BofA update shows where active managers are putting money

Introduction & Market Context

Eastman Chemical Company (NYSE:EMN) released its second quarter 2025 financial results on July 31, revealing significant challenges across multiple business segments. The company’s stock plunged 15.43% following the announcement, as investors reacted to both the earnings miss and lowered guidance for the third quarter.

The chemical manufacturer reported adjusted earnings per share of $1.60, falling short of analyst expectations of $1.73, while revenue came in at $2.29 billion, slightly below the forecasted $2.30 billion. The results reflect ongoing pressures from increased tariffs, customer inventory destocking, and general economic uncertainty.

Quarterly Performance Highlights

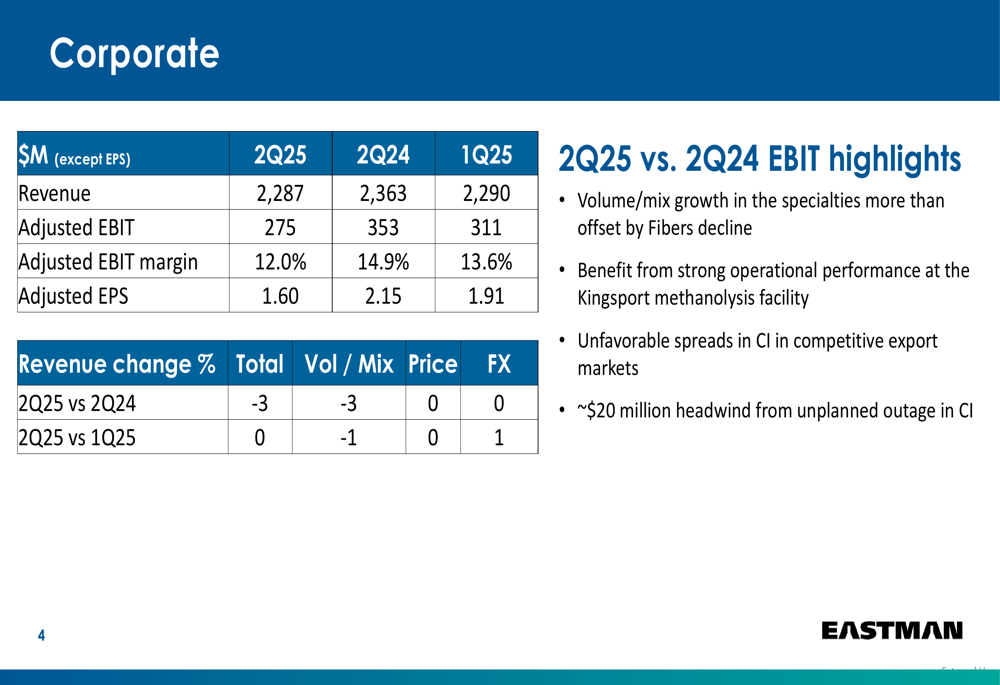

Eastman’s Q2 2025 financial performance showed a year-over-year decline across most key metrics. Revenue decreased 3% compared to Q2 2024, while adjusted EBIT fell to $275 million from $353 million in the prior-year period. The company’s adjusted EBIT margin contracted to 12.0% from 14.9% a year ago.

As shown in the following corporate financial results:

