Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

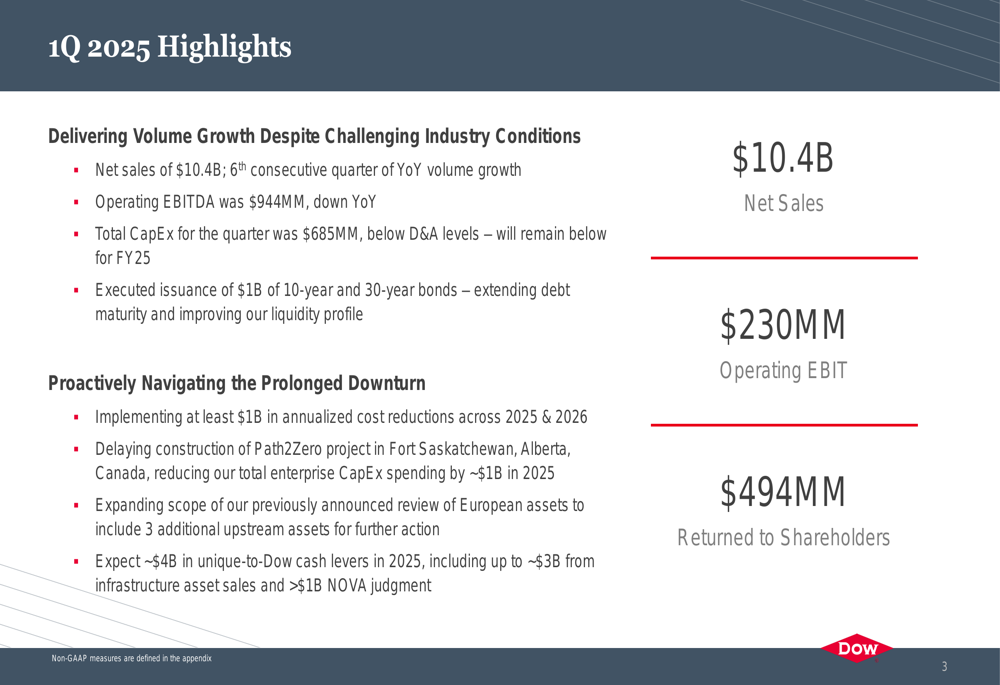

Dow Inc (NYSE:DOW) unveiled its first quarter 2025 results on April 24, revealing a strategic shift toward aggressive cost-cutting measures amid persistent industry headwinds. Despite achieving its sixth consecutive quarter of year-over-year volume growth, the chemical giant faces significant margin pressure in key segments, prompting a comprehensive plan to preserve financial flexibility.

The company reported net sales of $10.4 billion for Q1 2025, with operating EBITDA of $944 million, down from the year-ago period. In response to these challenging conditions, Dow announced plans to implement at least $1 billion in annualized cost reductions across 2025 and 2026, while delaying major capital projects.

As shown in the following summary of Q1 2025 highlights:

Quarterly Performance Highlights

Dow’s performance across its three operating segments revealed mixed results, with volume growth offset by margin compression in two divisions. The company returned $494 million to shareholders during the quarter while executing a $1 billion issuance of 10-year and 30-year bonds.

