Moody’s upgrades Agnico Eagle’s rating to A3 on debt reduction

Introduction & Market Context

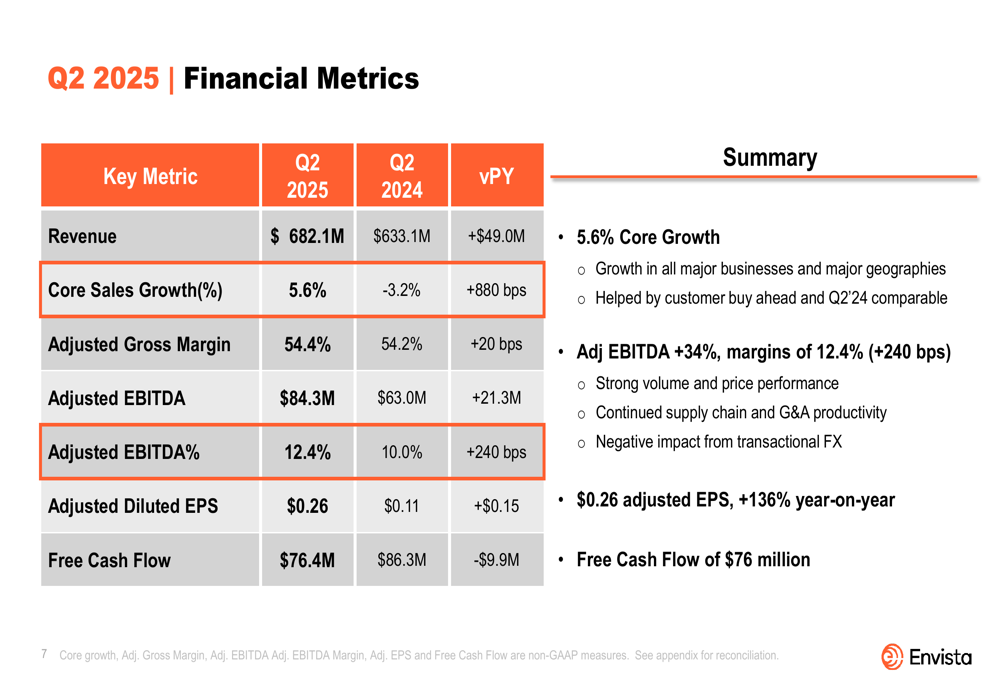

Envista Holdings (NYSE:NVST) presented its second-quarter 2025 results on July 31, showcasing accelerated growth and improved profitability metrics. The dental products company reported 5.6% core growth for Q2, a significant improvement from the 0.2% growth reported in the first quarter.

Despite the strong quarterly performance and raised full-year guidance, Envista’s stock declined 5.21% on the day of the presentation, closing at $19.96. This market reaction suggests investors may have had even higher expectations or concerns about growth sustainability in the current macroeconomic environment.

Quarterly Performance Highlights

Envista reported substantial improvements across key financial metrics for the second quarter of 2025. Revenue increased to $682.1 million, representing 7.7% reported growth and 5.6% core growth compared to Q2 2024. The company achieved an adjusted EBITDA margin of 12.4% and adjusted EPS of $0.26, marking a remarkable 136% increase year-over-year.

As shown in the following comprehensive financial overview for Q2 2025:

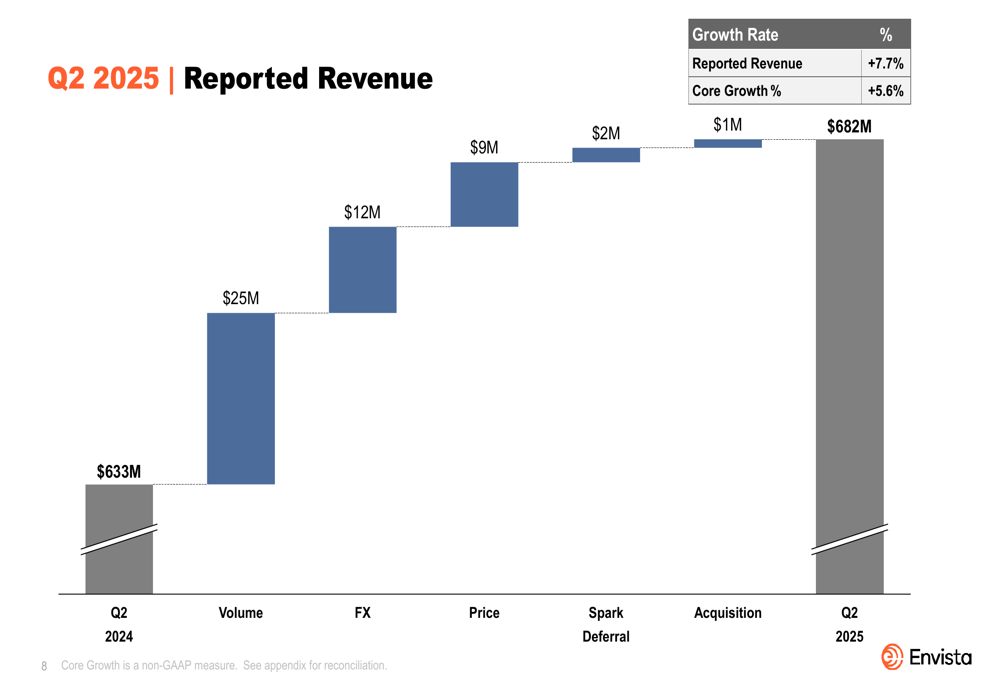

The revenue growth was driven by multiple factors, with volume contributing $25 million, favorable foreign exchange adding $12 million, and pricing actions generating $9 million. Additional contributions came from Spark Deferral ($2 million) and acquisitions ($1 million).

This breakdown of revenue growth drivers is illustrated in the following waterfall chart:

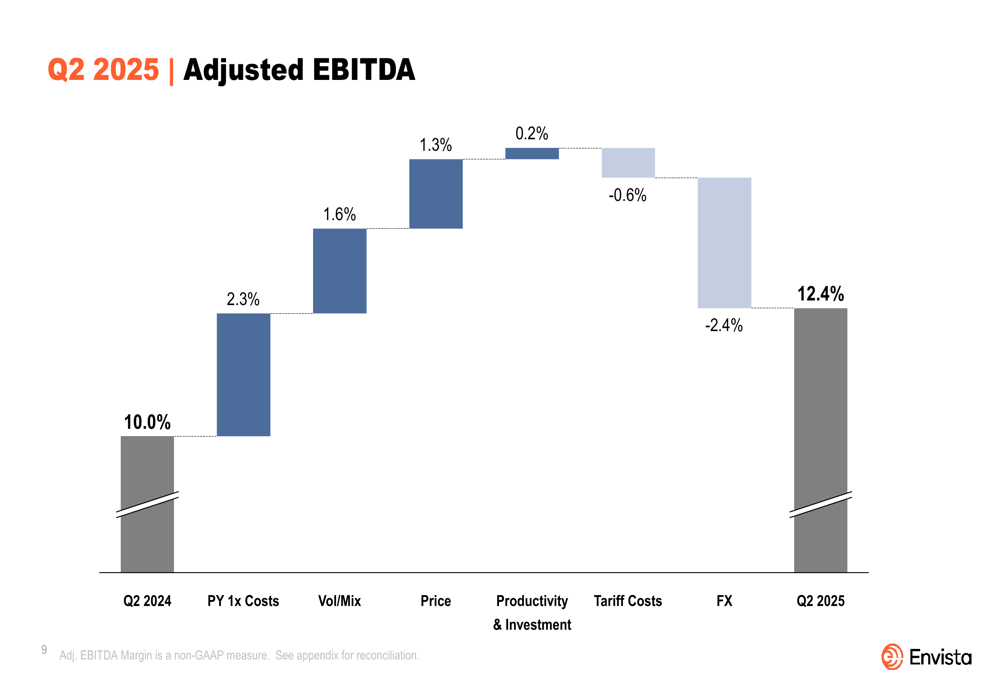

Adjusted EBITDA margin improved by 240 basis points year-over-year to 12.4%. This improvement was primarily driven by the absence of prior year one-time costs (+2.3%), favorable volume/mix (+1.6%), and pricing actions (+1.3%). These gains were partially offset by tariff costs (-0.6%) and foreign exchange impacts (-2.4%).

The following bridge chart details these factors affecting the adjusted EBITDA margin:

Segment Analysis

Both of Envista’s business segments contributed to the strong quarterly performance, with each showing solid revenue growth and margin expansion.

The Specialty Products & Technologies segment, which includes orthodontics and implant solutions, reported revenue of $445.1 million, representing 7.2% reported growth and 4.7% core growth. The adjusted operating margin for this segment improved significantly from 9.1% in Q2 2024 to 13.5% in Q2 2025. Management highlighted double-digit growth in Spark clear aligners and high-single-digit growth in brackets and wires, with premium products growing for the third consecutive quarter.

The Equipment & Consumables segment performed even better, with revenue of $237.0 million representing 8.7% reported growth and 7.3% core growth. The adjusted operating margin improved from 16.1% to 17.5% year-over-year. Consumables showed double-digit growth against softer prior-year comparables, while diagnostics grew at a low-single-digit rate globally.

Both segments experienced negative margin impacts from transactional foreign exchange losses, with approximately 200 basis points impact for Specialty Products & Technologies and 300 basis points for Equipment & Consumables.

Financial Position & Cash Flow

Envista generated $76.4 million in free cash flow during Q2 2025, compared to $86.3 million in the same period last year. For the first half of 2025, free cash flow totaled $71.3 million, down from $115.6 million in H1 2024.

