Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Dollarama Inc (TSX:DOL) shared its Q2-FY2026 investor presentation on August 27, 2025, highlighting continued strong financial performance and ambitious global expansion plans. The Canadian value retailer reported 10.3% sales growth for the quarter while maintaining industry-leading margins and accelerating its international footprint.

Introduction & Market Context

Dollarama continues to strengthen its position as a leading value retailer in Canada with growing international operations. The company’s stock has performed well in 2025, trading near its 52-week high of $198.66, despite a slight 0.51% decline to $192.07 in the most recent session on August 26.

Building on its strong Q1-FY26 performance, when the stock surged 9.38% following better-than-expected results, Dollarama’s Q2 presentation reinforces the company’s growth trajectory and operational efficiency in a challenging retail environment.

Quarterly Performance Highlights

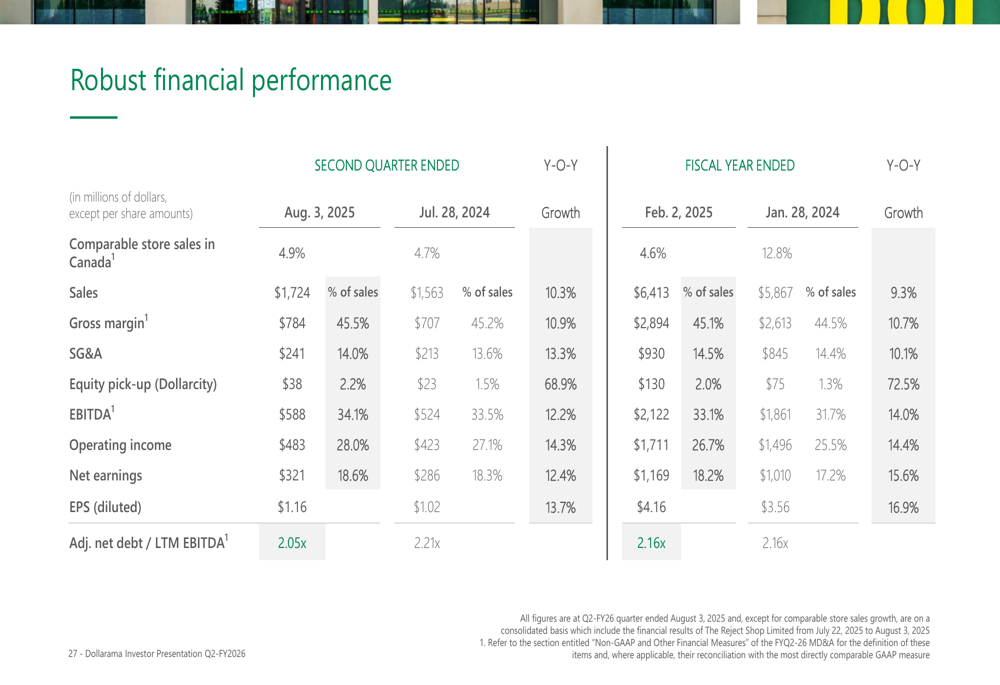

For Q2-FY26, Dollarama reported sales of $1,724 million, representing a 10.3% increase compared to the same period last year. The company maintained strong profitability with a gross margin of 45.5% (up 10.9%), EBITDA margin of 34.1% (up 12.2%), and net earnings growth of 12.4% year-over-year.

As shown in the following financial performance summary:

On a last twelve months (LTM) basis, Dollarama achieved $6.7 billion in revenues with 9.5% sales growth and 4.5% comparable store sales growth in Canada. The company generated $2.3 billion in EBITDA (34.0% of sales) and $0.8 billion in free cash flow.

