US stock futures steady with China trade talks, Q3 earnings in focus

Introduction & Market Context

Donegal Group Inc. (NASDAQ:DGICA) presented its second quarter 2025 financial results on July 24, showcasing significant profitability improvements despite a modest decline in premiums. The regional property and casualty insurer, which operates across Mid-Atlantic, Midwestern, Southern, and Southwestern states, reported a dramatic 306.1% increase in net income compared to the same period last year.

The company’s stock closed at $18.52 on July 23, up 1.09% for the day and continuing a positive trend that began after its strong Q1 2025 performance. With shares trading near their 52-week high of $21.12, investors appear to be responding favorably to Donegal’s strategic shift toward commercial lines and improved underwriting results.

Quarterly Performance Highlights

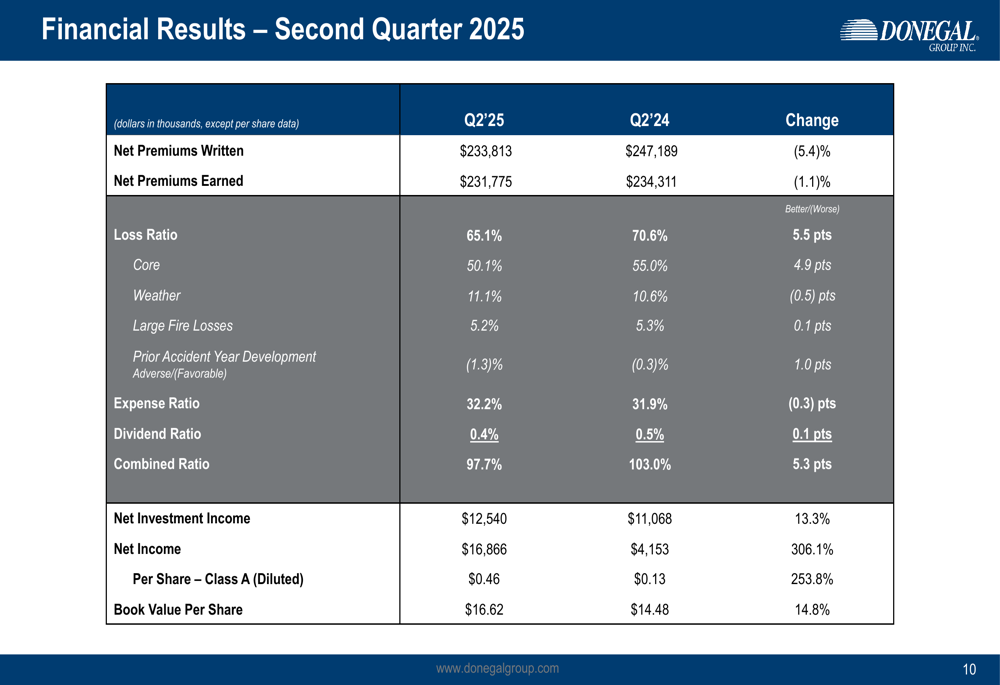

Donegal reported Q2 2025 net income of $16.9 million, or $0.46 per diluted Class A share, compared to just $4.2 million, or $0.13 per share, in Q2 2024. While this represents a sequential decline from the exceptional $0.72 EPS reported in Q1 2025, it still marks substantial year-over-year improvement.

The company’s combined ratio improved to 97.7% from 103.0% in the prior-year quarter, driven primarily by a 5.5 percentage point improvement in the loss ratio to 65.1%. This improvement occurred despite a slight 0.3 percentage point increase in the expense ratio to 32.2%.

