Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Dermapharm Holding SE (ETR:DMPG) (DMP) presented its Q1 2025 financial results on May 15, showing modest revenue growth but declining profitability as the company continues to navigate a strategic transition away from its vaccine business. The German pharmaceutical company reported a 1.2% year-over-year increase in revenue while adjusted EBITDA and earnings after tax declined significantly.

The company’s stock closed at €38.95 on May 14, down 1.27% ahead of the earnings presentation, with shares trading well below their 52-week high of €42.45 but above the 52-week low of €30.60.

Quarterly Performance Highlights

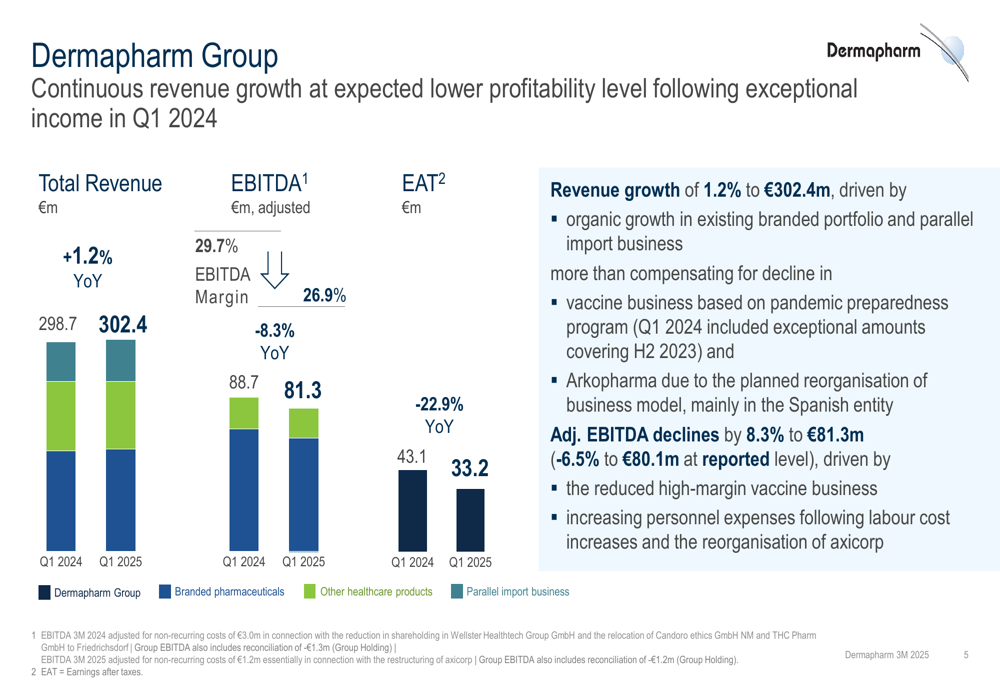

Dermapharm reported total revenue of €302.4 million for Q1 2025, representing a 1.2% increase compared to the same period last year. However, adjusted EBITDA fell by 8.3% to €81.3 million, resulting in an EBITDA margin of 26.9%. Earnings after tax (EAT) saw an even steeper decline of 22.9% to €33.2 million.

As shown in the following chart of Dermapharm’s Q1 2025 results, the company’s revenue growth was primarily driven by branded pharmaceuticals and parallel import business, which helped offset declines in the vaccine business and Arkopharma:

