Oil prices extend losses as traders downplay Russia sanction risks

Introduction & Market Context

Dexterra Group Inc (TSX:DXT) presented its Q2 2025 results on August 6, 2025, revealing a strategic focus on expansion through acquisitions despite mixed financial performance. The company’s stock closed at $9.37 on August 5, down 1.88% ahead of the results announcement, reflecting some market caution.

The presentation comes after Dexterra’s Q1 2025 results fell short of analyst expectations, with the company having reported EPS of $0.14 against a forecast of $0.145 and revenue of $239.73 million versus an expected $252.59 million. Against this backdrop, Q2 2025 results show sequential improvement but continued year-over-year revenue challenges.

Quarterly Performance Highlights

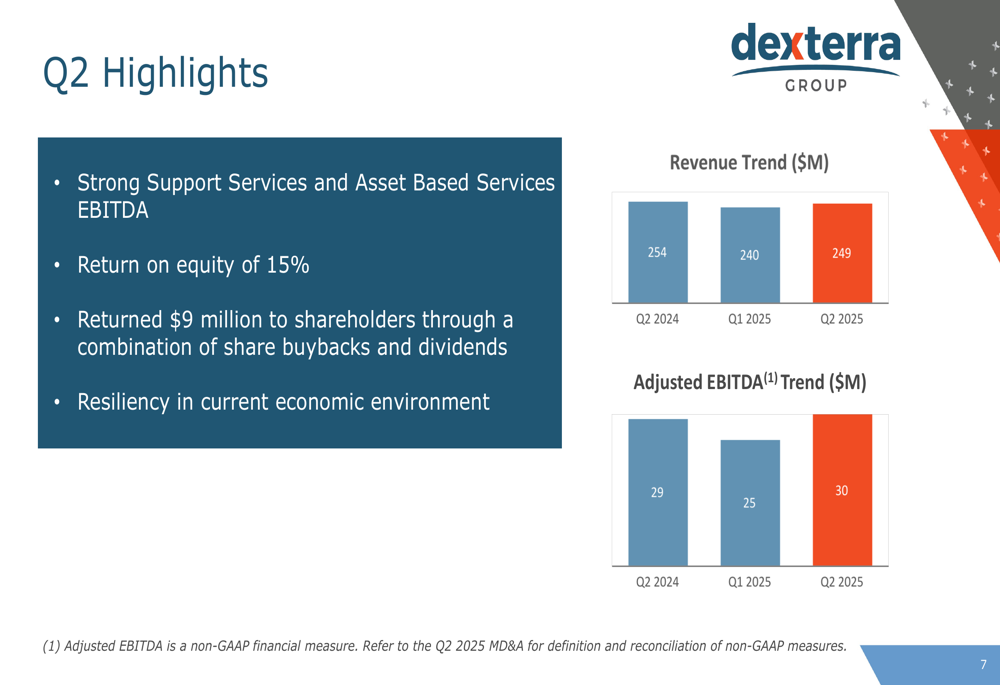

Dexterra reported Q2 2025 revenue of $249.3 million, representing a 1.7% decrease from $253.6 million in Q2 2024, but a 4% increase from $239.7 million in Q1 2025. Despite the year-over-year revenue decline, adjusted EBITDA improved to $30.0 million, up from $29.3 million in Q2 2024 and $25.2 million in Q1 2025.

The company highlighted its strong return on equity of 15% and returned $9 million to shareholders through a combination of share buybacks and dividends during the quarter, demonstrating its commitment to shareholder value despite economic headwinds.

As shown in the following chart of quarterly performance metrics:

Strategic Acquisitions

A central focus of Dexterra’s Q2 presentation was its strategic acquisition strategy. The company announced two significant acquisitions aimed at expanding both its U.S. presence and strengthening its Canadian operations.

