TSX runs higher on rate cut expectations

Introduction & Market Context

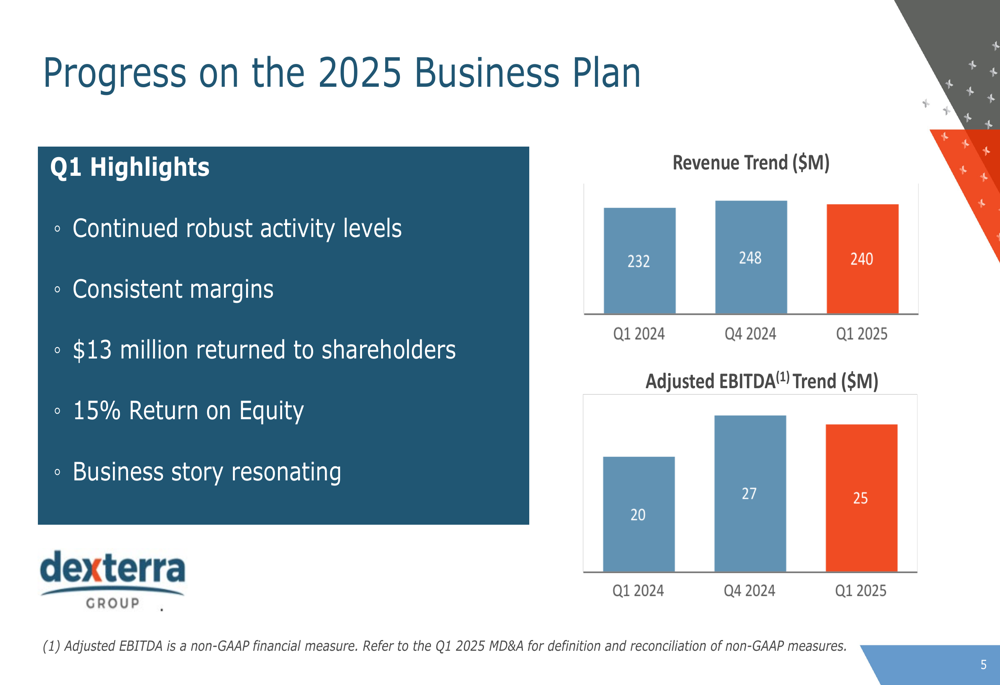

Dexterra Group Inc (TSX:DXT) presented its Q1 2025 financial results on May 7, 2025, highlighting year-over-year growth despite a sequential decline from the previous quarter. The company reported revenue of $240 million and Adjusted EBITDA of $25 million for the quarter, representing improvements of 3.5% and 25% respectively compared to Q1 2024.

The results come after Dexterra missed earnings expectations in Q4 2024, when the company reported EPS of $0.11 against a forecast of $0.135. The stock has shown resilience since then, with shares trading at $8.43 as of May 6, 2025, up from $7.34 following the Q4 earnings release.

Quarterly Performance Highlights

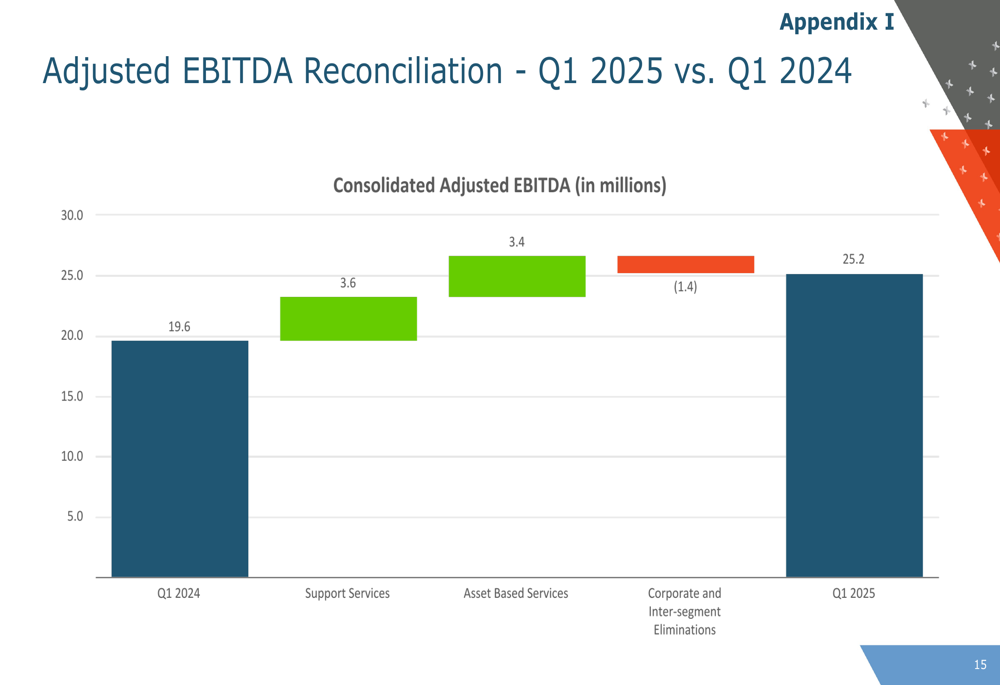

Dexterra’s Q1 2025 performance demonstrated continued progress on its business plan, with revenue of $240 million representing a modest increase from $232 million in Q1 2024, though down from $248 million in Q4 2024. More significantly, Adjusted EBITDA reached $25 million, a substantial 25% improvement from $20 million in the same period last year, but slightly below the $27 million reported in Q4 2024.

