Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Elevance Health Inc (NYSE:ELV) presented its first quarter 2025 earnings results on April 22, showing strong revenue growth despite ongoing pressure from medical costs. The healthcare giant reported double-digit increases in both revenue and adjusted earnings per share, while reaffirming its full-year outlook.

The company’s stock closed at $406.69 on April 21, 2025, down 4.2% from the previous session, and was trading down an additional 0.93% in pre-market activity. Elevance Health shares have traded between $362.21 and $567.26 over the past 52 weeks, indicating significant volatility in investor sentiment.

Quarterly Performance Highlights

Elevance Health reported first quarter operating revenue of $48.8 billion, representing a 15.4% increase from $42.3 billion in the same period last year. Adjusted diluted earnings per share grew 10.5% to $11.97, up from $10.83 in Q1 2024.

As shown in the following comprehensive financial performance table:

The company’s medical loss ratio (MLR) increased 80 basis points year-over-year to 86.4%, reflecting higher healthcare costs. However, this was partially offset by improvements in the adjusted operating expense ratio, which decreased 60 basis points to 10.7%. Net investment income showed strong growth of 26.9%, reaching $590 million.

Operating cash flow decreased significantly from $2.0 billion in Q1 2024 to $1.0 billion in Q1 2025. Despite this reduction, the company returned $1.3 billion to shareholders during the quarter.

Segment Analysis: Health Benefits vs. Health Services

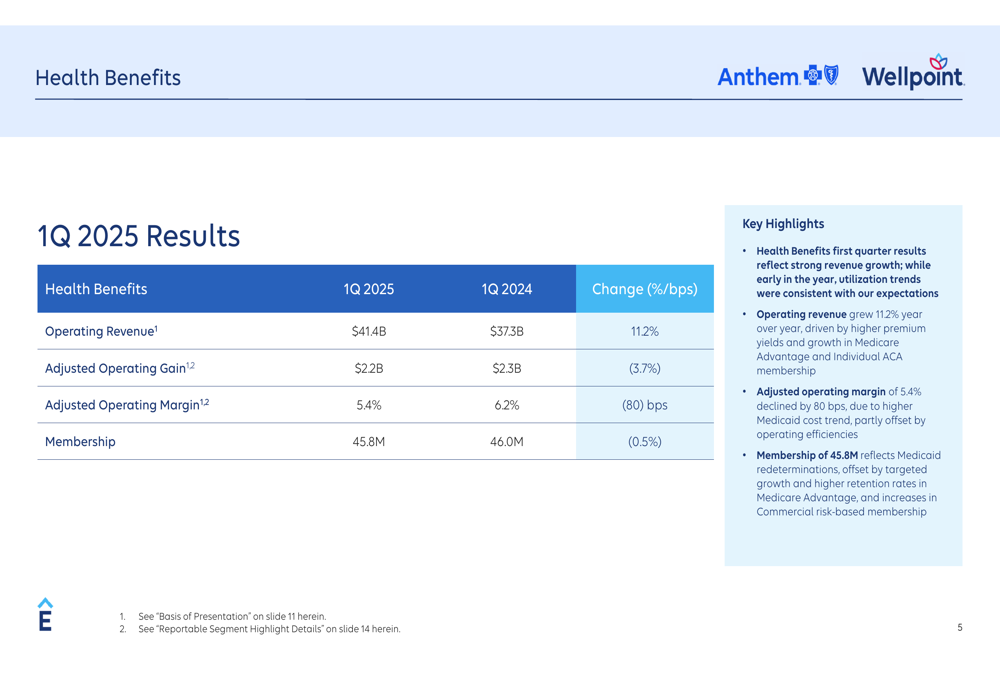

Elevance Health’s performance showed divergent trends across its two main business segments. The Health Benefits segment, which includes Anthem and Wellpoint branded insurance products, reported operating revenue of $41.4 billion, an 11.2% increase year-over-year. However, adjusted operating gain decreased by 3.7% to $2.2 billion, and adjusted operating margin declined 80 basis points to 5.4%.