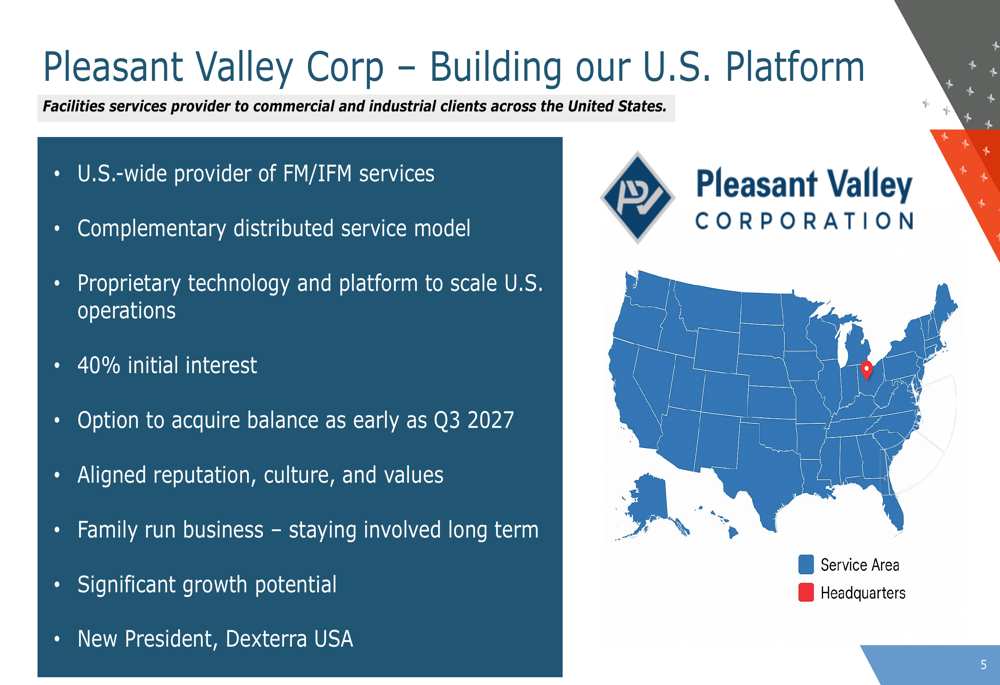

The first acquisition involves Pleasant Valley Corp (PVC), which provides facilities services to commercial and industrial clients across the United States. This move represents Dexterra’s strategic entry into the U.S. market with a 40% initial interest and an option to acquire the balance as early as Q3 2027. The company emphasized the complementary service model and proprietary technology platform that will help scale U.S. operations.

The U.S. expansion strategy is illustrated in this acquisition overview:

