Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

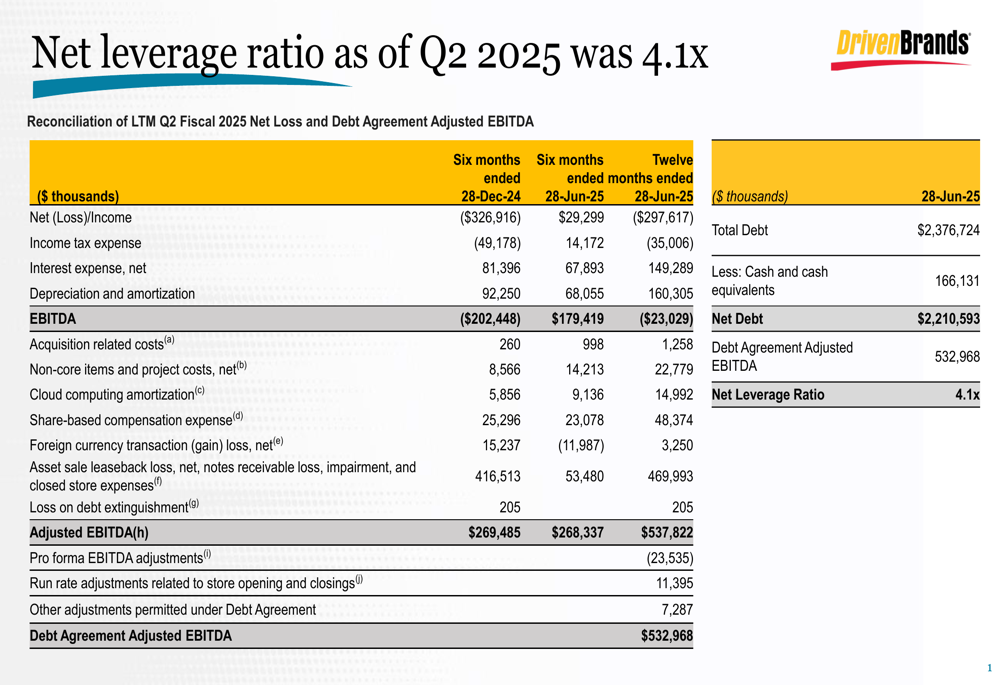

Driven Brands Holdings Inc. (NASDAQ:DRVN), North America’s largest automotive services company, revealed in its Q2 2025 financial presentation that its net leverage ratio stands at 4.1x, highlighting the company’s ongoing debt management efforts amid challenging market conditions.

The presentation, released on August 5, 2025, provides a detailed reconciliation of the company’s financial position, particularly focusing on its debt structure and adjusted EBITDA calculations. This comes as Driven Brands continues to execute its strategic initiatives, including portfolio optimization and franchise expansion.

Detailed Financial Analysis

The company’s Q2 2025 slides reveal a significant gap between reported net loss and adjusted EBITDA figures. For the twelve months ended June 28, 2025, Driven Brands reported a net loss of $297.6 million, while its Debt Agreement Adjusted EBITDA reached $533 million.

As shown in the following financial reconciliation:

This substantial difference stems from several major adjustments, most notably $469.9 million related to "Asset sale leaseback loss, net, notes receivable loss, impairment, and closed store expenses." Other significant adjustments include $160.3 million in depreciation and amortization and $149.3 million in interest expenses.

The company’s total debt stands at approximately $2.38 billion, with cash and cash equivalents of $166.1 million, resulting in a net debt position of $2.21 billion. When divided by the Debt Agreement Adjusted EBITDA of $533 million, this yields the current net leverage ratio of 4.1x.

Debt Reduction Strategy

Driven Brands appears to be actively working to reduce its leverage. Based on previous earnings information, the company has set a target to decrease its leverage ratio to below 3x by the end of 2026, meaning it still has considerable progress to make from the current 4.1x level.

