Fed Governor Adriana Kugler to resign

Introduction & Market Context

Energizer Holdings Inc (NYSE:ENR) presented its Q2 fiscal 2025 earnings results on May 6, 2025, revealing mixed performance as the company navigates global supply chain challenges. The battery manufacturer’s shares were already under pressure, falling 2.12% to close at $25.88 on May 5, with premarket trading on presentation day showing a further 5.33% decline to $24.50, suggesting investors’ concerns about the company’s revised outlook.

The quarterly results come as Energizer continues to implement strategic supply chain initiatives aimed at reducing dependency on Chinese manufacturing and mitigating tariff impacts, while also managing its debt structure in a challenging economic environment.

Quarterly Performance Highlights

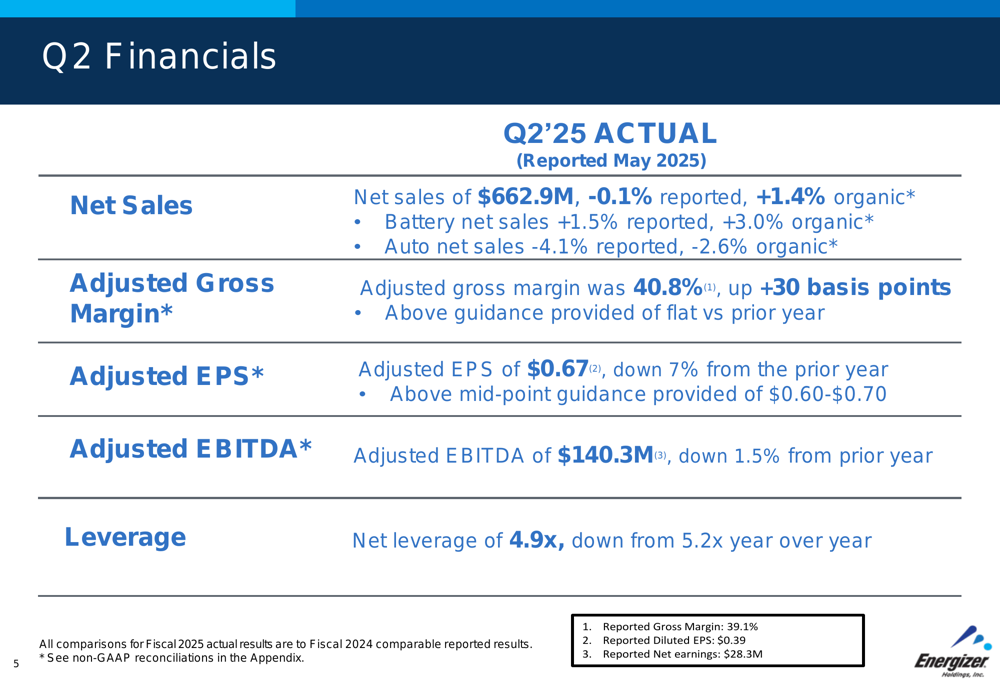

Energizer reported Q2 fiscal 2025 net sales of $662.9 million, representing a slight 0.1% decrease on a reported basis but a 1.4% increase on an organic basis. The company’s performance was driven by contrasting results across its business segments.

The Battery segment showed positive momentum with net sales increasing 1.5% on a reported basis and 3.0% organically. However, this growth was offset by weakness in the Auto Care segment, which declined 4.1% on a reported basis and 2.6% organically.

As shown in the following financial results summary:

Adjusted gross margin reached 40.8%, up 30 basis points compared to the prior year and exceeding the company’s guidance of flat year-over-year performance. Adjusted earnings per share came in at $0.67, down 7% from the prior year but above the midpoint of the previously provided guidance range of $0.60-$0.70.

Adjusted EBITDA declined slightly to $140.3 million, representing a 1.5% decrease from the prior year. On a positive note, the company reduced its net leverage to 4.9x, down from 5.2x year-over-year, indicating progress in managing its debt load.