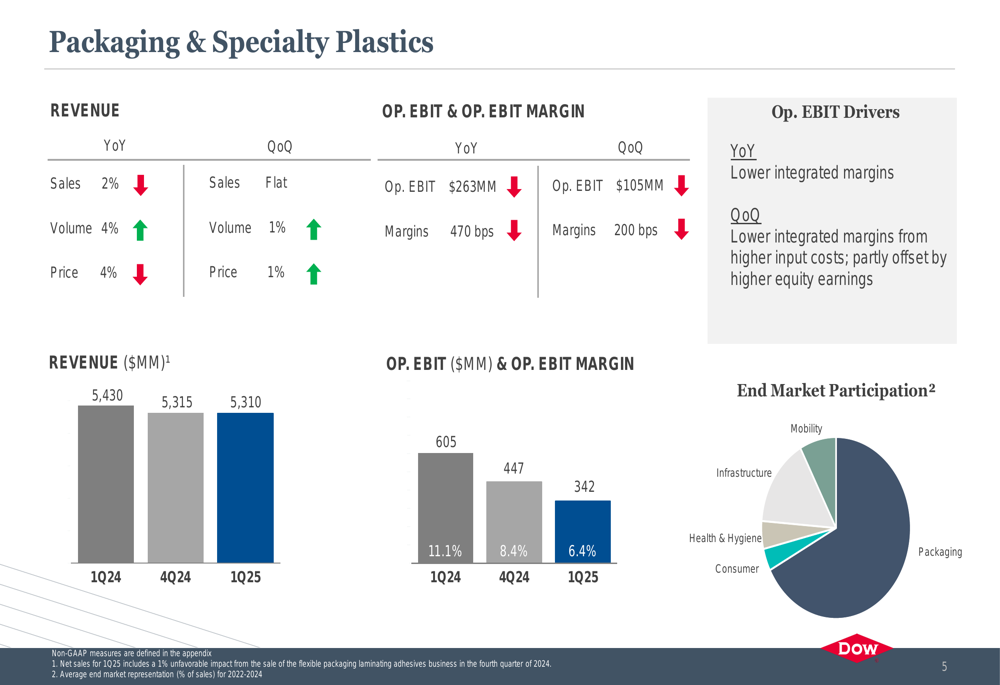

The Packaging (NYSE:PKG) & Specialty Plastics segment, Dow’s largest business unit, reported sales of $5.31 billion, down 2% year-over-year but flat quarter-over-quarter. While volume increased 4% year-over-year, operating EBIT margin declined 470 basis points to 6.4%, primarily due to lower integrated margins.

As illustrated in the segment performance breakdown:

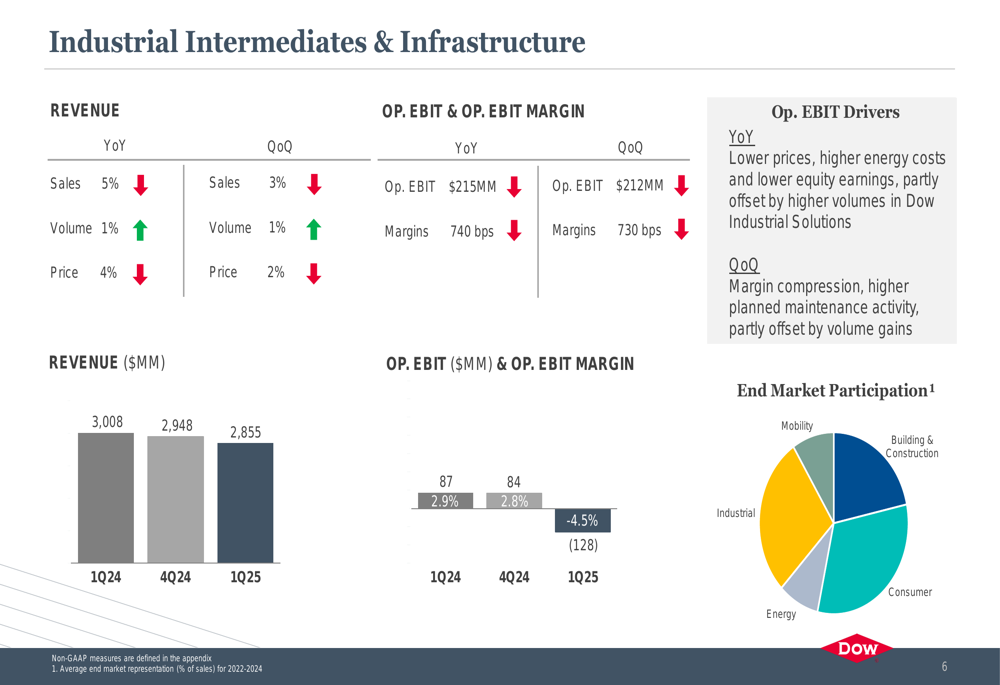

The Industrial Intermediates & Infrastructure segment faced the most significant challenges, with an operating EBIT margin of -4.5%, representing a 740 basis point decline year-over-year. Despite a 5% increase in sales to $2.86 billion, the segment struggled with lower prices, higher energy costs, and reduced equity earnings.

