Trump to appeal tariff ruling, warns of economic consequences

Introduction & Market Context

Ecovyst Inc (NYSE:ECVT), a catalyst and services provider for the refining, petrochemical and emissions control industries, reported mixed second-quarter 2025 results on August 7, showing sales growth despite volume challenges. The company maintained its full-year guidance midpoint while continuing strategic investments and capital return initiatives.

Trading at $8.39 per share, Ecovyst stock has been range-bound between its 52-week low of $5.24 and high of $9.07, reflecting investor caution amid the company’s transition and strategic review of its Advanced Materials & Catalysts segment.

Quarterly Performance Highlights

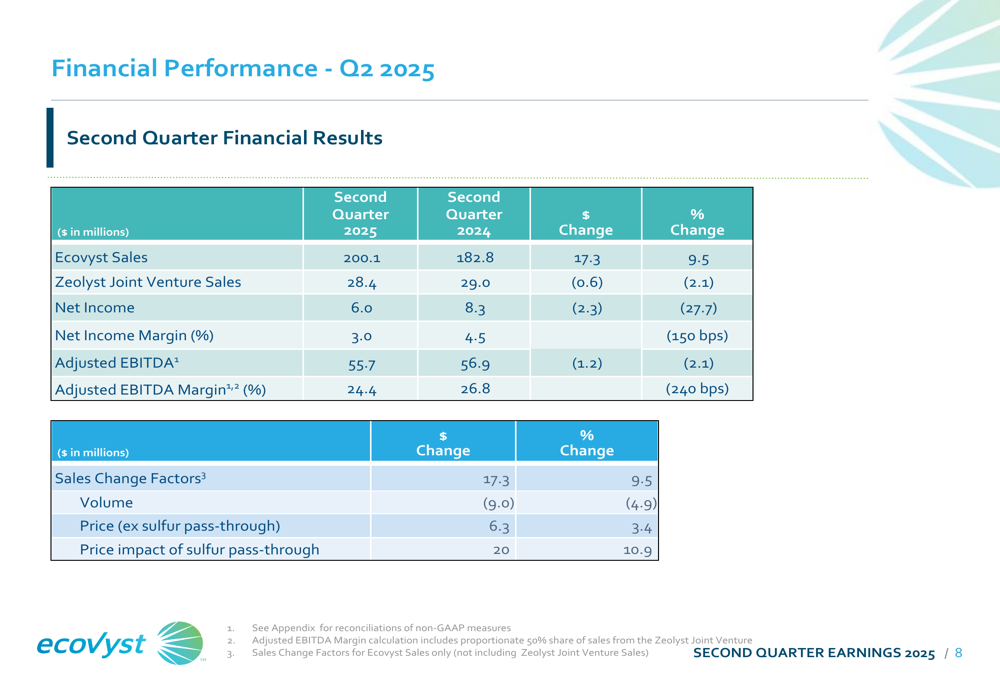

Ecovyst reported Q2 2025 sales of $200.1 million, a 9.5% increase compared to the same period last year. However, this growth was primarily driven by favorable pricing and sulfur pass-through rather than volume increases. The company’s adjusted EBITDA declined slightly to $55.7 million, down 2.1% year-over-year, with margins compressing by 240 basis points to 24.4%.

As shown in the following financial highlights slide, net income fell more substantially, dropping 27.7% to $6.0 million:

The company’s sales growth was driven by a 3.4% increase in price (excluding sulfur pass-through) and a 10.9% increase from sulfur pass-through, which was partially offset by a 4.9% decrease in volume. This volume decline was primarily attributed to unplanned downtime in the Ecoservices segment and timing of catalyst sales in the Advanced Materials segment.

The following slide details the financial results comparison between Q2 2025 and Q2 2024:

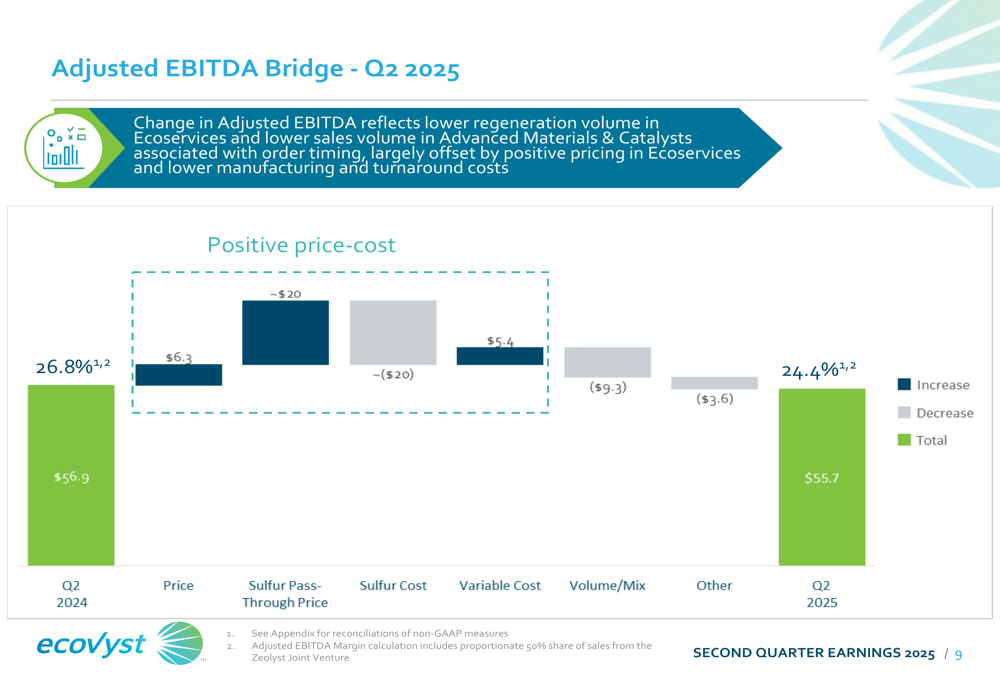

The adjusted EBITDA bridge below illustrates how positive pricing was largely offset by negative volume/mix effects and other factors:

Segment Performance Analysis

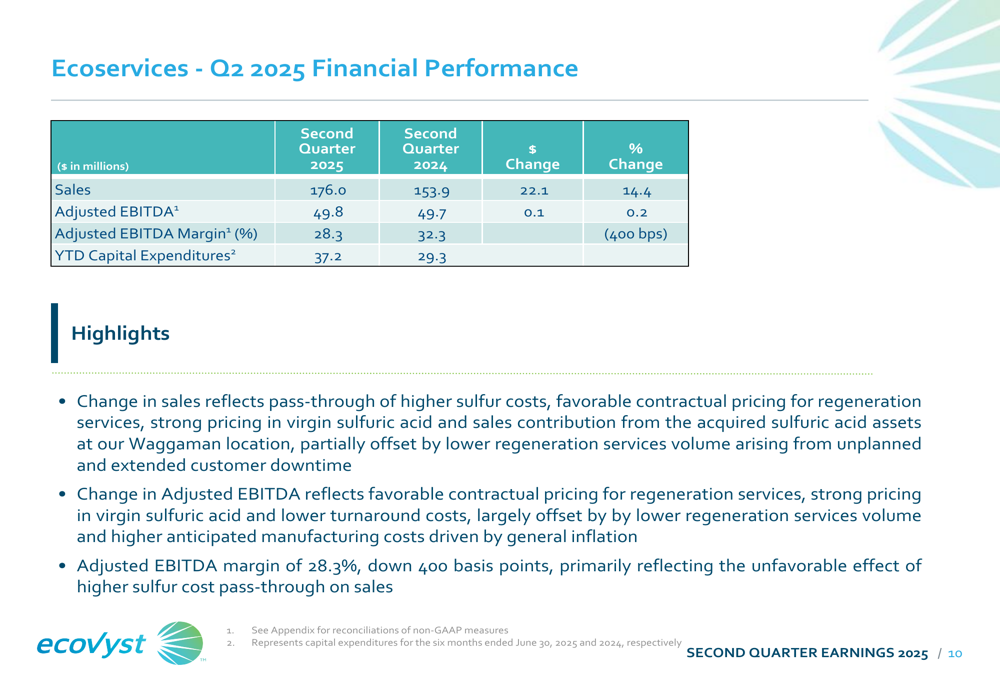

Ecovyst’s Ecoservices segment, which provides sulfuric acid regeneration services to refineries, posted strong sales growth of 14.4% to $176.0 million. However, adjusted EBITDA increased only marginally by 0.2% to $49.8 million, with margin compression of 400 basis points to 28.3%. This performance reflects higher sulfur costs and lower regeneration volume from unplanned downtime, partially offset by favorable contractual pricing.