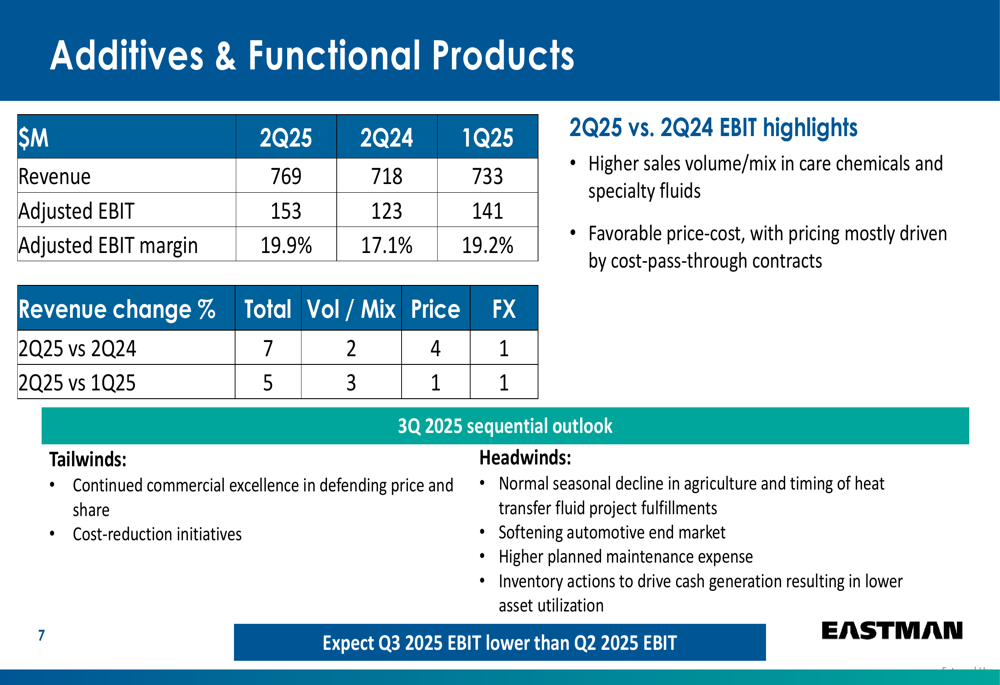

Performance varied significantly across Eastman’s business segments. The Additives & Functional Products segment was a standout performer with revenue of $769 million (up 7% year-over-year) and an adjusted EBIT margin of 19.9%, driven by higher sales volume in care chemicals and specialty fluids, along with favorable price-cost dynamics.

The segment’s strong results are detailed in this breakdown:

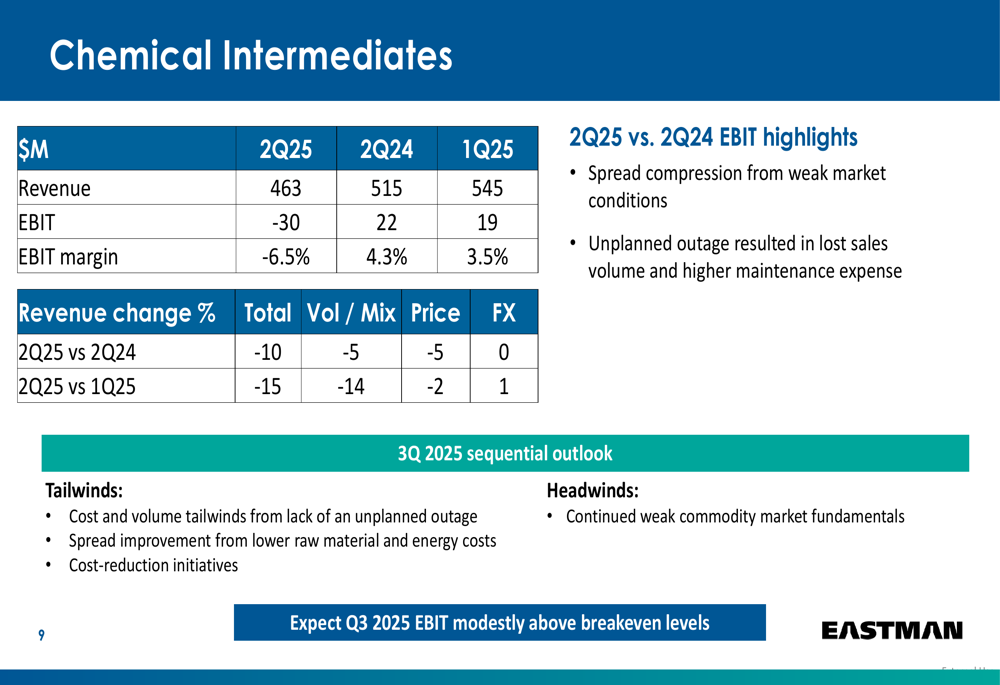

By contrast, the Chemical Intermediates segment struggled considerably, posting an operating loss of $30 million and a negative EBIT margin of 6.5%. Management attributed this poor performance to spread compression from weak market conditions and an unplanned outage that resulted in lost sales volume and higher maintenance expenses.

