year-over-year change) and higher tax payments (-$22 million). However, these negative factors were partially offset by improved adjusted EBITDA from continuing operations (+$37 million) and reduced capital spending (+$70 million).

Despite the quarterly cash flow challenges, Dana’s full-year outlook remains positive, with the company raising its adjusted free cash flow guidance for 2025. Management cited higher profit, improved working capital efficiency, and lower capital investment as key drivers for the improved annual cash flow projection.

Forward-Looking Statements

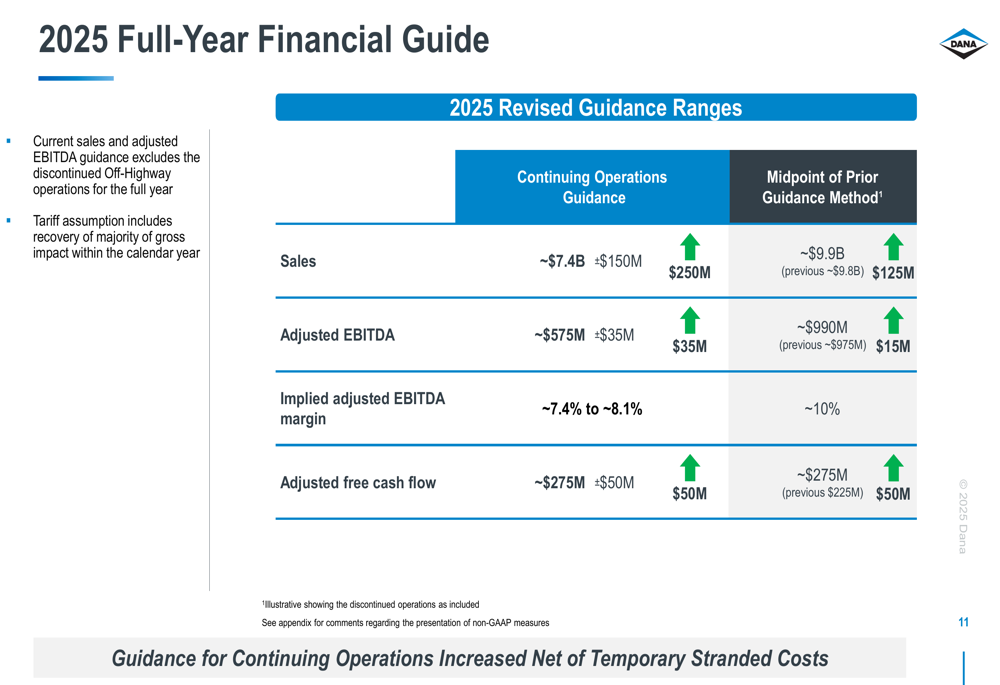

Dana raised its full-year 2025 guidance across key metrics, as detailed in the following slide:

The revised guidance for continuing operations includes:

- Sales of approximately $7.4 billion (increased by $150 million)

- Adjusted EBITDA of approximately $575 million (increased by $35 million)

- Implied adjusted EBITDA margin of 7.4% to 8.1%

- Adjusted free cash flow of approximately $275 million (increased by $50 million)

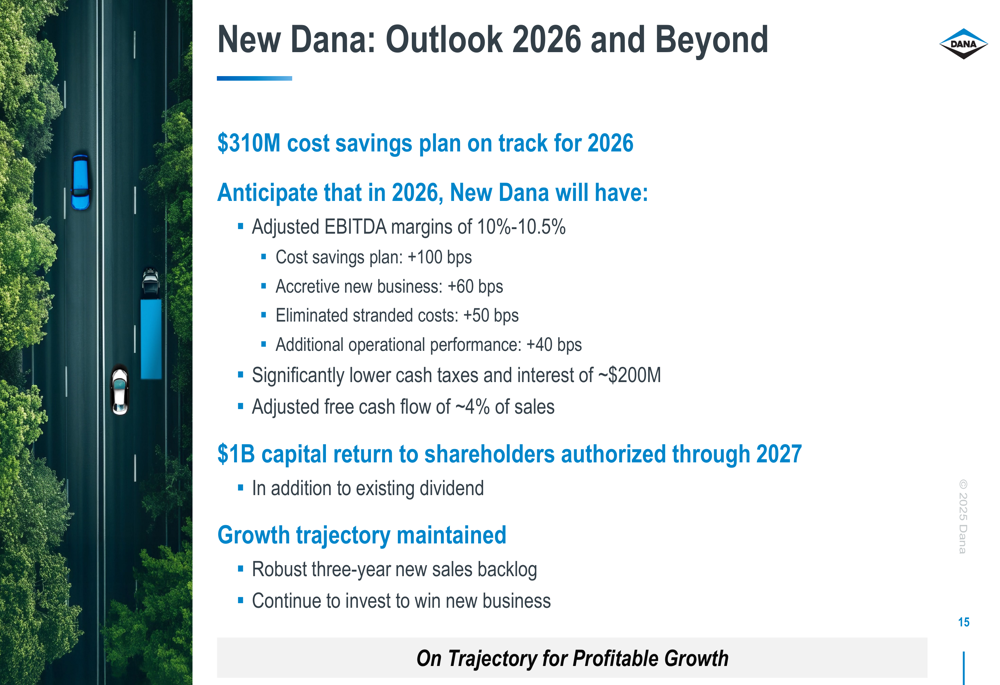

Looking beyond 2025, Dana provided an optimistic outlook for 2026 and beyond:

The company expects to achieve adjusted EBITDA margins of 10%-10.5% by 2026, driven by its $310 million cost savings plan, accretive new business, elimination of stranded costs, and additional operational performance improvements. Dana also anticipates significantly lower cash taxes and interest payments of approximately $200 million, with adjusted free cash flow reaching approximately 4% of sales.

This forward-looking guidance aligns with CEO Bruce McDonald’s (NYSE:MCD) comments in the earnings call, where he expressed confidence in the company’s strategic initiatives and ability to achieve these ambitious targets.

Strategic Initiatives

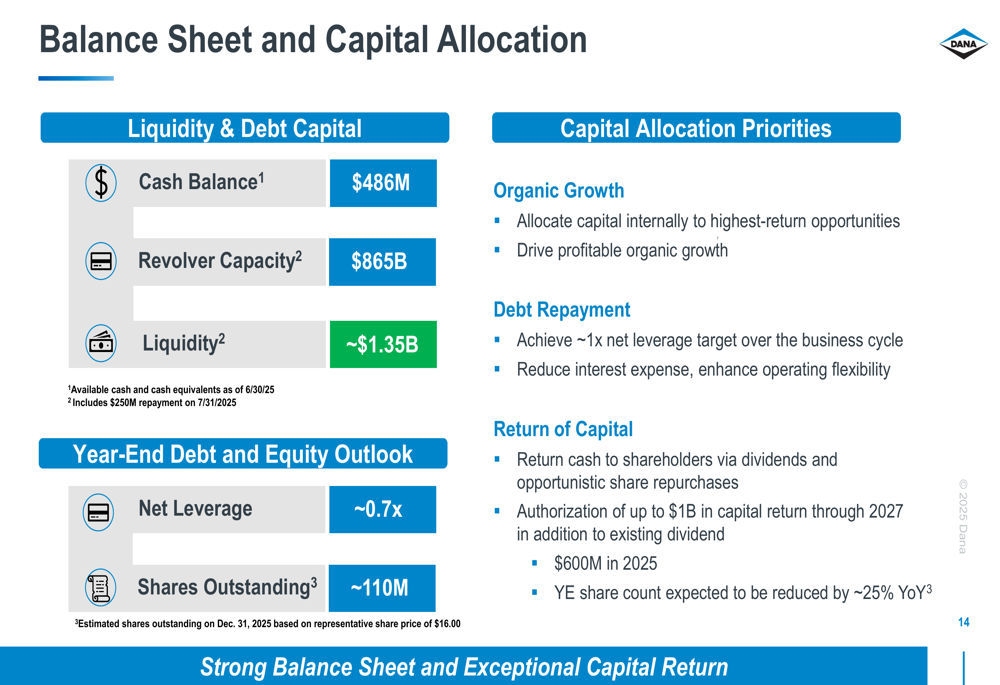

Dana’s capital allocation strategy is central to its transformation, as outlined in this slide:

With a strong liquidity position of approximately $1.35 billion (including $486 million in cash and $865 billion in revolver capacity), Dana is well-positioned to execute its strategic priorities. The company expects to achieve a net leverage ratio of approximately 0.7x by year-end, with shares outstanding reduced to approximately 110 million.

Dana’s capital allocation priorities include:

1. Organic growth through internal capital allocation

2. Debt repayment to achieve a net leverage target of approximately 1x

3. Return of capital to shareholders

The company has authorized a $1 billion capital return to shareholders through 2027, in addition to its existing dividend. In Q2 alone, Dana repurchased 14.6 million shares, returning $257 million to shareholders, with plans to repurchase an additional $100-$150 million in shares during Q3 2025.

Conclusion

Dana’s Q2 2025 presentation reveals a company in strategic transition, divesting its off-highway business to focus on its core light vehicle and commercial vehicle segments. Despite revenue challenges, Dana demonstrated improved profitability through effective cost management and operational efficiencies, leading to raised guidance for the full year.

The market has responded positively to Dana’s transformation strategy and improved performance, with the stock outperforming many peers year-to-date with a 34.74% gain. As Dana progresses toward completing its divestiture and implementing its cost savings initiatives, investors will be watching closely to see if the company can deliver on its ambitious margin and cash flow targets for 2026 and beyond.

With a strong balance sheet, clear capital allocation priorities, and a focused business strategy, Dana appears well-positioned to navigate industry challenges while creating shareholder value through both operational improvements and capital returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.