These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Entegris Inc (NASDAQ:ENTG) released its second quarter 2025 earnings presentation on July 30, showing sequential revenue improvement but continued year-over-year declines. The semiconductor materials and solutions provider reported mixed results across its business segments, with its stock falling 8.31% in premarket trading to $85.04, extending the negative market reaction that began after its Q1 results.

The latest quarterly performance comes amid ongoing challenges in the semiconductor industry, including concerns about China tariffs that were highlighted during the company’s previous earnings call, where management had warned of potential revenue impacts of up to $50 million.

Quarterly Performance Highlights

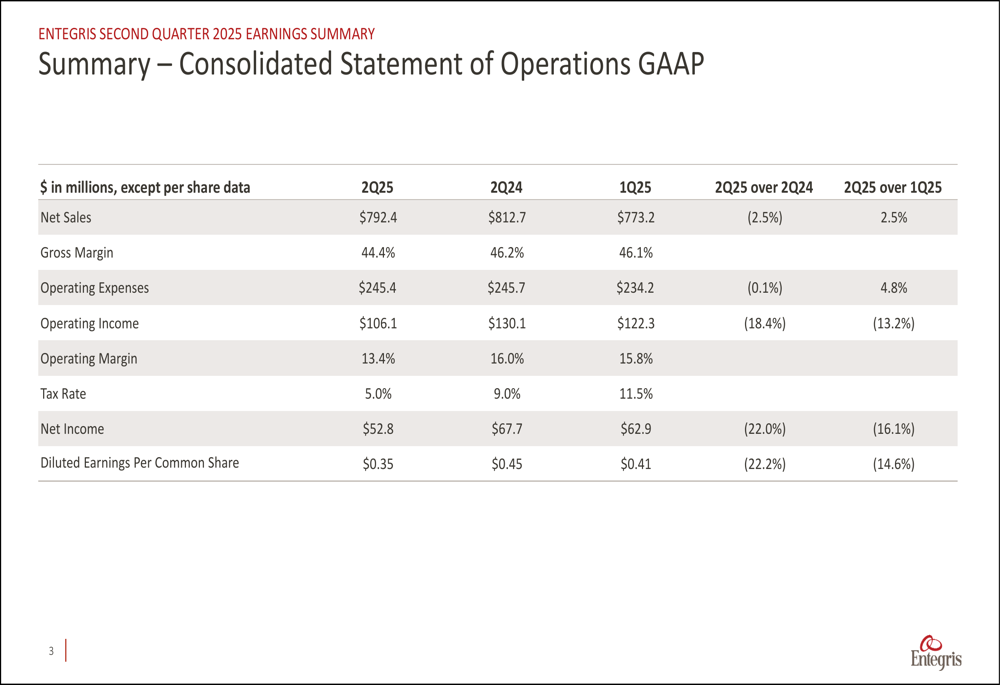

Entegris reported Q2 2025 net sales of $792.4 million, representing a 2.5% decline year-over-year but a 2.5% improvement sequentially. The company’s GAAP operating income fell to $106.1 million, down 18.4% from the same period last year and 13.2% from the previous quarter.

As shown in the following consolidated statement of operations:

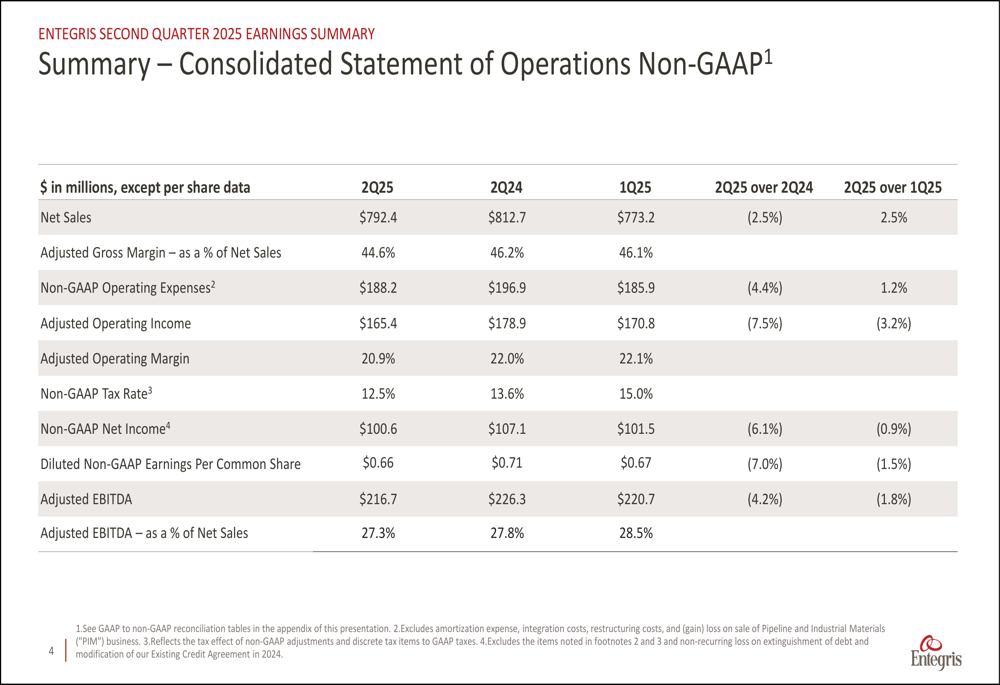

On a non-GAAP basis, the company’s adjusted operating income was $165.4 million with an operating margin of 20.9%, down from 22.0% in Q2 2024 and 22.1% in Q1 2025. Diluted non-GAAP earnings per share came in at $0.66, compared to $0.71 in the prior year period and $0.67 in the first quarter of 2025.

The detailed non-GAAP performance metrics reveal the ongoing margin pressure:

Segment Analysis

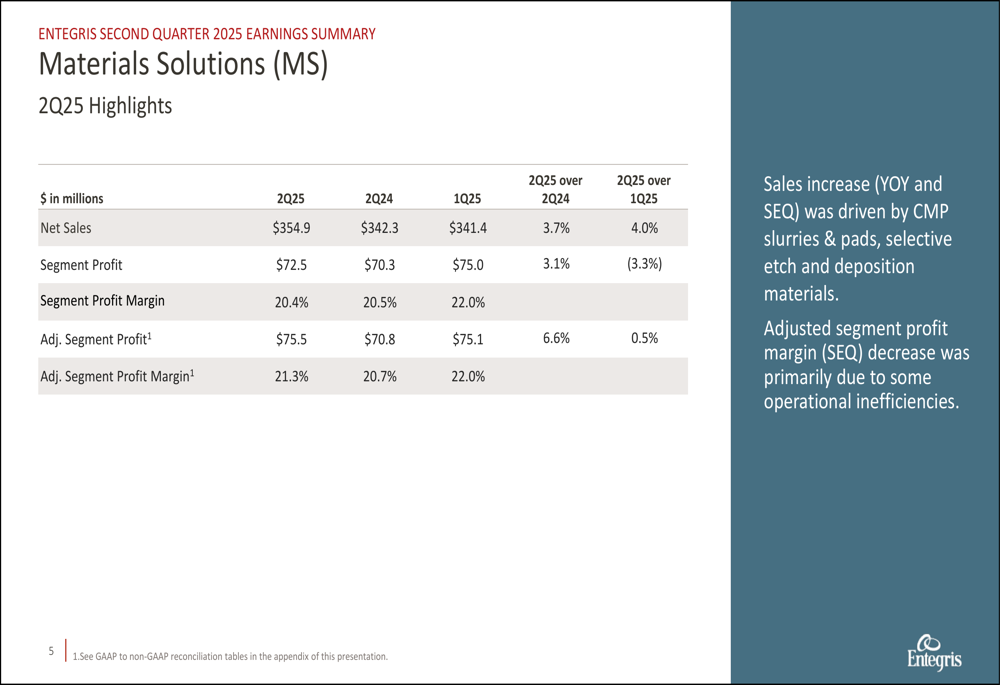

Entegris’ business segments showed divergent performance in the second quarter. The Materials Solutions (MS) segment demonstrated solid growth with sales of $354.9 million, up 3.7% year-over-year and 4.0% sequentially. This growth was primarily driven by CMP slurries & pads, selective etch, and deposition materials.

However, the segment’s adjusted profit margin declined to 21.3% from 22.0% in the previous quarter, which the company attributed to operational inefficiencies:

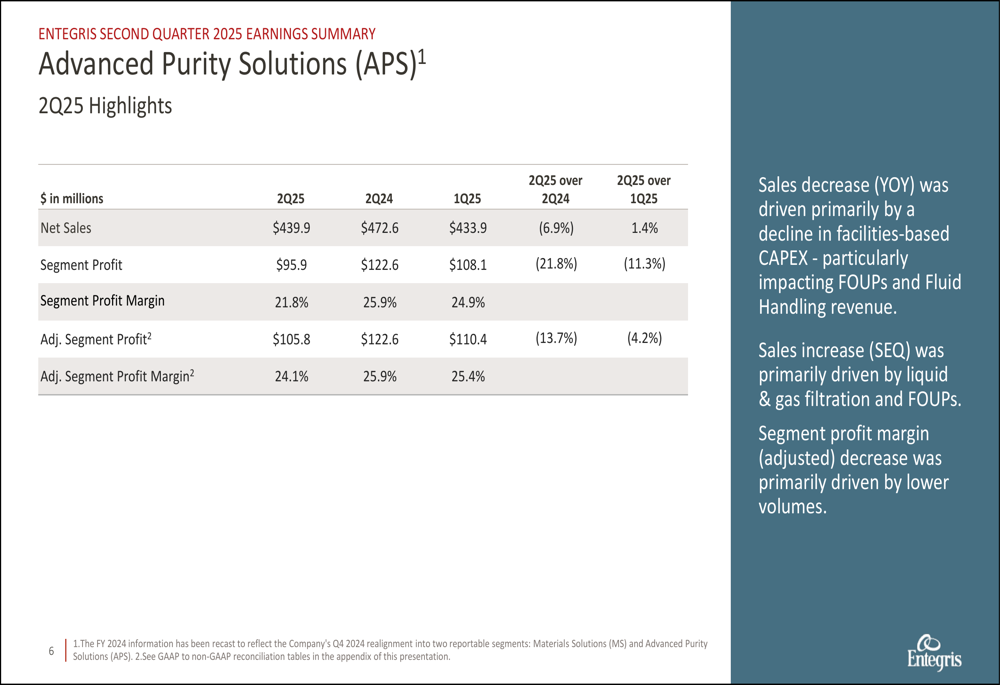

In contrast, the Advanced Purity Solutions (APS) segment continued to face headwinds with sales of $439.9 million, down 6.9% year-over-year but up slightly by 1.4% from the previous quarter. The decline was primarily due to reduced facilities-based capital expenditures, particularly affecting FOUP (Front Opening Unified Pod) and Fluid Handling revenue.

The APS segment’s adjusted profit margin also compressed to 24.1%, down from 25.9% in Q2 2024 and 25.4% in Q1 2025:

Balance Sheet and Cash Flow

Entegris ended the quarter with $376.8 million in cash and cash equivalents, an improvement from $320.0 million a year ago and $340.9 million at the end of Q1 2025. The company’s inventory levels increased to $694.6 million, up 9.7% year-over-year, potentially reflecting preparation for anticipated demand or supply chain adjustments.

