Gold prices just lower; monthly gains on track

Introduction & Market Context

Dynex Capital, Inc. (NYSE:DX) released its first quarter 2025 earnings presentation on April 21, 2025, revealing a mixed financial performance with improved economic returns despite posting a net loss. The mortgage real estate investment trust (REIT) continues to navigate a complex interest rate environment while maintaining its focus on agency residential mortgage-backed securities (RMBS).

The company’s presentation comes as mortgage REITs face ongoing challenges from interest rate volatility and changing Federal Reserve policies. Dynex’s stock closed at $11.67 on April 17, 2025, and was trading down 2.4% in pre-market activity following the earnings release.

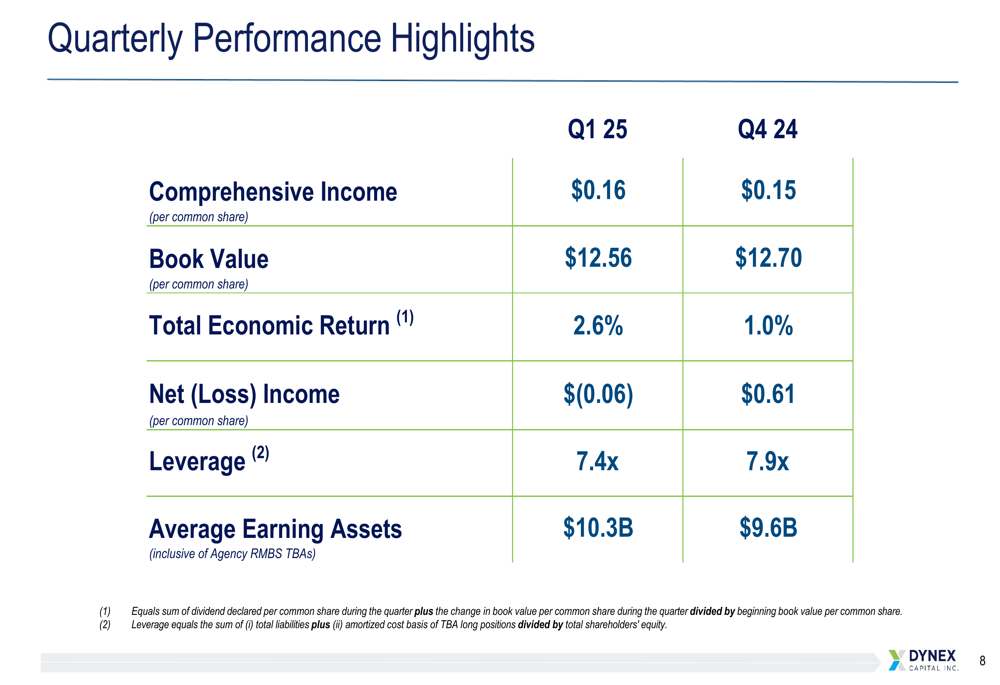

Quarterly Performance Highlights

Dynex reported a comprehensive income of $0.16 per common share for Q1 2025, a slight improvement from $0.15 in Q4 2024. However, the company posted a net loss of $(0.06) per share, a significant decline from the $0.61 net income reported in the previous quarter. Despite this, the company’s total economic return improved to 2.6% from 1.0% in Q4 2024.

As shown in the following quarterly performance comparison:

Book value per common share decreased slightly to $12.56 from $12.70 in the previous quarter. The company reduced its leverage to 7.4x from 7.9x while increasing average earning assets to $10.3 billion from $9.6 billion.