The company’s recent sale of its Canadian distribution business, PH Vitres, represents one of the strategic moves aimed at debt reduction. This divestiture aligns with Driven Brands’ broader portfolio optimization strategy, focusing resources on its core service offerings while generating cash to strengthen its balance sheet.

Financial Adjustments Context

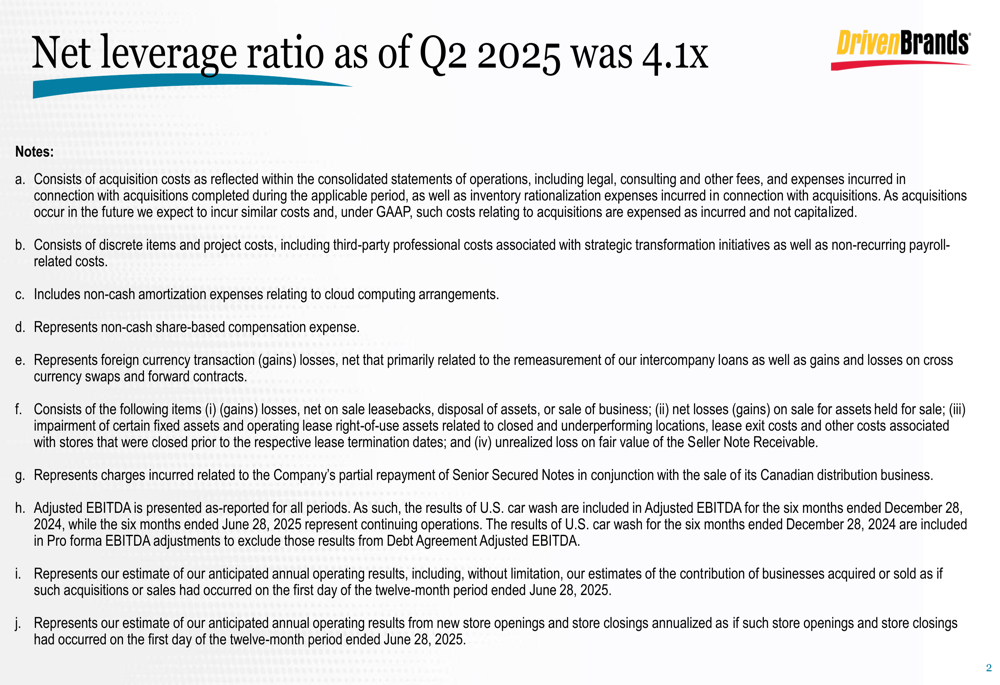

The presentation provides extensive explanatory notes regarding the various adjustments made to calculate Adjusted EBITDA, highlighting the complexity of the company’s financial structure. These adjustments include acquisition-related costs, project expenses, share-based compensation, and foreign currency transaction impacts.

The detailed notes explain:

Particularly noteworthy is item (f), which explains the nearly $470 million adjustment related to asset sales, impairments, and lease-related expenses. This substantial adjustment significantly impacts the gap between reported net loss and adjusted EBITDA.

Forward-Looking Statements

While the Q2 2025 presentation focuses primarily on the company’s current debt position, Driven Brands’ previously stated financial goals indicate a continued focus on deleveraging. The company aims to leverage its diverse portfolio of automotive service brands, including Take 5 Oil Change, which has demonstrated consistent same-store sales growth.

The company’s strategy appears to balance unit growth, primarily through franchising, with debt reduction initiatives. Based on previous earnings information, Driven Brands has been experiencing consistent same-store sales growth across its portfolio, which should support its deleveraging efforts if maintained.

However, investors should note the significant discrepancy between reported net loss and adjusted EBITDA figures, which reflects the challenges the company faces in generating bottom-line profitability despite operational growth. The substantial adjustments to EBITDA, particularly those related to asset sales and impairments, warrant close monitoring in future quarters.

As Driven Brands continues its journey toward its targeted leverage ratio of below 3x by the end of 2026, the company’s ability to generate consistent cash flow while managing its substantial debt load will remain a key focus for investors and analysts alike.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.