Street Calls of the Week

Introduction & Market Context

Dominion Hosting Holding SpA (DHH) reported solid organic growth across all key performance indicators in its Q1 2025 earnings presentation on May 22. The internet infrastructure provider maintained stable margins despite inflationary pressures, while completing a strategic acquisition expected to boost future results.

DHH shares responded positively to the earnings presentation, trading up 2.51% at €20.40 as of the latest market data. The stock remains closer to its 52-week low of €19.20 than its high of €29.40, suggesting investors see potential upside from current levels following the positive quarterly report.

Quarterly Performance Highlights

DHH reported growth across all companies in its portfolio, spanning multiple geographies and business segments. The company’s diversified approach appears to be paying dividends, with particularly strong performance in its Balkan operations.

As shown in the following slide detailing growth metrics across the company’s portfolio:

Evolink achieved double-digit growth following a successful turnaround, while the company’s cloud hosting businesses in the Balkans showed robust performance with Plus growing 8%, mCloud 13%, and Webtasy 5%. Italian and Swiss operations also contributed positively, with Tophost and Artera growing 4% and 6% respectively.

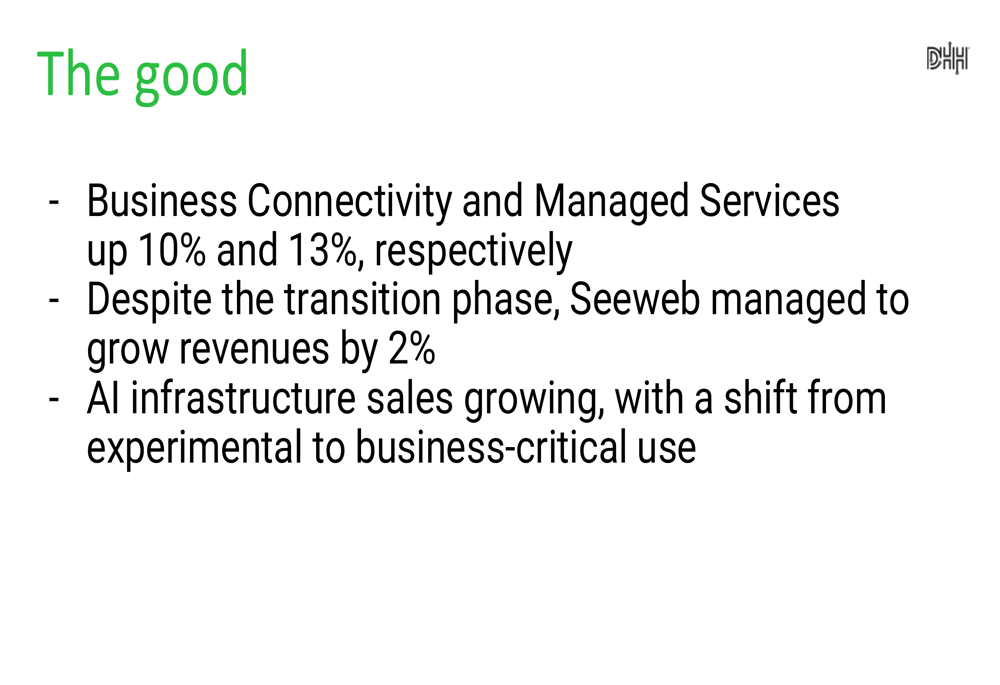

Business connectivity and managed services were standout performers, as illustrated in this highlights slide:

Business connectivity grew 10% while managed services increased by 13%. The company also noted that AI infrastructure sales are growing, with customer usage shifting from experimental to business-critical applications, though this segment still represents less than 5% of total revenue.