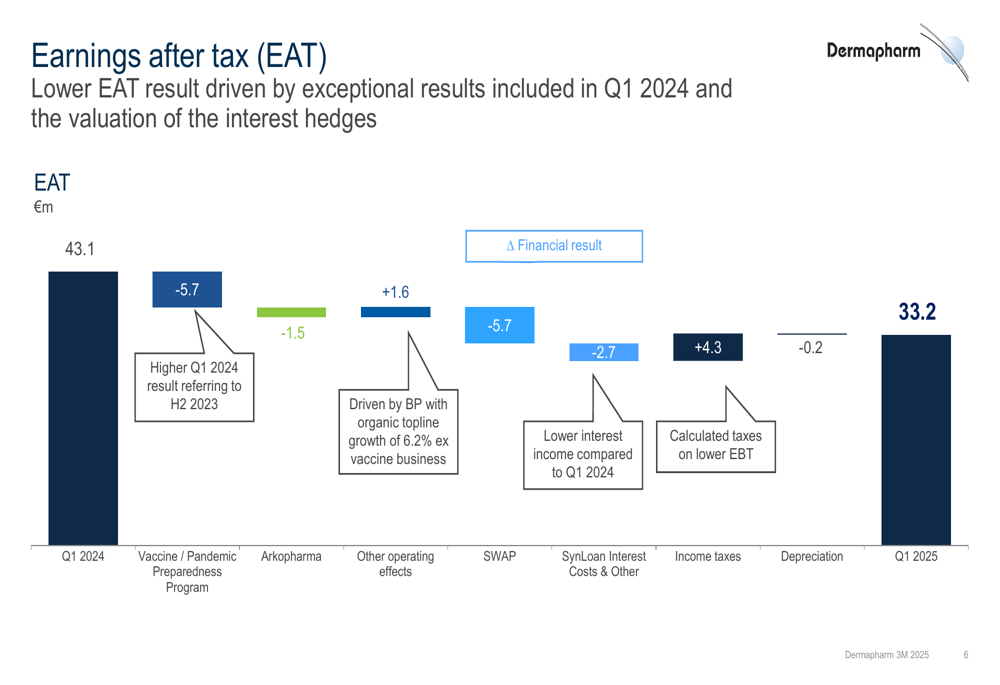

The company’s earnings after tax bridge reveals the key factors behind the 22.9% profit decline. The most significant negative impacts came from the vaccine/pandemic preparedness program (-€5.7 million) and interest rate swaps (-€5.7 million), while income taxes provided a positive contribution of €4.3 million:

Segment Performance Analysis

Dermapharm’s performance varied significantly across its three main business segments. The branded pharmaceuticals segment, which represents the company’s core business, saw revenue increase by 1.9% to €145.7 million. Notably, organic growth in this segment reached 6.2% when excluding the declining vaccine business. While adjusted EBITDA for the segment declined overall, it increased by 9% when excluding the vaccine business.

The other healthcare products segment experienced a 2.9% revenue decline to €96.2 million, primarily attributed to the ongoing restructuring of Arkopharma’s business model. EBITDA in this segment decreased by 5.9% to €17.4 million.

The parallel import business showed the strongest revenue growth at 7.1%, reaching €60.6 million. However, this segment reported negative EBITDA of -€0.9 million as the company initiated portfolio streamlining measures in Q1, including a €1.1 million restructuring provision. Management expects these measures to begin showing positive results from Q2 2025 onward.