The segment performance is detailed in the following slide:

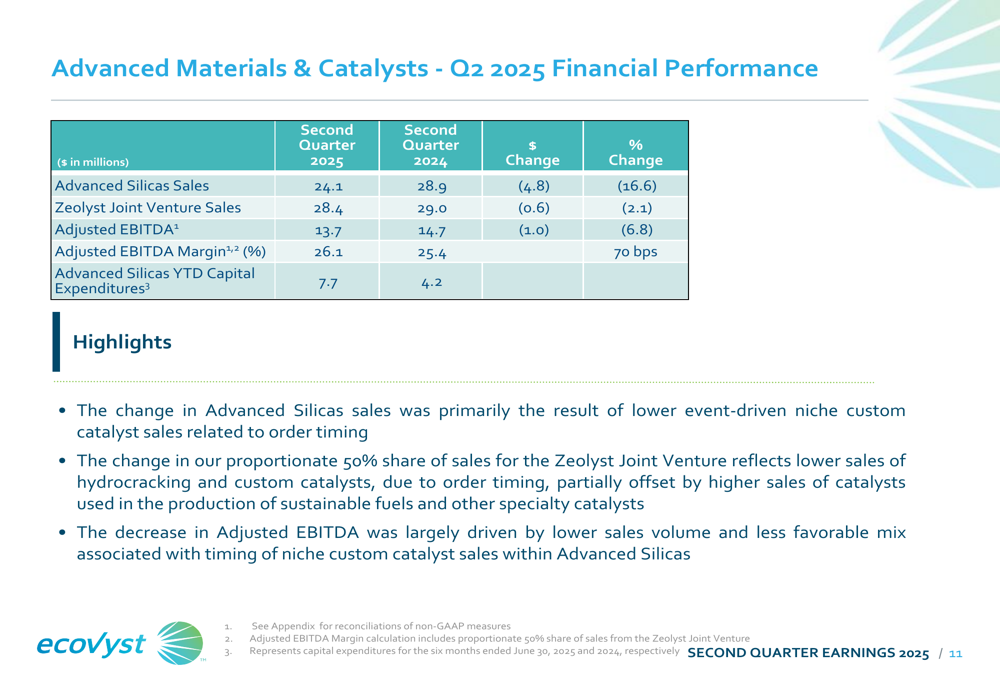

Meanwhile, the Advanced Materials & Catalysts segment faced more significant challenges, with Advanced Silicas sales declining 16.6% to $24.1 million due to lower niche custom catalyst sales. The Zeolyst Joint Venture, which is accounted for as an equity method investment, saw sales decrease by 2.1% to $28.4 million. Combined adjusted EBITDA for the segment fell 6.8% to $13.7 million, though margins improved slightly by 70 basis points to 26.1%.

Strategic Initiatives & Acquisitions

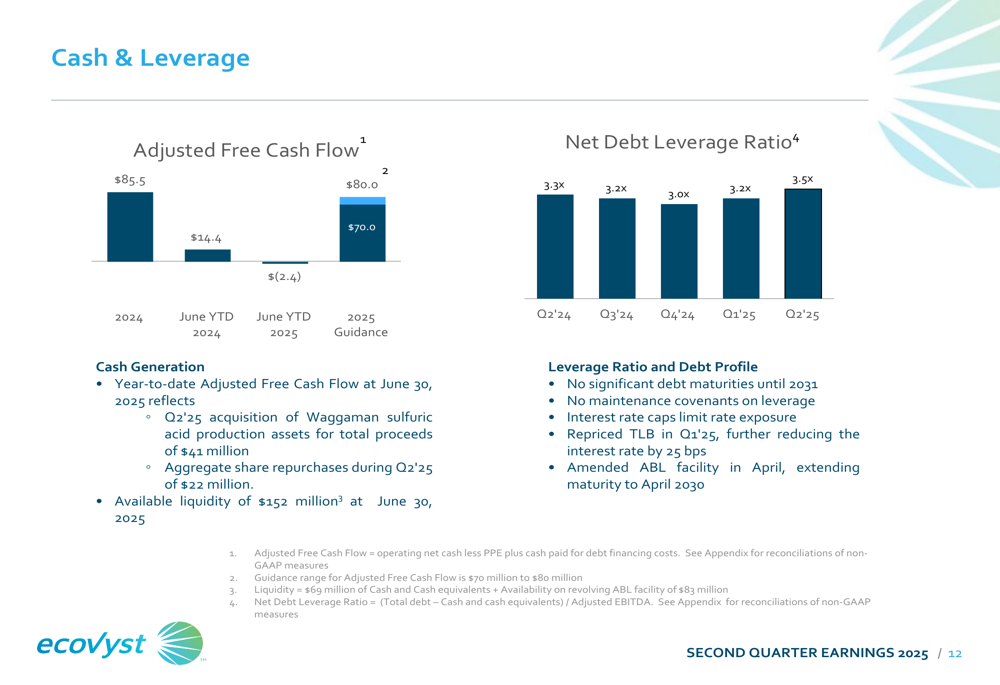

Despite the challenging quarter from a cash flow perspective, Ecovyst continued to execute on its strategic initiatives. The company completed the acquisition of Waggaman sulfuric acid production assets for $41 million, expanding its capacity in the virgin sulfuric acid market. Additionally, Ecovyst repurchased 2.9 million shares for approximately $22 million during the quarter, demonstrating confidence in its long-term outlook.