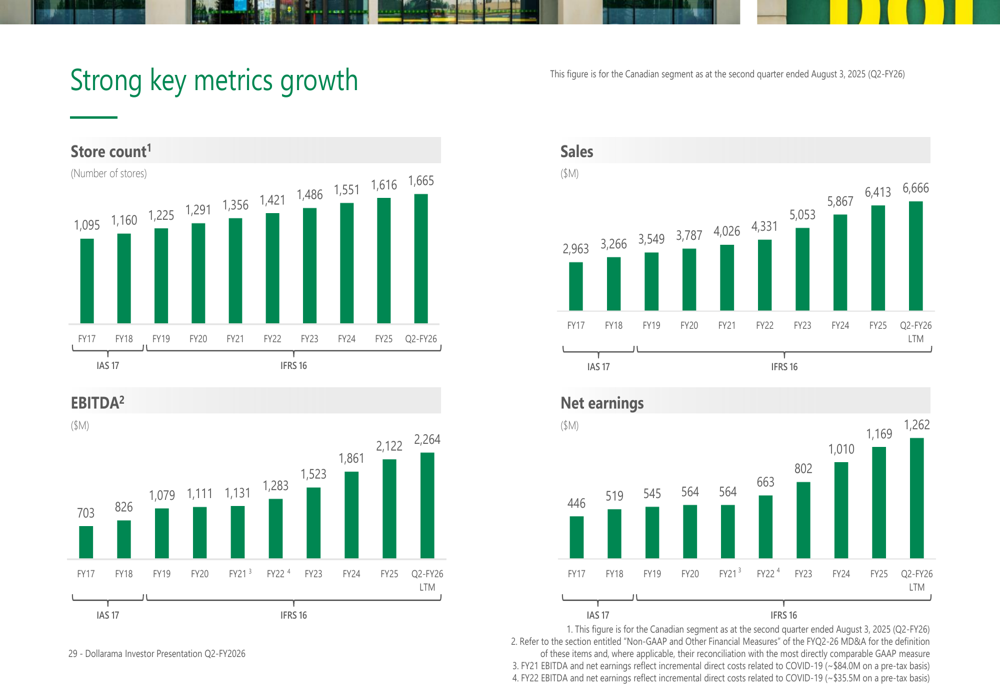

The company’s growth trajectory remains impressive, with consistent increases in store count, sales, EBITDA, and net earnings over recent years:

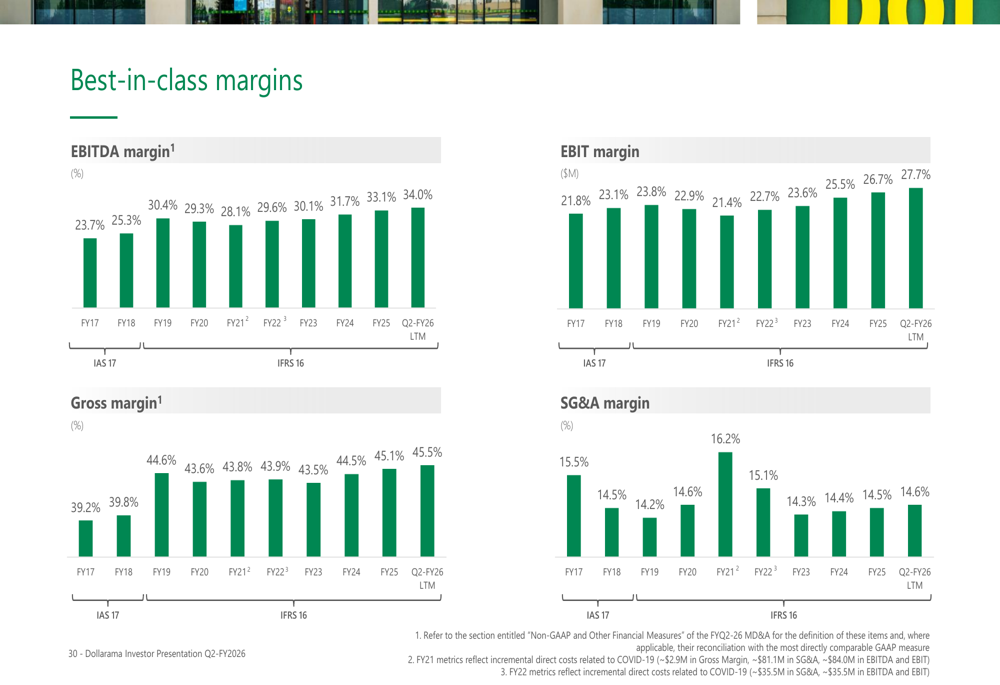

Dollarama continues to maintain industry-leading profit margins, with EBITDA margins now at 34%:

Strategic Initiatives

Dollarama outlined a four-pillar strategy for sustainable growth: profitably growing its Canadian footprint, scaling up Dollarcity business in Latin America, optimizing and accelerating growth in Australia, and optimizing capital allocation to drive returns.