The Health Benefits segment data reveals these contrasting trends:

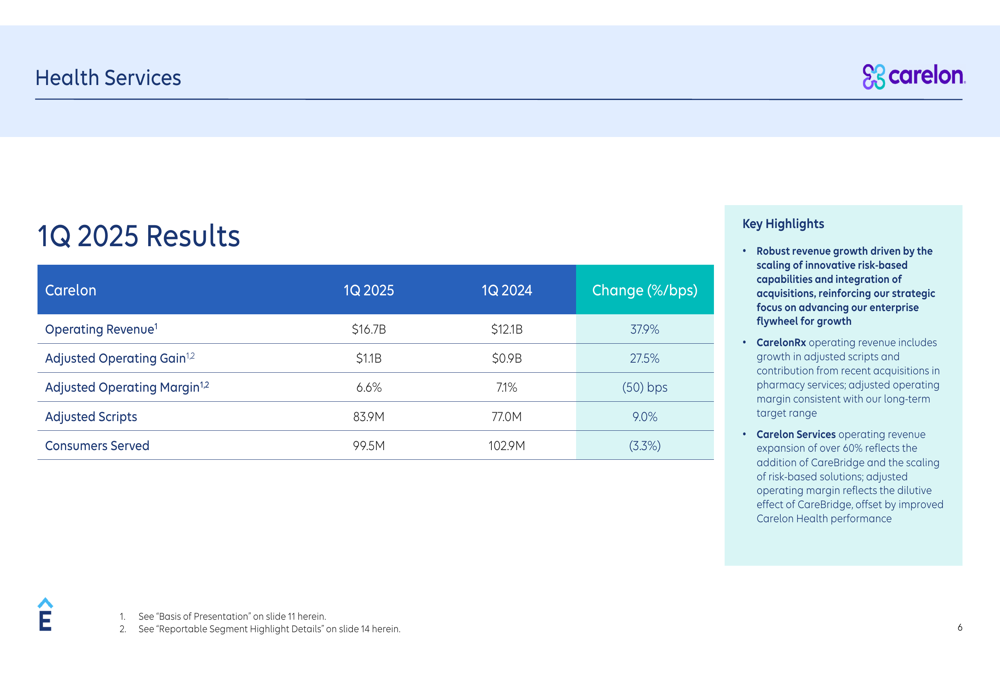

Meanwhile, the Health Services segment, operated under the Carelon brand, demonstrated robust growth. Operating revenue surged 37.9% to $16.7 billion, while adjusted operating gain increased 27.5% to $1.1 billion. Adjusted scripts grew 9.0% to 83.9 million, though the segment’s adjusted operating margin decreased slightly by 50 basis points to 6.6%.

The Carelon segment’s strong performance is illustrated in the following metrics:

The company highlighted that Carelon’s robust revenue growth was driven by "the scaling of innovative risk-based capabilities and integration of acquisitions," reinforcing the strategic focus on advancing the enterprise’s growth flywheel.

