Oil prices extend losses as traders downplay Russia sanction risks

Introduction & Market Context

Enact Holdings Inc (NYSE:NASDAQ:ACT), a leading private mortgage insurance provider, presented its first quarter 2025 financial results on April 30, 2025, showcasing solid performance despite ongoing challenges in the housing market. The company navigated a complex market environment characterized by low affordability and tight housing supply, while maintaining strong financial metrics and enhancing shareholder returns.

Enact’s stock closed at $35.50 on April 30, 2025, and remained stable in aftermarket trading, reflecting investor confidence in the company’s performance and strategic direction. The mortgage insurance industry continues to benefit from favorable underpinnings including a healthy labor market and strong first-time homebuyer demographics, despite near-term pressures from elevated mortgage rates.

Quarterly Performance Highlights

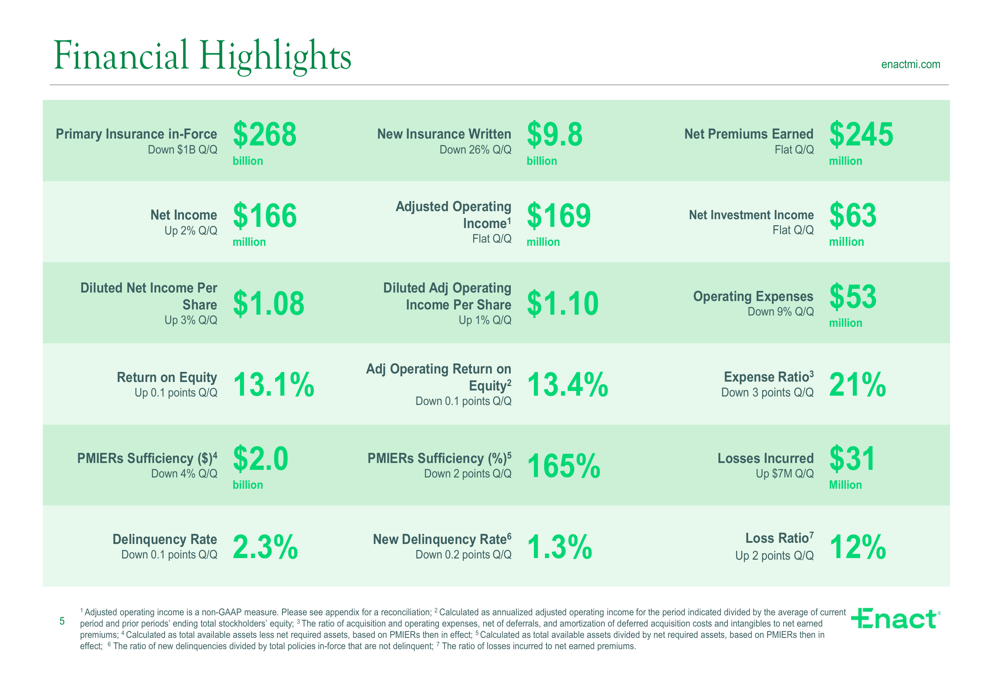

Enact reported net income of $166 million for Q1 2025, up 2% quarter-over-quarter, with diluted earnings per share of $1.08, representing a 3% increase from the previous quarter. Adjusted operating income remained flat at $169 million, with adjusted operating income per share of $1.10, up 1% from Q4 2024.

As shown in the comprehensive financial highlights chart below, the company maintained strong returns with a return on equity of 13.1% and adjusted operating return on equity of 13.4%:

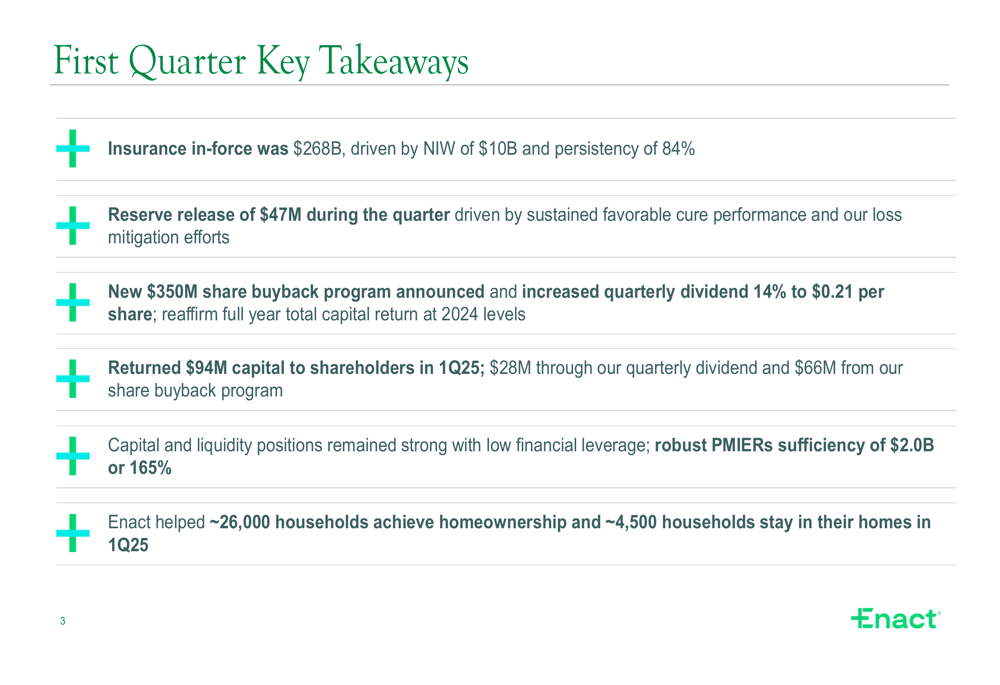

Insurance in-force stood at $268 billion, while new insurance written was $9.8 billion, down 26% quarter-over-quarter primarily due to seasonality of purchase originations. The company’s persistency rate remained elevated at 84%, helping to offset the impact of higher mortgage rates on production.

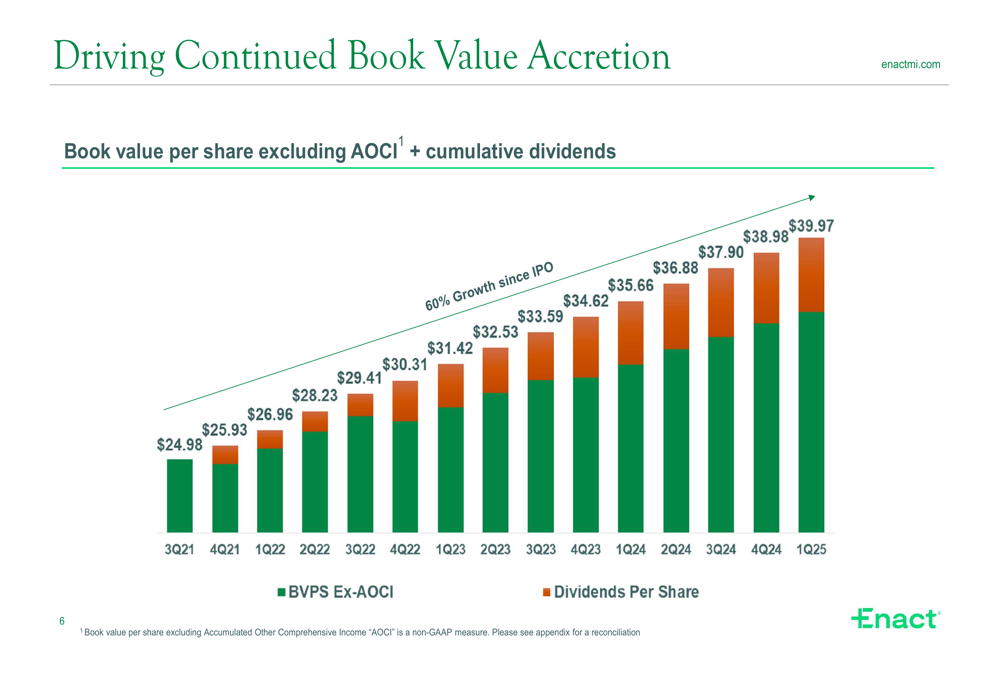

Enact’s book value per share excluding accumulated other comprehensive income continued its steady growth trajectory, reaching $39.97 in Q1 2025, up from $38.98 in Q4 2024. This consistent growth demonstrates the company’s ability to generate shareholder value over time, as illustrated in the following chart:

Capital Management and Shareholder Returns

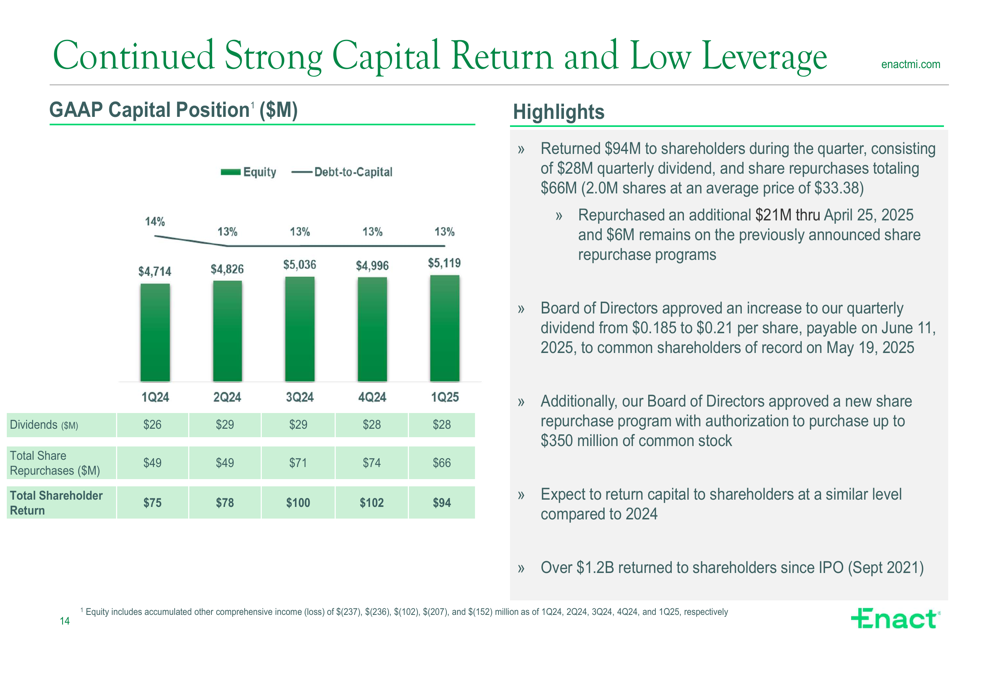

Enact maintained a strong focus on capital return to shareholders during the quarter, returning a total of $94 million through dividends and share repurchases. This included $28 million in quarterly dividends and $66 million in share buybacks, with 2.0 million shares repurchased at an average price of $33.38.

The company’s board approved a 14% increase to the quarterly dividend, raising it from $0.185 to $0.21 per share, payable on June 11, 2025. Additionally, a new share repurchase program with authorization to purchase up to $350 million of common stock was announced, underscoring Enact’s commitment to returning capital to shareholders.

The following chart illustrates Enact’s consistent capital return strategy and strong capital position with a low debt-to-capital ratio of 13%:

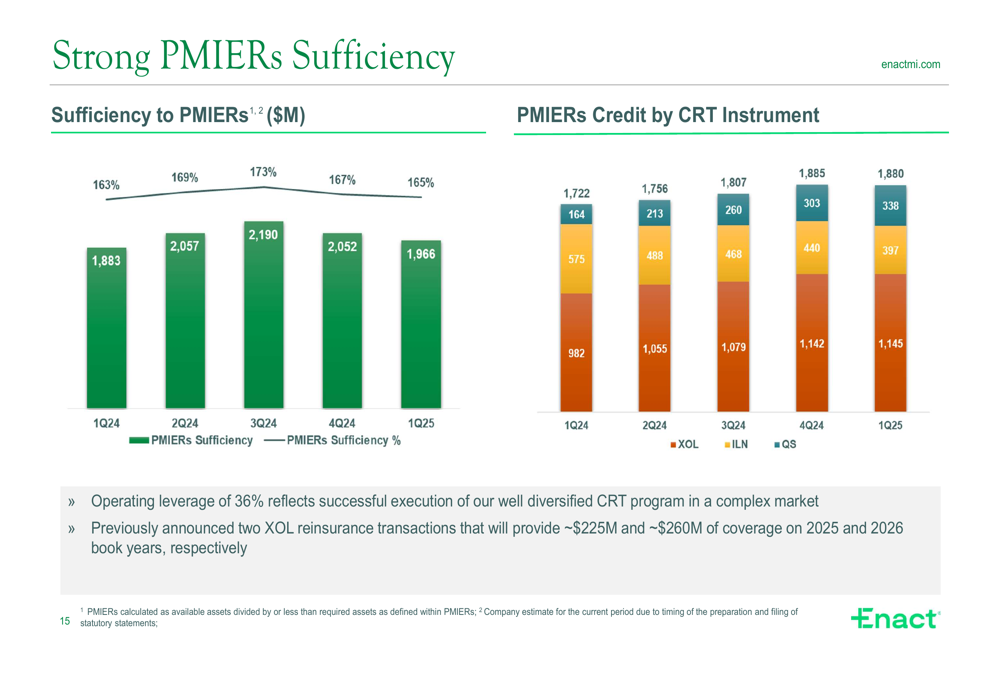

Enact’s capital position remains robust, with PMIERs sufficiency of $2.0 billion or 165%, providing ample flexibility for capital deployment while maintaining regulatory compliance. The company has returned over $1.2 billion to shareholders since its IPO in September 2021 and expects to maintain similar capital return levels in 2025 compared to 2024.

Credit Performance and Risk Management

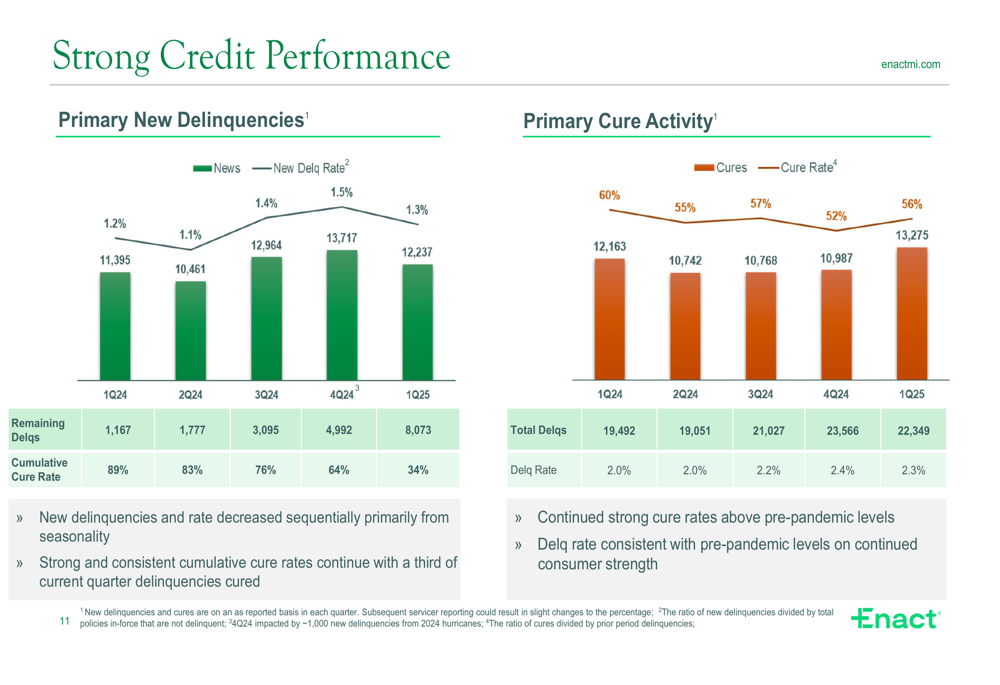

Enact demonstrated strong credit performance in Q1 2025, with a delinquency rate of 2.3%, down 0.1 percentage points from the previous quarter. New delinquencies decreased sequentially to 12,237 (1.3% rate) from 13,717 (1.5% rate) in Q4 2024, primarily due to seasonality. The company continued to experience strong cure rates at 56%, above pre-pandemic levels.

