e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Introduction & Market Context

The Ensign Group, Inc. (NASDAQ:ENSG) recently presented its November 2025 investor presentation following strong third-quarter results that exceeded analyst expectations. The post-acute care provider continues to demonstrate robust growth across its portfolio of healthcare facilities, with shares rising 1.09% to $183.88 following its earnings release on November 4, 2025.

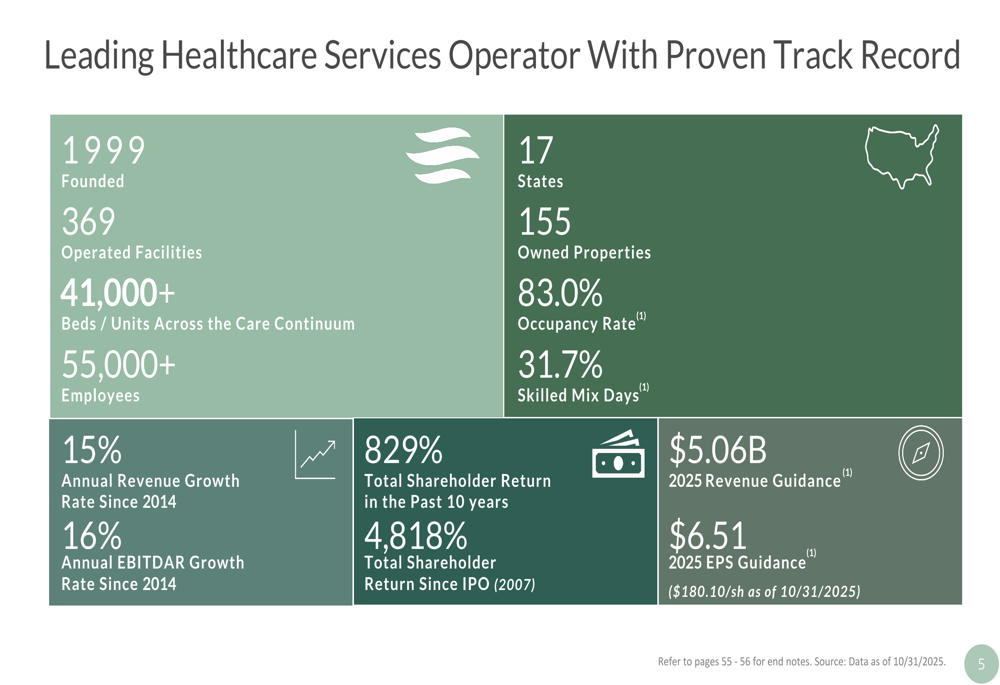

Founded in 1999, Ensign has established itself as a leading operator in the post-acute care sector, with a substantial footprint across 17 states. The company’s business model emphasizes clinical excellence, local leadership, and strategic acquisitions as key drivers of growth.

As shown in the following comprehensive overview of the company’s key metrics, Ensign operates 369 facilities with more than 41,000 beds/units and employs over 55,000 people:

Quarterly Performance Highlights

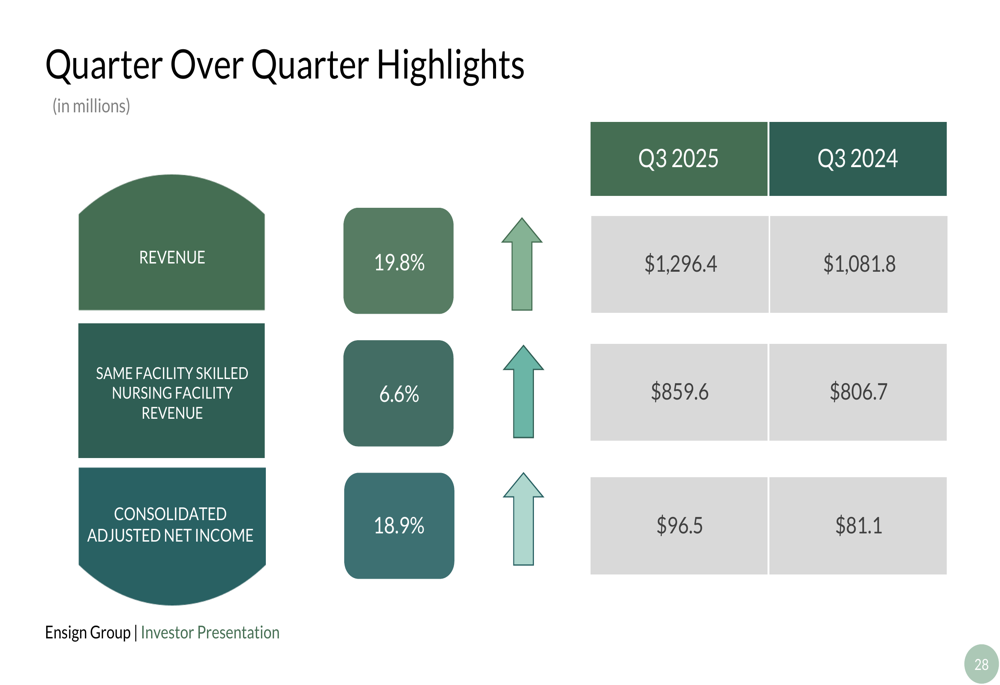

Ensign reported impressive financial results for Q3 2025, with revenue reaching $1.3 billion, representing a 19.8% increase compared to the same period in 2024. This exceeded analyst expectations of $1.28 billion. The company’s adjusted earnings per share of $1.64 also surpassed the forecast of $1.61, resulting in a positive surprise of 1.86%.

Same facility skilled nursing revenue increased by 6.6% year-over-year, while consolidated adjusted net income grew by 18.9% to $96.5 million. These strong results reflect Ensign’s ability to improve operational performance across its portfolio, particularly in recently acquired facilities.

The following chart illustrates the quarter-over-quarter highlights, showing the significant growth in key financial metrics:

Year-to-date performance has been equally impressive, with revenue increasing by 18.2% to $3.7 billion and consolidated adjusted net income rising by 19.7% to $278.8 million compared to the first nine months of 2024.

Strategic Initiatives

Ensign’s investment thesis centers on delivering superior clinical results, which in turn drive strong financial performance. The company’s strategy is built around several interconnected elements, including clinical excellence, strategic positioning across the care continuum, and a distinctive corporate culture.

The following visual representation highlights the key components of Ensign’s investment approach:

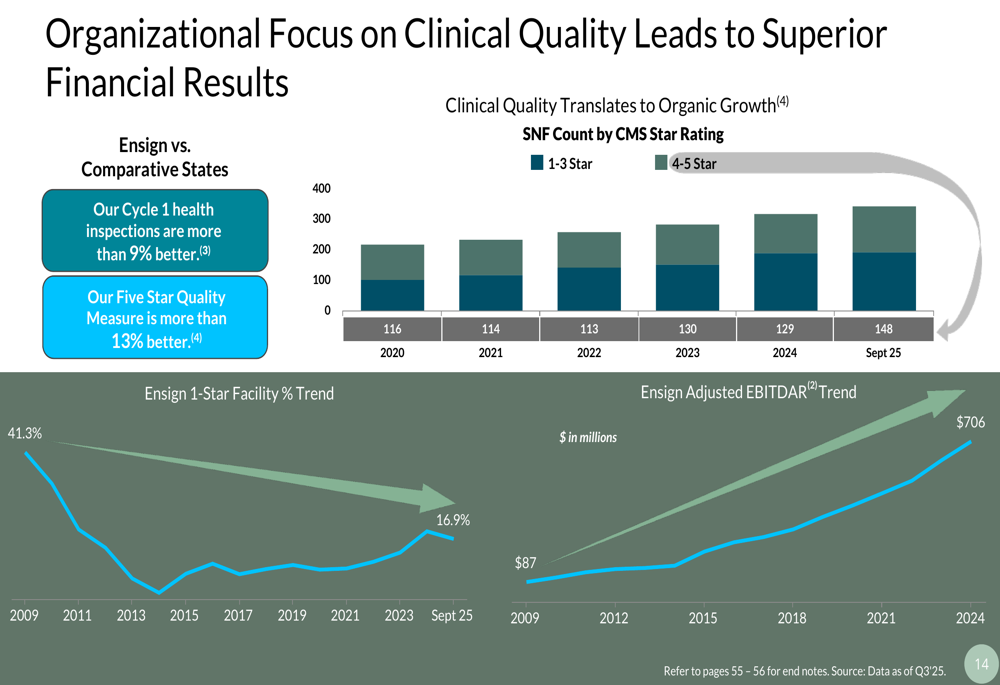

A cornerstone of Ensign’s strategy is its focus on clinical quality as a competitive differentiator. During the earnings call, CEO Barry Port emphasized that "clinical performance continues to be the key differentiator for us." This focus is evident in the company’s superior CMS star ratings compared to industry peers.

The data clearly demonstrates that Ensign’s emphasis on clinical quality translates to superior financial results, as illustrated in this chart showing the relationship between clinical metrics and financial performance:

Ensign employs a "cluster model" that empowers local leadership while providing the benefits of scale. This approach allows for sharing of best practices and resources among geographically proximate facilities, while maintaining the agility of local decision-making.

Growth Strategy & Acquisitions

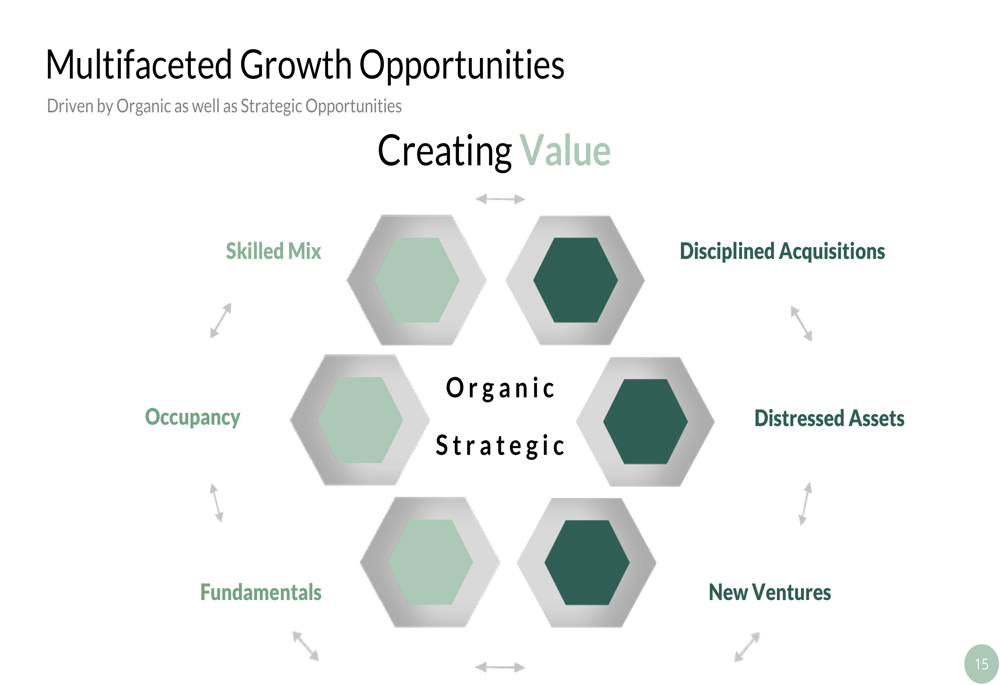

Ensign’s growth strategy encompasses multiple avenues, including organic growth through improved occupancy and skilled mix, strategic acquisitions, real estate investments, and new ventures.