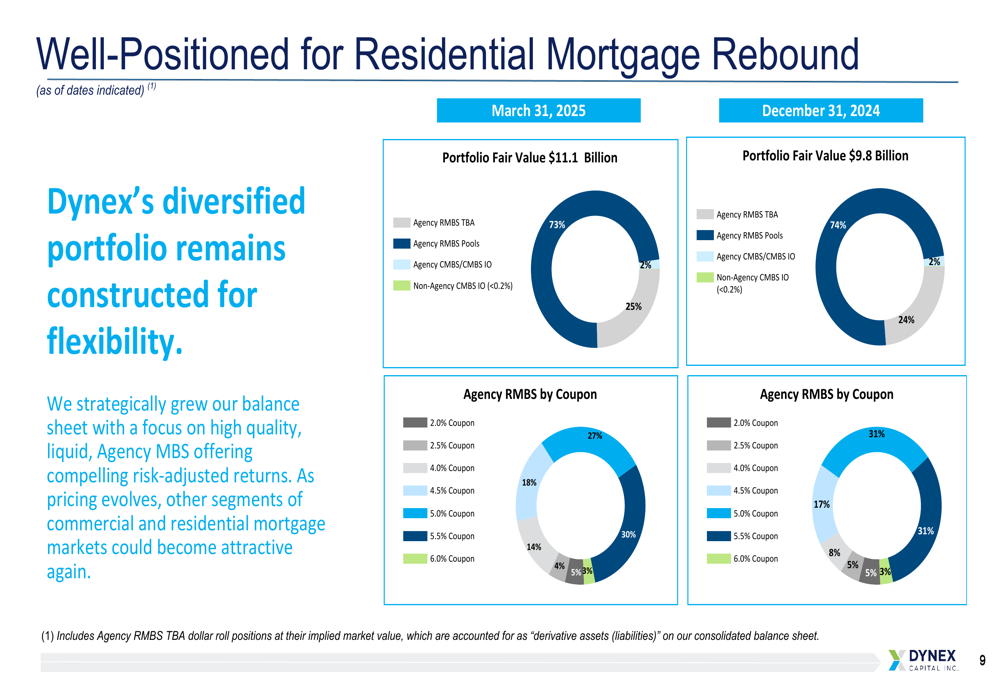

Portfolio Composition and Strategy

Dynex maintained its strategic focus on agency RMBS, with 98% of its portfolio allocated to this asset class. As of March 31, 2025, the company’s portfolio had a fair value of $11.1 billion, up from $9.8 billion at the end of December 2024.

The portfolio composition shows a slight shift in agency RMBS coupon distribution, with increases in 4.0%, 4.5%, 5.5%, and 6.0% coupons, while reducing exposure to 2.0% and 5.0% coupons:

A notable strategic shift has been the company’s move from treasury futures to interest rate swaps for hedging. This transition is expected to enhance portfolio yield and return on equity (ROE).

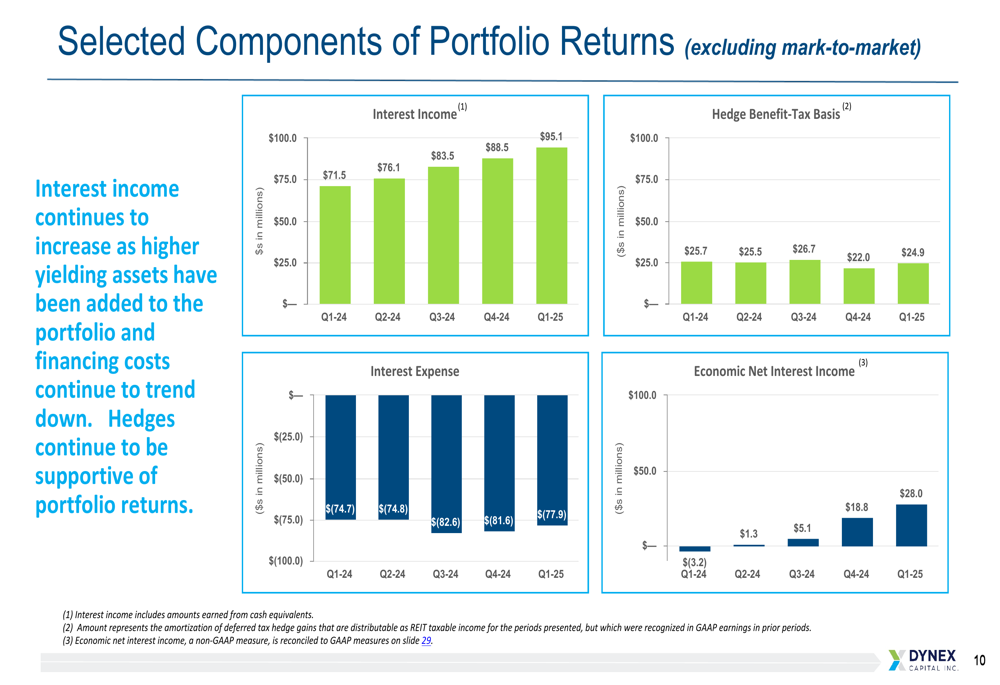

As illustrated in the components of portfolio returns chart:

The company has significantly improved its economic net interest income, which increased from $(3.2) million in Q1 2024 to $28.0 million in Q1 2025, driven by higher interest income and relatively stable interest expense despite portfolio growth.

