Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Dolphin Drilling AS (EURONEXT:DDRIL) presented its first half 2025 results on August 29, highlighting the company’s return to positive EBITDA territory while navigating persistent financial challenges. The offshore drilling contractor, which operates three semi-submersible rigs, has positioned itself in the growing moored semi-submersible market segment, with operations in the UK and India.

The company’s stock price currently sits at NOK 0.01, significantly below its 52-week high of NOK 4.50, reflecting ongoing investor concerns despite operational improvements.

Executive Summary

Dolphin Drilling reported EBITDA of USD 10.4 million for the first half of 2025, a marked improvement from the USD 23.2 million loss recorded in the same period of 2024. This turnaround was primarily driven by having two rigs on contract throughout the period, with the Paul B Loyd Junior and Blackford Dolphin achieving utilization rates of 97.6% and 86.3%, respectively.

As shown in the following highlights from the presentation:

Despite the positive EBITDA, the company still reported a net loss of USD 34.4 million for the period, impacted by depreciation, interest expenses, and a significant tax claim loss related to HMRC. The company’s cash position declined to USD 21.8 million, while net debt stood at USD 59.7 million.

A key development during the period was the completion of a comprehensive refinancing package, which included USD 29 million in equity and USD 28.7 million in loans, extending debt maturities to 2027 and providing additional financial runway.

Quarterly Performance Highlights

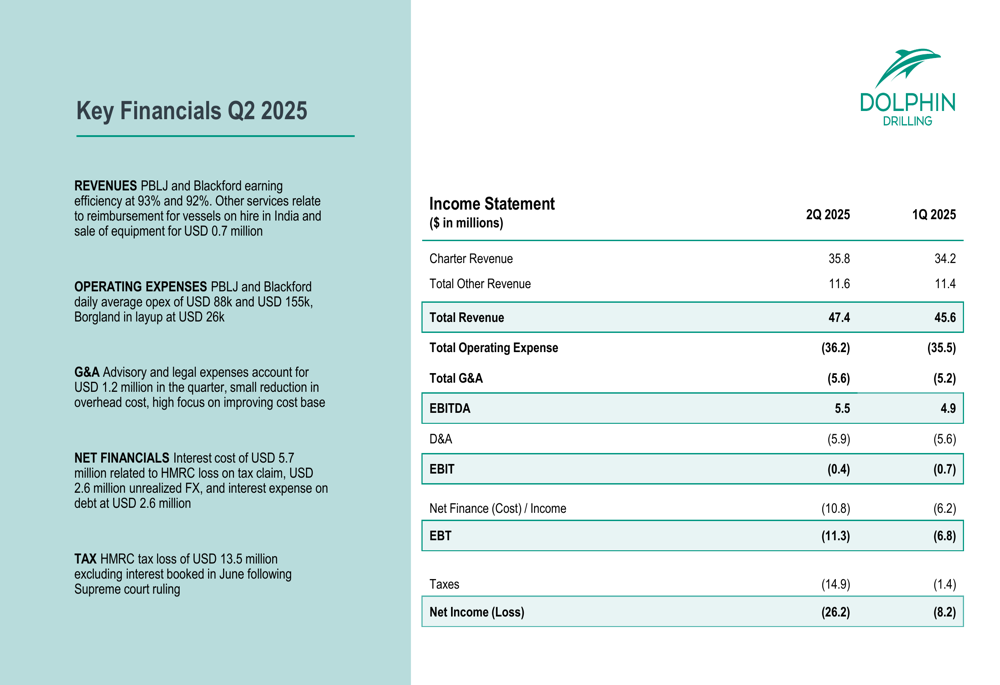

In Q2 2025, Dolphin Drilling reported revenue of USD 47.4 million, slightly up from USD 45.6 million in Q1. EBITDA for the quarter reached USD 5.5 million, compared to USD 4.9 million in the previous quarter. However, the company recorded a substantial net loss of USD 26.2 million in Q2, significantly higher than the USD 8.2 million loss in Q1, primarily due to a USD 13.5 million tax loss related to an HMRC claim.