Balance Sheet and Cash Flow

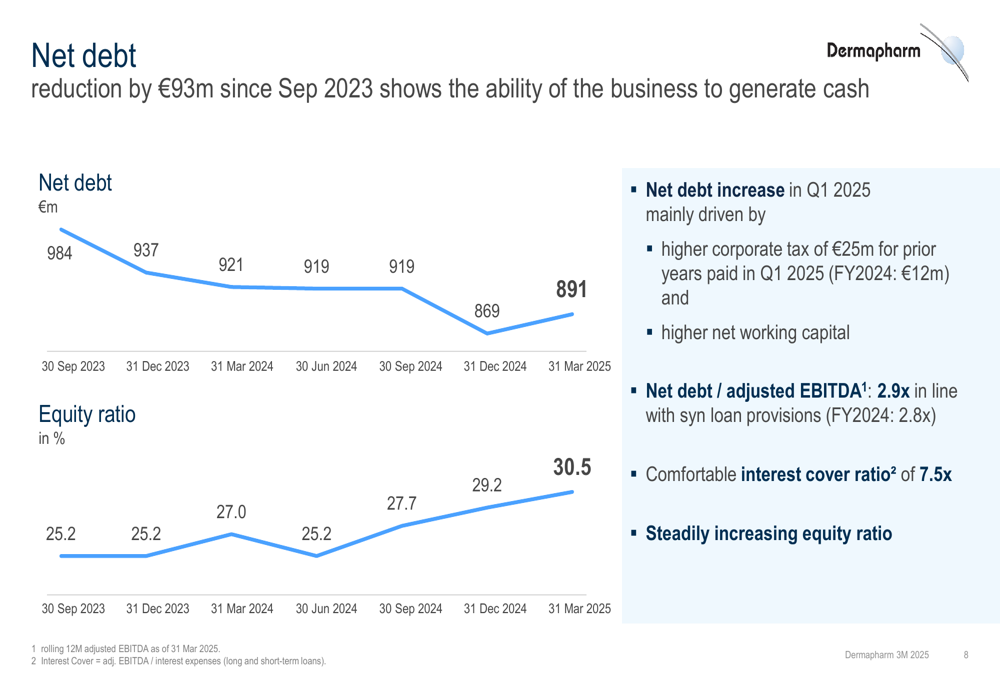

Dermapharm has made significant progress in strengthening its balance sheet, with net debt decreasing by €93 million since September 2023. The company’s equity ratio has steadily improved to 30.5% as of March 31, 2025, up from 29.2% at the end of 2024.

As illustrated in the following chart of net debt and equity ratio trends, the company has demonstrated consistent improvement in its financial position:

Despite these improvements, Dermapharm’s cash flow performance weakened in Q1 2025. Cash flow from operating activities declined to €4.2 million from €33.1 million in Q1 2024, primarily due to lower earnings before tax, increased tax payments, and higher working capital requirements. This resulted in a negative free cash flow of -€5.1 million compared to a positive €26.4 million in the prior-year period.

The company’s cash conversion rate dropped dramatically from 37.3% to 5.2%, reflecting these challenges. Working capital increased by more than 7%, driven by higher inventory levels and lower trade payables. Management attributed the inventory increase to underlying growth, inflationary production costs, and higher buffer stock requirements.