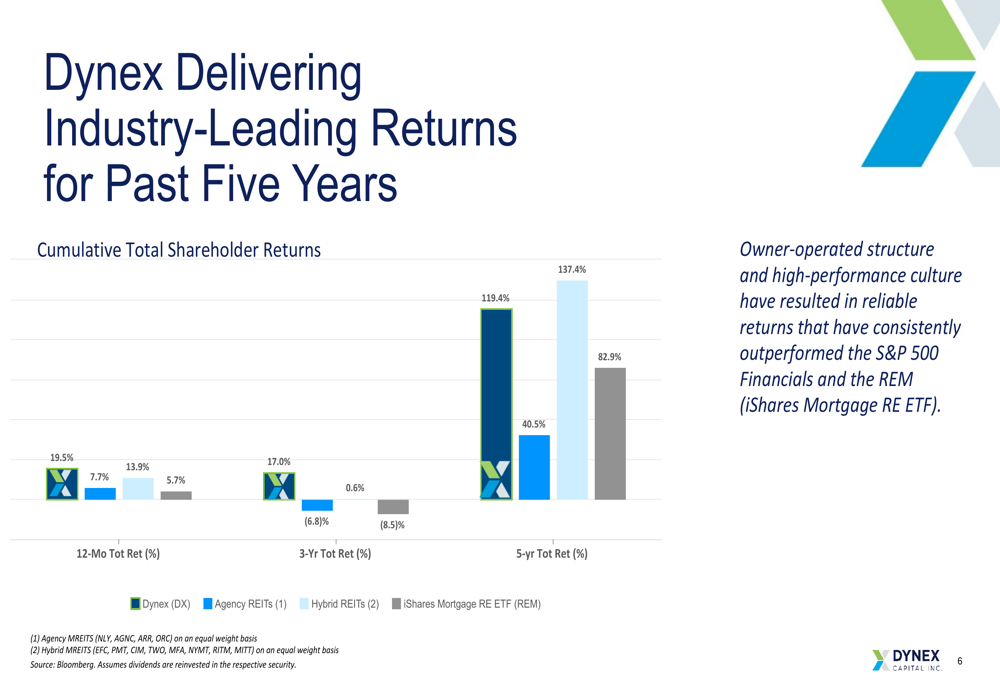

Competitive Industry Position

Dynex continues to outperform its peers across multiple timeframes. The presentation highlighted the company’s superior total shareholder returns compared to other agency REITs, hybrid REITs, and the iShares Mortgage RE ETF (REM).

As shown in the following comparative performance chart:

The company’s 12-month total return of 19.5% significantly outpaced agency REITs (7.7%), hybrid REITs (13.9%), and the iShares Mortgage RE ETF (5.7%). Similarly, Dynex’s 3-year and 5-year returns demonstrate consistent outperformance.

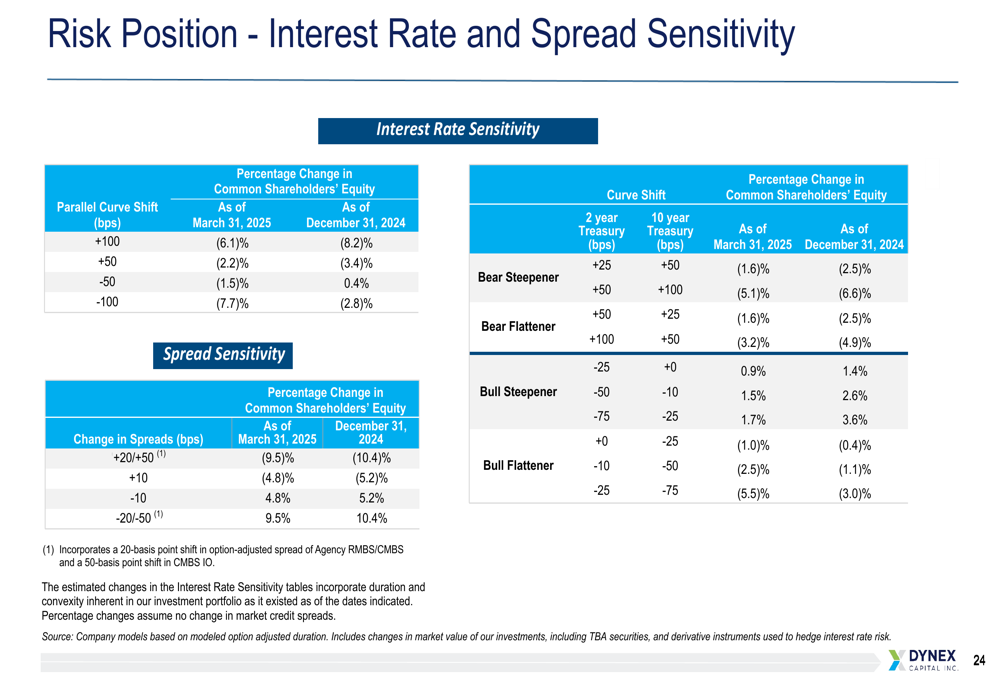

Risk Management and Sensitivity

Dynex’s risk management approach focuses on maintaining a balanced exposure to interest rate movements. The company’s interest rate sensitivity profile shows improvements compared to the previous quarter:

The presentation reveals that a 100-basis-point parallel increase in interest rates would impact book value by (6.1)%, an improvement from (8.2)% at the end of December 2024. This reflects the company’s strategic adjustments to its hedge positions.