The following diagram illustrates these multifaceted growth opportunities:

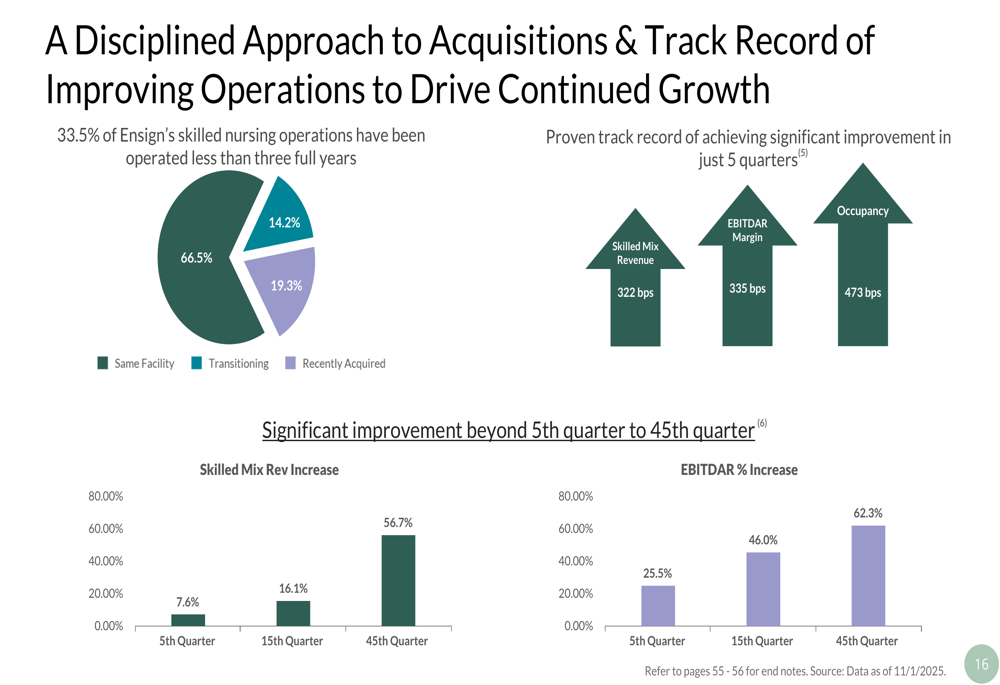

The company has demonstrated a disciplined approach to acquisitions, with a proven track record of improving operations at newly acquired facilities. Ensign reported that 33.5% of its skilled nursing operations have been operated for less than three full years, highlighting the company’s active acquisition strategy.

The presentation showcases how Ensign transforms underperforming assets, with significant improvements in skilled mix revenue, EBITDAR margin, and occupancy over time:

In 2025 alone, Ensign has acquired 45 new operations, expanding into new markets including Alabama and Tennessee. Despite what management described as a "choppy deal environment" during the earnings call, the company continues to find attractive acquisition opportunities in fragmented markets.

Real Estate Portfolio & Standard Bearer REIT

Ensign has developed a significant real estate portfolio, with 29.4% of its 369 facilities owned and operated by the company. The remainder are primarily leased, with 8.9% having purchase options.

The company’s real estate strategy includes Standard Bearer REIT, which was formed in 2022 to separate real estate ownership from operations. Standard Bearer currently owns 149 properties across 16 states, with a real estate fair value of $1.6 billion.

This structure provides increased visibility into real estate value, expands acquisition opportunities, and offers capital flexibility. It also creates optionality for a potential future spin-out of the REIT.