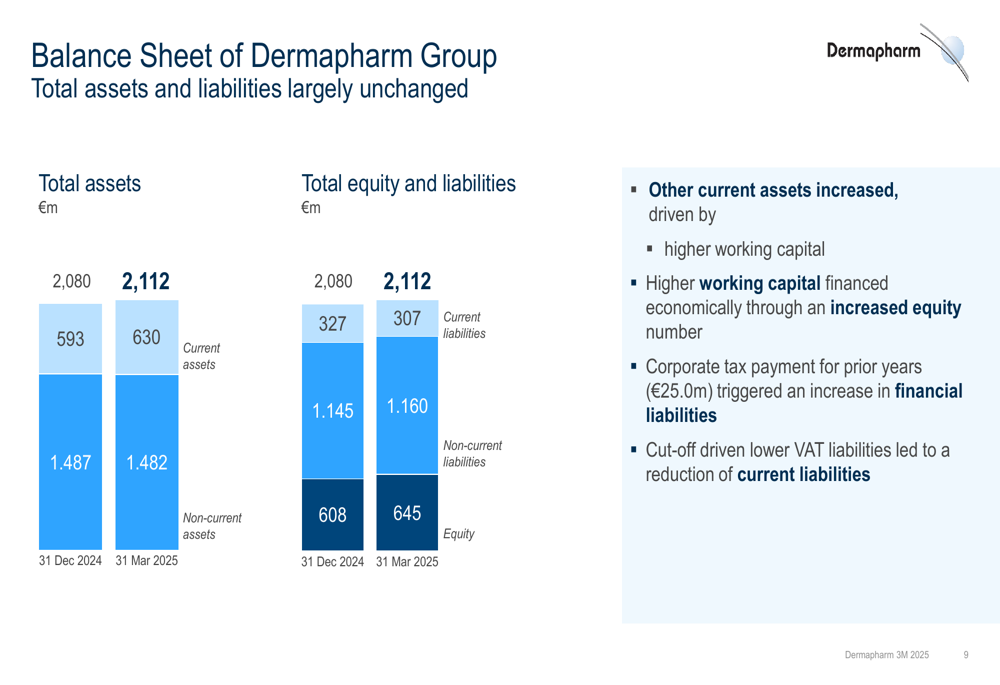

The following balance sheet overview shows the company’s financial position as of March 31, 2025:

Forward-Looking Statements

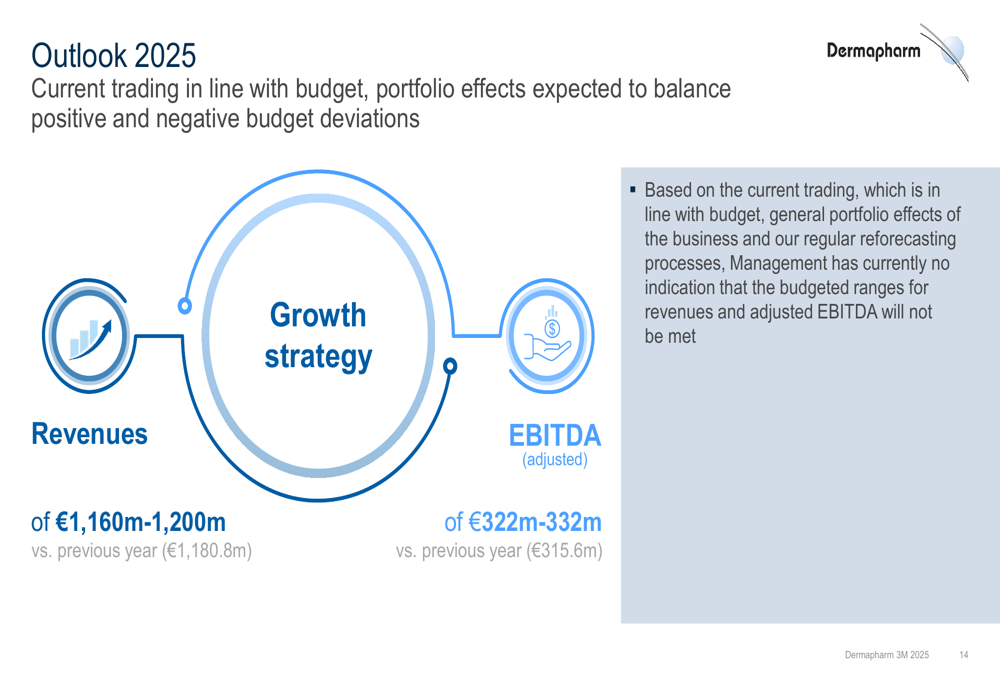

Despite the mixed Q1 results, Dermapharm maintained its full-year 2025 guidance, projecting revenues between €1,160 million and €1,200 million compared to €1,180.8 million in 2024. The company expects adjusted EBITDA to improve to between €322 million and €332 million, up from €315.6 million in the previous year.

Management expressed confidence in meeting these targets, stating they have "no indication that the budgeted ranges for revenues and adjusted EBITDA will not be met." The outlook suggests that the company expects its performance to improve in the coming quarters as restructuring efforts begin to yield results.

As shown in the following outlook slide, Dermapharm’s 2025 guidance reflects the company’s confidence in its growth strategy:

The company highlighted several positive factors expected to drive performance for the remainder of 2025, including strong organic growth in high-margin branded pharmaceuticals, international business expansion, growth in allergology products, and improvements in the parallel import business following the restructuring initiatives. These factors are anticipated to compensate for the continued revenue decline in the vaccine business and challenges at Arkopharma.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.