As shown in the following chart of quarterly revenue and EBITDA trends:

The company highlighted its achievement of a 15% Return on Equity target and returned $13 million to shareholders during the quarter. Management emphasized consistent margins and robust activity levels across its business segments, though with varying performance between divisions.

Segment Analysis

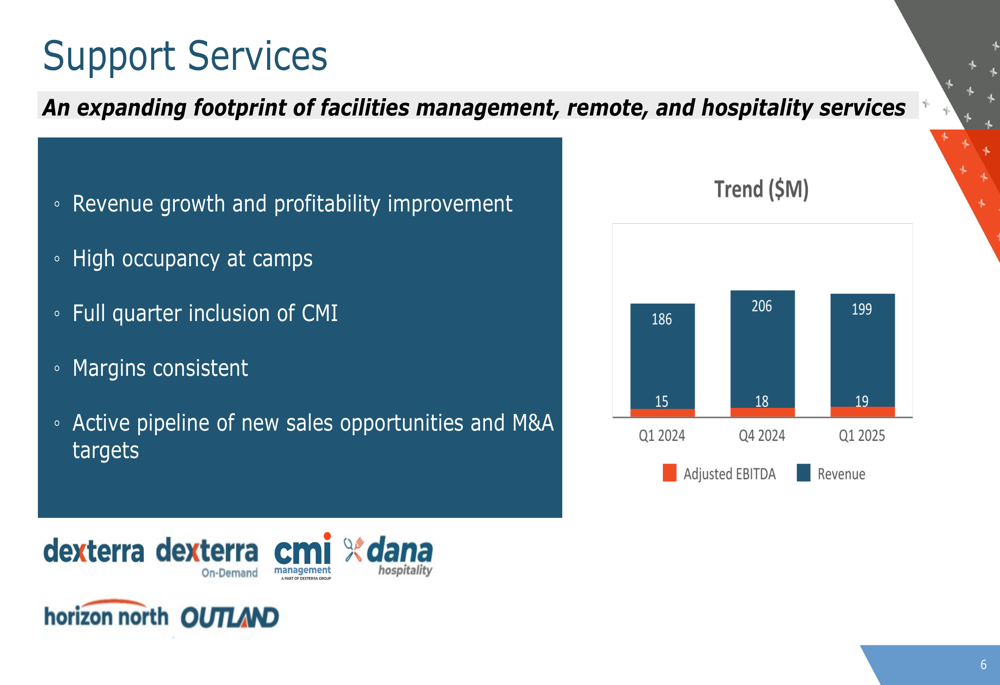

Dexterra’s Support Services segment, which encompasses facilities management, remote services, and hospitality, showed strong performance with revenue of $199 million and Adjusted EBITDA of $19 million in Q1 2025. This represents year-over-year growth in both revenue and profitability compared to Q1 2024 figures of $186 million and $15 million respectively.

The segment benefited from high occupancy at camps and the full quarter inclusion of the CMI acquisition. Management noted an active pipeline of new sales opportunities and potential M&A targets in this segment.

The following chart illustrates the Support Services segment’s consistent growth trajectory:

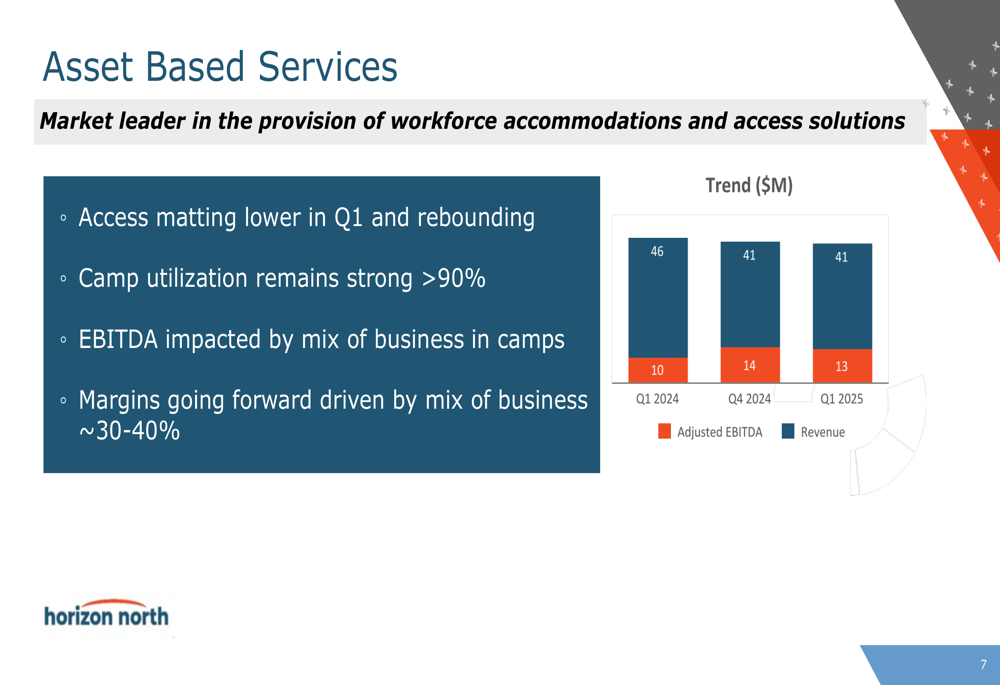

In contrast, the Asset Based Services segment, which focuses on workforce accommodations and access solutions, faced some challenges. Revenue remained stable at $41 million compared to Q4 2024 but decreased from $46 million in Q1 2024. Adjusted EBITDA was $13 million, up from $10 million in Q1 2024 but slightly down from $14 million in Q4 2024.

Management attributed the mixed performance to lower access matting activity in Q1, though noted it was rebounding. Camp utilization remained strong at over 90%, but EBITDA was impacted by the mix of business in camps.

The segment’s performance is illustrated in the following chart:

Financial Position & Outlook

Dexterra maintained a strong financial position with a debt to Adjusted EBITDA ratio of 1.0X. The company emphasized its strong EBITDA to free cash flow conversion rate of over 50% annually and highlighted the renewal of its credit facility, providing flexibility for future acquisitions.

During the quarter, Dexterra repurchased approximately 1 million shares at an average price of $7.69, demonstrating confidence in its business outlook and commitment to returning value to shareholders.

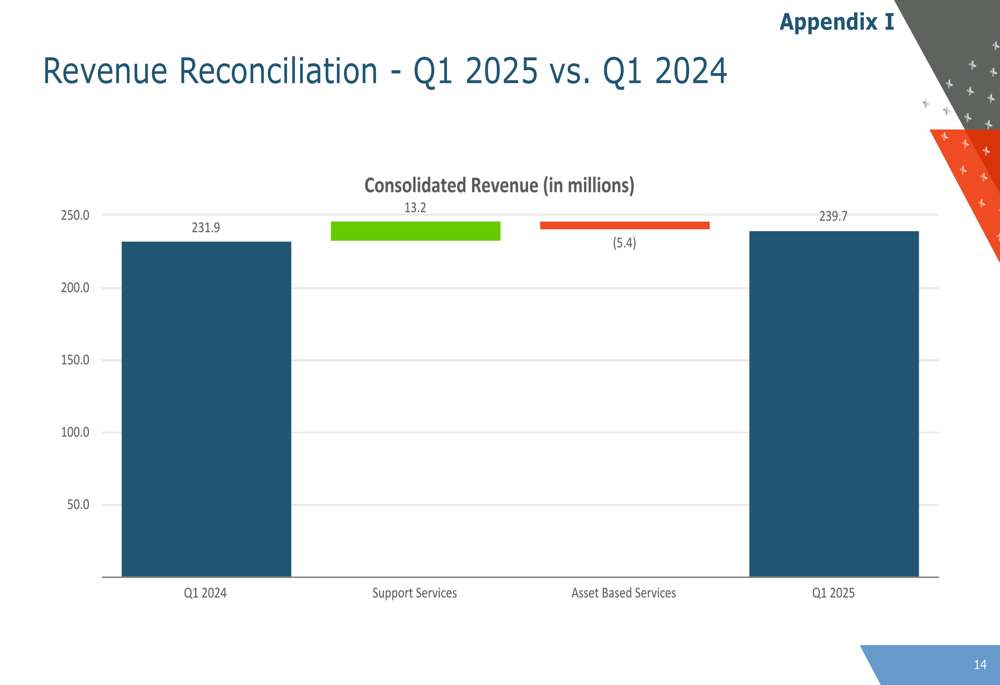

The revenue reconciliation between Q1 2024 and Q1 2025 provides additional insight into the drivers of Dexterra’s performance:

Similarly, the Adjusted EBITDA reconciliation shows the contribution of each segment to the overall improvement:

Forward-Looking Statements

Looking ahead, Dexterra outlined its path forward with a continued focus on maintaining its 15% or higher return on equity target. The company is actively monitoring potential tariff impacts and changing economic conditions that could affect its business.

Capital allocation priorities remain consistent: maintaining the dividend, supporting selective high-return capital investments, opportunistic share buybacks, and pursuing accretive acquisitions. Management emphasized continued execution, profitability, and building a business for the long term.

For the Asset Based Services segment, Adjusted EBITDA margins are expected to fluctuate between 30-40% depending on the mix of business. The Support Services segment is anticipated to maintain consistent margins with opportunities for organic growth and strategic acquisitions.

Despite the sequential decline from Q4 2024, Dexterra’s year-over-year improvements and strong financial position suggest the company is making progress on its strategic objectives while navigating changing market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.