Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

DexCom , Inc. (NASDAQ:DXCM) released its second quarter 2025 earnings presentation on July 30, highlighting continued revenue growth and key product developments. The continuous glucose monitoring (CGM) leader reported 15% organic revenue growth, driven by strong performance in both domestic and international markets. In after-hours trading, DexCom shares rose 0.44% to $89.74, building on a regular session close of $89.35.

The company’s performance comes amid continued expansion in the diabetes care market, with particular emphasis on new product features and extended sensor wear time to enhance competitive positioning. DexCom has maintained its growth trajectory despite increasing competition in the CGM space.

Quarterly Performance Highlights

DexCom reported Q2 2025 revenue of $1.157 billion, representing 15% organic growth compared to the same period last year. The company achieved balanced growth across its markets, with 15% revenue growth in the U.S. and 14% international growth.

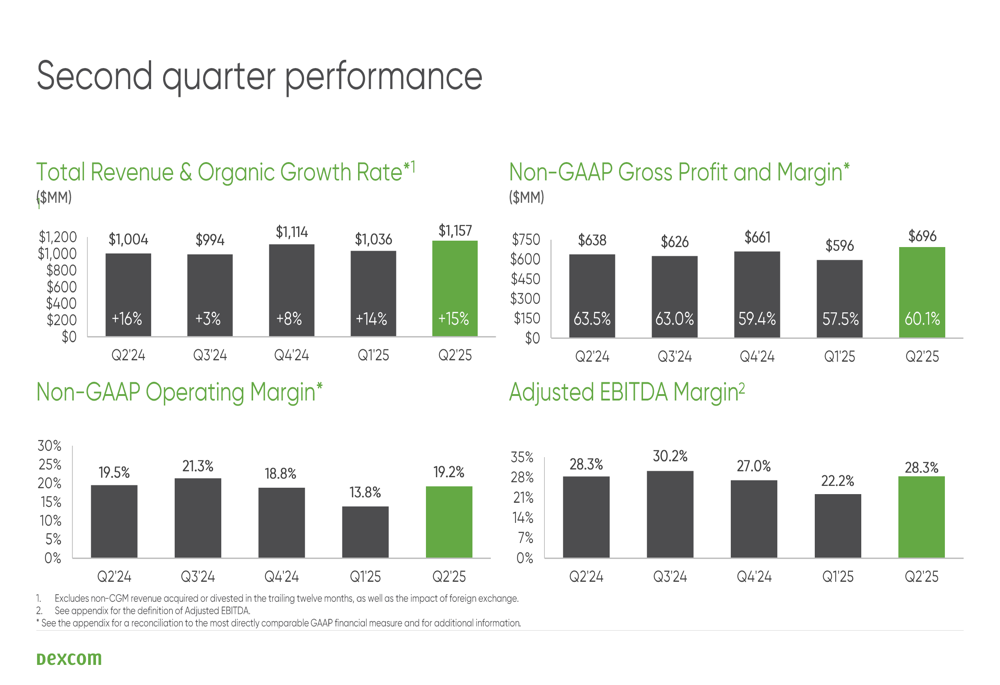

As shown in the following quarterly highlights slide:

Beyond revenue growth, DexCom generated over 300 basis points of operating expense leverage compared to Q2 2024. The company also highlighted two significant product developments: FDA clearance for the Dexcom G7 15-day sensor and the launch of an AI Smart Food Logging feature, both aimed at enhancing the user experience and competitive differentiation.

Detailed Financial Analysis

DexCom’s financial performance showed strength across multiple metrics, though with some margin compression. The company’s quarterly performance trends are illustrated in the following chart:

Total (EPA:TTEF) revenue increased from $1,004 million in Q2 2024 to $1,157 million in Q2 2025. Non-GAAP gross profit rose to $696 million, up from $638 million in the prior year period. However, gross profit margin decreased slightly to 60.1% from 63.5% a year earlier.

Non-GAAP operating margin showed a minor decline to 19.2% from 19.5% in Q2 2024, while adjusted EBITDA margin remained stable at 28.3%. The company maintained profitability despite ongoing investments in product development and market expansion.

