Oil prices steady near 1-mth high on US-Iran sanctions; OPEC+ meeting awaited

Introduction & Market Context

Drilling Tools International Corp (NASDAQ:DTI) released its Summer 2025 investor presentation, highlighting the company’s strategic growth initiatives and financial performance. The presentation comes as DTI’s stock has faced pressure, currently trading at $2.75 after a recent 4.96% gain, but still significantly below its 52-week high of $6.36.

The oilfield services provider emphasized its expanding global footprint and technological capabilities amid industry challenges, showcasing how its acquisition strategy is driving growth despite market headwinds.

Executive Summary

DTI reported Q1 2025 revenue of $42.9 million, representing a 16% quarter-over-quarter growth, with a revenue mix of 89% from the Western Hemisphere and 11% from the Eastern Hemisphere. The company has completed four strategic acquisitions in the past nine months, expanding its patented product portfolio from 2 to 16 products.

CEO Wayne Prejean highlighted the company’s focus on "strategic consolidation, innovative technologies, driving efficiency, expanding global footprint, and delivering value to stockholders."

As shown in the following strategic plan and achievements summary:

Strategic Initiatives & Acquisitions

DTI’s aggressive acquisition strategy has been central to its growth narrative. The company has completed four acquisitions in nine months: Deep Casing Tools, Superior Drilling Products (NYSE:SDPI), European Drilling Projects, and Titan Tools. These acquisitions have strengthened DTI’s technological capabilities and expanded its international presence.

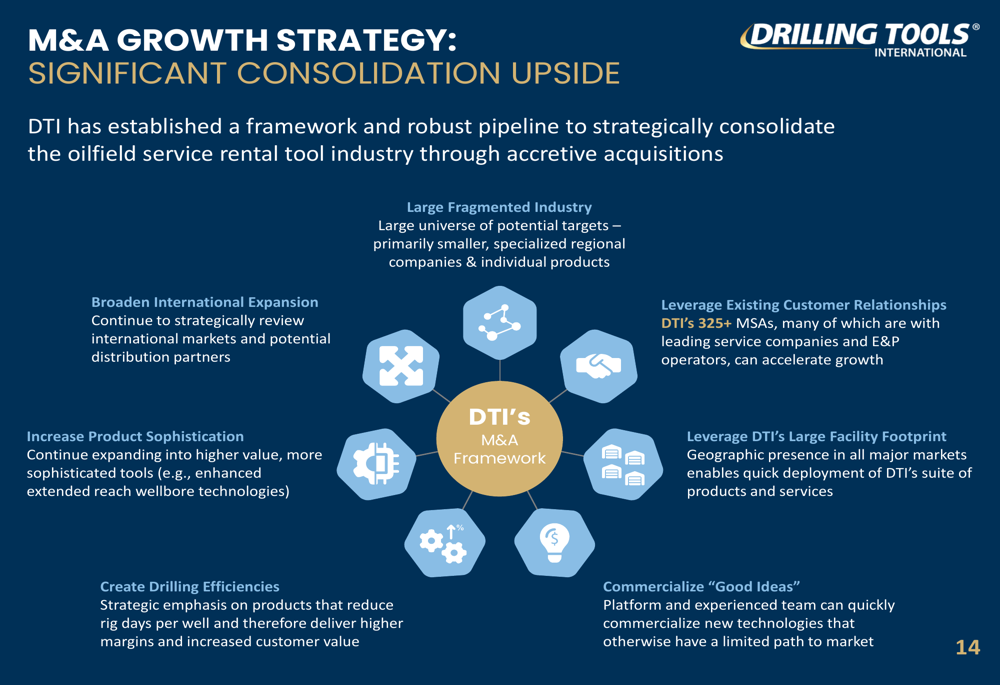

The company’s M&A strategy targets a fragmented industry with over 500 potential acquisition candidates, currently focusing on approximately 25 active targets with 5 near-term priority targets identified.

