Deere and Tractor Supply shares fall after Trump criticizes farm equipment prices

Introduction & Market Context

Devyser Diagnostics AB (DVYSR) reported its first quarter 2025 results on April 29, showing modest revenue growth amid ongoing restructuring efforts and currency headwinds. The company’s stock declined 2.83% following the presentation, trading at 95.5 SEK, significantly below its 52-week high of 145 SEK.

The diagnostics company, which specializes in clinical genetics and transplantation testing, highlighted its strategic shift toward becoming a "one-stop shop" for genetics and transplantation laboratories while navigating organizational adjustments and preparing for several product launches.

Quarterly Performance Highlights

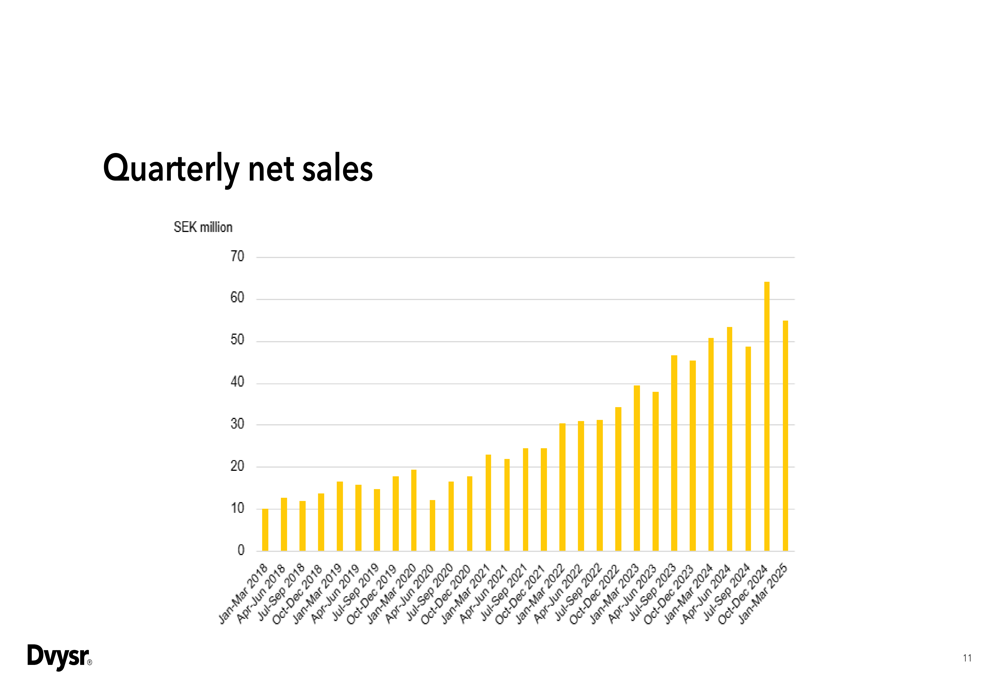

Devyser reported Q1 2025 revenue of 54.8 million SEK, representing a 7.9% increase from 50.7 million SEK in the same period last year. The company maintained a strong gross margin of 83.4%, slightly improved from 82.7% in Q1 2024.

As shown in the following quarterly net sales trend:

However, EBIT declined to -20.5 million SEK compared to -12.2 million SEK in Q1 2024, impacted by 8 million SEK in one-off restructuring costs and 6 million SEK in negative foreign exchange effects. Despite these challenges, the company maintained a solid financial position with 114 million SEK in cash and no debt.