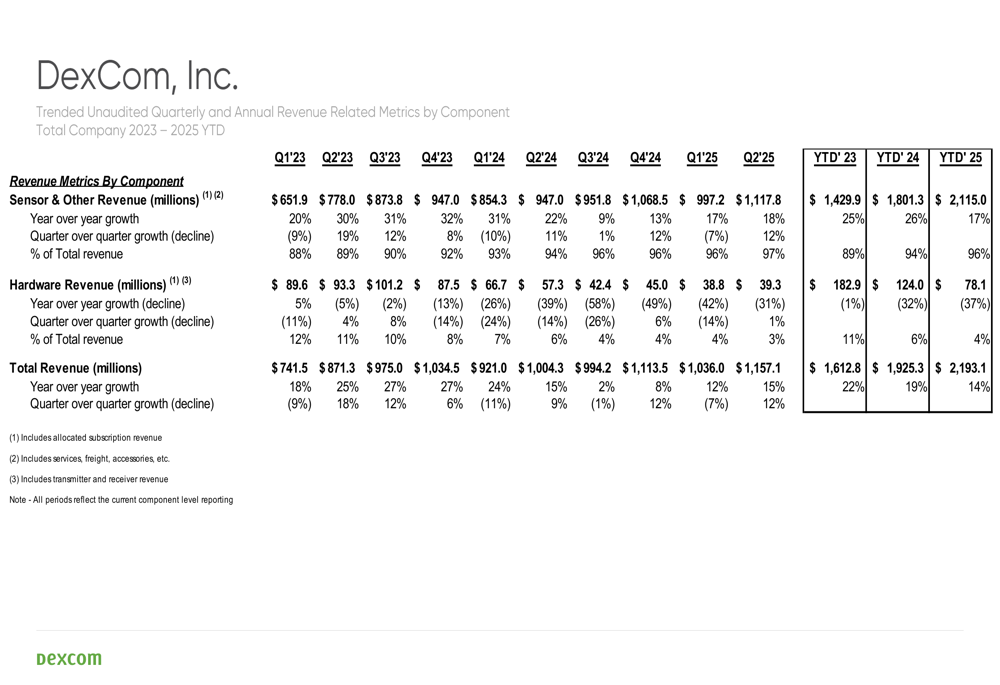

A deeper analysis of revenue components reveals divergent trends between sensor and hardware sales:

Sensor and other revenue, which represents DexCom’s recurring revenue stream, grew to $1,117.8 million in Q2 2025, a 17% increase year-to-date. In contrast, hardware revenue continued its expected decline, falling to $39.3 million, representing a 37% decrease year-to-date. This shift reflects DexCom’s business model transition toward recurring sensor revenue.