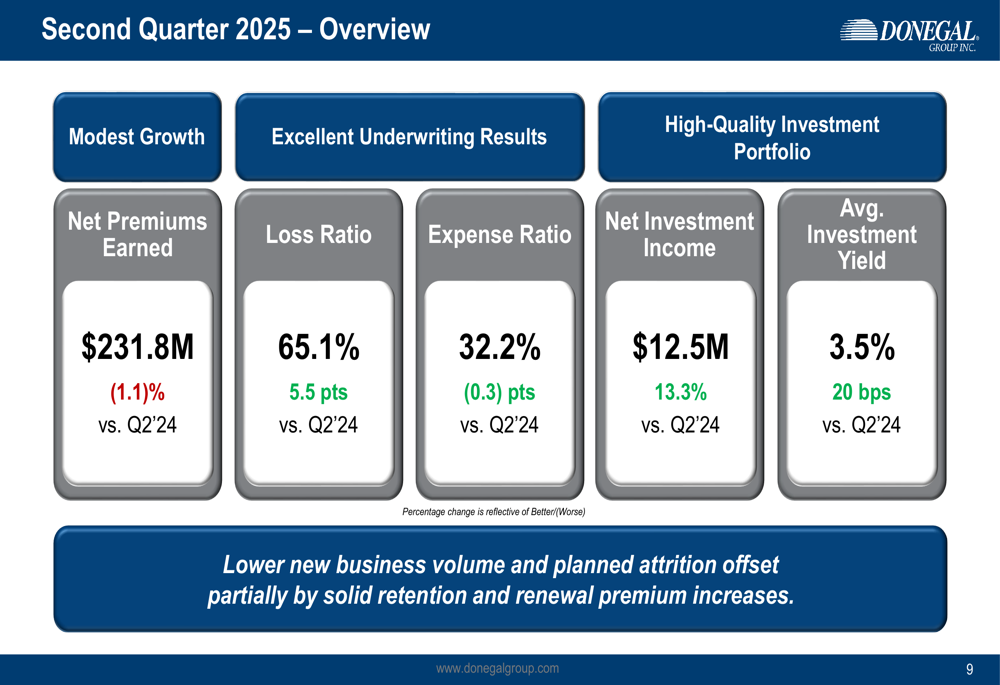

As shown in the following quarterly overview:

Net premiums earned decreased slightly by 1.1% to $231.8 million, while net investment income increased by 13.3% to $12.5 million. The average investment yield improved by 20 basis points to 3.5%. The company attributed the premium decline to lower new business volume and planned attrition, partially offset by solid retention and renewal premium increases.

Strategic Initiatives

Donegal continues to execute its strategic shift toward commercial lines while optimizing its personal lines portfolio. Commercial lines now represent 58% of net premiums written, while personal lines account for 42%, as illustrated in the following breakdown:

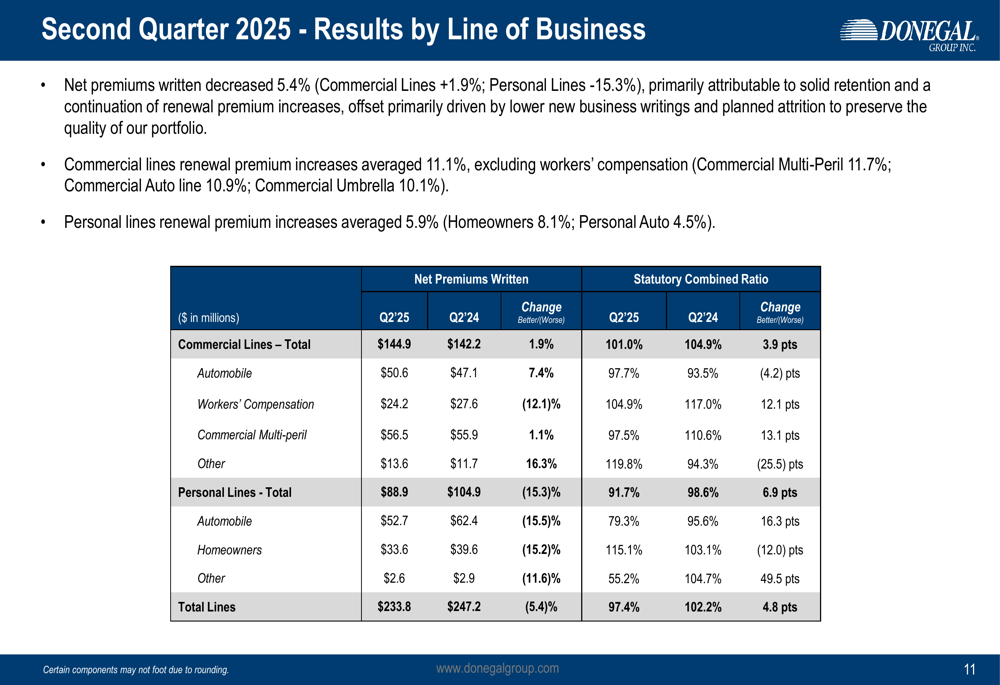

The company’s emphasis on commercial lines growth is evident in both its retention metrics and premium trends. Commercial lines net premiums written increased by 1.9% to $144.9 million, while personal lines decreased by 15.3% to $88.9 million. This reduction in personal lines reflects intentional underwriting actions to non-renew underperforming accounts and classes of business.

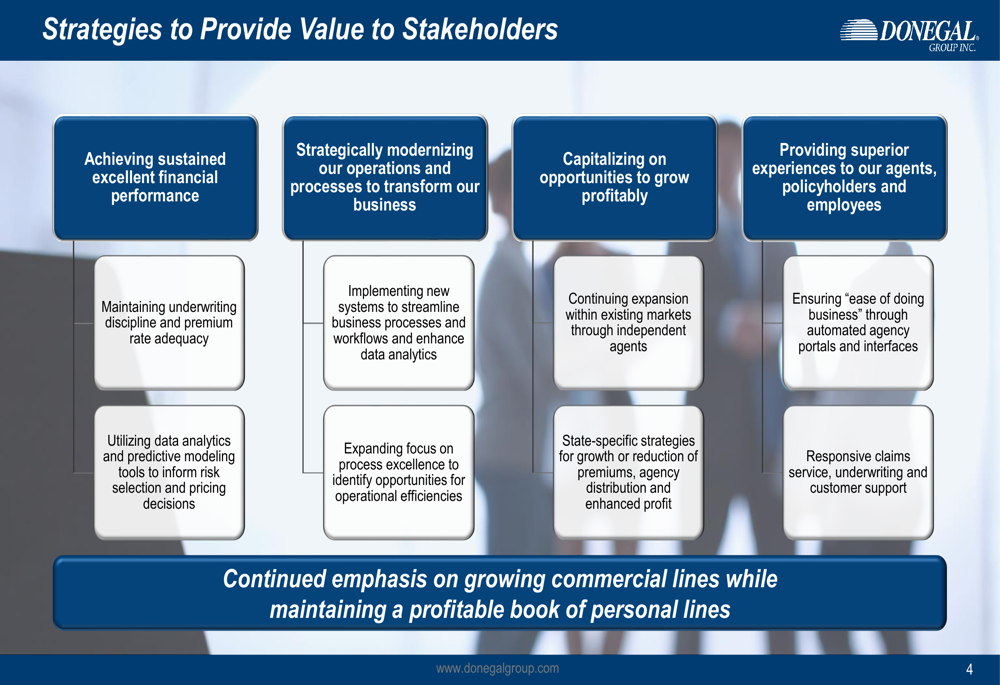

Donegal outlined four key strategic priorities to provide value to stakeholders:

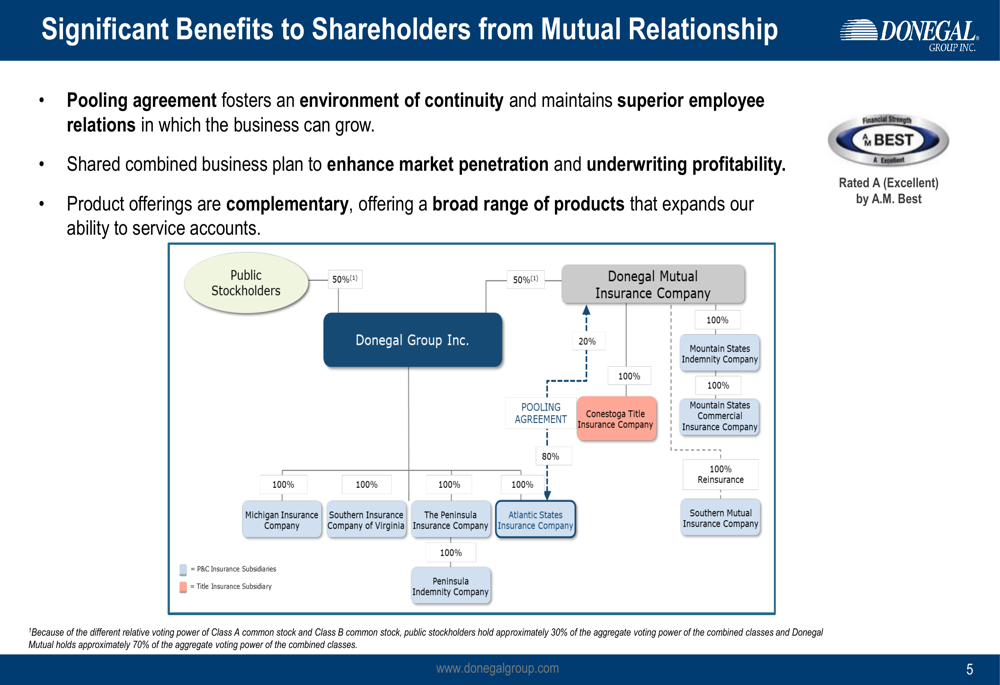

The company’s mutual relationship structure provides significant benefits to shareholders, including a pooling agreement that fosters continuity, a shared business plan to enhance market penetration and underwriting profitability, and complementary product offerings:

Detailed Financial Analysis

A closer examination of Donegal’s Q2 2025 financial results reveals significant improvements across multiple metrics compared to Q2 2024:

By line of business, commercial lines showed a combined ratio of 101.0%, an improvement of 3.9 percentage points from Q2 2024. Personal lines performed even better with a combined ratio of 91.7%, improving by 6.9 percentage points. The detailed breakdown by product line shows varied performance:

Commercial auto and workers’ compensation showed notable improvements, while the "other" commercial category deteriorated. In personal lines, automobile showed dramatic improvement with a combined ratio of 79.3%, while homeowners deteriorated to 115.1%.

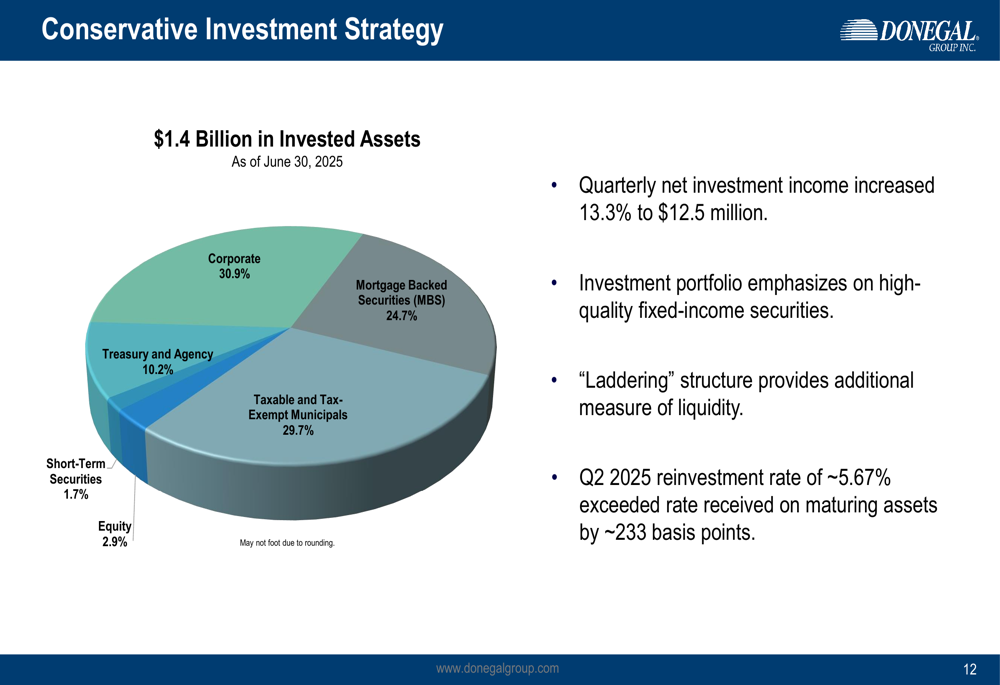

Donegal maintains a conservative investment strategy, with a $1.4 billion portfolio heavily weighted toward high-quality fixed-income securities:

The company’s quarterly net investment income increased 13.3% to $12.5 million, benefiting from a favorable reinvestment rate of approximately 5.67%, which exceeded the rate received on maturing assets by 233 basis points.

Competitive Positioning

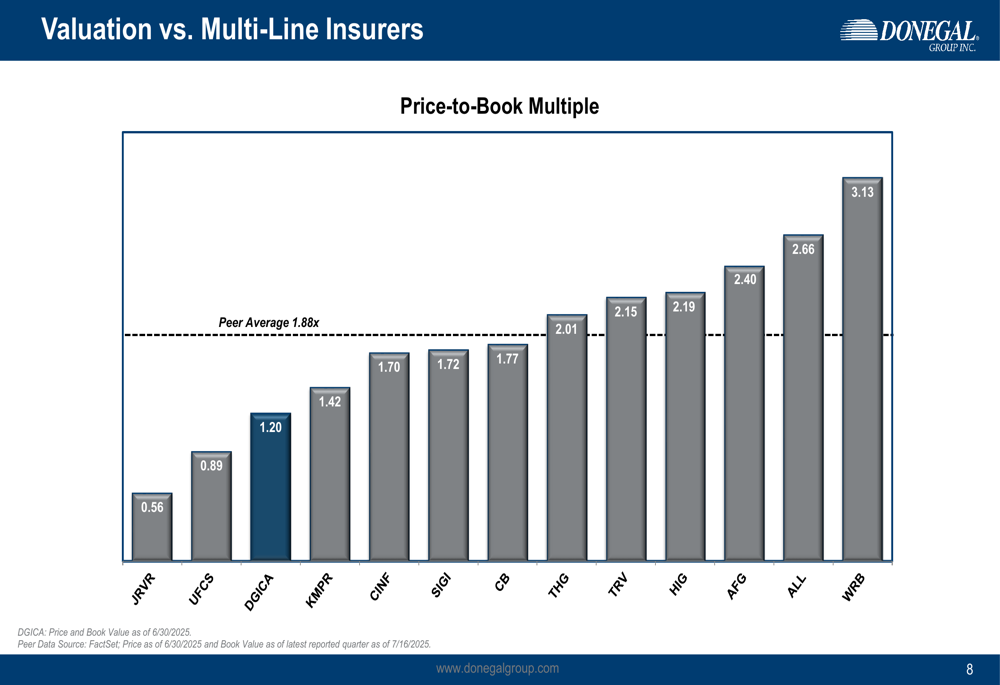

Donegal’s price-to-book multiple of 1.20 remains below the peer average of 1.88x, suggesting potential undervaluation relative to other multi-line insurers:

This valuation gap persists despite the company’s improved profitability and strategic initiatives. Donegal maintains an A (Excellent) rating from A.M. Best, reflecting its strong financial position and operational stability.

Forward-Looking Statements

Looking ahead, Donegal Group is focused on continuing its strategic modernization of operations and processes while capitalizing on opportunities to grow profitably, particularly in commercial lines. The company plans to maintain its disciplined approach to underwriting and pricing, with emphasis on achieving sustained excellent financial performance.

Management expects renewal premium increases to continue, with commercial lines renewal premiums averaging 11.1% increases (excluding workers’ compensation) and personal lines averaging 5.9% increases. These rate actions, combined with ongoing portfolio optimization efforts, are expected to support improved underwriting results going forward.

The company’s investment thesis centers on its established regional presence, diverse book of business, ongoing optimization of business mix with emphasis on commercial lines, and focus on maintaining highly responsive service levels to agents, policyholders, and employees.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.