The segment’s performance details show the extent of the margin pressure:

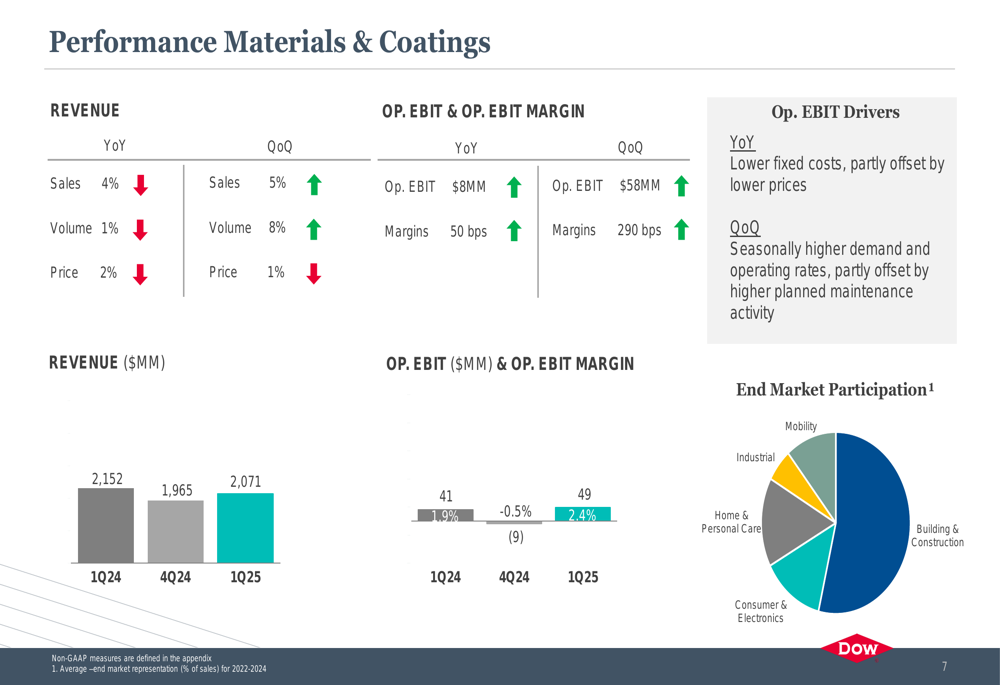

In contrast, Performance Materials & Coatings showed modest improvement, with sales increasing 4% year-over-year to $2.07 billion and operating EBIT margin expanding by 50 basis points to 2.4%. The segment benefited from lower fixed costs and seasonally higher demand.

The detailed breakdown of this segment’s performance:

Strategic Initiatives

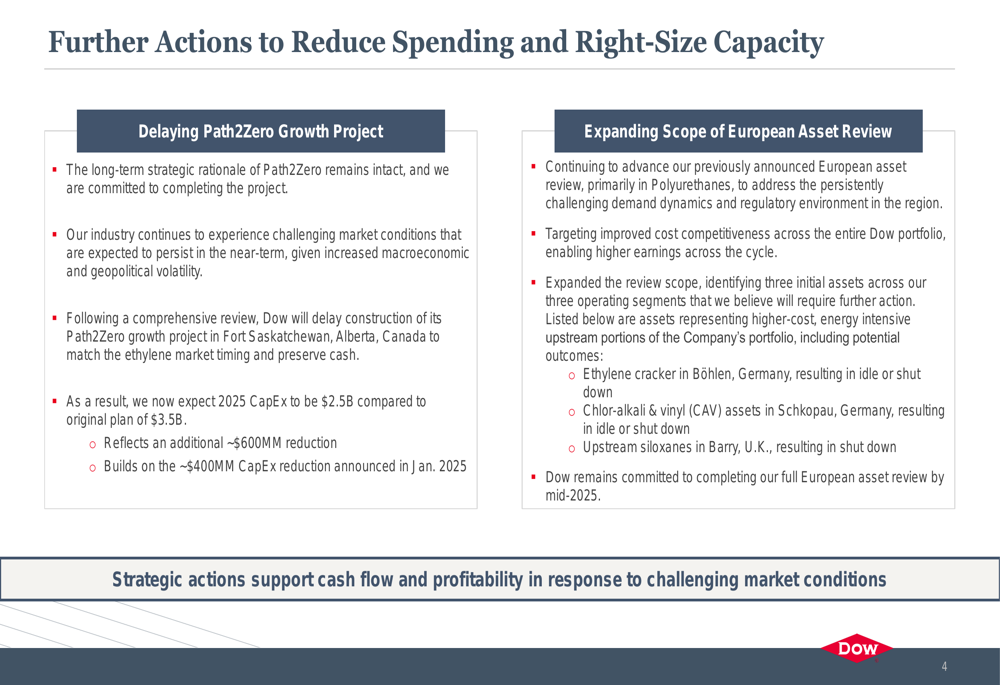

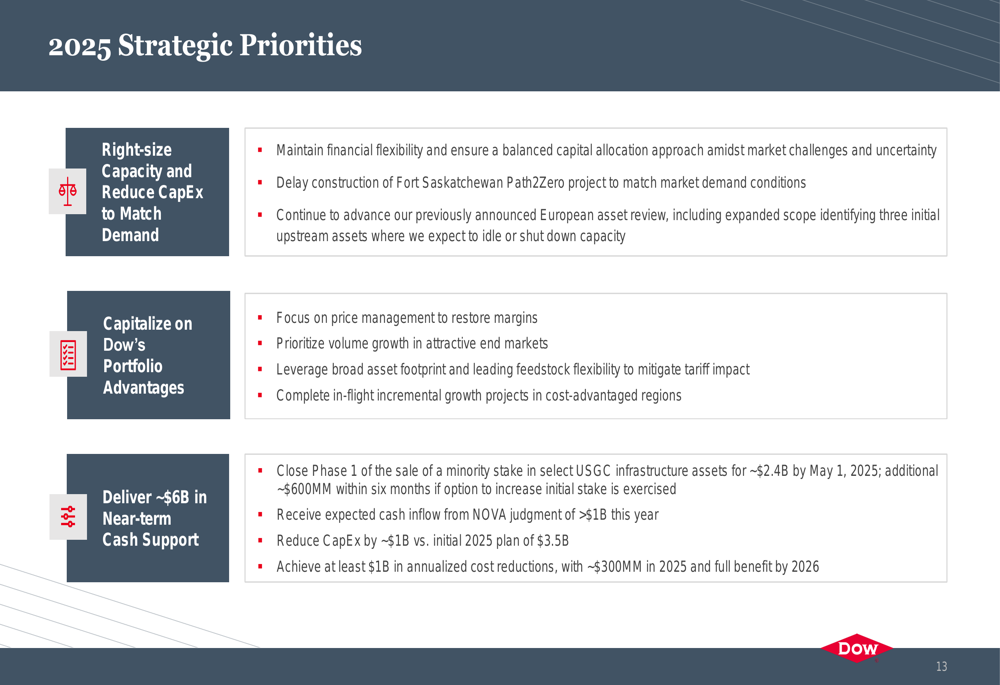

In response to the prolonged industry downturn, Dow announced several strategic initiatives aimed at preserving cash and enhancing financial flexibility. Most notably, the company is delaying construction of its Path2Zero growth project in Fort Saskatchewan, Alberta, Canada, which will reduce total enterprise capital expenditure by approximately $1 billion in 2025.

The company’s capital spending plan now targets $2.5 billion for 2025, down from the original plan of $3.5 billion. Management emphasized that the long-term strategic rationale for the project remains intact, but timing is being adjusted to match market conditions.

As detailed in the following slide on spending reduction actions:

Additionally, Dow is expanding the scope of its previously announced European asset review, primarily in Polyurethanes, with three initial assets identified for potential restructuring. The company remains committed to completing the full European asset review by mid-2025.