The Chemical Intermediates segment’s challenges are illustrated here:

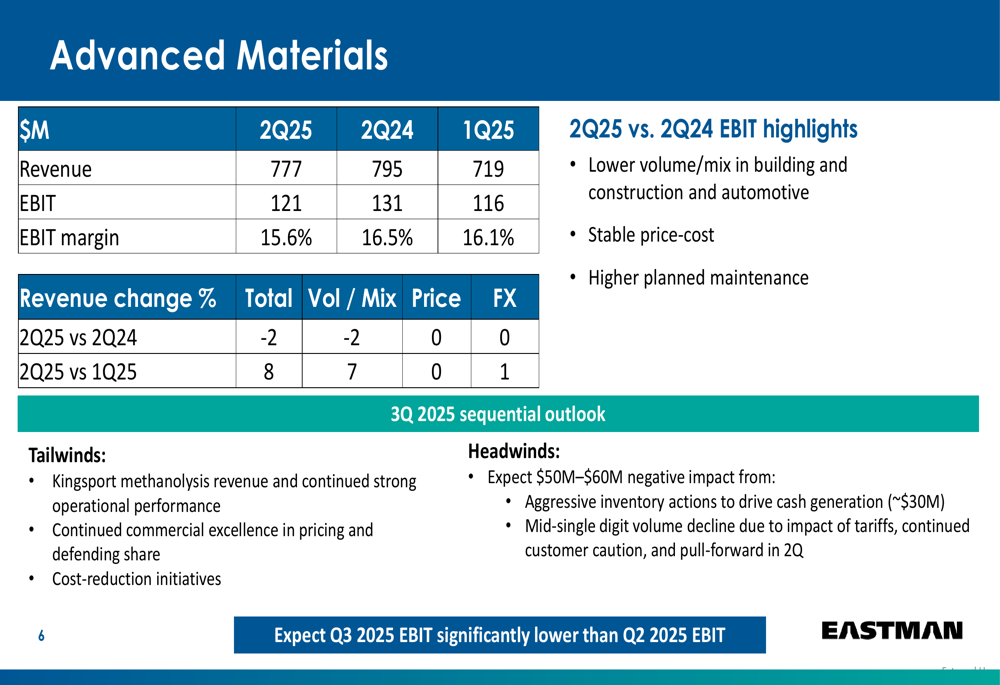

The Advanced Materials segment saw modest declines with revenue of $777 million (down 2% year-over-year) and EBIT of $121 million, impacted by lower volume in building and construction and automotive applications.