These investments, along with planned maintenance turnarounds, contributed to negative adjusted free cash flow of $2.4 million for the first half of 2025. However, management expects positive cash generation in the second half of the year, with full-year adjusted free cash flow projected between $70-80 million.

The company’s cash position and leverage ratio are illustrated in the following slide:

The net debt leverage ratio increased slightly to 3.5x from 3.3x a year ago, reflecting the impact of acquisitions and share repurchases. Ecovyst maintains adequate liquidity of $152 million, with no major debt maturities until 2031.

Forward Outlook & Guidance

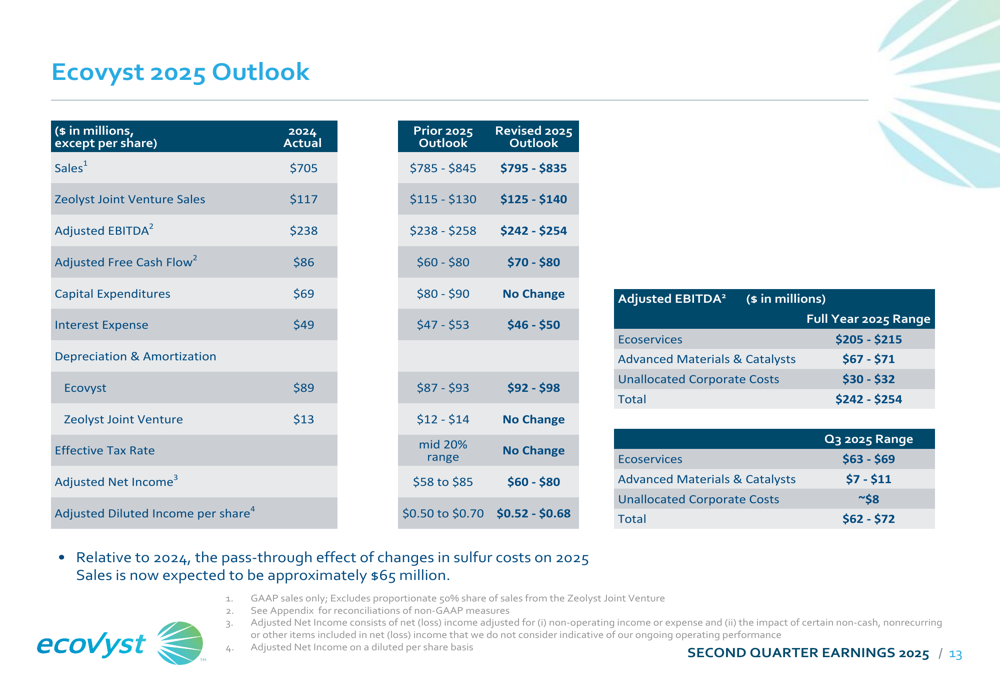

Ecovyst maintained the midpoint of its full-year 2025 adjusted EBITDA guidance at $242-254 million, while slightly narrowing the sales range to $795-835 million. The company also raised its outlook for Zeolyst Joint Venture sales to $125-140 million and increased the lower end of its adjusted free cash flow guidance to $70-80 million.

The detailed 2025 outlook is presented in the following slide:

For the remainder of 2025, Ecovyst expects high refinery utilization rates and incremental demand for virgin sulfuric acid in mining applications to benefit the Ecoservices segment. In Advanced Materials & Catalysts, the company anticipates increased sales of hydrocracking and polyethylene catalysts compared to 2024.