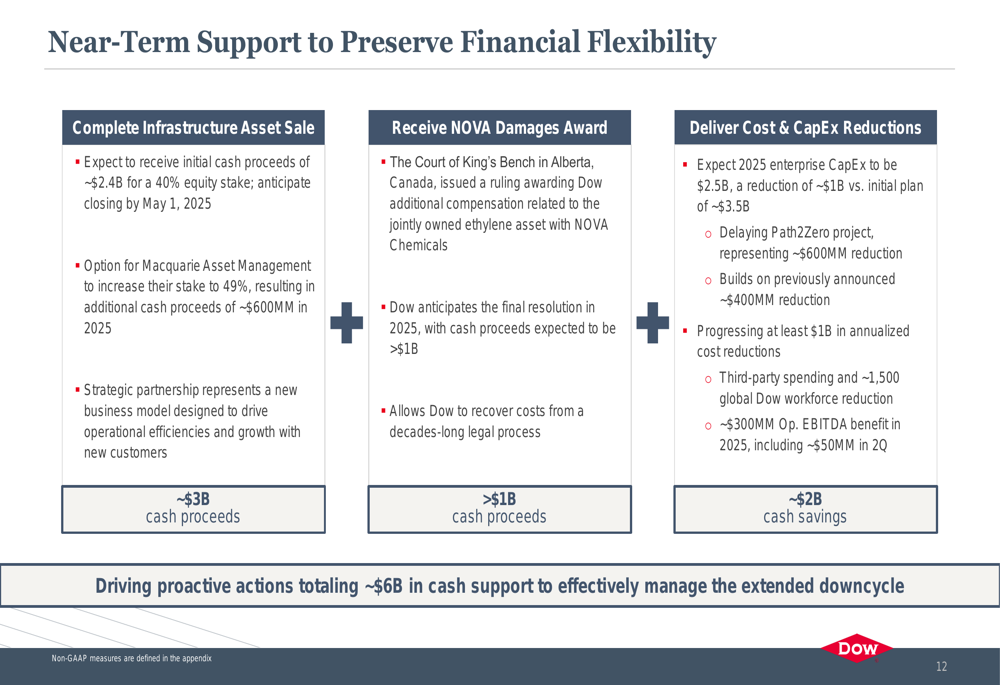

Dow expects to generate approximately $6 billion in near-term cash support through various initiatives, including the completion of an infrastructure asset sale expected to yield about $3 billion, receipt of a NOVA damages award exceeding $1 billion, and the delivery of cost and capital expenditure reductions totaling around $2 billion.

The company’s near-term financial support strategy is illustrated here:

Competitive Industry Position

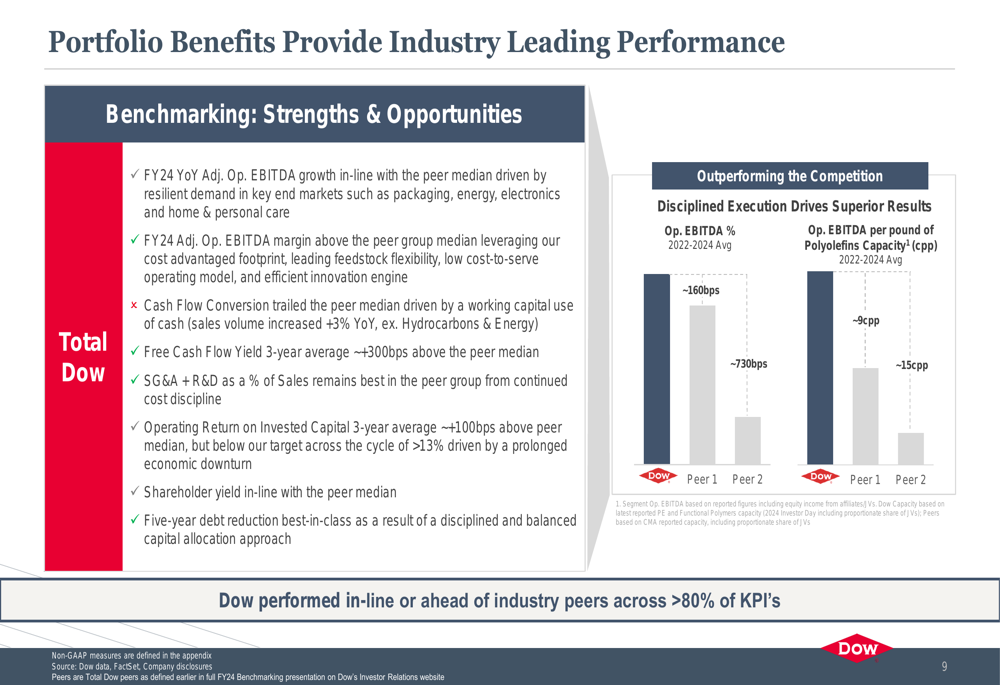

Despite current challenges, Dow highlighted its competitive advantages, including a strategic global asset footprint and industry-leading feedstock flexibility. The company emphasized its ability to mitigate against direct tariff impacts and volatile feedstock environments through its diversified portfolio.