The following illustration demonstrates DTI’s M&A framework and consolidation strategy:

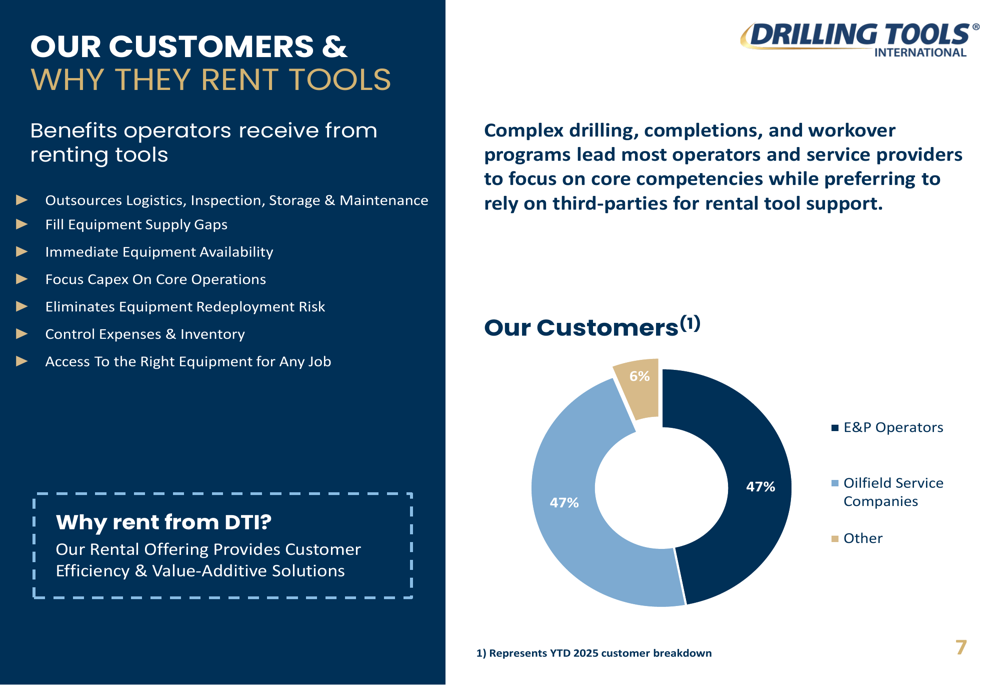

DTI’s customer base is evenly split between E&P operators (47%) and oilfield service companies (47%), with the remaining 6% classified as "Other." This diversified customer portfolio includes blue-chip companies such as ADNOC, Saudi Aramco (TADAWUL:2222), Baker Hughes (NASDAQ:BKR), Chevron (NYSE:CVX), ConocoPhillips (NYSE:COP), ExxonMobil (NYSE:XOM), and SLB.

The company’s customer breakdown and value proposition are illustrated in this chart:

Financial Performance & Outlook

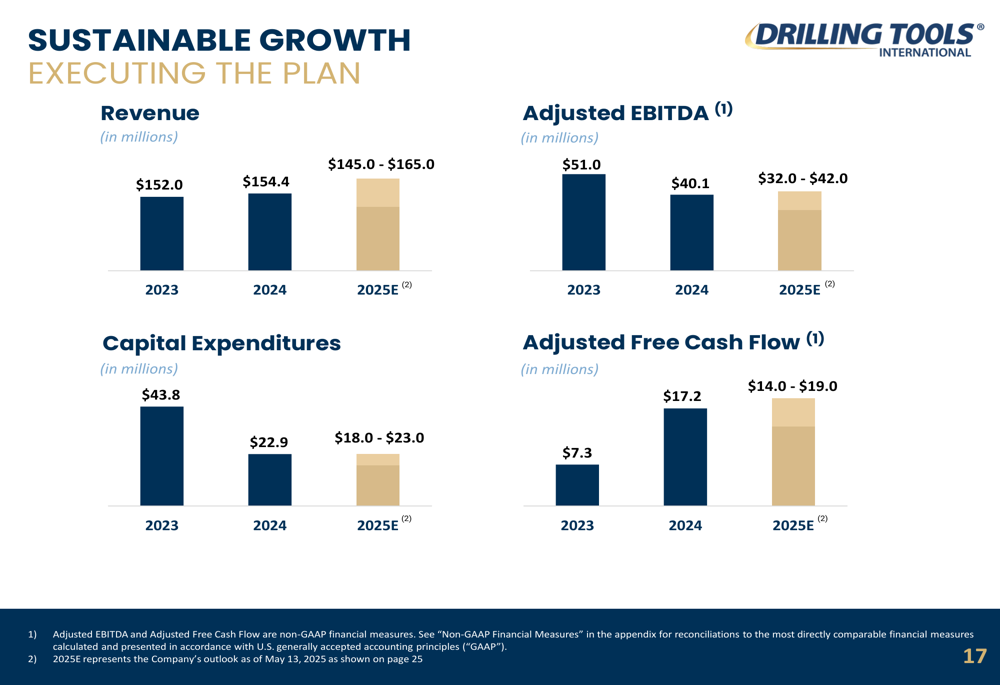

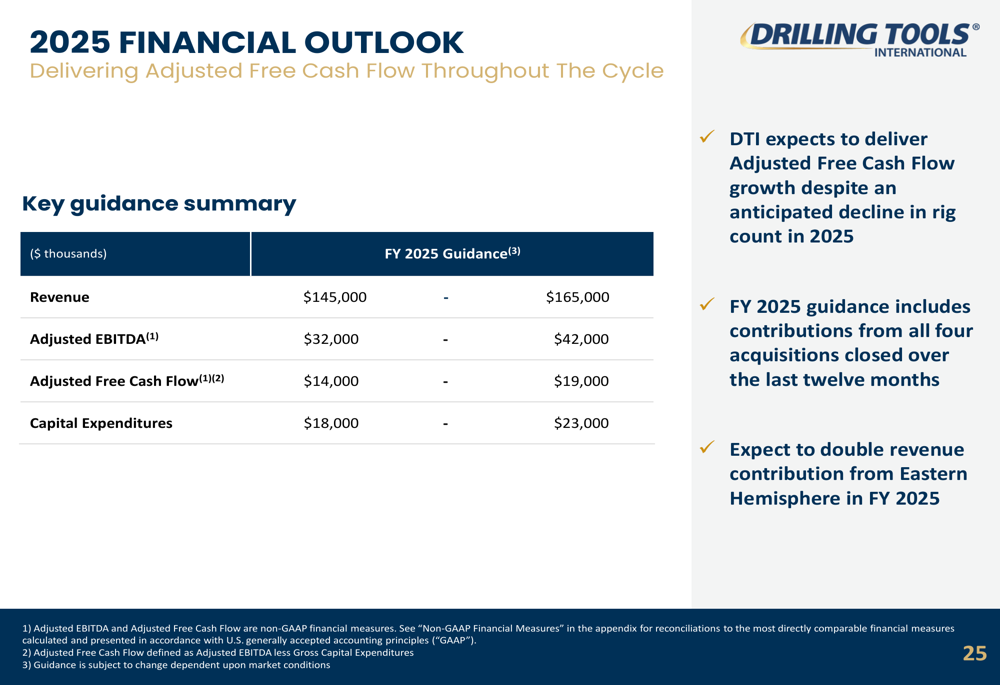

DTI’s financial outlook for 2025 projects revenue between $145 million and $165 million, adjusted EBITDA between $32 million and $42 million, and adjusted free cash flow between $14 million and $19 million. This represents a slight potential increase from 2024’s revenue of $154.4 million, though the range allows for potential contraction.

The company expects to maintain strong adjusted free cash flow margins despite anticipated declines in rig count, with contributions from all four recent acquisitions and a doubling of revenue from the Eastern Hemisphere.