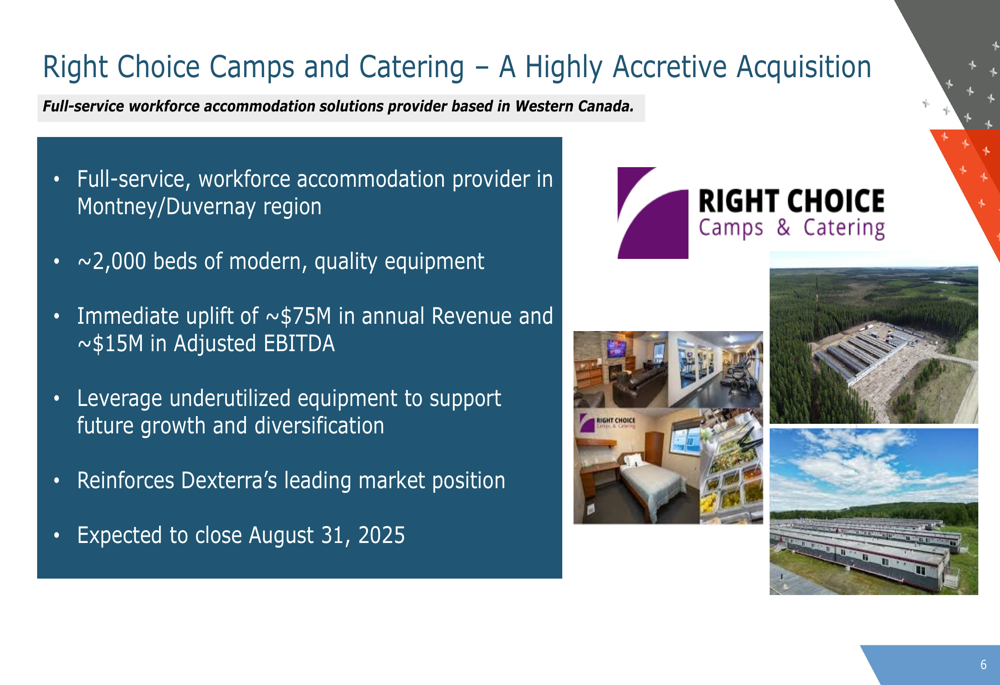

The second acquisition, described as "highly accretive," is Right Choice Camps and Catering, a full-service workforce accommodation solutions provider based in Western Canada. This acquisition is expected to add approximately $75 million in annual revenue and $15 million in adjusted EBITDA. The deal includes about 2,000 beds of modern equipment in the Montney/Duvernay region and is expected to close by August 31, 2025.

The details of this strategic Canadian expansion are shown here:

Detailed Financial Analysis

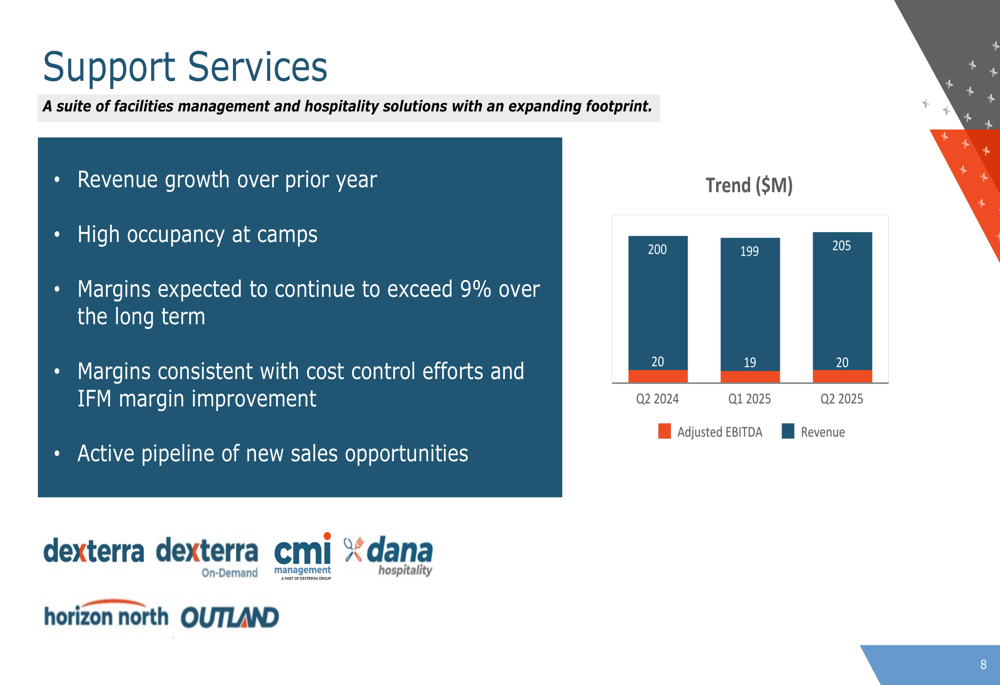

Dexterra’s financial performance showed divergent trends across its business segments. The Support Services segment posted revenue of $205 million in Q2 2025, representing a 2.5% increase from $200 million in Q2 2024 and a 3% increase from $199 million in Q1 2025. Adjusted EBITDA for this segment remained stable at $20 million.

The company noted that Support Services margins are expected to continue exceeding 9% over the long term, with consistent margins reflecting cost control efforts and integrated facilities management margin improvement.

