Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

Elanco Animal Health (NYSE:ELAN) presented its second quarter 2025 earnings results on August 7, 2025, highlighting strong organic growth and raised full-year guidance despite potential tariff headwinds. The company’s shares closed at $13.95 on August 6, down 1.76% ahead of the earnings release, with the stock trading within a 52-week range of $8.02 to $15.78.

The animal health company reported significant progress across its pet health portfolio and innovation pipeline, continuing the momentum seen in Q1 2025 when the company beat expectations with $0.37 EPS and $1.19 billion in revenue.

Quarterly Performance Highlights

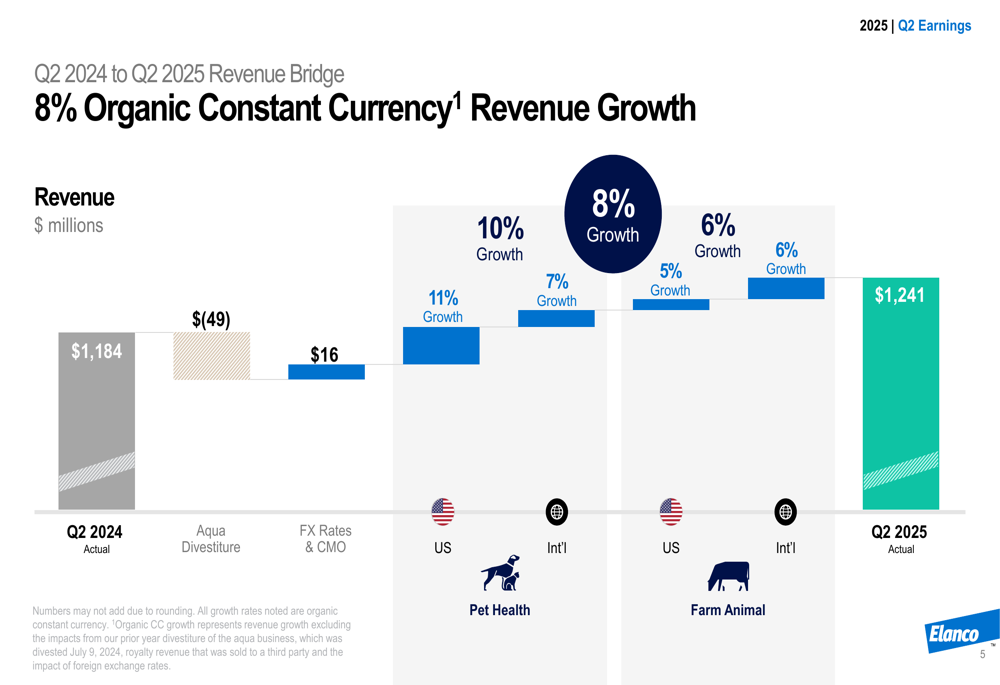

Elanco reported Q2 2025 revenue of $1,241 million, representing 5% total growth and 8% organic constant currency growth compared to the same period last year. This performance exceeded the company’s guidance by $56 million, with particularly strong results in the U.S. Pet Health segment, which grew 11% and marked the eighth consecutive quarter of underlying growth.

As shown in the following revenue bridge chart, the company’s growth was broad-based across segments, despite a $49 million revenue reduction from the Aqua divestiture:

The company’s adjusted EBITDA reached $238 million, exceeding guidance by $28 million, while adjusted EPS of $0.26 surpassed expectations by $0.07. However, both metrics declined 13% year-over-year, primarily due to the Aqua divestiture and increased operating expenses.