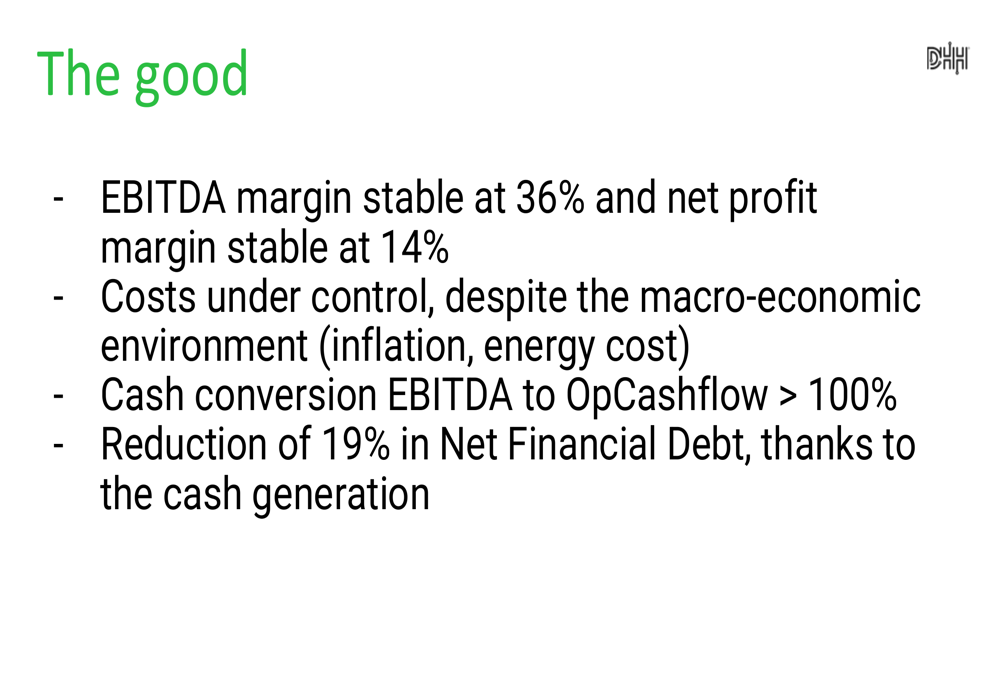

Despite cost pressures, DHH maintained strong financial metrics as shown in the following financial stability slide:

EBITDA margin remained stable at 36% while net profit margin held at 14%. The company achieved cash conversion from EBITDA to operating cash flow exceeding 100%, enabling a 19% reduction in net financial debt through strong cash generation.

Strategic Initiatives & Acquisition

A key development during the quarter was DHH’s preparation for the acquisition of Teknonet, which was completed in April 2025. Management expects this strategic move to contribute to results starting from Q2 2025, providing an additional growth driver for the remainder of the year.

The company also highlighted its ongoing investments in AI infrastructure, positioning itself to benefit from the transition of artificial intelligence applications from experimental to business-critical use cases. While AI-related revenue currently represents less than 5% of total revenue, management views this as an early-stage opportunity with significant growth potential.

Challenges & Cost Pressures

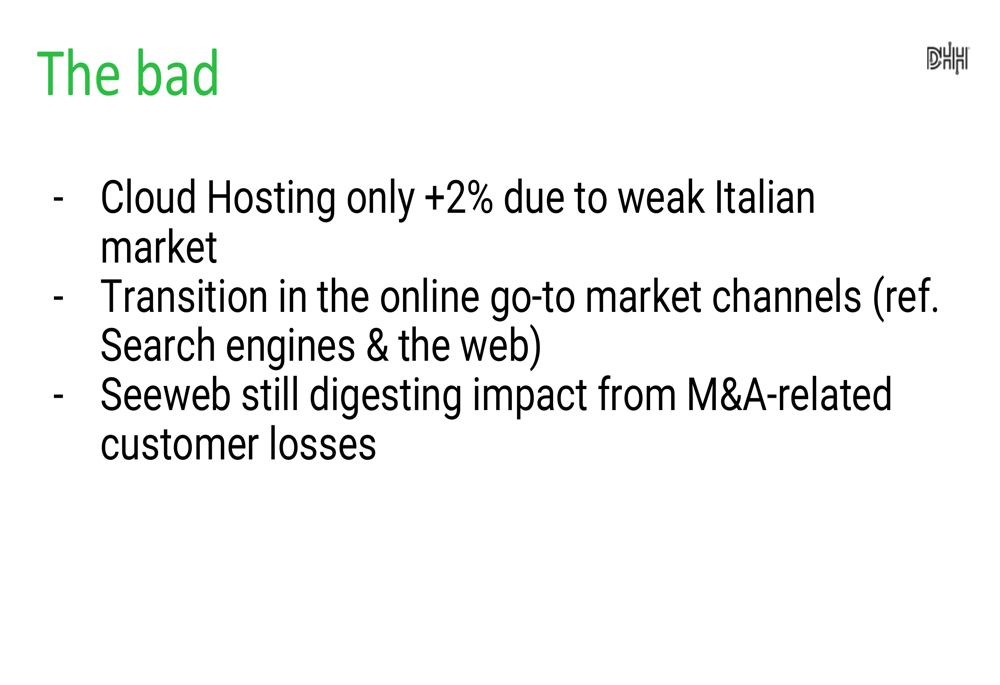

Despite the overall positive performance, DHH faced several challenges during the quarter, as outlined in the following slide:

Cloud hosting growth was limited to just 2%, which the company attributed to weakness in the Italian market. DHH also noted ongoing transition issues in its online go-to-market channels, while Seeweb continues to recover from customer losses related to previous M&A activity.