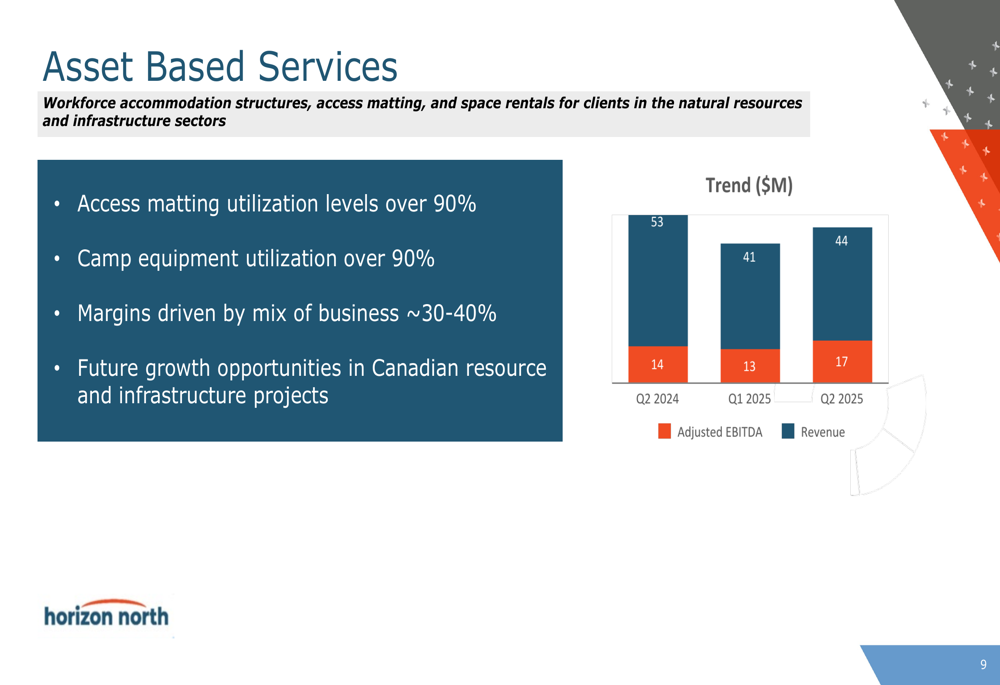

The Asset Based Services segment reported revenue of $44 million in Q2 2025, down from $53 million in Q2 2024 but up from $41 million in Q1 2025. Despite the revenue decline, adjusted EBITDA for this segment improved to $17 million in Q2 2025 from $14 million in Q2 2024 and $13 million in Q1 2025.

The company highlighted exceptionally strong utilization rates exceeding 90% for both access matting and camp equipment, driving margins of 30-40% in this segment. This performance is particularly notable given the previous quarter’s challenges.

The following charts illustrate the segment performance:

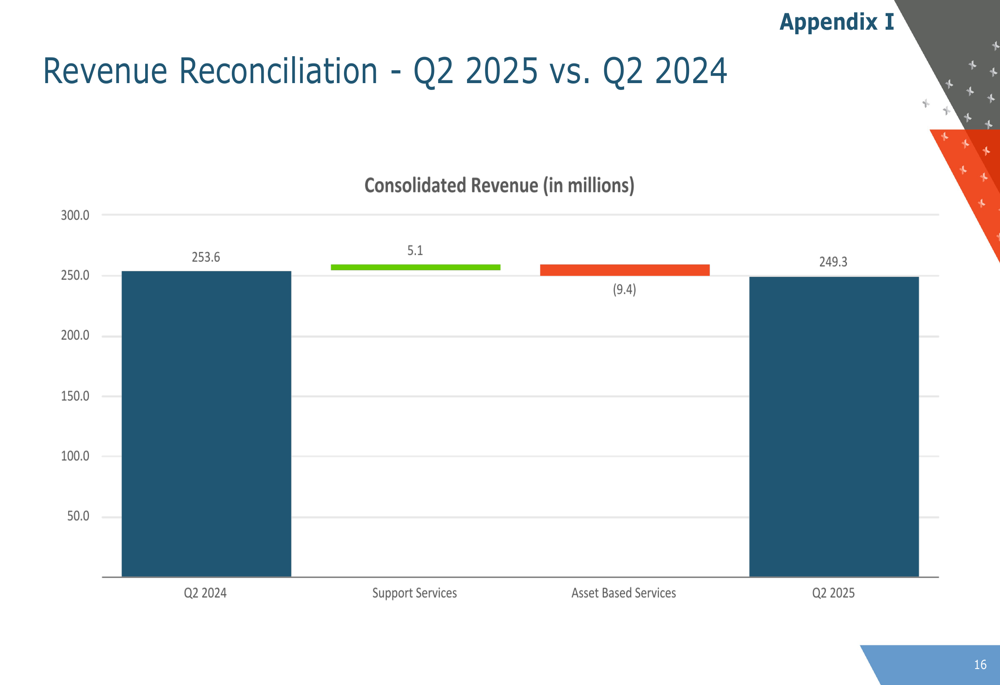

A closer look at the revenue changes between Q2 2024 and Q2 2025 reveals the specific contributions from each segment:

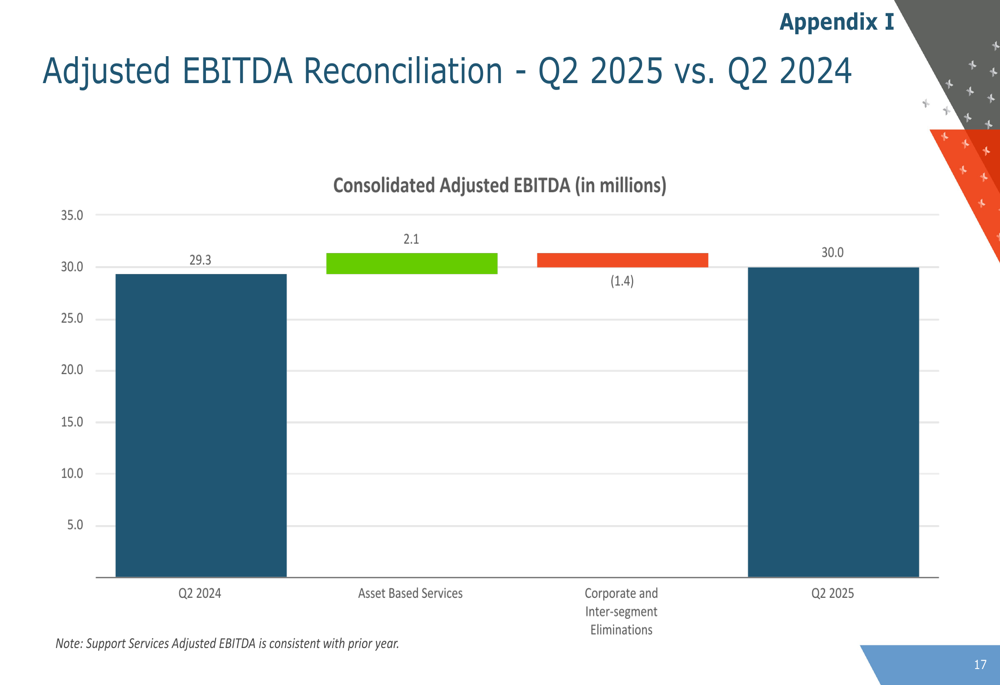

Similarly, the adjusted EBITDA reconciliation between periods provides insight into profitability drivers:

Forward-Looking Statements

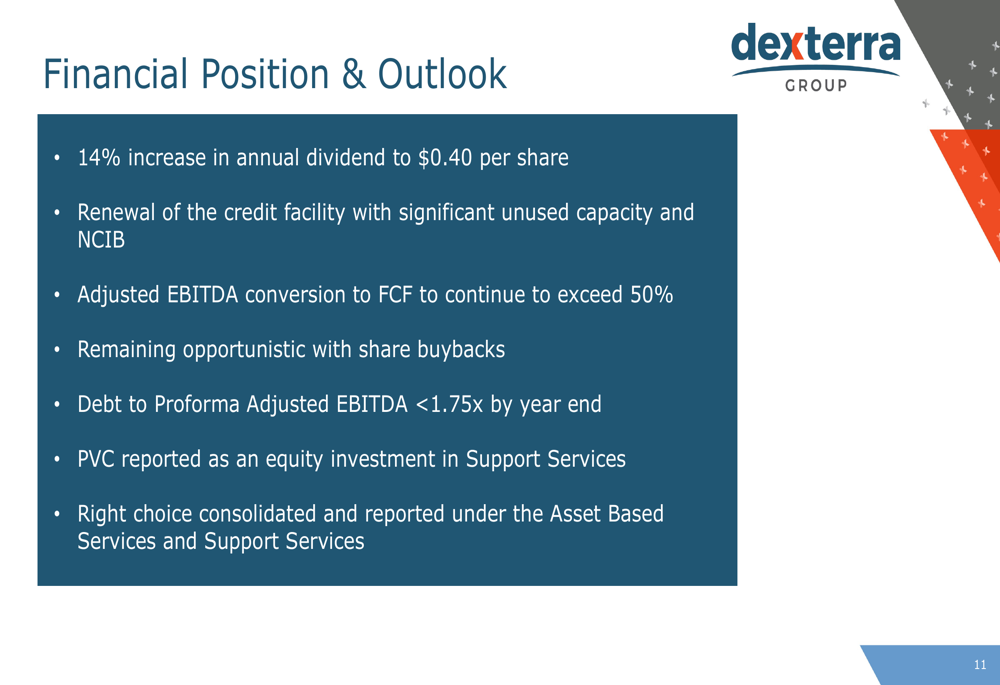

Dexterra announced a 14% increase in its annual dividend to $0.40 per share, signaling confidence in its future cash flow generation despite mixed current results. The company expects adjusted EBITDA conversion to free cash flow to continue exceeding 50% and aims to maintain a debt to proforma adjusted EBITDA ratio below 1.75x by year-end.

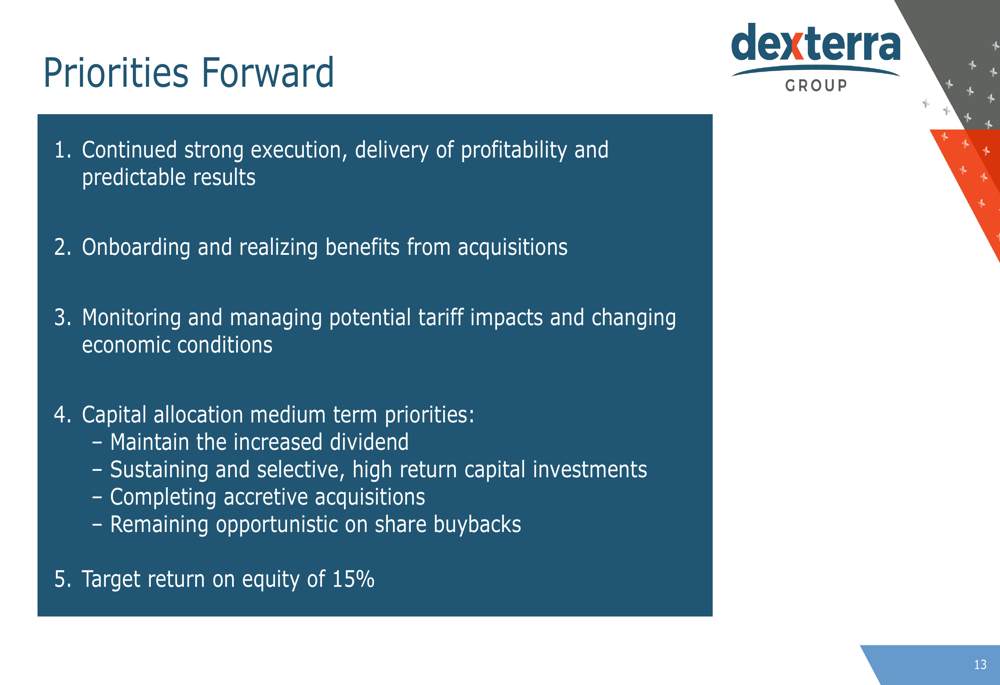

Looking ahead, Dexterra outlined several priorities, including continued strong execution, delivery of profitability and predictable results, successful onboarding and realization of benefits from the announced acquisitions, and monitoring potential tariff impacts and changing economic conditions.

The company’s financial outlook and capital allocation priorities are detailed here:

Management emphasized its medium-term capital allocation priorities, including maintaining the increased dividend, making selective high-return capital investments, completing accretive acquisitions, and remaining opportunistic with share buybacks. The target return on equity remains at 15%.

As CEO Mark Becker noted in the previous earnings call, "Our strategic focus remains the delivery of strong profitability, consistent and predictable results," a theme that continues in this quarter’s presentation despite the ongoing revenue challenges.

The company’s forward-looking priorities are summarized in this slide:

With these strategic acquisitions and financial discipline, Dexterra appears positioned to navigate the current economic environment while building platforms for future growth, though investors will be watching closely to see if revenue growth can match the company’s profitability and expansion ambitions in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.