The following chart illustrates Enact’s delinquency trends and cure activity:

Losses incurred were $31 million in Q1 2025, resulting in a loss ratio of 12%, up from 10% in the previous quarter. This increase was primarily driven by a lower reserve release of $47 million compared to $56 million in Q4 2024. The reserve release was attributed to favorable cure performance and loss mitigation activities.

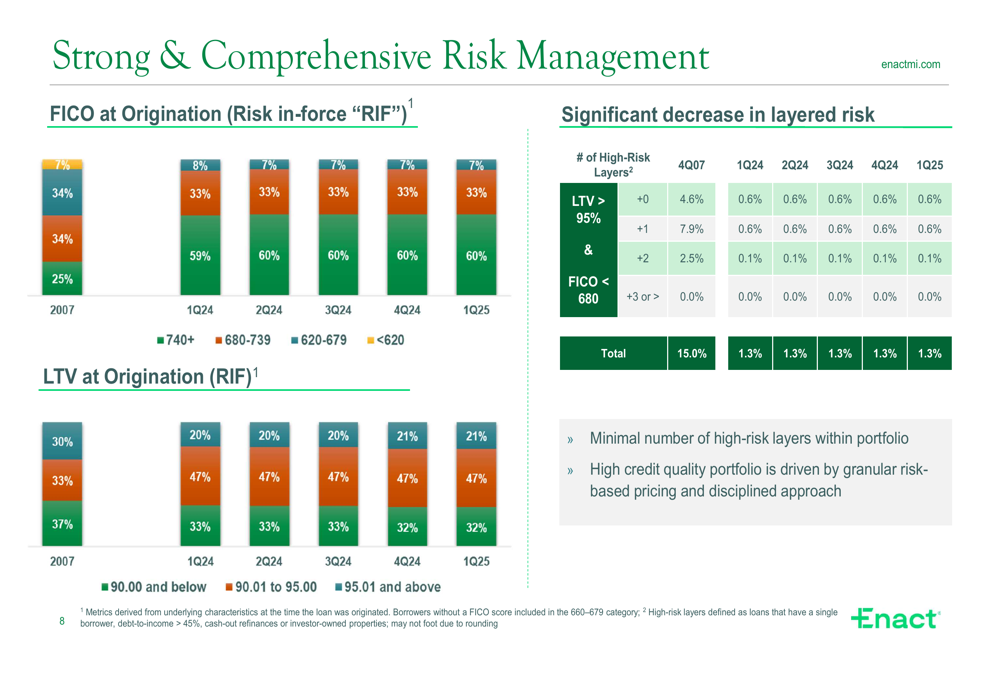

Enact’s risk management approach has resulted in a high-quality credit portfolio, with 93% of delinquent policies having at least 10% equity. The company’s comprehensive risk management is reflected in the distribution of FICO scores and loan-to-value ratios in its portfolio:

Forward-Looking Statements

Enact’s market outlook acknowledges near-term challenges in the housing market due to low affordability but highlights several favorable underpinnings. Tight housing supply continues to support home prices, while a healthy labor market and generally healthy household balance sheets support credit performance. Long-term demand dynamics remain favorable, driven by strong first-time homebuyer demographics.

The company is well-positioned to navigate a range of economic scenarios with its high-quality credit portfolio, strong capital position, and ability to adapt to market changes with granular risk-based pricing models. Enhanced credit protections from robust and diversified credit risk transfer programs provide additional resilience.

Enact reaffirmed its commitment to return capital to shareholders at levels similar to 2024, supported by its strong capital and liquidity positions. The company’s strategic focus remains on driving profitable growth in the mortgage insurance market, transforming its business to maximize value and efficiency, generating shareholder value by leveraging core capabilities, and driving an exceptional employee experience.

In Q1 2025, Enact helped approximately 26,000 households achieve homeownership and around 4,500 households stay in their homes, demonstrating its commitment to its mission of enabling the dream of homeownership.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.