The following chart illustrates DTI’s financial projections:

DTI has been strategically reducing its capital expenditures, with maintenance CapEx projected to decrease from 13% of revenue in 2023 to 9% in 2025, and growth CapEx declining from 16% of revenue in 2023 to just 4% in 2025. This capital discipline has contributed to improved adjusted free cash flow, which is expected to reach 44% of EBITDA in 2025, up from 14% in 2023.

The 2025 financial outlook summary provides a comprehensive view of DTI’s projections:

Competitive Positioning

DTI emphasized its strong market position, noting that over 60% of drilling rigs in North America utilize its tools and equipment. The company has approximately 62,000 tools deployed across North America and maintains a leading position in the deep-water Gulf of America.

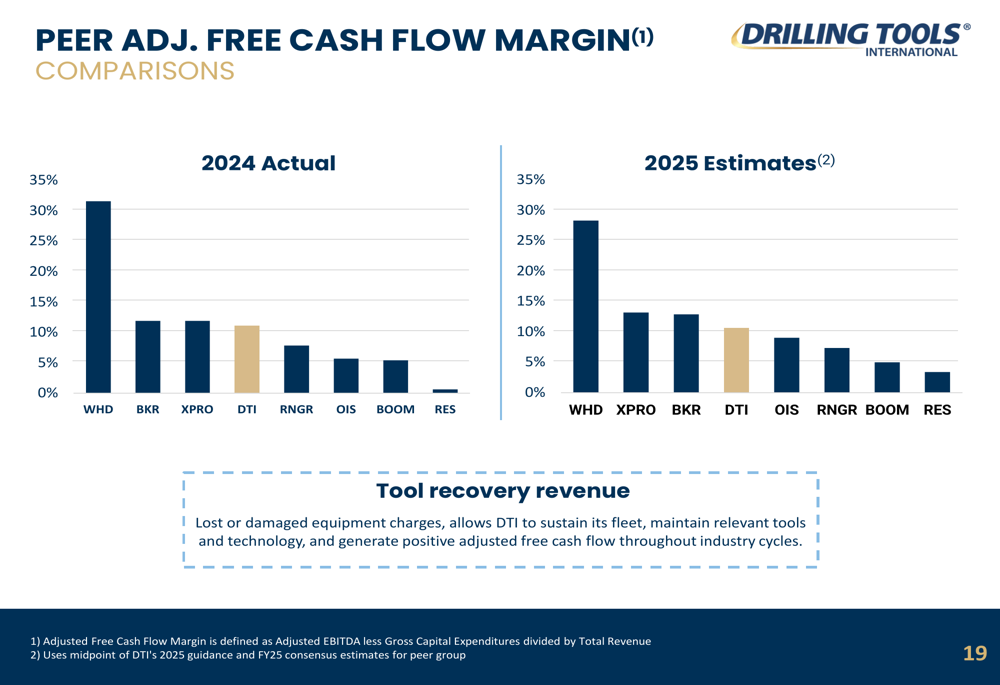

The company’s adjusted free cash flow margin compares favorably to industry peers, as illustrated in the following comparison:

DTI’s proprietary COMPASS Order Management System serves as a key operational differentiator, providing customers with tool traceability, transparency, and online ordering capabilities. The system also generates data for capital allocation decisions and fleet management.

Forward-Looking Statements

Looking ahead, DTI identified several organic growth drivers, including full-year contributions from recent acquisitions, leveraging its expanded global footprint, and growing adoption of its leading-edge downhole technologies such as Deep Casing Tools, Next (LON:NXT) Generation Stabilizers, RotoSteer, and Drill-N-Ream.

The company also noted a trend toward longer laterals in drilling operations, which favors DTI’s technology offerings, and increasing adoption of shale-type drilling applications in international markets.

CFO David Johnson emphasized the company’s capital allocation strategy: "We remain focused on maintaining financial strength while strategically deploying capital to drive growth and maximize value for our shareholders." The company has authorized a $10 million share repurchase program as part of its commitment to returning capital to shareholders.

While DTI faces industry headwinds, including rig count softness in key markets, its diversified customer base, technological capabilities, and strategic acquisitions position the company to navigate these challenges while pursuing sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.