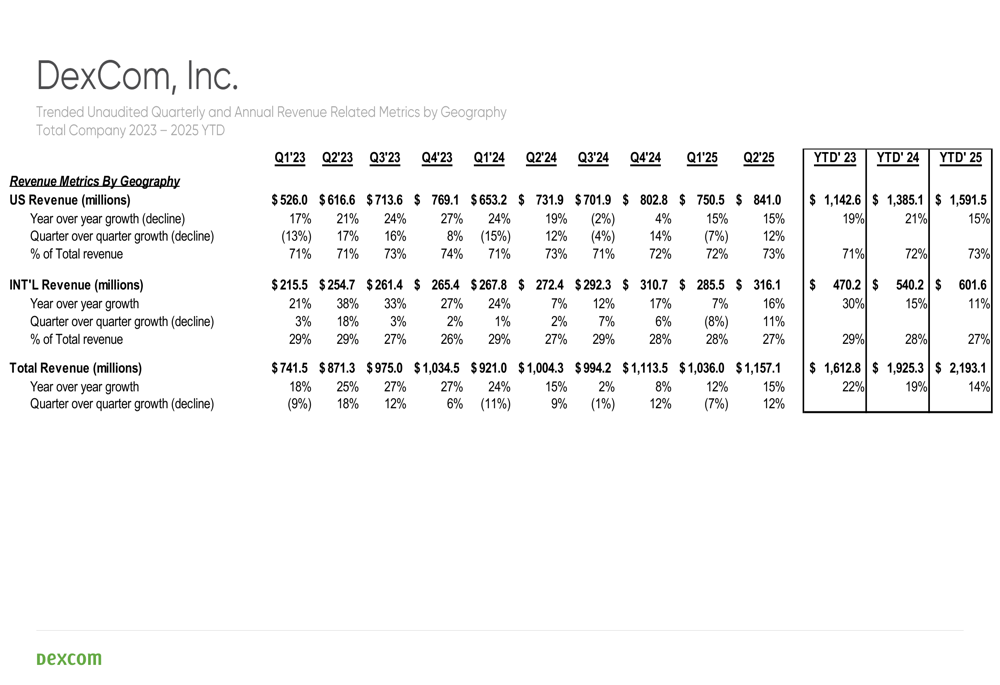

Geographic performance shows continued growth across regions, though at a moderating pace compared to previous years:

U.S. revenue reached $841.0 million in Q2 2025, representing 15% growth year-to-date, while international revenue grew to $316.1 million, an 11% increase year-to-date. Both figures show a slowing growth rate compared to 2024, when U.S. and international revenues grew 21% and 15% respectively.

Strategic Initiatives & Product Development

DexCom’s strategic focus remains on product innovation and market expansion. The FDA clearance for the extended-wear G7 sensor represents a significant competitive advantage, allowing users to wear the sensor for 15 days instead of the current 10-day period. This development addresses a key user preference for longer wear time and reduced sensor changes.

The company also launched its AI Smart Food Logging feature, leveraging artificial intelligence to improve the user experience and provide more comprehensive diabetes management tools. These innovations align with DexCom’s strategy to enhance its product ecosystem and maintain leadership in the CGM market.

In the previous quarter’s earnings call, CEO Kevin Sayer had emphasized the value DexCom’s products bring, stating, "We are one of the few medical products that provides tremendous information and also saves cost to the system." The Q2 developments further support this value proposition.

Forward-Looking Statements

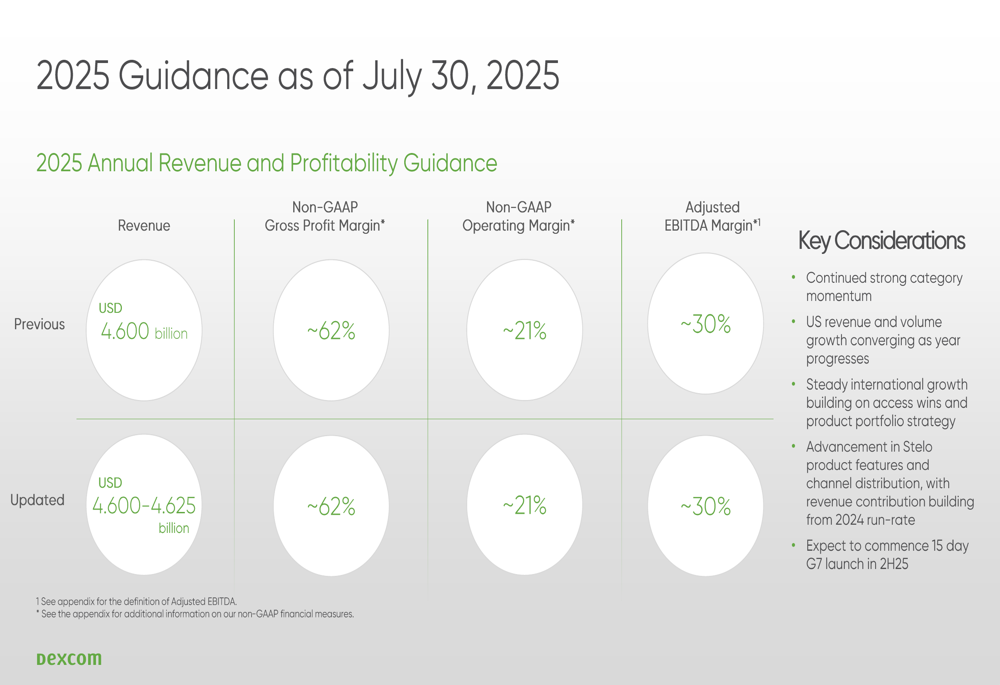

DexCom slightly raised its 2025 revenue guidance and maintained its margin expectations, as shown in the following guidance slide:

The updated revenue guidance range of $4.600-$4.625 billion represents a modest increase from the previous guidance of $4.600 billion. The company continues to expect a non-GAAP gross profit margin of approximately 62%, a non-GAAP operating margin of about 21%, and an adjusted EBITDA margin of approximately 30%.

Key considerations for the remainder of 2025 include:

1. Continued strong category momentum

2. Convergence of U.S. revenue and volume growth as the year progresses

3. Steady international growth building on access wins and product portfolio strategy

4. Advancement in Stelo product features and channel distribution

5. Commencement of the 15-day G7 sensor launch in the second half of 2025

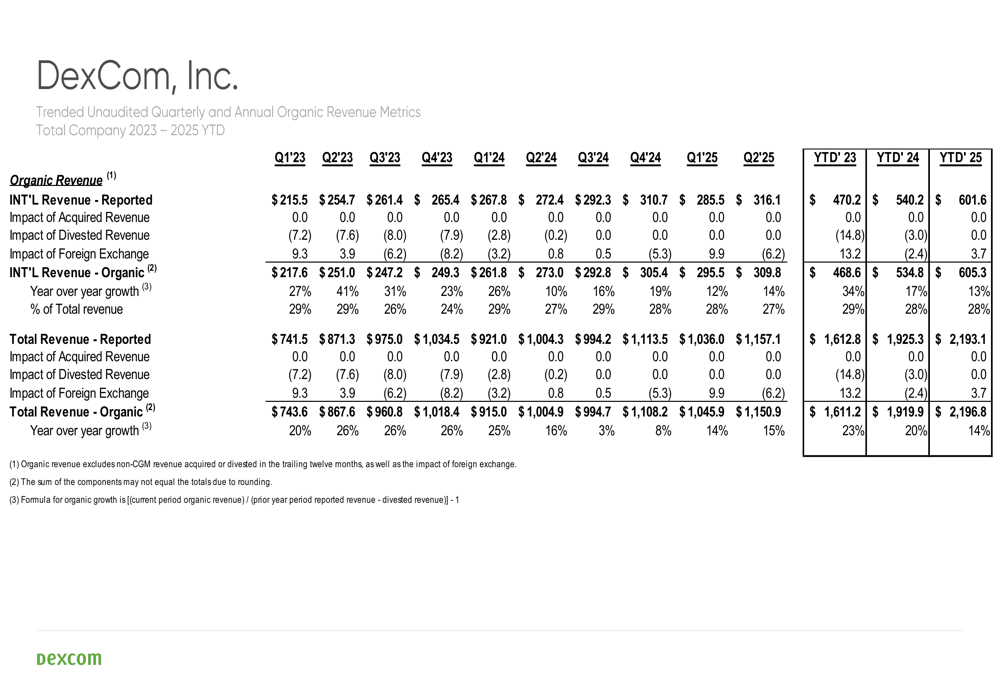

The organic revenue trends provide context for DexCom’s growth trajectory:

Total organic revenue has grown from $743.6 million in Q1 2023 to $1,150.9 million in Q2 2025, demonstrating consistent expansion despite a gradually moderating growth rate. International organic revenue has shown similar trends, increasing from $217.6 million to $309.8 million over the same period.

DexCom’s Q2 2025 performance and guidance suggest continued growth, albeit at a more moderate pace than in previous years. The company’s focus on product innovation, particularly the extended-wear G7 sensor and AI features, positions it to maintain its leadership in the competitive CGM market while addressing evolving user needs and preferences.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.