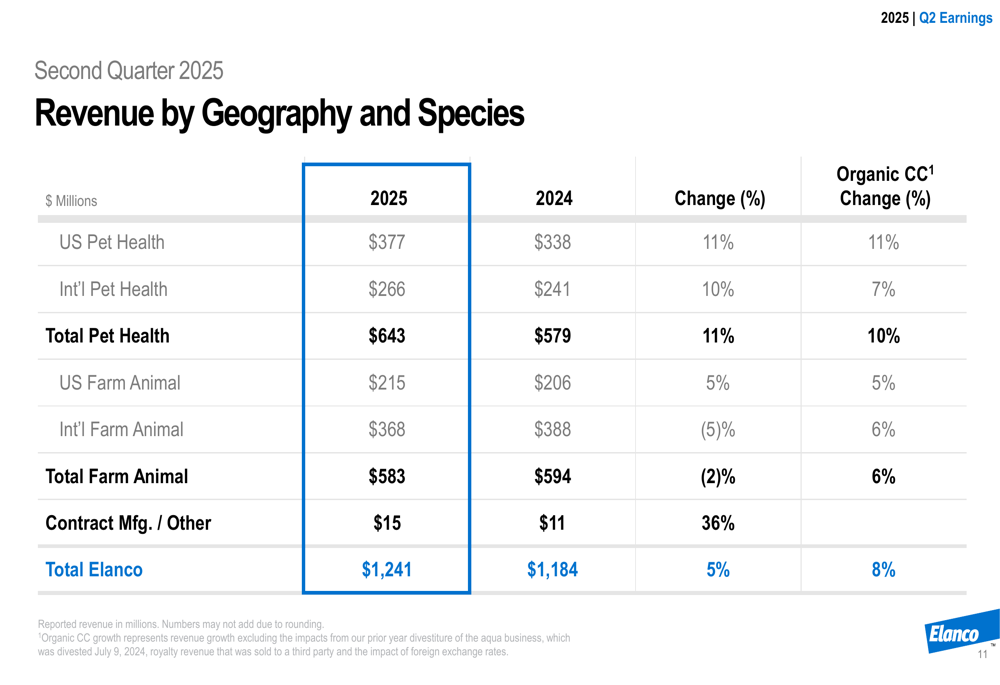

The detailed breakdown of revenue by geography and species shows strength across most segments:

Innovation Portfolio

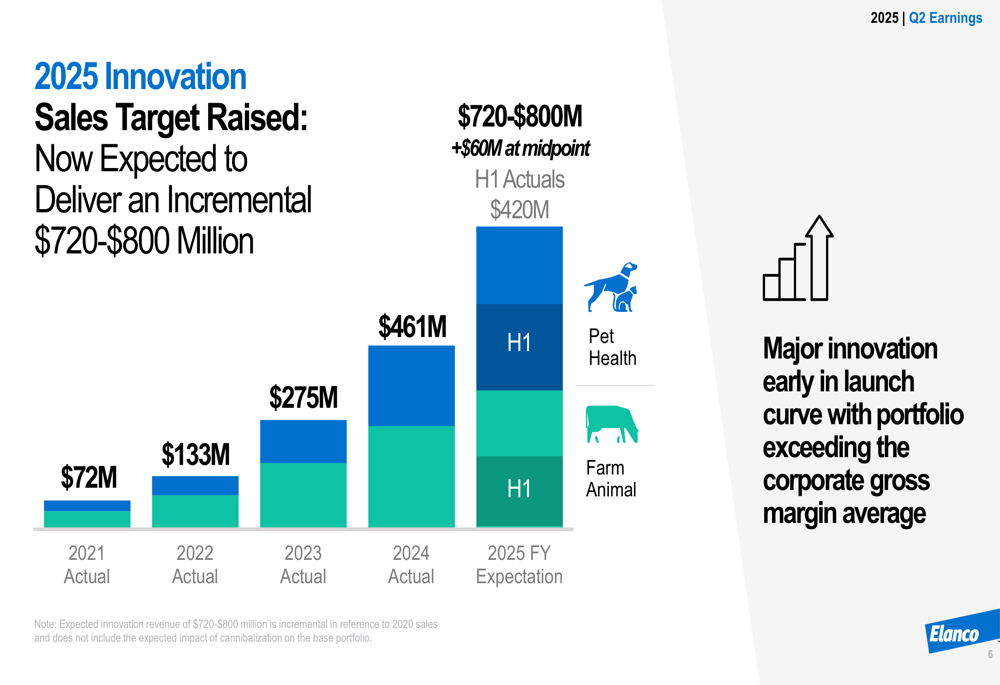

A key driver of Elanco’s performance has been its innovation portfolio, which contributed $420 million in revenue during the first half of 2025. Based on this strong performance, the company raised its full-year innovation revenue target to $720-$800 million, as illustrated in the following chart:

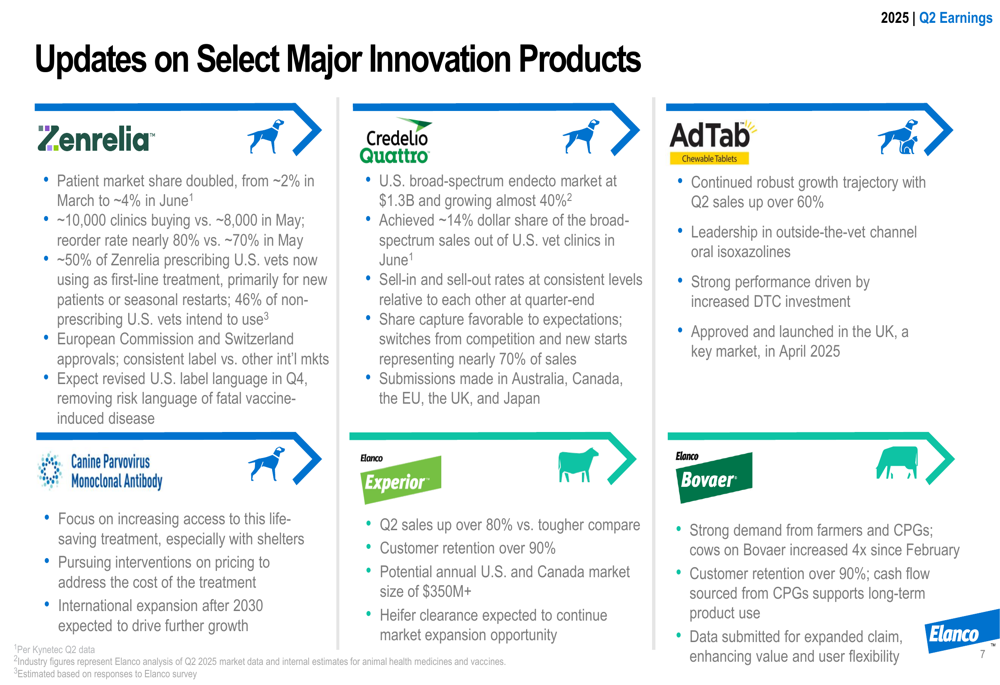

Several major innovation products are showing significant market traction. As detailed in the presentation, Zenrelia has doubled its market share with approximately 10,000 clinics now purchasing the product, while Credelio Quattro has achieved approximately 14% dollar share in the U.S. broad-spectrum endecto market:

Financial Position

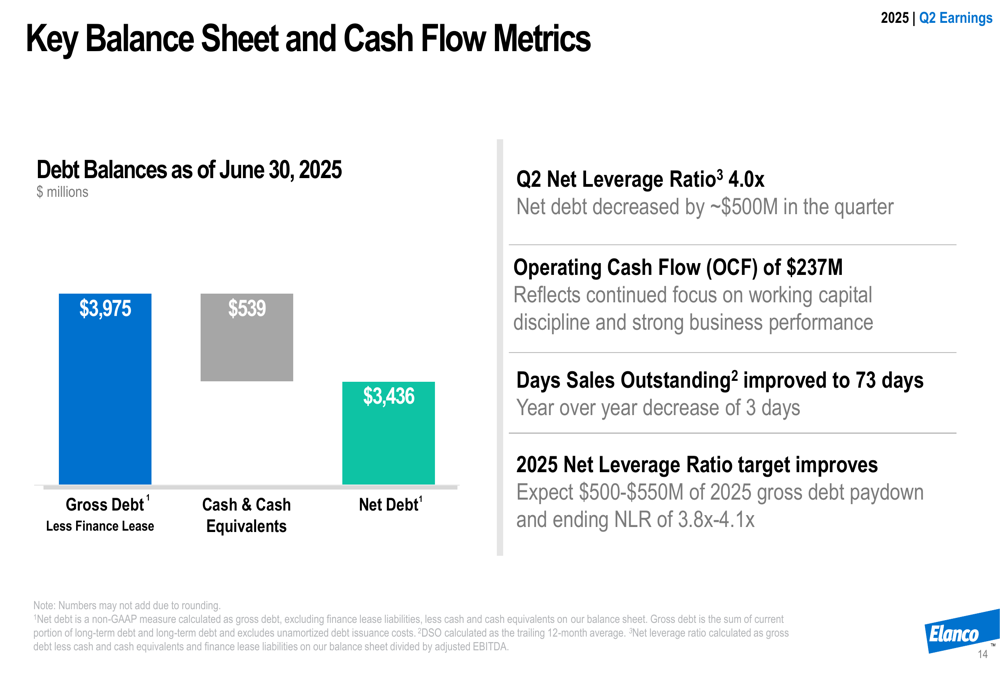

Elanco continues to make progress on its deleveraging strategy, with the net leverage ratio improving to 4.0x at the end of Q2 2025. The company reduced net debt by approximately $500 million during the quarter, with operating cash flow of $237 million.

The following slide illustrates key balance sheet and cash flow metrics:

For 2025, Elanco expects gross debt paydown of $500-$550 million, which should improve the year-end net leverage ratio to 3.8x-4.1x, better than previously anticipated. The company maintains its capital allocation strategy of prioritizing debt reduction while investing in R&D, manufacturing capabilities, and commercial launches.

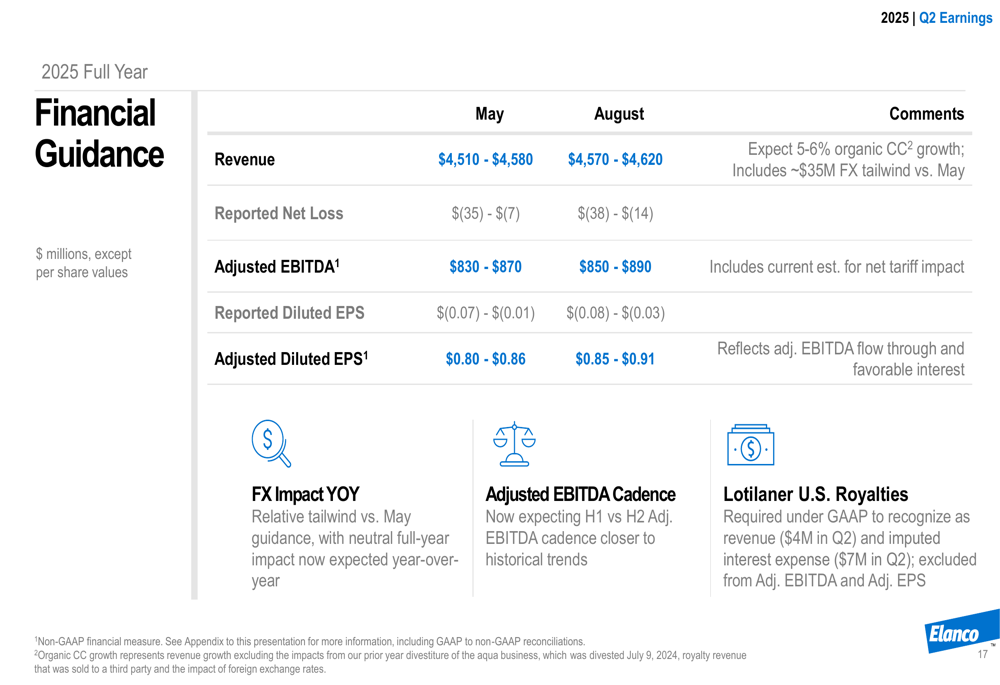

Updated Guidance

Based on strong Q2 results and positive outlook, Elanco raised its full-year 2025 guidance across all key metrics:

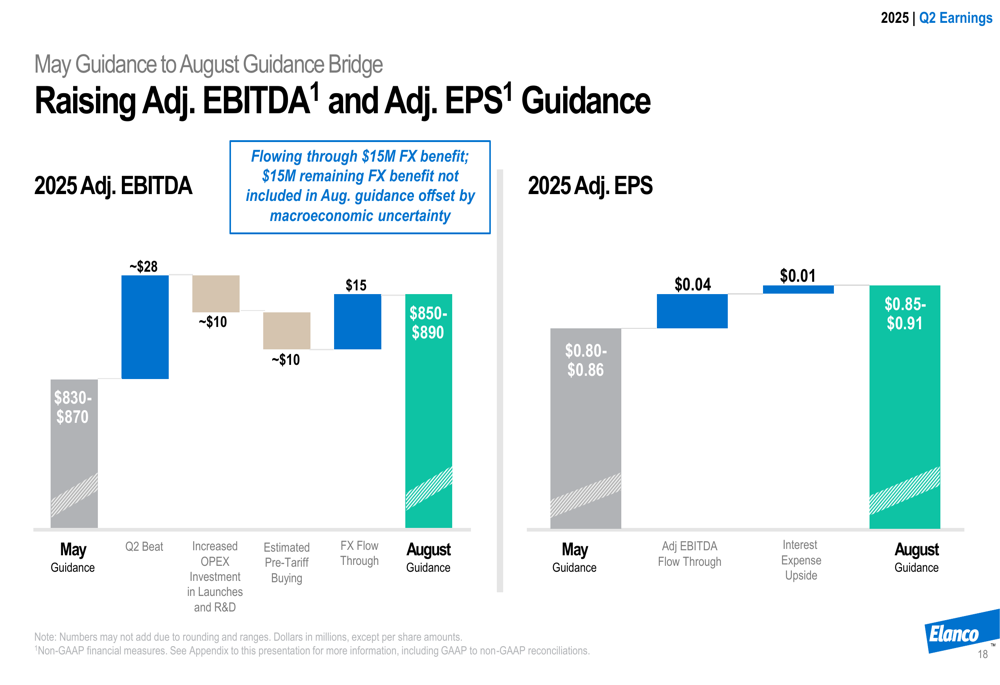

The guidance increase reflects several factors, including the Q2 earnings beat, favorable foreign exchange impacts, and partially offset by increased investments in product launches and R&D:

For Q3 2025, Elanco expects revenue between $1,080-$1,110 million, adjusted EBITDA of $160-$180 million, and adjusted EPS of $0.12-$0.16.