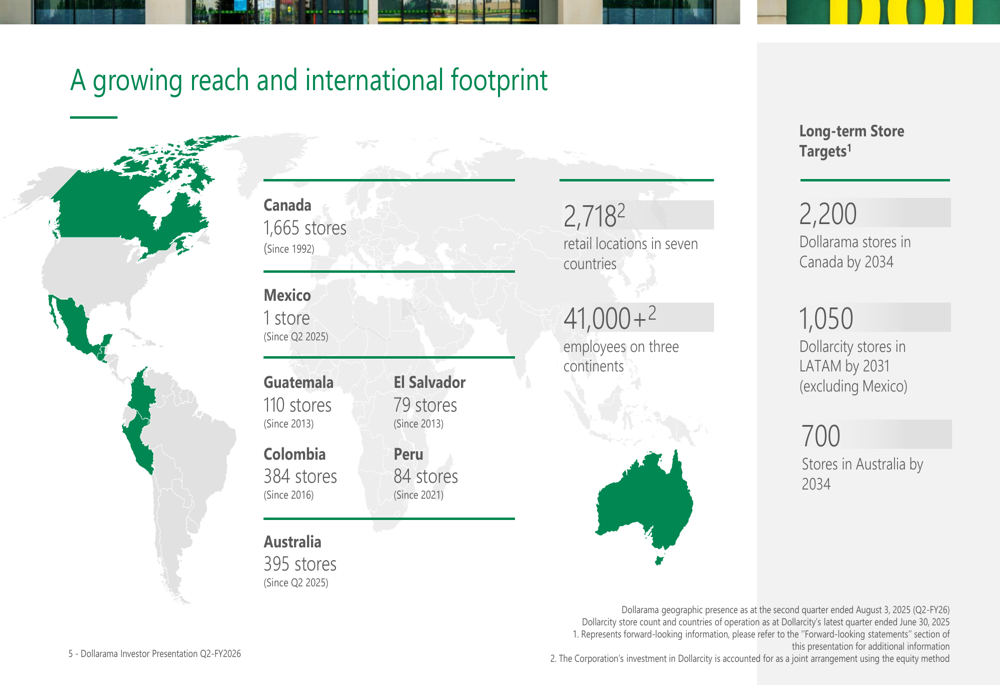

The company’s global reach now spans 2,718 retail locations across seven countries on three continents, with 41,000+ employees worldwide. This international footprint is illustrated in the following map:

In Canada, Dollarama operates 1,665 stores and has set an ambitious target of 2,200 stores by 2034. The company’s efficient network growth model features an average investment of ~$920,000 per new store with a payback period of approximately two years, demonstrating strong capital efficiency.