The detailed quarterly financials are presented below:

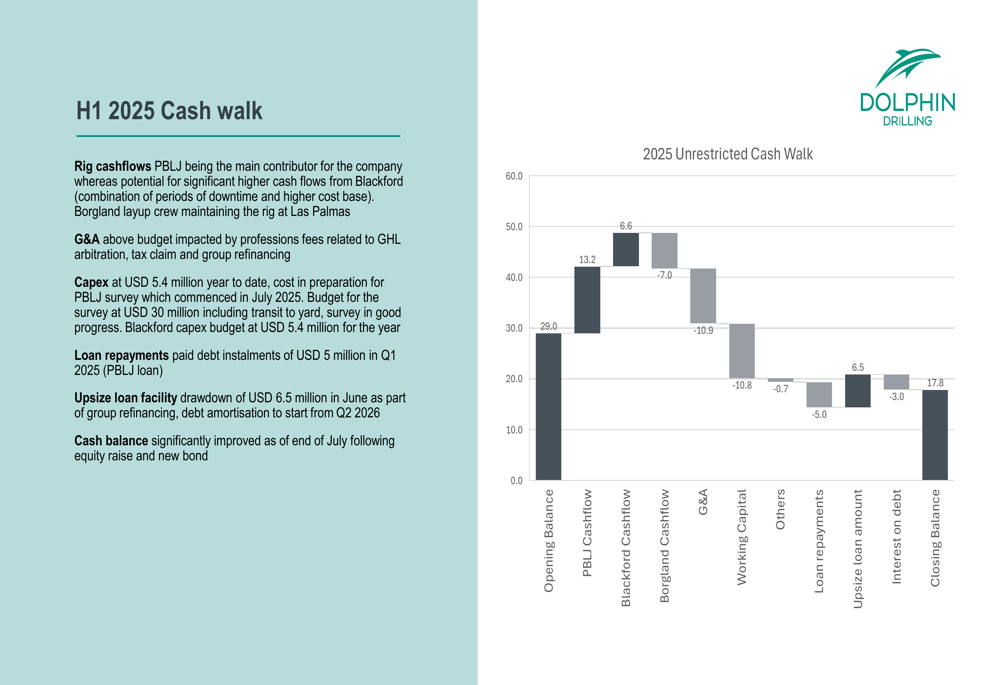

The company’s cash position continued to decline during the first half of 2025, dropping from USD 29.0 million at the end of 2024 to USD 17.8 million by the end of Q2 2025. This cash walk illustrates the primary factors affecting the company’s liquidity:

While the Paul B Loyd Junior and Blackford Dolphin rigs generated positive cash flows of USD 13.2 million and USD 6.6 million respectively, these were offset by the idle Borgland Dolphin’s negative cash flow of USD 7.0 million and general administrative expenses of USD 10.9 million.

Detailed Financial Analysis

Dolphin Drilling’s balance sheet as of June 2025 showed total assets of USD 179.5 million, down from USD 196.3 million at the end of 2024. The company’s shareholders’ equity declined significantly to USD 12.4 million from USD 42.0 million, reflecting the continued losses.

The refinancing completed during the period has provided some breathing room for the company, extending debt maturities until Q3 2027 and strengthening the balance sheet. The refinancing package included:

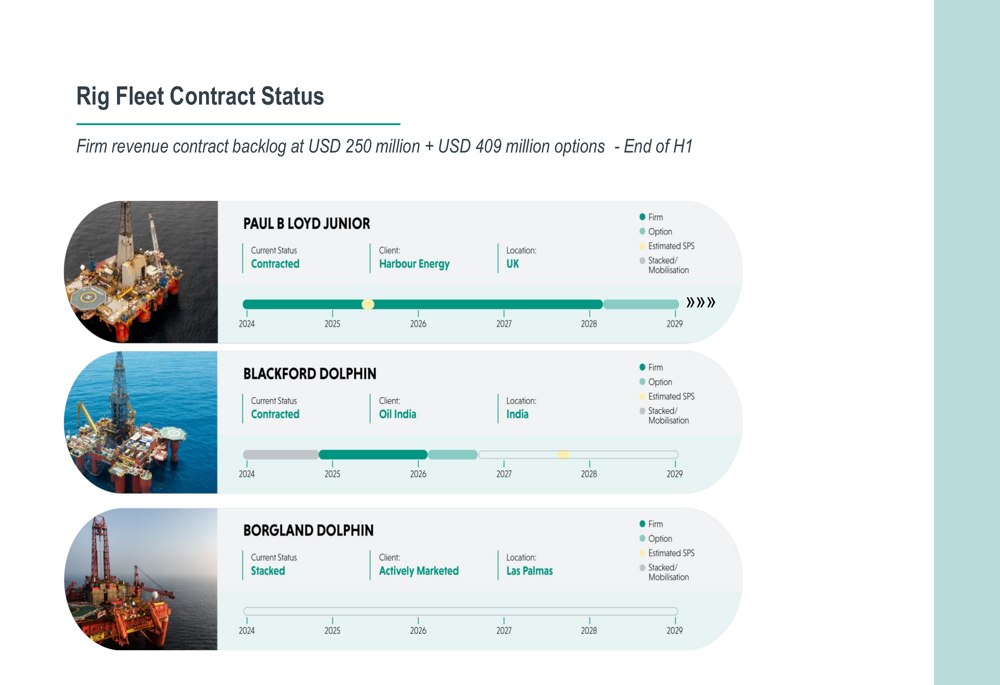

The company’s contract backlog provides some revenue visibility, with firm contracts worth USD 250 million and additional options valued at USD 409 million. The Paul B Loyd Junior is contracted to Harbour Energy in the UK until 2027, with options extending to 2029, while the Blackford Dolphin is working for Oil India until 2026, with options to 2029.

The current status of the rig fleet is illustrated below:

The idle Borgland Dolphin remains a financial drag, incurring daily operating expenses of USD 26,000 while generating no revenue. Management continues to actively market this rig from its current location in Las Palmas.

Strategic Initiatives & Outlook

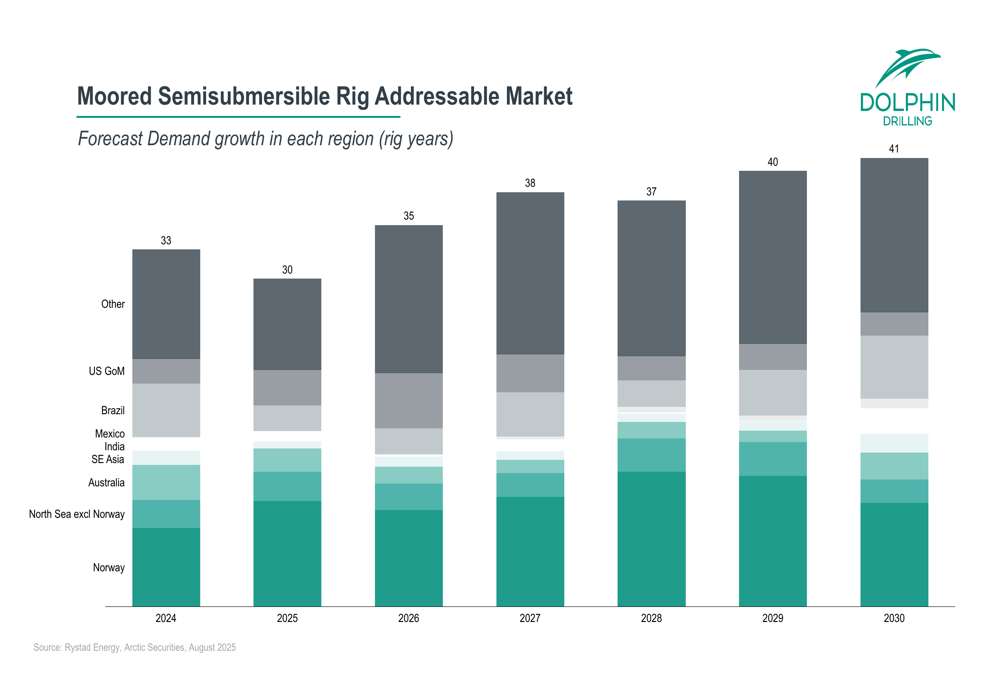

Dolphin Drilling operates in a market that is projected to see growing demand for moored semi-submersible rigs over the coming years. According to the company’s market analysis, demand is expected to increase from approximately 30 rig years in 2025 to 41 rig years by 2030:

This projected market growth could provide opportunities for the company to secure a contract for its idle Borgland Dolphin rig and potentially improve its financial performance.

The company’s strategic focus remains on improving operational uptime and reducing costs while leveraging its contracted assets. Management highlighted the significant potential of its operational platform:

With its debt now refinanced and extended until 2027, Dolphin Drilling has gained valuable time to execute its turnaround strategy. However, the continued cash burn and substantial net losses underscore the challenges ahead. The company’s ability to secure a contract for the Borgland Dolphin and further improve the operational efficiency of its working rigs will be crucial for achieving sustainable profitability and reversing the negative cash flow trend.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.