The company maintained a strong balance sheet with a net debt to adjusted EBITDA ratio of approximately 1x. During the quarter, Envista repurchased 4.8 million shares, with year-to-date repurchases totaling $100 million. The company has a $250 million share repurchase authorization extending through December 2026.

Updated Guidance & Outlook

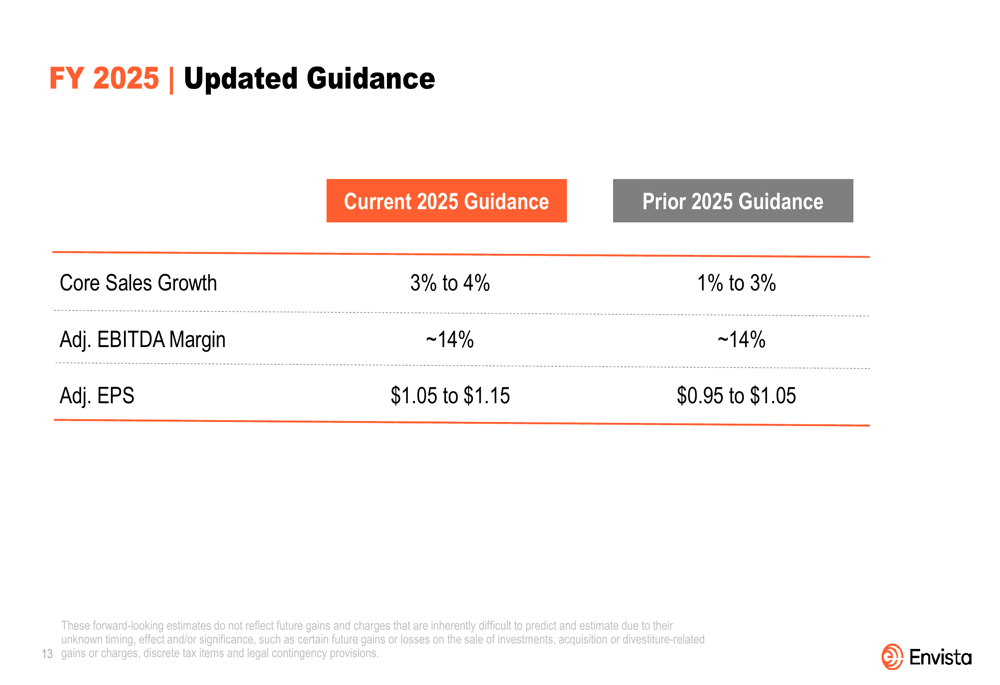

Based on the strong performance in the first half of the year, Envista raised its full-year 2025 guidance. The company now expects core sales growth of 3-4%, up from the previous guidance of 1-3%. Adjusted EPS guidance was also raised to $1.05-$1.15, compared to the previous range of $0.95-$1.05. The adjusted EBITDA margin guidance remained unchanged at approximately 14%.

The updated guidance compared to prior expectations is clearly presented in the following table:

Management noted that the dental market remains stable despite continuing macroeconomic uncertainties. They acknowledged that some of the Q2 growth was attributable to customers buying ahead of expected price increases and tariff impacts. The guidance assumes no significant improvement in market conditions during the second half of the year.

Other key assumptions underlying the updated guidance include:

- Exchange rates providing a revenue benefit of approximately 150 basis points year-over-year

- Tariff costs being offset by supply chain, pricing, and cost actions

- Spark Net Deferral Impact estimated at approximately $30 million

- An adjusted tax rate of approximately 33% for the full year

Strategic Initiatives

Envista continues to execute on its value creation plan, which focuses on growth, operational excellence, and people. The company reported a 5% increase in sales and marketing investment and a 14% increase in R&D spending to drive innovation.

Strategic highlights from the first half of 2025 included:

- Effective price capture in an inflationary environment

- Gains in the DSO (Dental Service Organizations) market, with DEXIS CBCT and DTX AI Implant Planning implemented in over 1,000 sites of a large DSO

- Expansion in emerging markets

- Two small acquisitions in the Specialty Products & Technologies segment

- Announced manufacturing expansion in China

- 15% decrease in G&A spending

- Customer service levels maintained above 95%

Investor Reaction & Market Perspective

Despite the strong quarterly results and raised guidance, Envista’s stock declined 5.21% on July 31, 2025, closing at $19.96. This negative market reaction contrasts with the 1.59% gain following the Q1 2025 earnings announcement, when the company reported much more modest growth of 0.2%.

The disconnect between improved performance and negative stock movement could be attributed to several factors:

- Concerns about the sustainability of growth, particularly given management’s acknowledgment that some Q2 growth was due to customers buying ahead of price and tariff impacts

- Ongoing macroeconomic uncertainties affecting the dental market

- The significant foreign exchange impacts on margins, which could persist

- Potential investor expectations for even stronger results or guidance given the stock’s valuation

With a current market capitalization of approximately $2.78 billion and trading within its 52-week range of $14.22 to $23.00, Envista continues to navigate a challenging market environment while demonstrating improved operational performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.