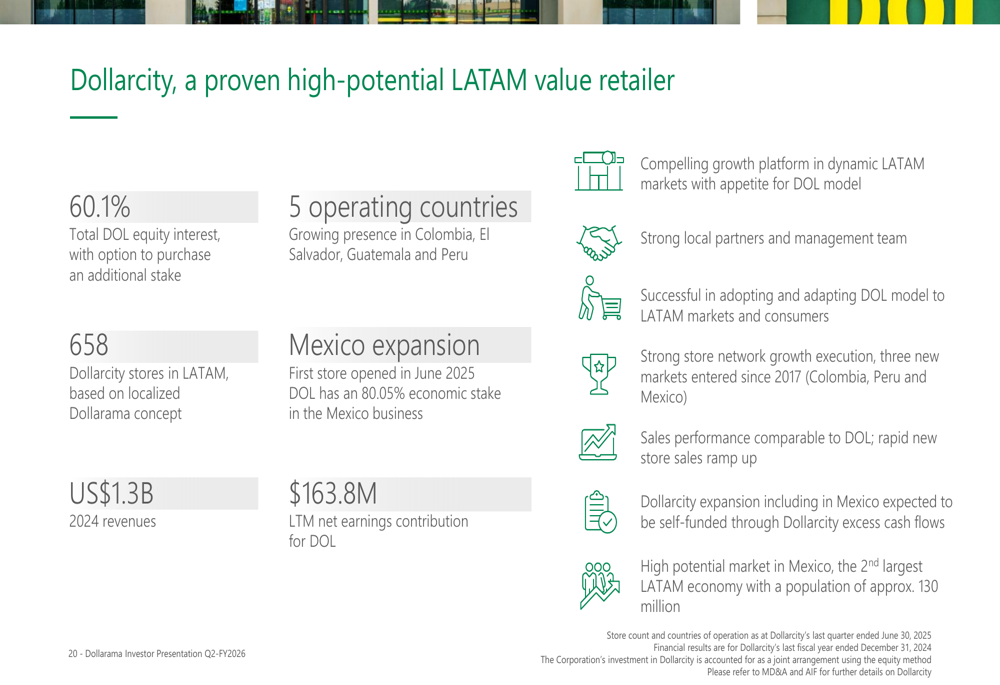

Internationally, Dollarama holds a 60.1% equity interest in Dollarcity, which operates 658 stores across Latin America. Dollarcity contributed $163.8 million in LTM net earnings to Dollarama and has a long-term target of 1,050 stores by 2031. The company is also expanding into Mexico, though management acknowledged in their Q1 earnings call that this initiative may incur initial losses over the next 1-2 years.

In Australia, Dollarama operates 395 stores with annual sales of A$866 million in 2024. The company has set a target of 700 Australian stores by 2034, focusing on merchandising strategy, operational excellence, store experience, and accelerated network growth.

Detailed Financial Analysis

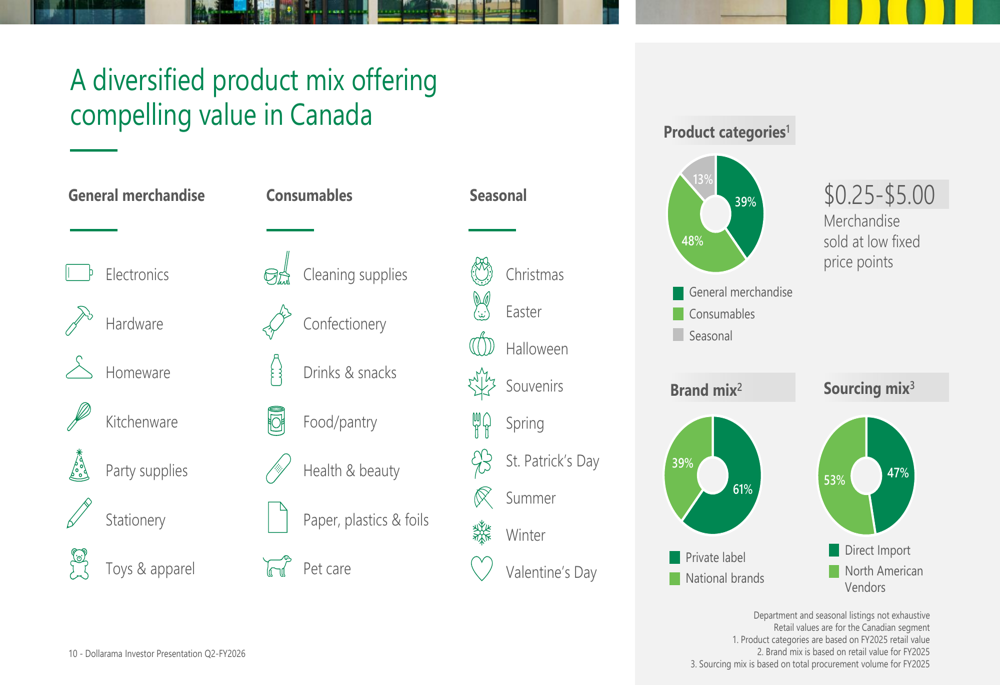

Dollarama’s business model continues to deliver strong financial results. The company maintains a diversified product mix in Canada, with General Merchandise (48%), Consumables (39%), and Seasonal items (13%) sold at fixed price points ranging from $0.25 to $5.00:

The company’s capital allocation strategy balances investments in organic growth with returning capital to shareholders. Since FY13, Dollarama has returned approximately $7.6 billion to shareholders through share repurchases and an additional $781 million in dividends since FY12:

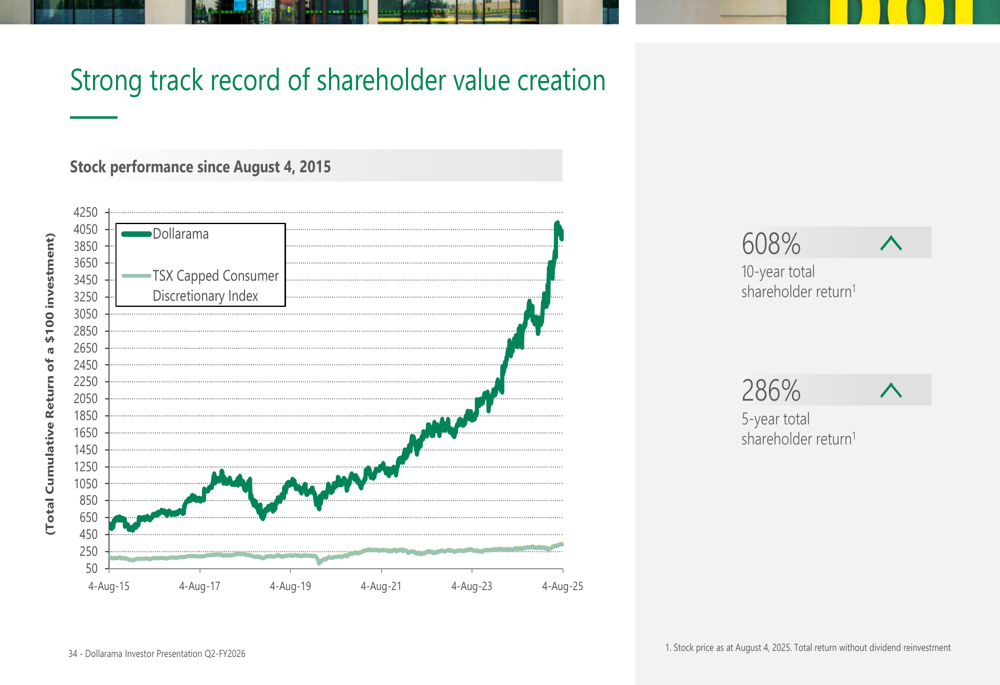

This approach has generated exceptional returns for long-term investors, with a 10-year total shareholder return of 608% and a 5-year return of 286%:

Dollarama maintains a prudent capital structure with 89% fixed-rate debt, $1,764 million in available liquidity, a weighted average cost of debt of 3.49%, and a leverage ratio of 2.05x. The company holds investment-grade BBB credit ratings.

Forward-Looking Statements

Looking ahead, Dollarama remains focused on executing its multi-year growth strategy across all markets. The company’s long-term store targets (2,200 in Canada, 1,050 in Latin America, and 700 in Australia by 2034) represent significant growth potential from the current 2,718 locations.

The company is also enhancing its customer experience through digital initiatives, including partnerships with third-party delivery platforms such as Instacart, Uber Eats, DoorDash, and Skip. This aligns with consumer trends toward convenience and omnichannel shopping experiences.

On the sustainability front, Dollarama highlighted its MSCI AA rating as of August 2025 and various ESG initiatives, including enhanced human rights risk management, first Scope 3 emissions quantification, and multiple decarbonization projects.

While the presentation maintains an optimistic outlook, investors should note management’s acknowledgment during the Q1 earnings call of "consumer fragility" in the current economic environment, though increased store traffic was cited as a positive indicator. The company’s value proposition positions it well to navigate potential economic headwinds as consumers seek affordable shopping options.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.