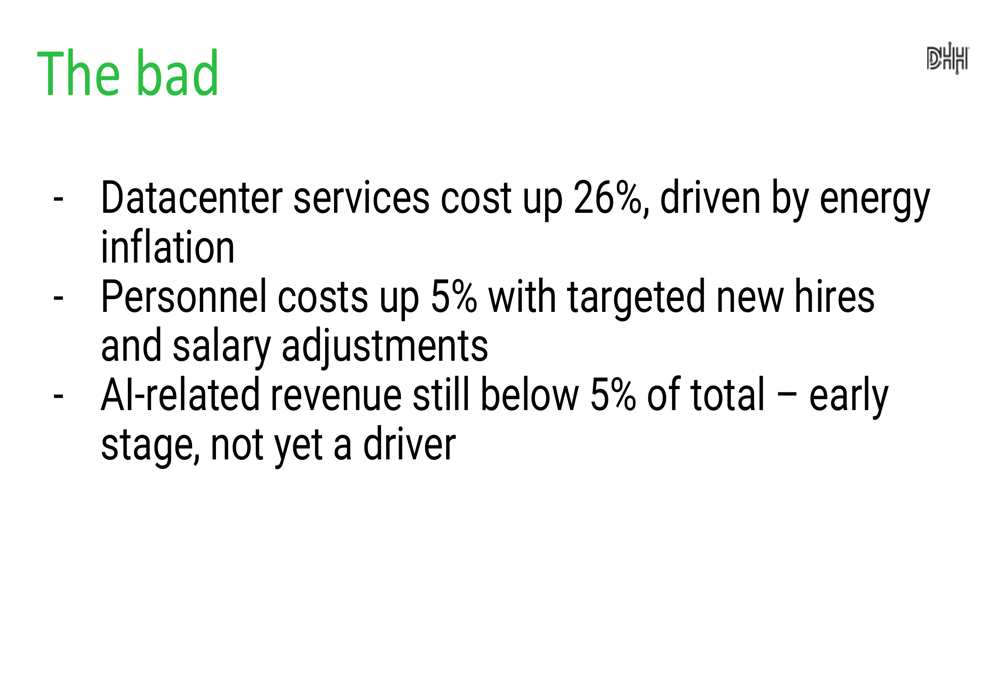

Cost pressures also presented headwinds, as detailed in this slide:

Datacenter services costs increased by 26%, primarily driven by energy inflation. Personnel costs rose 5% due to targeted new hires and salary adjustments. The company also acknowledged that AI-related revenue remains below 5% of total revenue, indicating this promising segment is still in its early stages.

Forward-Looking Statements

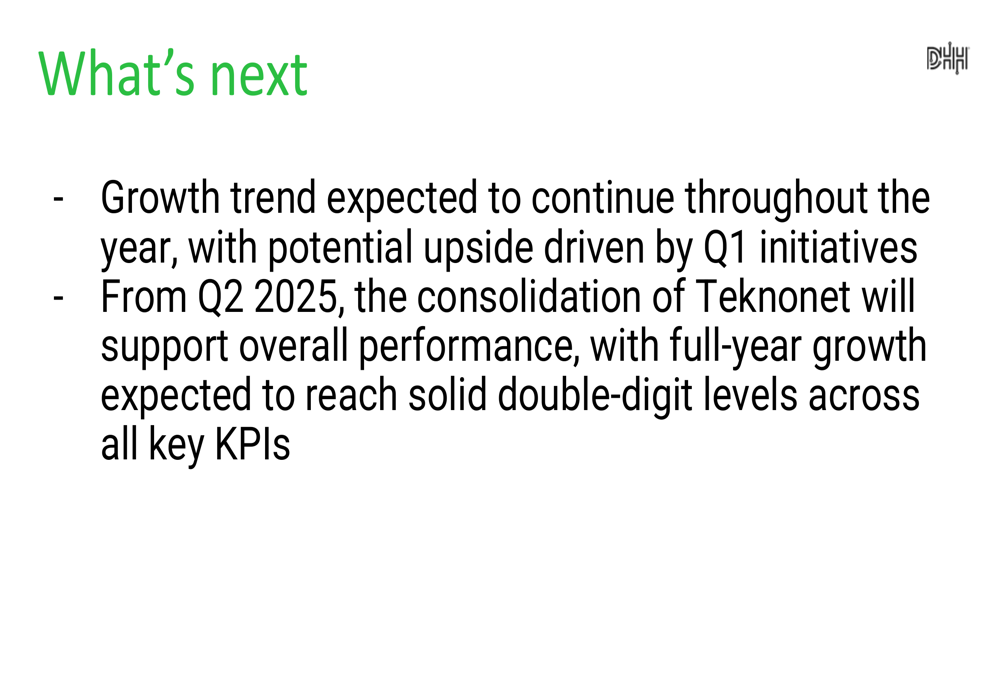

Looking ahead, DHH provided an optimistic outlook for the remainder of 2025, as shown in the following forward guidance slide:

Management expects the growth trend to continue throughout the year, with potential upside from initiatives launched in Q1. The consolidation of Teknonet from Q2 2025 is anticipated to support overall performance, with full-year growth projected to reach "solid double-digit levels" across all key performance indicators.

DHH’s balanced presentation of both achievements and challenges suggests a realistic assessment of its market position. While energy costs and regional market weaknesses present ongoing challenges, the company’s geographic diversification, strategic acquisition, and emerging AI capabilities position it for continued growth in the internet infrastructure sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.