The company generated $113.5 million in cash from operations during Q2 2025, slightly higher than the $111.2 million in the same period last year. Capital expenditures were $66.5 million, resulting in free cash flow of $47.0 million, down from $51.9 million in Q2 2024 but improved from $32.4 million in Q1 2025.

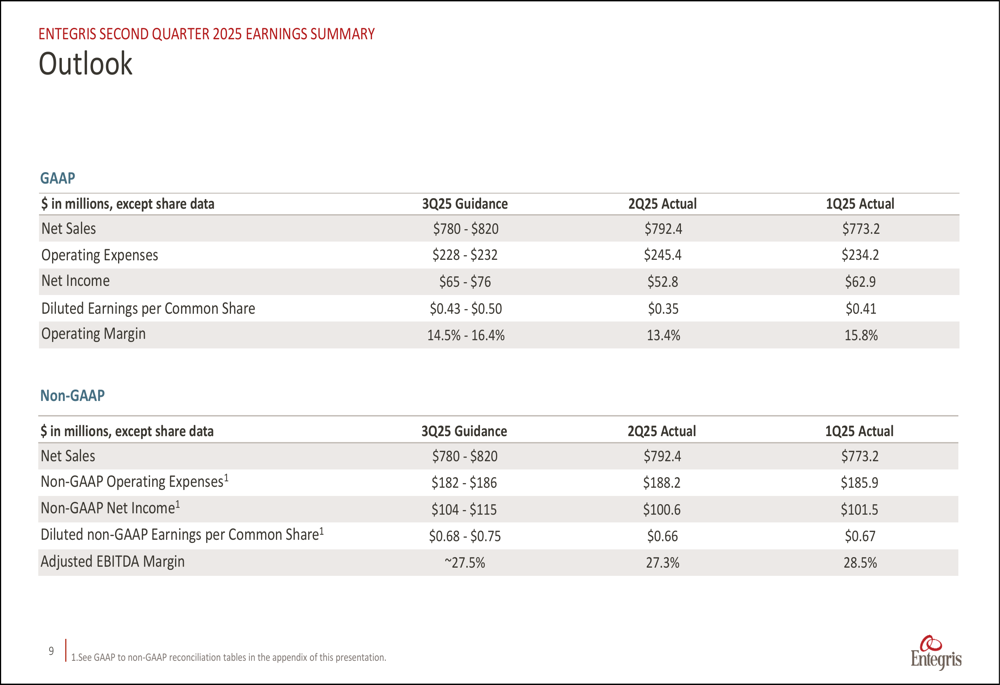

Outlook and Guidance

Looking ahead to the third quarter of 2025, Entegris provided guidance that suggests continued sequential improvement. The company expects net sales between $780 million and $820 million, which at the midpoint would represent a slight decrease from Q2 2025.

The company projects Q3 2025 GAAP earnings per share between $0.43 and $0.50, a potential improvement from the $0.35 reported in Q2. Non-GAAP earnings per share are expected to range from $0.68 to $0.75, which would be higher than the $0.66 reported for Q2 2025.

Adjusted EBITDA margin is forecasted at approximately 27.5%, a slight improvement from the 27.3% reported in Q2 2025, as shown in the following outlook table:

Market Reaction

The market response to Entegris’ Q2 2025 results was decidedly negative, with the stock falling 8.31% in premarket trading to $85.04. This decline follows a 13.14% drop after the company’s Q1 2025 results, indicating continued investor concern about Entegris’ performance and outlook.

The stock’s reaction suggests investors may be focusing on the year-over-year declines in revenue and margins rather than the sequential improvements. With the stock now trading significantly below its 52-week high of $119.95, market sentiment appears cautious about Entegris’ near-term prospects despite the company’s guidance suggesting modest improvement in the coming quarter.

Investors will likely be watching closely for signs that the company can reverse the margin compression trend and accelerate revenue growth in both business segments as the semiconductor industry continues to navigate through its current cycle.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.