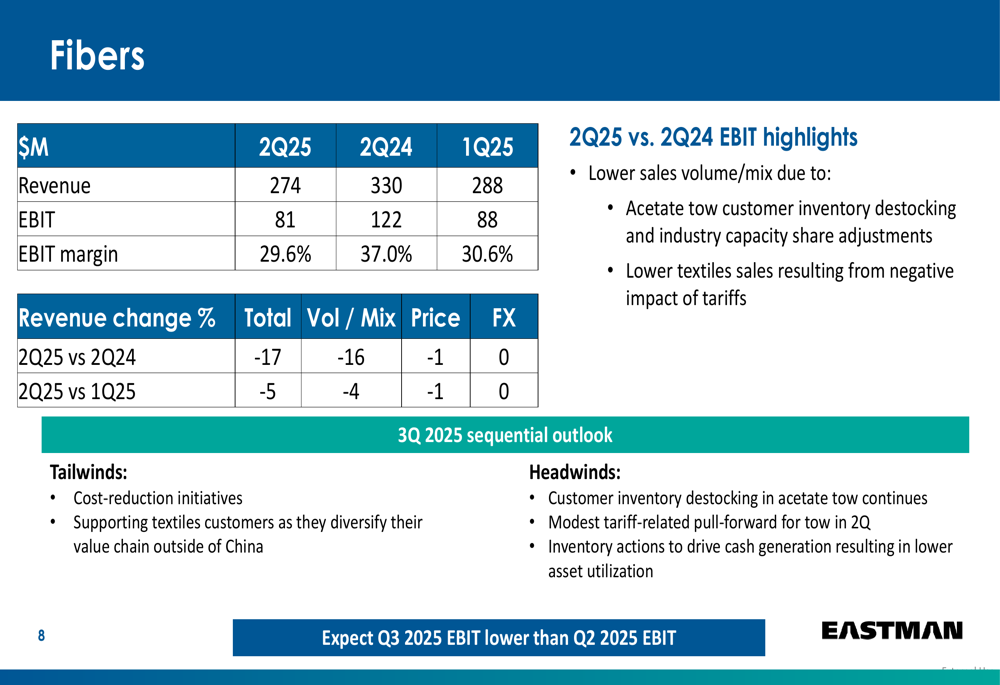

The Fibers segment experienced the most significant revenue decline at 17% year-over-year, with EBIT falling to $81 million from $122 million in Q2 2024. This was primarily due to acetate tow customer inventory destocking and lower textiles sales resulting from tariff impacts.

Circular Economy Platform Progress

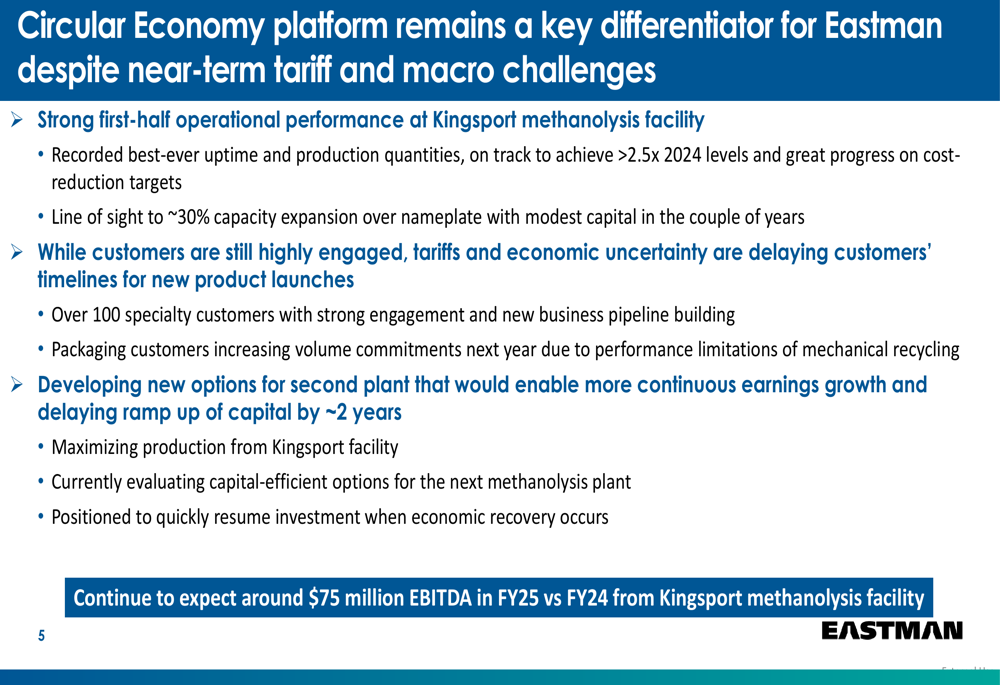

Despite broader challenges, Eastman highlighted strong operational performance at its Kingsport methanolysis facility, a key component of its circular economy strategy. The facility recorded its best-ever uptime and production quantities, on track to achieve more than 2.5 times 2024 levels.

The company expects approximately $75 million in incremental EBITDA from the Kingsport facility in fiscal year 2025 compared to 2024. However, management noted that while customer engagement remains strong, tariffs and economic uncertainty are delaying customers’ timelines for new product launches.

The presentation also revealed that Eastman is developing capital-efficient options for its second methanolysis plant while delaying the capital ramp-up by approximately two years, allowing the company to maximize production from the existing Kingsport facility.