Dow’s benchmarking against peers showed fiscal year 2024 adjusted operating EBITDA margin above the peer group median, while its SG&A and R&D expenses as a percentage of sales remain best-in-class. The company’s three-year average operating return on invested capital is approximately 100 basis points above the peer median.

The following slide illustrates Dow’s competitive positioning:

Forward-Looking Statements

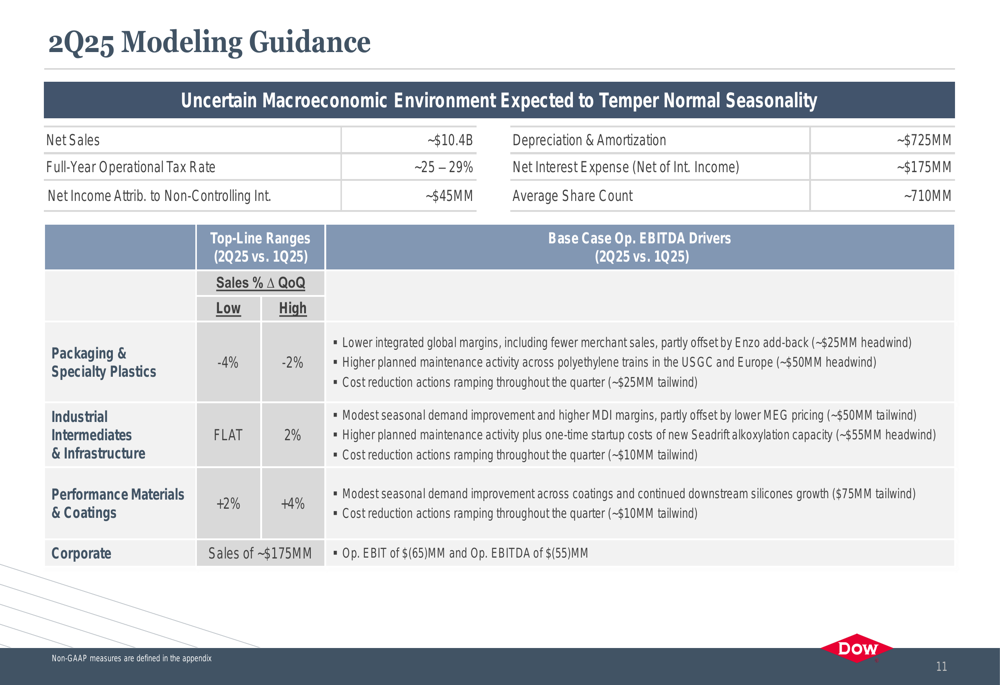

Looking ahead to the second quarter of 2025, Dow expects net sales to remain steady at approximately $10.4 billion, with the uncertain macroeconomic environment tempering normal seasonality. The company projects a full-year operational tax rate of 25-29% and average share count of approximately 710 million.

For 2025, Dow outlined three strategic priorities: right-sizing capacity and reducing capital expenditure to match demand, capitalizing on portfolio advantages, and delivering approximately $6 billion in near-term cash support. The company remains focused on price management to restore margins while prioritizing volume growth in attractive end markets.

The detailed Q2 2025 modeling guidance provides further insight into expected performance:

The company’s 2025 strategic priorities framework demonstrates its comprehensive approach to navigating current market conditions:

Dow’s premarket trading on April 24 showed positive momentum, with shares up 2.1% to $29.61, suggesting cautious investor optimism about the company’s strategic direction despite ongoing industry challenges. The stock has traded between $25.06 and $60.19 over the past 52 weeks, reflecting the volatile operating environment.

As the chemical industry continues to face headwinds from slower global growth and increasing macroeconomic uncertainty, Dow’s focus on cost discipline, portfolio optimization, and financial flexibility positions the company to weather the current downturn while maintaining its competitive advantages for an eventual market recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.