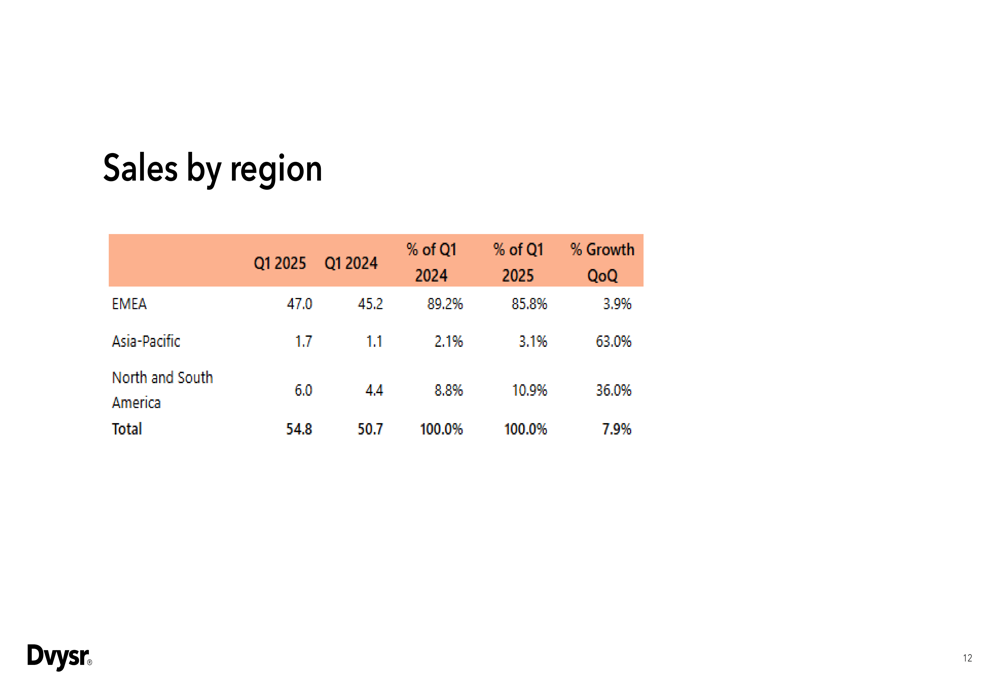

Regional performance varied significantly, with North and South America growing 36% and Asia-Pacific surging 63%, while the core EMEA region, which represents 85.8% of total sales, grew by just 3.9%:

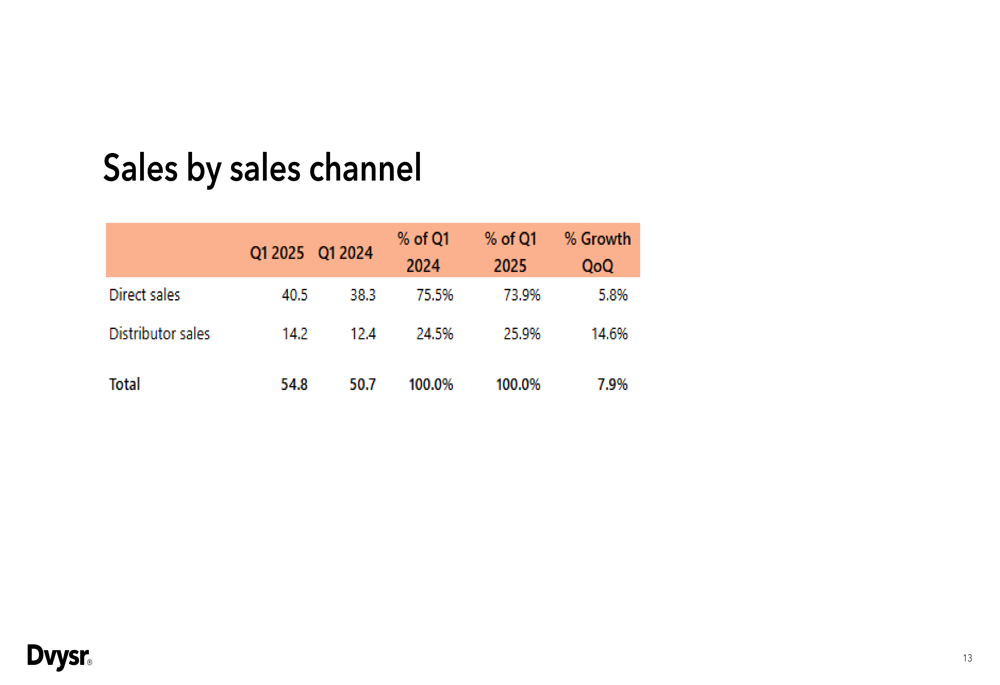

The company’s sales channels showed distributor sales outpacing direct sales, with 14.6% growth compared to 5.8% for direct sales:

Strategic Initiatives

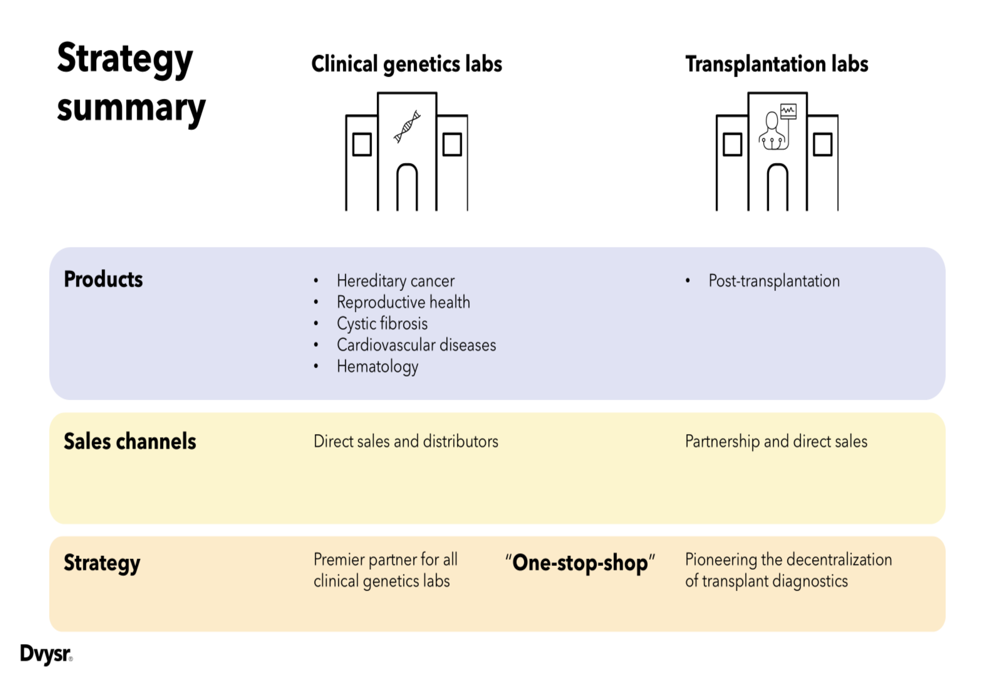

Devyser’s presentation emphasized its two-pronged strategy focusing on clinical genetics laboratories and transplantation laboratories. For clinical genetics, the company offers products for hereditary cancer, reproductive health, cystic fibrosis, cardiovascular diseases, and hematology through both direct sales and distributors. In transplantation, Devyser is focusing on post-transplantation diagnostics primarily through partnerships and direct sales.

The company’s strategic approach is illustrated in this summary:

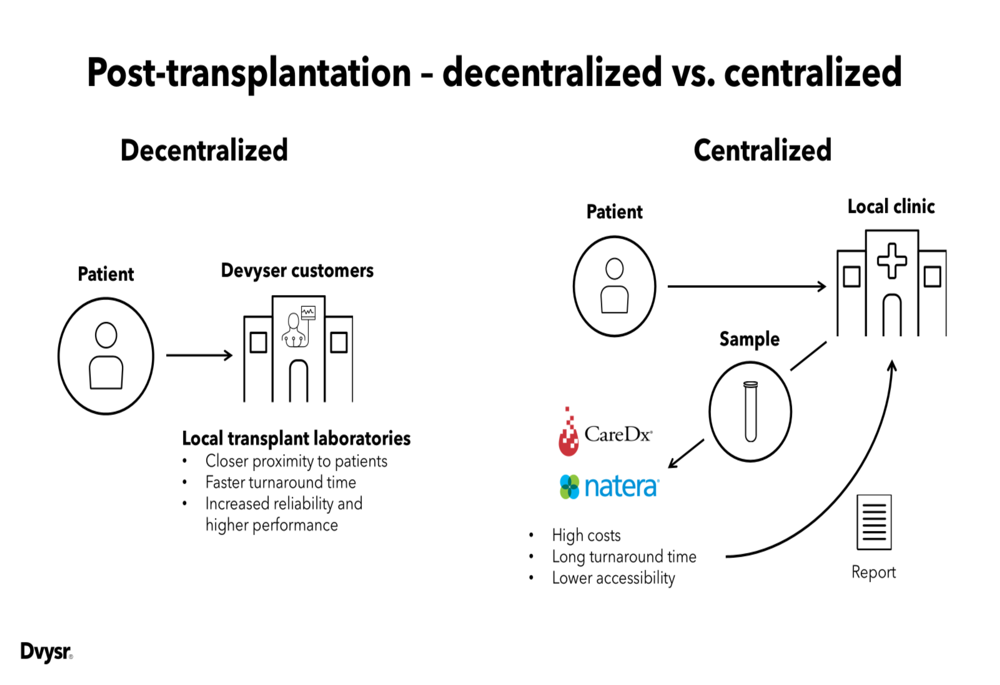

A key competitive advantage highlighted in the presentation is Devyser’s decentralized approach to post-transplantation diagnostics, which the company claims offers closer proximity to patients, faster turnaround times, and increased reliability compared to centralized testing offered by competitors:

Product Development Pipeline

Devyser outlined several important product launches and regulatory milestones for 2025:

1. HLA loss product scheduled for launch before summer, addressing clinical needs in patients with malignant disease after stem cell transplantation

2. Genomic blood group typing product on schedule for summer launch

3. Reimbursement submission to MolDx for Transplant trace cfDNA product

4. FDA approval process for cfDNA progressing with enrollment studies at 3-5 transplant centers

The company also highlighted securing IVDR approval for Devyser RHD, its first Class D IVD product, which it described as a major milestone that demonstrates capability to support development of any IVD product regardless of risk class.

The Thermo Fisher Scientific (NYSE:TMO) partnership continues to show momentum:

Regional Performance

North America emerged as a growth driver, with several initiatives underway:

1. Devyser Genomic Laboratories in Atlanta progressing with Accept cfDNA timeline for reimbursement during summer 2025

2. RHD testing positioned as a potential "gamechanger" in the US market, with Canadian Blood Services already placing orders

3. Large US accounts expected to go live during Q3/Q4 2025

4. CFTR customers starting clinical routine in Q2

European performance was mixed, with strong growth in Spain, France, UK and DACH regions (~50% year-over-year) offset by softer performance in Italy, Benelux and Nordics, which the company attributed to large orders placed in Q4 2024. Across Europe, Devyser increased its total number of buying customers by 10% and average selling prices by 13% (excluding Transplantation).

Forward-Looking Statements

Despite the modest 7.9% growth in Q1, Devyser maintained its target of 30% organic growth for 2025, suggesting significant acceleration in coming quarters. The company outlined four key focus areas going forward:

1. Executing on updated strategy

2. Continuing to work on organizational efficiency

3. Launching new products

4. Progressing toward profitability

Fredrik Dahl, Interim CEO, emphasized that 2025 would focus on leveraging recent investments, focusing the organization, and turning the company toward profitability.

Challenges and Outlook

While Devyser highlighted several positive developments, the presentation revealed significant challenges, including the substantial impact of one-off costs and currency headwinds on profitability. The company’s ability to achieve its ambitious 30% growth target for 2025 will depend on successfully accelerating growth from the current 7.9% level.

The restructuring efforts appear to be ongoing, with the presentation noting that "majority of organizational adjustments done, still a few more on-going reflecting updated strategy." These adjustments may continue to impact short-term financial performance as the company positions itself for long-term growth in the diagnostics market.

With several product launches planned and expanding presence in North America, Devyser is betting on innovation and geographic expansion to drive growth while working toward profitability in an increasingly competitive diagnostic testing landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.