The circular economy platform update is detailed here:

Financial Position & Outlook

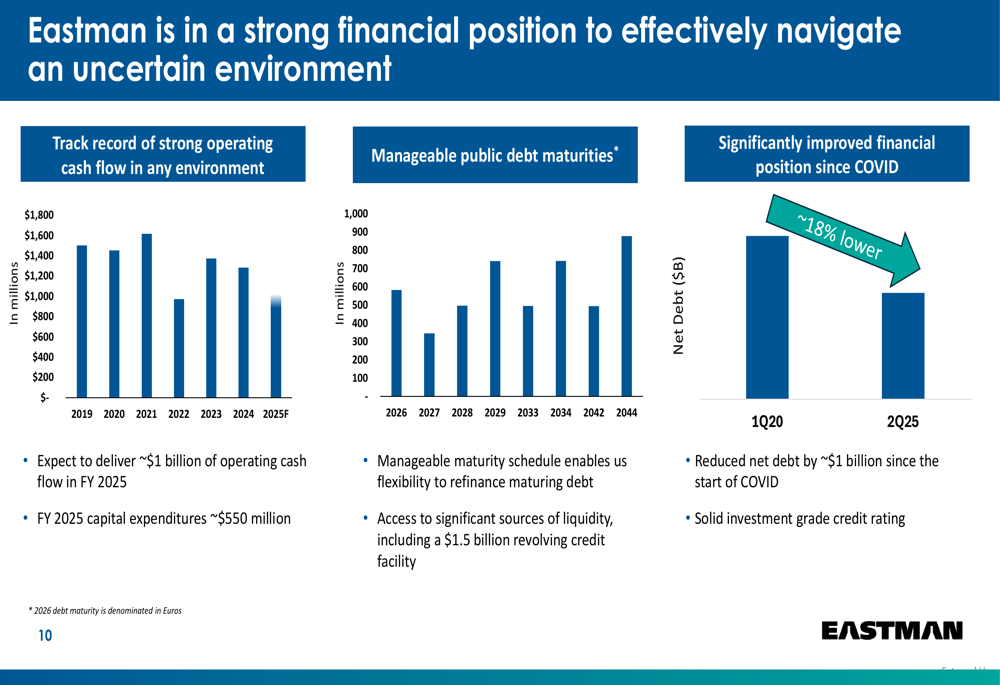

Eastman emphasized its strong financial position, noting that net debt has decreased by approximately 18% since the start of the COVID pandemic. The company expects operating cash flow of approximately $1 billion in FY 2025, with capital expenditures of around $550 million.

As illustrated in the financial position slide:

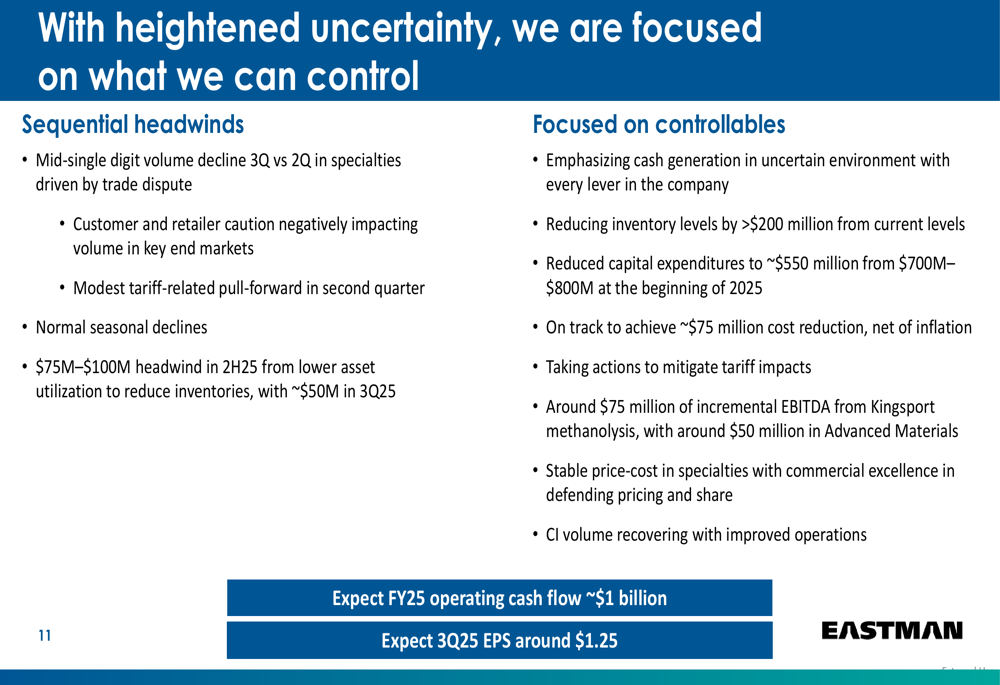

Looking ahead to Q3 2025, Eastman projects earnings per share of around $1.25, significantly lower than Q2’s $1.60. Management cited several sequential headwinds, including a mid-single-digit volume decline, customer and retailer caution, modest tariff-related pull-forward, normal seasonal declines, and a $75-100 million headwind in the second half of 2025 from lower asset utilization.

The company’s focus on controllable factors includes:

Strategic Initiatives

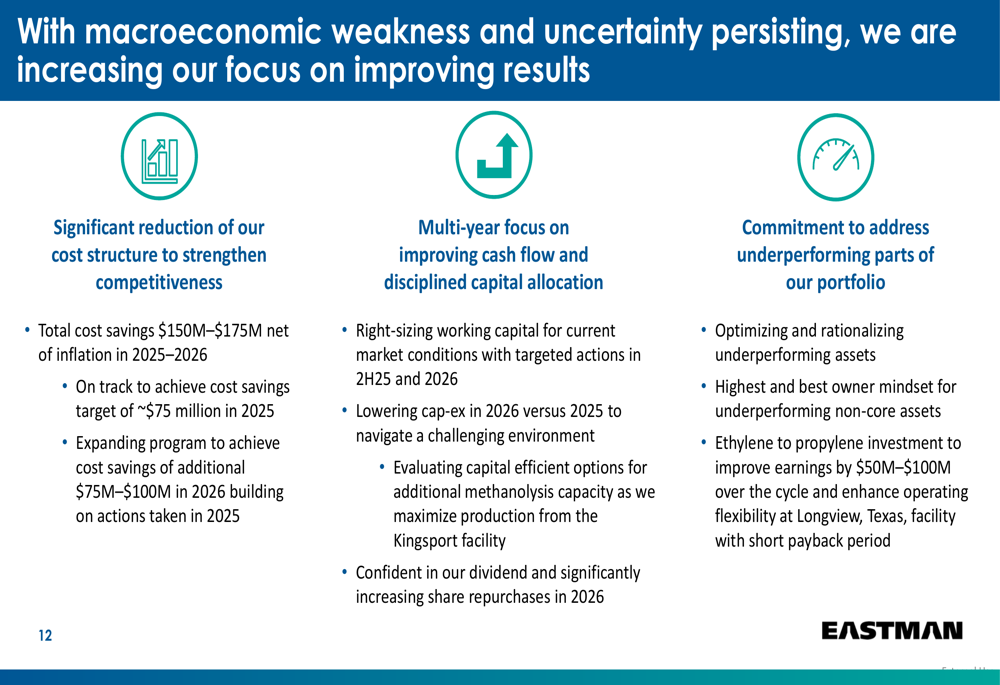

In response to the challenging environment, Eastman is implementing several strategic initiatives to improve performance. The company is on track to achieve cost savings of approximately $75 million in 2025 and is targeting an additional $75-100 million in cost reductions for 2026.

Other key initiatives include right-sizing working capital, lowering capital expenditures in 2026, optimizing underperforming assets, and an ethylene to propylene investment expected to improve earnings by $50-100 million.

The strategic focus areas are outlined here:

CEO Mark Costa emphasized the company’s strategic focus during the earnings call, stating, "To get out of a weak environment, you gotta create your own growth." Costa expressed confidence in the company’s ability to recover earnings next year despite the current challenges.

With the stock now trading near its 52-week low following the earnings release, investors will be closely monitoring Eastman’s ability to execute on its cost-cutting initiatives and navigate the ongoing challenges from tariffs and economic uncertainty in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.