Strategic Initiatives & Long-Term Growth

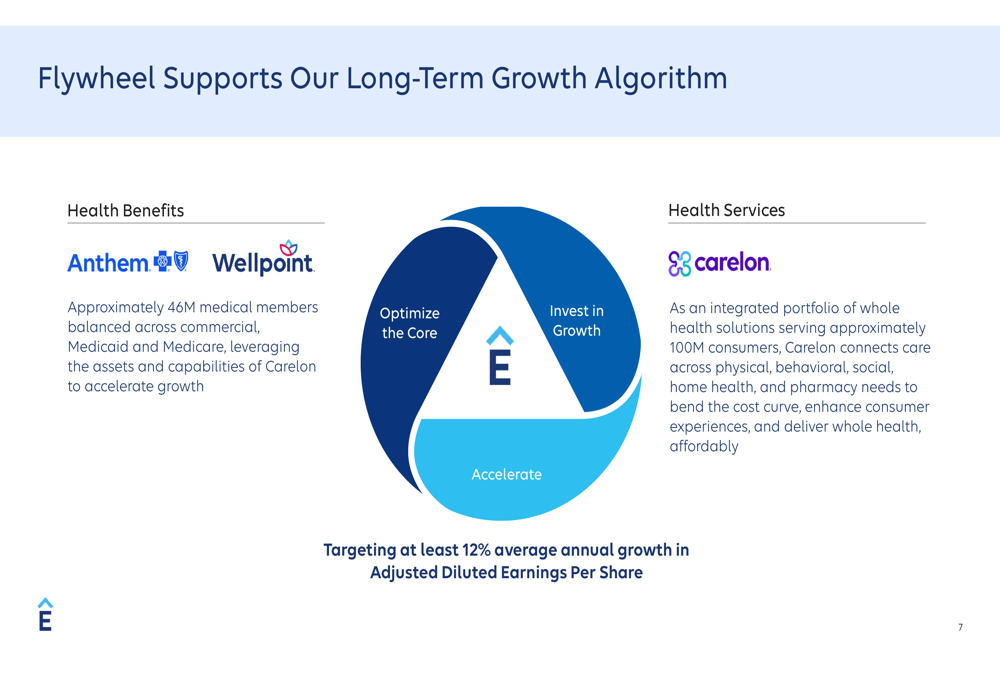

Elevance Health emphasized its long-term growth strategy, which centers on what it calls a "flywheel" approach that leverages the complementary nature of its Health Benefits and Carelon businesses. The company serves approximately 46 million medical members across commercial, Medicaid, and Medicare segments, while Carelon provides whole health solutions to approximately 100 million consumers.

The company’s growth flywheel is visualized in this strategic framework:

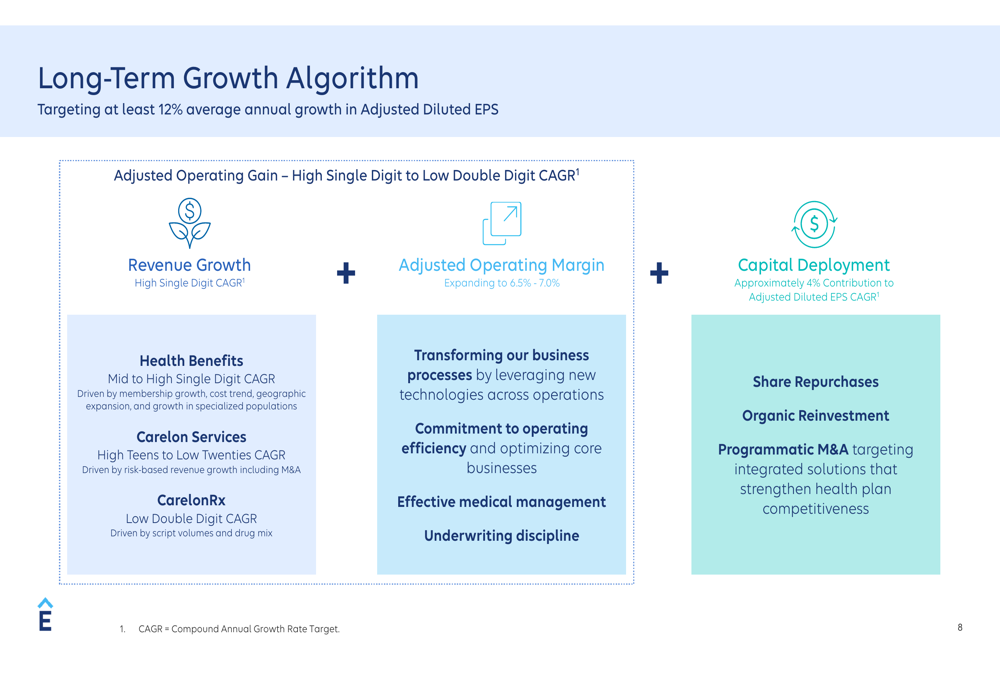

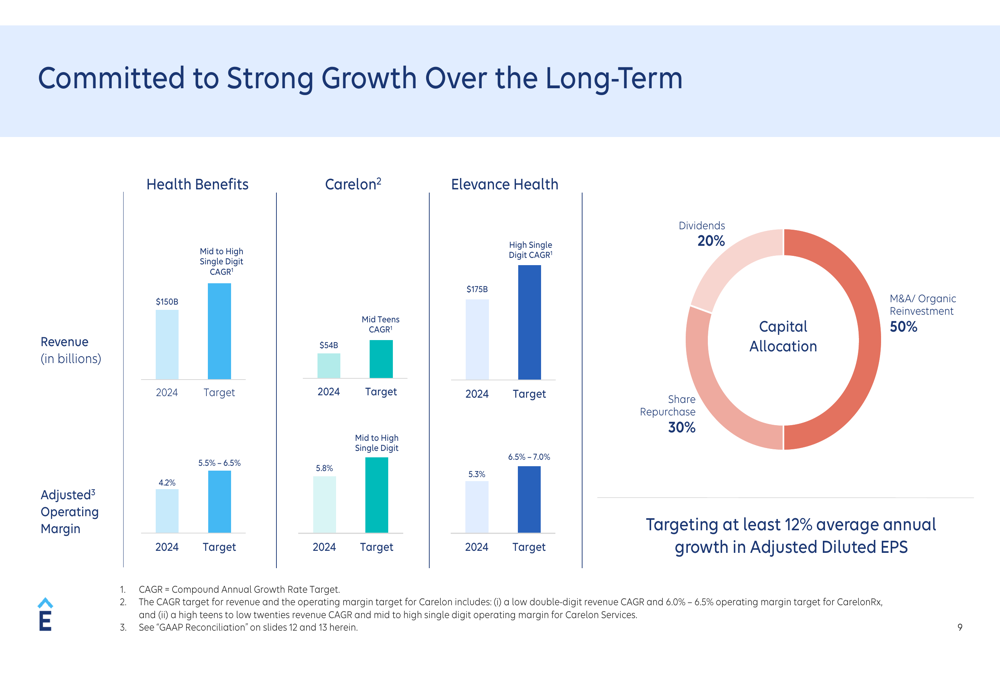

Elevance Health’s long-term growth algorithm targets at least 12% average annual growth in adjusted diluted earnings per share. This growth is expected to be driven by high single-digit revenue growth, expanding operating margins to 6.5%-7.0%, and strategic capital deployment.

The detailed breakdown of this growth algorithm is shown here:

The company’s capital allocation strategy allocates 50% to M&A and organic reinvestment, 30% to share repurchases, and 20% to dividends, as illustrated in this comprehensive long-term growth commitment:

Forward-Looking Statements & Outlook

Elevance Health reaffirmed its full-year 2025 outlook, projecting adjusted diluted earnings per share to be in the range of $34.15 to $34.85. The company expects slightly more than 60% of its full-year adjusted diluted EPS to be realized in the first half of 2025, suggesting some moderation in growth during the second half of the year.

The company continues to focus on strategic investments to transform the healthcare experience, including patient advocacy, HealthOS, and value-based oncology care models. These initiatives aim to deliver personalized experiences while advancing the company’s long-term strategy for sustainable growth.

This outlook represents a significant improvement from the company’s performance in the third quarter of 2024, when Elevance Health reported adjusted EPS of $8.37, which fell short of analyst expectations. At that time, the company had reduced its full-year 2024 EPS guidance to approximately $33, primarily due to challenges in its Medicaid business.

The first quarter 2025 results suggest that Elevance Health has successfully navigated the Medicaid cost challenges that affected its performance in 2024, while continuing to drive strong growth through its integrated health services strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.