Strategic Supply Chain Initiatives

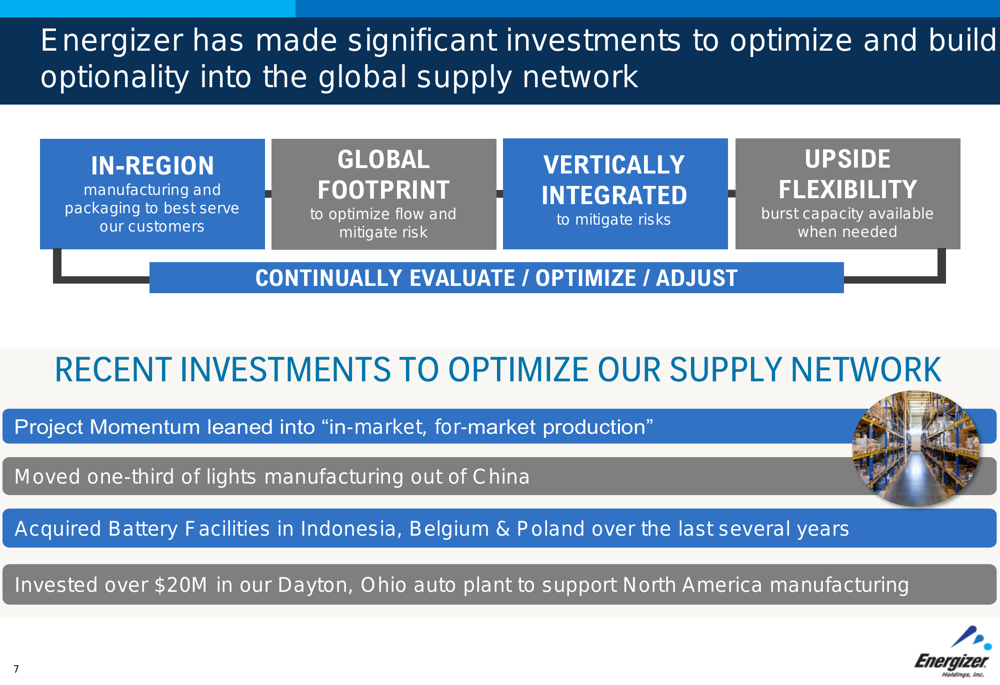

A significant portion of Energizer’s presentation focused on the company’s efforts to optimize its global supply network, particularly in response to tariff pressures and the need for manufacturing flexibility.

The company highlighted four key elements of its supply strategy: in-region manufacturing and packaging, global footprint optimization, vertically integrated operations, and upside flexibility to handle burst capacity. Energizer emphasized that it "continually evaluates, optimizes, and adjusts" its supply network to maintain competitiveness.

The following slide illustrates these strategic initiatives:

Recent investments include Project Momentum, moving one-third of lights manufacturing out of China, acquiring battery facilities in Indonesia, Belgium, and Poland, and investing over $20 million in the Dayton, Ohio auto plant. These moves are designed to create more supply chain resilience and reduce dependency on any single manufacturing region.

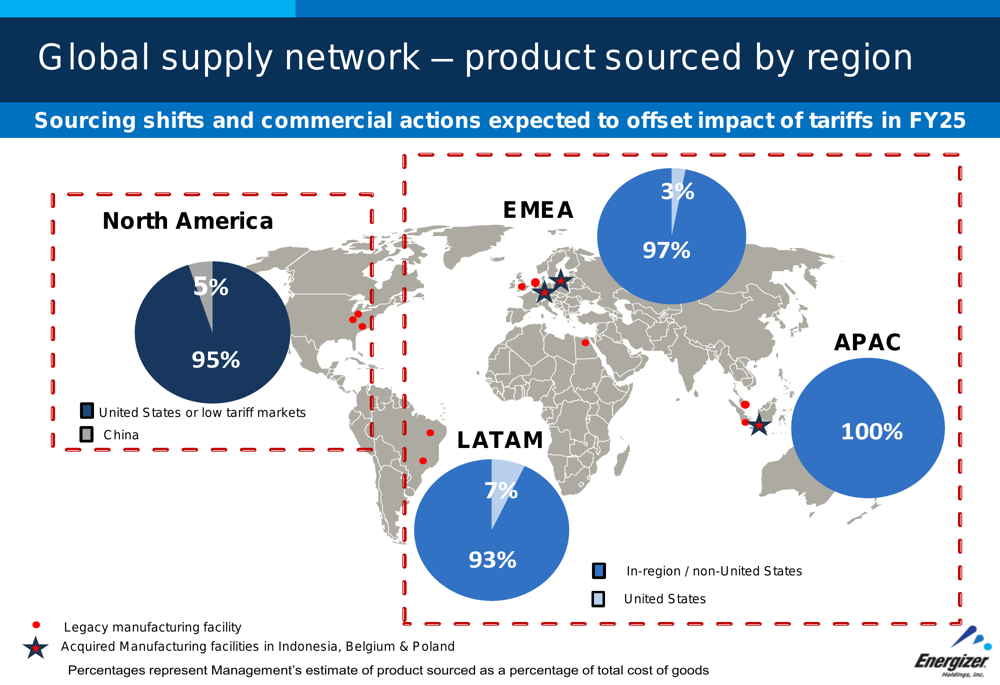

The company also provided a detailed breakdown of its sourcing by region, highlighting the significant portion of products still sourced from China and other high-tariff markets:

This visualization demonstrates Energizer’s current supply chain exposure and the opportunity for further diversification to mitigate tariff impacts across its global operations.