Financial Performance & Outlook

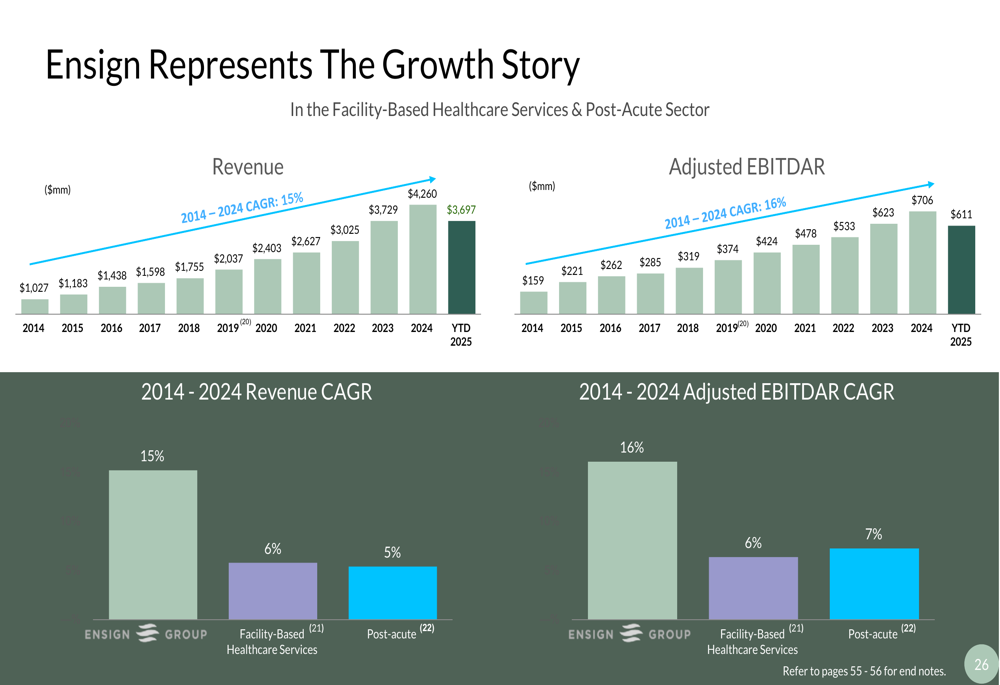

Ensign’s long-term financial performance demonstrates consistent growth, with revenue increasing at a compound annual growth rate of 15% and adjusted EBITDAR growing at 16% since 2014. This track record is illustrated in the following chart:

The company maintains a strong balance sheet with $443.7 million in cash and cash equivalents as of September 30, 2025, and a net debt to adjusted EBITDAR ratio of 1.86x. Cash flow from operations for the first nine months of 2025 was $381.0 million.