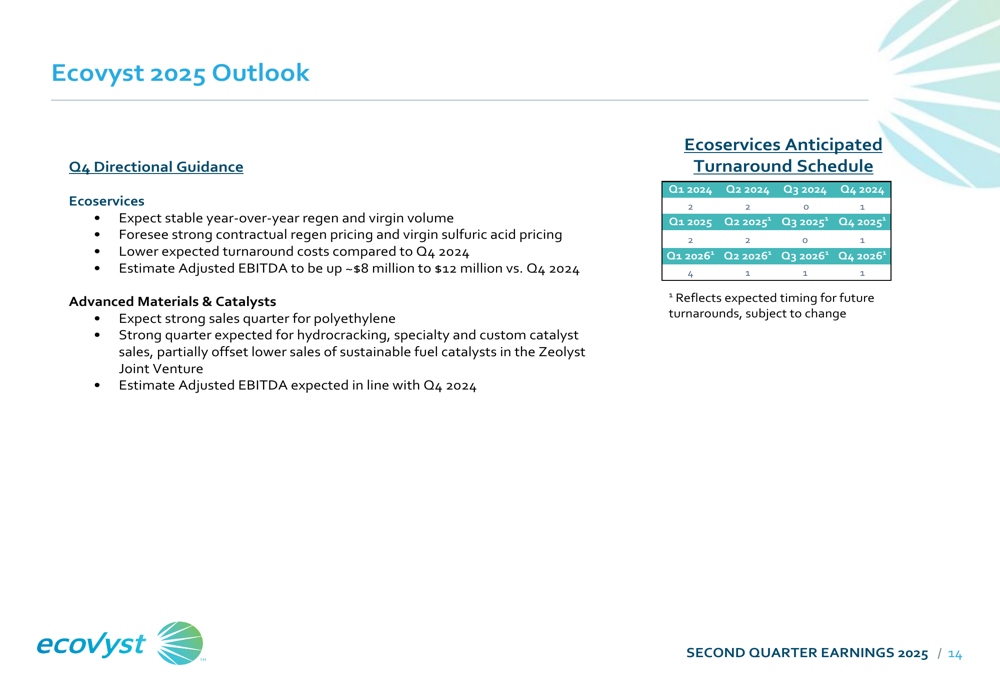

Management also provided directional guidance for Q4 2025, expecting Ecoservices adjusted EBITDA to increase by approximately $8-12 million compared to Q4 2024, driven by stable regeneration and virgin volume, strong pricing, and lower turnaround costs. Advanced Materials & Catalysts adjusted EBITDA is expected to be in line with Q4 2024.

Notably, Ecovyst mentioned that it expects to provide an update on the strategic review of its Advanced Materials & Catalysts segment "in the near future," suggesting potential portfolio changes that could reshape the company’s structure and focus areas.

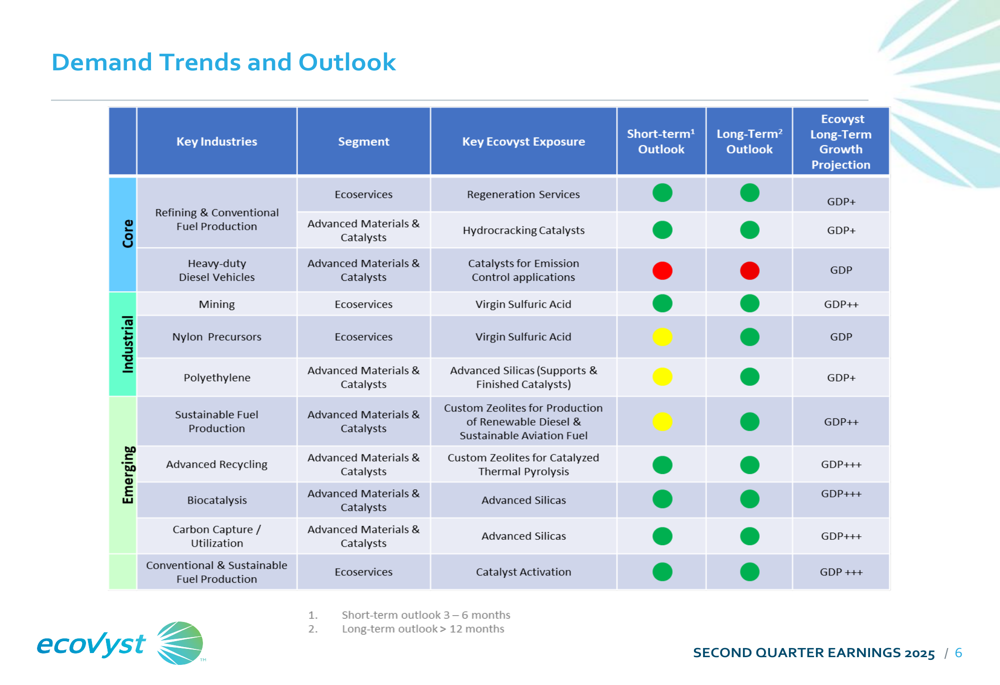

The company’s demand trends and outlook slide provides additional context for long-term growth expectations across various end markets:

With its maintained guidance, strategic acquisitions, and ongoing capital return program, Ecovyst appears positioned to navigate the current operational challenges while continuing to invest in long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.