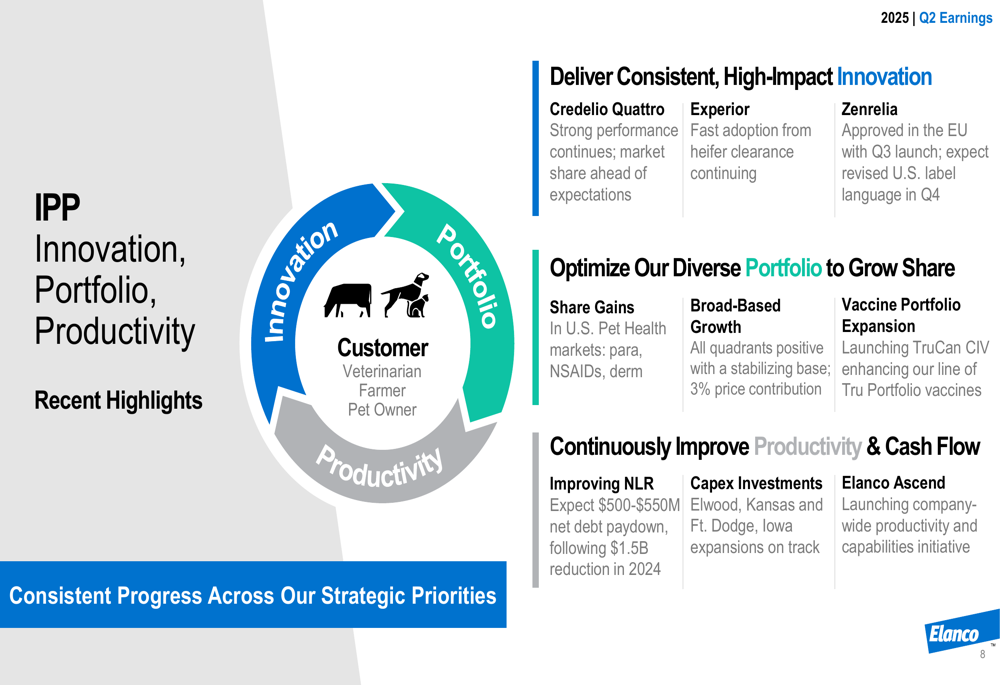

Strategic Initiatives

Elanco’s strategic framework centers around "IPP" - Innovation, Portfolio, and Productivity. The company is focusing on driving sustainable topline growth through its innovation pipeline while optimizing its existing portfolio and improving operational efficiency:

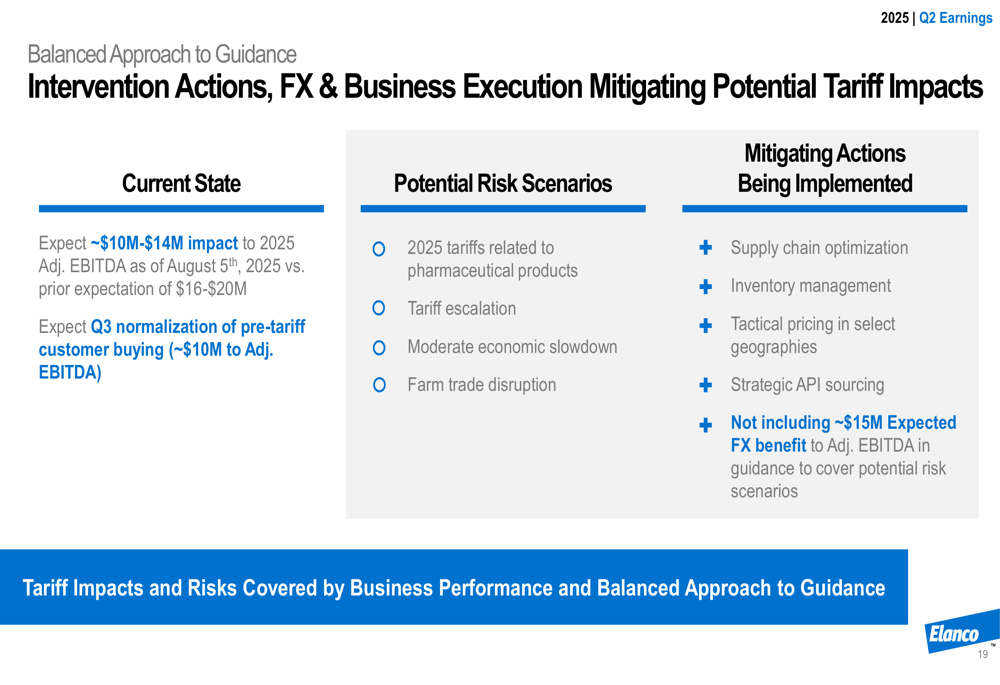

The company is also taking a balanced approach to mitigating potential tariff impacts, which are currently estimated at $10-$14 million for 2025. Mitigation strategies include supply chain optimization, inventory management, tactical pricing, and strategic API sourcing:

Forward-Looking Statements

Looking ahead, Elanco sees itself well-positioned for sustainable revenue growth in 2025 and beyond, building on the foundation established since becoming a pure-play animal health company in 2018. The company’s strategic trajectory emphasizes multiple potential blockbuster products in the market and a stabilizing business base driving growth.

Elanco’s management remains focused on execution in a dynamic environment, echoing CEO Jeff Simmons’ statement from the Q1 earnings call that "Elanco is an execution story." The Q2 results demonstrate the company’s ability to deliver on its strategic priorities while navigating potential headwinds from tariffs and macroeconomic challenges.

With the raised guidance and accelerating organic growth, Elanco appears to be gaining momentum as it progresses through 2025, though investors will be watching closely to see if the company can maintain this trajectory in the face of potential tariff escalations and competitive pressures in both the pet health and farm animal markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.