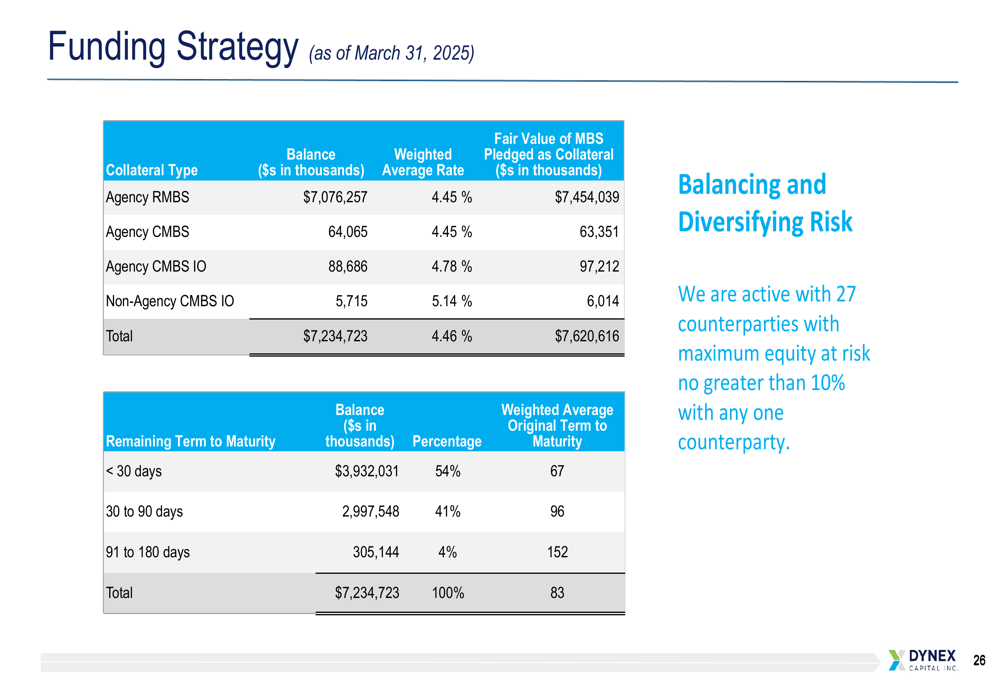

The company’s funding strategy remains focused on agency RMBS collateral, which accounts for the vast majority of its $7.23 billion in secured financing:

Macroeconomic Outlook and Strategy

Dynex identified several key macroeconomic themes influencing its strategy, including global power shifts, government policy changes, fiscal policy with large deficits, Federal Reserve policy becoming less restrictive, and improving liquidity in dollar financing markets.

The company expects mortgage spreads to tighten modestly but remain wide enough to continue attracting private capital to the sector. This environment is viewed as favorable for generating attractive returns.

Management emphasized its positioning to generate income and drive value through:

1. Income opportunities in the current wide-spread environment

2. High liquidity to capitalize on market dislocations

3. Experience in navigating policy changes and market volatility

Forward-Looking Statements

Looking ahead, Dynex remains focused on its core strategy of delivering consistent returns through disciplined risk management and strategic asset selection. The company maintains a positive outlook on the agency RMBS market, citing attractive spreads and the potential for spread tightening as supportive factors.

Management expressed confidence in the company’s ability to navigate potential policy changes, including GSE reform discussions, which could create volatility but also opportunities to deploy capital accretively.

The company’s 15.7% annualized dividend yield remains a key attraction for investors seeking income in the current market environment. With a market capitalization of $1.3 billion and a book value of $12.56 per share, Dynex continues to position itself as a value proposition for investors seeking exposure to mortgage assets with monthly dividend income.

In summary, while Dynex Capital’s Q1 2025 results present a mixed picture with improved economic returns despite a net loss, the company’s strategic positioning, outperformance versus peers, and attractive dividend yield provide a foundation for potential future growth in a challenging but opportunity-rich mortgage market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.