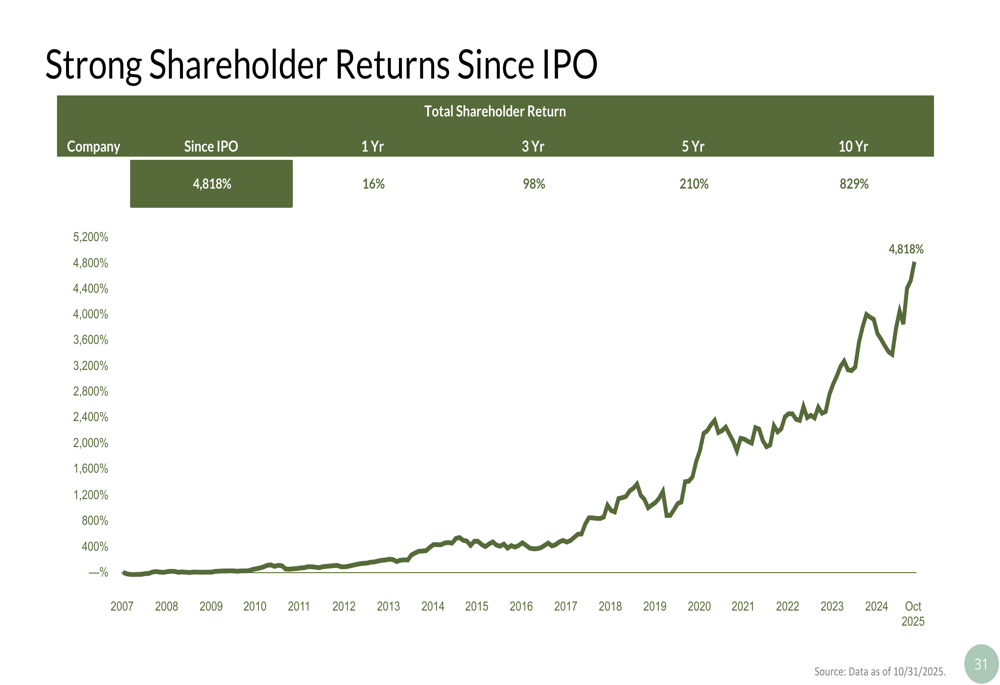

Ensign has delivered exceptional shareholder returns since its IPO in 2007, with a total return of 4,818%. More recent performance remains strong, with 10-year returns of 829% and 3-year returns of 98%:

Forward-Looking Statements

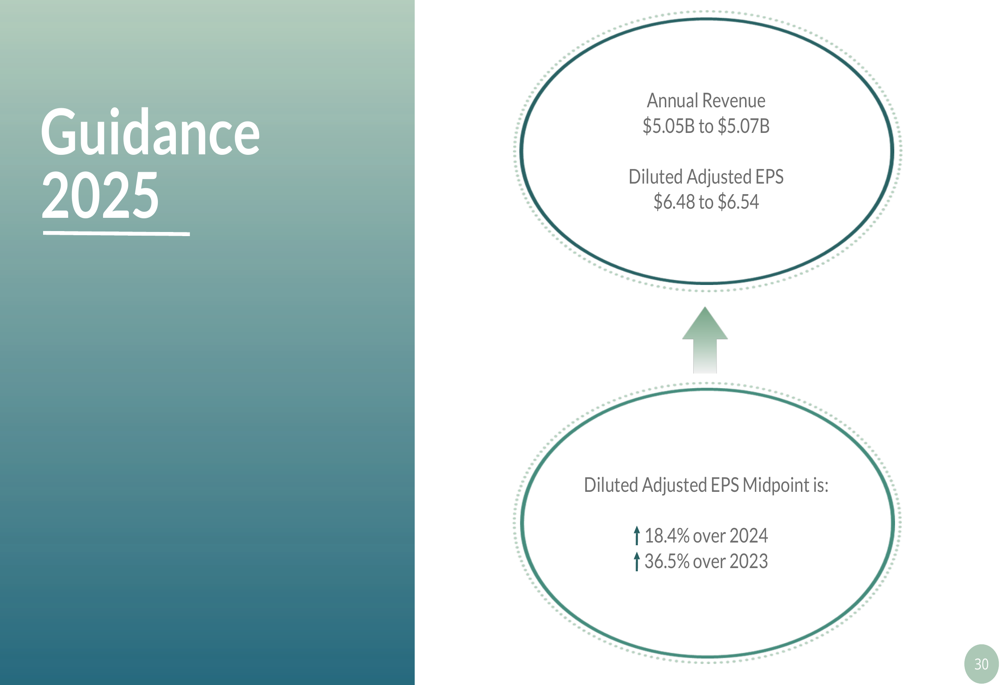

Following the strong Q3 results, Ensign raised its 2025 earnings guidance to $6.48-$6.54 per share, up from previous estimates and representing an 18.4% increase over 2024 results. Annual revenue guidance was also increased to $5.05-$5.07 billion.

The company remains optimistic about future growth, citing favorable industry fundamentals including an aging population, shift to value-based care, and market fragmentation that creates consolidation opportunities. Medicare spending on post-acute care is projected to continue growing, with 44% of post-acute Medicare dollars allocated to skilled nursing facilities.

Ensign’s management expressed confidence in the company’s ability to continue its growth trajectory through both organic improvements and strategic acquisitions, leveraging its proven operational model and focus on clinical excellence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.