Updated Guidance & Outlook

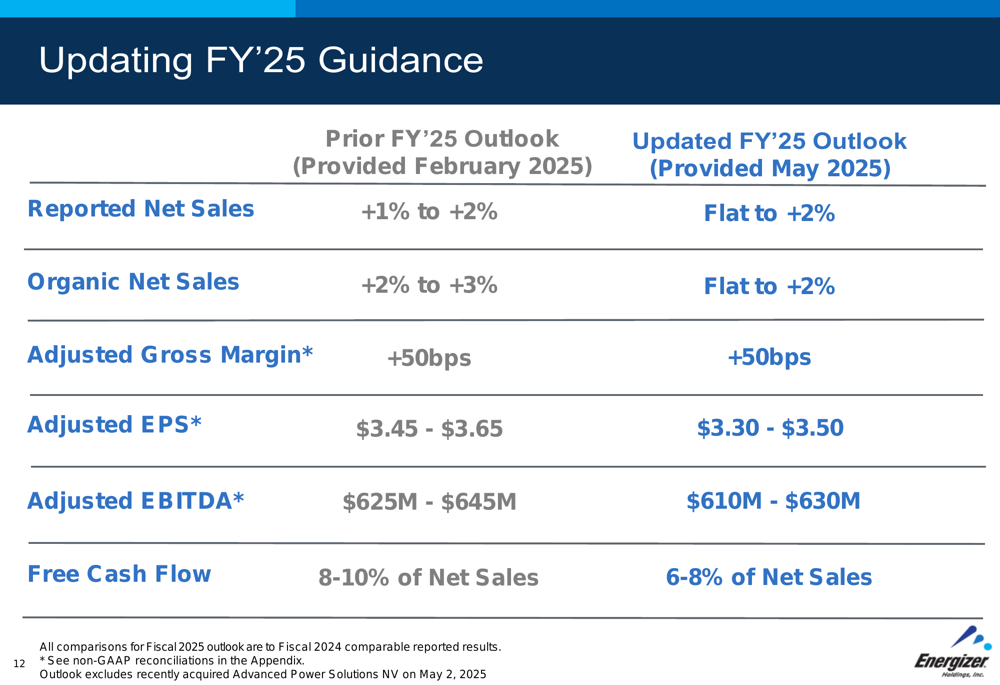

In a move that likely contributed to the negative market reaction, Energizer revised its full-year fiscal 2025 guidance downward across several key metrics. The updated outlook reflects ongoing challenges in the operating environment.

The revised guidance compared to previous projections is detailed in the following slide:

Most notably, Energizer reduced its organic net sales growth projection from 2-3% to 0-2%, adjusted EPS from $3.45-$3.65 to $3.30-$3.50, and adjusted EBITDA from $625-645 million to $610-630 million. Free cash flow expectations were also lowered from 8-10% of net sales to 6-8%.

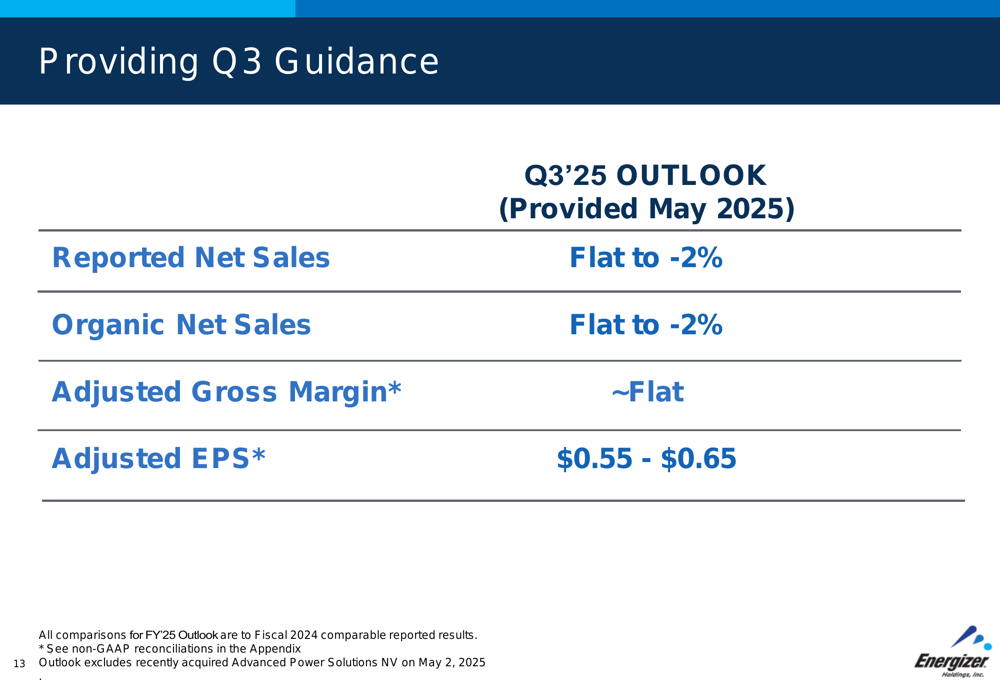

For the upcoming third quarter, Energizer provided a cautious outlook:

The Q3 guidance projects flat to negative 2% growth in both reported and organic net sales, with flat adjusted gross margins and adjusted EPS between $0.55 and $0.65. The company noted that this outlook excludes the impact of the recently acquired Advanced Power Solutions NV, which was completed on May 2, 2025.

Debt Management & Capital Structure

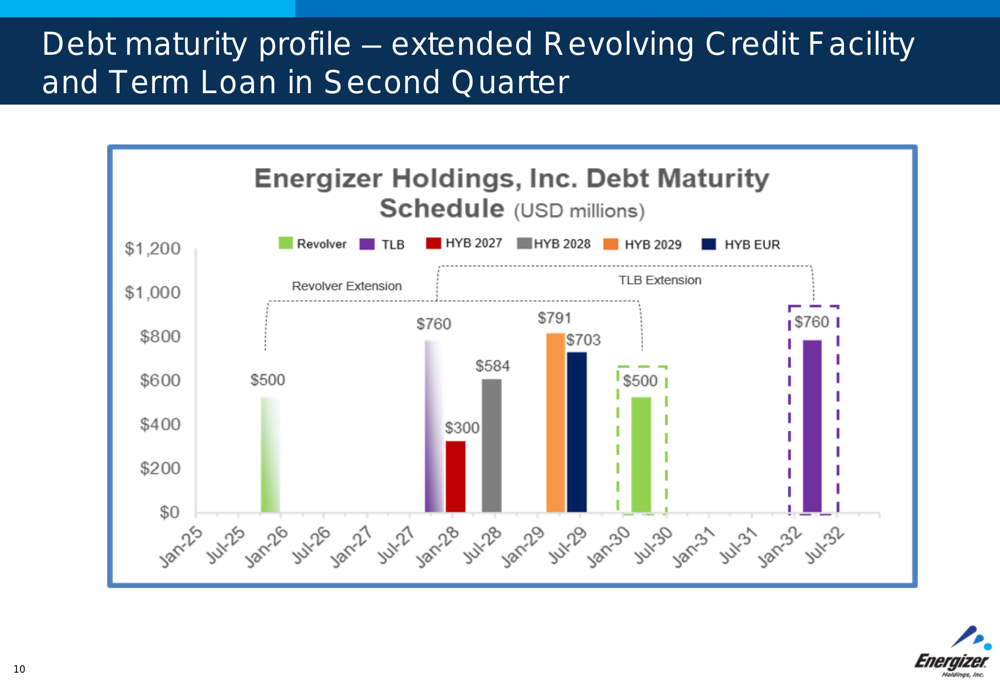

Energizer also addressed its debt maturity profile, providing visibility into upcoming obligations and refinancing needs. The company’s debt instruments span from January 2025 to July 2032, with various amounts coming due at different intervals.

The following chart illustrates the company’s debt maturity schedule:

This visualization shows Energizer’s debt obligations, including revolving credit facilities, term loans, and high-yield bonds. The company has been working to manage its leverage, as evidenced by the reduction in net leverage ratio from 5.2x to 4.9x year-over-year.

Conclusion

Energizer’s Q2 fiscal 2025 results present a mixed picture. While the company exceeded its quarterly guidance on adjusted gross margin and EPS, the downward revision of full-year projections signals ongoing challenges. The Battery segment continues to show resilience with organic growth, but weakness in the Auto Care business remains a concern.

The company’s strategic focus on supply chain optimization and debt management demonstrates proactive measures to address external pressures, particularly related to tariffs and manufacturing dependencies. However, the market’s negative reaction, as evidenced by the stock’s decline, suggests investors remain cautious about Energizer’s near-term prospects despite these initiatives.

As Energizer moves forward, the effectiveness of its supply chain restructuring and its ability to stabilize and grow the Auto Care segment will likely be key factors in determining whether the company can return to more robust growth and meet its revised financial targets for fiscal 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.